China spent $120B to lock down critical minerals overseas: report

China has invested more than $120 billion in overseas mining and upstream processing since 2023, accelerating a state-backed push to secure the raw materials underpinning the global energy transition, says Australian think tank Climate Energy Finance (CEF).

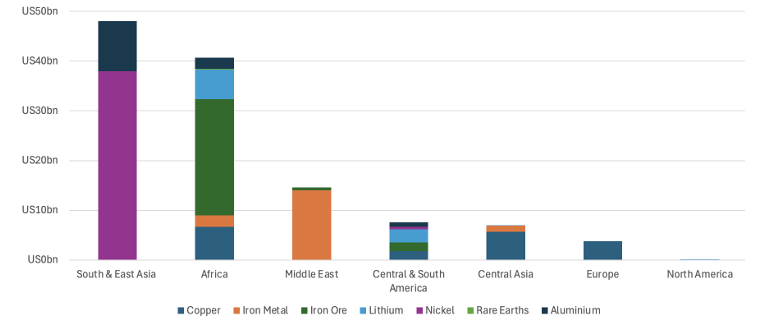

A study published last week reveals that China’s spending targeted a wide range of commodities — including lithium, copper, nickel, rare earths and bauxite — that are essential for electric vehicles, renewable power and industrial decarbonization.

The scale of the push reflects what the authors describe as a coordinated strategy of “green energy statecraft,” in which Beijing is working to dominate not just resource extraction, but the full value chain that turns raw materials into battery-grade and industrial inputs.

Vertical integration at scale

The CEF research also finds that China’s outbound investment in mining is only one piece of a much larger industrial strategy.

Since early 2023, Chinese firms have also deployed more than $220 billion into downstream sectors such as battery manufacturing, electric vehicles, grids, solar and wind infrastructure, creating what researchers describe as a vertically integrated global cleantech expansion.

Together, upstream resource investments and downstream manufacturing form a unified system designed to secure supply, reduce dependence on foreign inputs and reinforce China’s position at the center of the low-carbon economy.

That dominance is already evident. According to CEF estimates, China now controls about 90% of global rare earth refining, roughly 60% of lithium processing, more than 70% of cobalt refining and over half of global steel production. It also produces more than 90% of battery cathode and anode materials.

Africa and the Global South in focus

Much of China’s recent mining investment has flowed into resource-rich regions across Africa, Latin America and Southeast Asia.

In the Democratic Republic of Congo, Chinese companies have expanded their hold over copper and cobalt production, while in Indonesia, Chinese-backed investment has helped transform the country into the world’s largest nickel producer and processor.

Zimbabwe and other African nations have also seen rapid development of lithium mining and processing capacity backed by Chinese capital.

But the model has evolved. CEF analysis shows that Beijing is shifting away from the earlier Belt and Road approach — often criticized as extractive — toward a more collaborative framework.

Chinese firms are increasingly partnering with host governments to build in-country processing facilities, infrastructure such as railways, ports and power systems, and local industrial capacity, in exchange for long-term supply agreements, says CEF founder Tim Buckley, who co-authored the report.

This approach aligns China’s resource security goals with host countries’ ambitions to capture more value domestically and accelerate their own industrial development, he adds.

Supply chain control — and risk

China’s strategy is not just about access to raw materials, but about consolidating control over the entire supply chain.

By combining mining, processing and manufacturing, Beijing is strengthening its ability to influence pricing, availability and technology pathways in critical minerals markets, the CEF report notes, emphasizing that the trajectory remains one of expansion, not retreat, as China adapts its strategy to changing political and economic conditions.

Meanwhile, China’s growing market power is raising concerns among Western governments and industry players, who see growing risks to supply chain security and geopolitical stability.

Efforts to counterbalance China’s position are gaining momentum. Initiatives such as the US-led Minerals Security Partnership and the European Union’s Critical Raw Materials Act aim to diversify supply sources and rebuild domestic processing capacity.

A defining advantage

Still, replicating China’s scale and integration would take years.

As highlighted by CEF, China’s dominance is underpinned by a hybrid model that combines state direction with the speed and execution of private enterprise, supported by large-scale financing from state-backed institutions. For resource-rich nations, though, that model presents both risks and opportunities.

While dependence on a single dominant player raises strategic concerns, access to Chinese capital and technical expertise is also enabling faster development of mining, processing and infrastructure projects — particularly in emerging economies, the authors say.

Could This Be China’s Strategy To Paralyze the Pentagon?

Long before trade wars and tariffs, China secured manufacturing dominance by controlling rare earths - a reality so consequential that the United States and its allies are now pledging more than $8.5 billion just to claw back some control of the supply chain.

As global manufacturing expanded over the past two decades, rare earth processing was steadily pushed out of Western supply chains. It was capital-intensive, technically demanding, and difficult to defend on short-term economics.

China made the opposite choice, keeping those capabilities in place and methodically expanding them as others exited.

“China didn’t win this by mining. It won by building the entire system–separation, refining, metals, magnets–all connected. Everyone else walked away from it. At that point, control wasn’t up for debate anymore,” REalloys (NASDAQ: ALOY) CEO Lipi Sternheim said. “North America lost control, and the reality is simple: factories don’t run on ore. They run on metals and alloys and at this moment in time our company is the only one able to actually refine heavy metals and magnets. Our competitors, no matter how well funded they are, are at least 3 years away from production”

By the time rare earths became strategically visible, the infrastructure that determined who could actually build was already concentrated in one place. Then it was weaponized, with Beijing placing restrictions on rare earth exports in order to control which defense and advanced manufacturing programs received supply.

“That loss of end-to-end rare earth capability outside China is exactly what REAlloys was built to close,” Sternheim said.

And things are moving quickly, in tandem with the U.S. Department of Defense’s eye on the critical metal prize: domestic processing.

REalloys Inc. (NASDAQ: ALOY) has addressed the rare earth bottleneck that has constrained Western manufacturing for decades by reestablishing domestic conversion capacity, turning separated material into metals and alloys inside North America through its partnership with the Saskatchewan Research Council (SRC). Now, it’s the only North American company with North American supply from a heavy rare earth refinery.

With that conversion capacity in place, REalloys has moved to lock in feedstock, including a long-term offtake agreement tied to Kazakhstan.

Through a long-term non-binding offtake agreement with AltynGroup, REAlloys will pull rare earth feedstock out of Kazakhstan and route it straight into its North American metallization and alloying system. The material does not leave the chain as concentrate.

Oxides and concentrates don’t power anything. Metals and alloys do.

Until rare earths are converted into metal and alloy form, they cannot be used in motors, magnets, or weapons systems. That conversion step is where control has been lost for decades — and where most Western supply chains break.

By routing material all the way through to metals and alloys inside the United States, REAlloys is solving the part of the problem that cannot be fixed later, substituted, or rushed in a crisis.

The feedstock is tied to AltynGroup’s Kokbulak project, where rare earth-bearing material is recovered from an existing iron ore operation. The concentrate includes both light and heavy rare earths, including dysprosium and terbium.

North America has handled foreign rare earth material before, but almost always handed it back offshore before it reached metal or alloy form. This arrangement is built to stop that handoff. Material enters the chain and stays in the chain until it becomes defense-grade output.

This is not future capacity. The Kazakhstan feedstock will be routed into a system that is already running.

REalloys (NASDAQ: ALOY) operates the only facility in North America capable of converting rare earths through metallization and alloying at scale, including heavy rare earth elements.

That capability sits at its Euclid, Ohio site, where rare earth metals and alloys are already being produced for U.S. government customers.

This is the step in the chain where rare earths become usable for defense systems, motors, and high-performance magnets– and it is the step the West no longer controls. With new U.S. rules taking effect in 2027 restricting the use of Chinese rare earths in defense and federally backed manufacturing, existing domestic conversion capacity is becoming more relevant by the quarter.

There is no parallel facility in North America handling heavy rare earth conversion at this level. Building one is not a short-term exercise. Processing, metallization, and alloy qualification take years to permit, finance, construct, and qualify with defense customers. Even under accelerated timelines, meaningful competition is measured in half-decades, not quarters.

REalloys has assembled that capability into a single operating system.

Kazakhstan provides scale-ready feedstock. Hoidas Lake in Saskatchewan adds a second upstream source. The partnership with the Saskatchewan Research Council anchors midstream processing. Euclid closes the loop by turning material into defense-grade metals and alloys. This is not a collection of projects moving independently. It is a single conversion system designed to keep material inside Western control all the way to finished output.

The U.S. government is now saying out loud what defense planners have been warning about privately for years.

This week, Washington convened talks with allied and partner countries explicitly aimed at weakening China’s grip over critical minerals supply chains. The issue has moved out of the realm of industrial competition and into national security planning, at a point where there is almost no buffer left.

China has already used rare earth controls to cut off specific military and industrial customers.

In late 2025, Beijing imposed an explicit ban on exports of certain rare earth materials and processing technologies for military use, blocking shipments tied to defense and weapons manufacturing. The restrictions were not broad trade measures. They were targeted at materials and know-how required for guidance systems, magnets, and advanced electronics used by foreign militaries.

Japan has been on the receiving end as well.

Chinese authorities have recently tightened export controls and licensing around rare earths and related materials amid renewed political friction with Tokyo, reviving a playbook Japan knows well. In 2010, China abruptly curtailed rare earth exports to Japan during a diplomatic dispute, disrupting automotive and electronics supply chains and forcing emergency stockpiling.

The Pentagon has already crossed the line from concern to intervention.

Complementing DoD’s downstream focus, the U.S. government is launching a $12 billion strategic critical-minerals stockpile that will include rare earths, lithium, nickel, cobalt, and other essential elements. The initiative aims to reduce U.S. dependence on China and ensure material availability for defense, advanced manufacturing, and technology sectors by acquiring and holding key feedstocks and intermediates.

Using Defense Production Act authorities and direct financing, it has pushed capital into domestic rare earth processing and magnet production, including MP Materials (NASDAQ: MP), to keep U.S. weapons programs from remaining hostage to Chinese-controlled metals. Using Defense Production Act authorities and direct financing, it has pushed capital downstream into domestic rare earth processing and magnet materials to keep U.S. weapons programs from remaining dependent on Chinese-controlled metals.

The urgency extends across the entire defense industrial base. Major contractors, including Boeing (NYSE: BA), Northrop Grumman (NYSE: NOC), and General Dynamics (NYSE: GD) rely on rare earth-derived magnets and alloys across nearly every advanced platform—from stealth bombers and ballistic missile submarines to rotorcraft and maritime patrol aircraft. Without a domestic conversion layer, their supply chains run through Beijing.

Government action is still moving through policy channels and legacy projects, while REAlloys is already producing rare earth metals and alloys inside the United States–the layer the Department of Defense now treats as critical.

REalloys is right at the downstream choke point. The hardest part of the supply chain is already built, demand is real, and the barriers to entry are high.

By. Josh Owens

No comments:

Post a Comment