It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Saturday, May 16, 2026

Canada’s Economy Caught Between Oil Windfalls and Trade Wars

The Bank of Canada says Middle East geopolitical tensions and U.S. trade risks are now the biggest threats to Canada’s economy, replacing tariffs as the top concern.

High oil prices are boosting Canadian exports, government revenues, and the trade balance, but are also fueling inflation and raising the risk of higher interest rates.

Uncertainty around the future of United States-Mexico-Canada Agreement and potential new U.S. tariffs could slow growth and even push Canada into recession if trade relations worsen.

A recent Bank of CanadaMarket Participants Survey has flagged geopolitical and trade tensions as the biggest risks facing the Canadian economy. Leading the downside are geopolitical risks led by the Middle East war, with 82% of respondents identifying it as the biggest risk, while 79% and 57% of respondents picked growing trade tensions and tightening global financial conditions, respectively. The shift from trade tensions dominating headline risks to Canada’s economy amid Trump tariffs is largely attributed to the Iran war, which has disrupted global supply chains and impacted the shipping of oil, gas, and fertilizer through the Strait of Hormuz.

Governor Tiff Macklem has warned that persistent high energy prices resulting from these conflicts could necessitateinterest rate hikes to maintain the 2% inflation target. However, like many oil producers, Canada is also experiencing an "oil paradox" with high oil prices driving up domestic fuel costs and inflation while simultaneously generating significant government revenue windfalls.

Canada posted its first trade surplus in six months, with the country’s merchandise trade balance swinging to a $1.78 billion surplus in March against expectations of a shortfall of $2.88 billion, while total exports rose 8.5% to $72.8 billion, the second-highest level on record. Energy exports surged 15.6% to $17.1 billion, the highest level since September 2022, helped by a 18.9 % jump in crude oil exports thanks to a 33.1% spike in prices. Exports of metal products increased 24.0% to a record $15.3 billion, led by a $3 billion rise in gold exports thanks to a surge in safe-haven demand. Meanwhile, total imports fell 1.6% to $71.0 billion, driven by lower volumes of consumer goods, pharmaceuticals, and aircraft.

That said, trade tensions between Canada and the United States remain a major headwind, with 82% of respondents saying easing of the tensions is the leading upside risk to Canada’s economy. That’s significantly higher than 57% of respondents who identified a larger-than-expected fiscal stimulus as the top upside or 43% who listed decreasing geopolitical risks and higher commodity prices.

Currently, there’s plenty of uncertainty surrounding the review of CUSMA (USMCA). CUSMA is a trade agreement between Canada, the United States and Mexico that came into effect on July 1, 2020 during Trump’s first term, replacing the 26-year-old NAFTA. The agreement requires, among other things, that 75% of automobile components to be manufactured in North America to qualify for zero tariffs, aiming to boost regional production. The Trump administration is required to outline its new position by July 1; however, negotiations are likely to drag into the fall, influenced by U.S. midterm election politics. While a 16-year extension is the base case, there is a risk of a severely fragmented scenario where the U.S. imposes up to 35% tariffs on all Canadian exports, potentially inducing a Canadian recession. Further, there are reports that the White House is considering splitting the agreement into separate bilateral deals rather than maintaining it as a single trilateral agreement.

Canada is already doing much less business with its northern neighbor, with the U.S. accounting for just 66.7% of total exports in March, the lowest level ever, in large part due to Trump’s tariffs. Canada’strade surplus with the United States widened to $7.1 billion in March, its highest level since September 2025, largely driven by a 8.3% increase in shipments of passenger cars and light trucks to $48.51 billion. In contrast, imports from the U.S. dropped by 1.2% to $41.44 billion.

The Trump administration has imposed significant tariffs on Canadian goods, including a 50% tariff imposed on Canadian steel and aluminum; 35.2% combined anti-dumping and countervailing duties on soft lumber, 25% tariffs on auto exports and 50% tariffs on copper and copper products, among other levies. Canada initially announced reciprocal, dollar-for-dollar tariffs on $30 billion worth of U.S. goods but removed many of them in September 2025 after some U.S. exemptions. However, it still maintains retaliatory tariffs on specific U.S. steel, aluminum and auto products.

The results of the survey came just two weeks after Canada’s federal Finance Minister François-Philippe Champagne tabled thespring economic update, which revealed that Canada’s GDP growth is projected to slow down to 1.1% in 2026, down from 1.7% in 2025. However, the economy is expected to perk up again, growing 1.9% in 2027. Canada's deficit for FY 25/26 was reduced by $11.5 billion to $66.9 billion (2.1% of GDP), thanks in large part to higher oil revenues.

Last month, Canada unveiled the Canada Strong Fund, its first ever sovereign wealth fund. The federal government has pledged to seed the fund with $25 billion over three years on a cash basis. CSF will focus on achieving market-rate commercial returns by investing alongside private capital in strategic sectors. The investments will target nation-building projects in both clean energy and fossil fuels, transportation infrastructure, telecommunications, advanced manufacturing and critical minerals. However, the sovereign wealth fund’s unique feature is a planned retail investment product that will allow individual Canadians to directly invest their own money into the fund and share in the financial returns.

The Canadian federal government may reconsider a plan to privatize the Trans Mountain oil pipeline.

Since the expanded TMX pipeline launched in 2024, exports to Asia—especially China—have surged, with up to 70% of shipments from British Columbia heading to Asian buyers by late 2025.

Officials now see TMX as a highly profitable “strategically important asset,” with potential for further expansion

The Canadian federal government may reconsider a plan to privatize the Trans Mountain oil pipeline and keep it state-owned amid a surge in appetite for Canadian crude to replace lost Middle Eastern barrels.

“The prior narrative had been that this should be returning to private hands,” the head of the government entity that owns Trans Mountain said at an event this week, as quoted by the Financial Post. “That was in a different market and that was in a different time,” Elizabeth Wademan also said.

Indeed, this is a very different market from what it was when the government in Ottawa had to step in and buy Trans Mountain from Kinder Morgan, which quit the project under relentless pressure from climate activists who used environmental regulations to strangle the expansion project. The price tag for the nationalization deal, which took place in 2018, was about $3.3 billion, and the Trudeau government quickly signaled it would start looking for buyers as soon as possible.

By 2024, the cost of the pipeline expansion project had swelled to about $23 billion, but the project, somewhat surprisingly, was completed, and the expanded pipeline launched in May of that year, running at three times its original capacity or a total of 890,000 barrels daily.

The destination for these barrels was the vast Asian market, as a way to diversify away from the U.S., which has for decades been pretty much the only foreign market for Canadian crude—and an export conduit, with the oil transported from Canada to the U.S. Gulf Coast, and from there, to markets overseas. With the new TMX, Canadian crude producers got a new, more convenient channel to Asian energy buyers.

It did not take long for the effect to be felt: between the launch of the expanded pipe and spring 2025, the average flow rates for shipment to China reached 207,000 barrels daily. That compares with an average of 173,000 barrels daily pumped to the United States. Since spring, the shift has become even more marked. By October 2025, as much as 70% of Canadian crude exported from the British Columbia coast was going to China. Now, everyone else in Asia is also interested.

The Trans Mountain pipeline is a “strategically important asset”, Trans Mountain Corp.’s Wademan said this week, suggesting the project could be expanded further, with more “energy corridors” that would add value for Canadians, the Financial Post reported.

“Let’s look where we are, and look how important energy security is, and look how incredibly profitable this asset is; there’s a lot,” Wademan said. “There’s a lot of merit to holding onto it and realizing that full value.”

Indeed, it would be profitable for the federal government to hold on to the infrastructure as the price of Canadian crude inches closer to $90 per barrel—a level hardly seen as possible just five years ago, and even more recently. TMX has turned into a game-changer for the Canadian oil industry and it will be in the center of the “golden opportunity” that Canada has to become a bigger global player in both oil and gas.

Canada has a “golden opportunity” to become a major global oil player as the war in the Middle East limits sources of crude and natural gas, the head of the International Energy Agency, Fatih Birol, said earlier this month, adding that “The cost of missing this train will be incredible.” It seems the Canadian government is acutely aware of that risk and plans to avoid it and make the best of the country’s resources in a fascinating departure from the previous government’s focus on emission reduction and alternative energy.

By Charles Kennedy for Oilprice.com

UK Moves to Ban New North Sea Oil and Gas Licences Permanently

The UK government will introduce legislation banning new North Sea oil and gas exploration licences as part of its Energy Independence Bill.

Critics argue the policy will increase Britain’s reliance on imported fossil fuels while damaging Scotland’s oil and gas industry.

Rising oil prices and disruptions tied to the Iran conflict have intensified political pressure on Labour to reconsider the ban.

The government will make it illegal to grant new oil and gas licences in the North Sea, the King said at the state opening of Parliament, in a sign ministers are refusing to buckle in the face of a barrage of criticism that the policy is depriving the UK of billions of pounds in tax receipts without helping the environment.

As part of an Energy Independence Bill announced in the King’s Speech, the government will bake into law its pre-election pledge not to explore new oil and gas fields in a bid to “take control of our energy security”.

In its 2024 manifesto, the Labour Party made a ban on all new exploration and drilling licences in the North Sea a key pillar of its promise to turn Britain into a “clean energy superpower” by 2030.

But since entering government, the party has come under growing pressure to renege on the promise, with critics arguing it strangles one of Scotland’s most vibrant industries and fails to improve the UK’s environmental footprint.

Backlash against ‘deluded’ North Sea policy

Oil and gas still accounts for three-quarters of the UK’s energy mix. And the majority of those fossil fuels are now shipped in from abroad, meaning other economies benefit from the job creation and tax receipts that are derived from the lucrative drilling and refining processes.

Calls for the ministers to rethink the ban have grown louder since the outbreak of war in Iran led the price of crude oil to nearly double in a month. Last week, Norway, which drills for oil in the same area of the North Sea as Britain, approved plans to reopen three gasfields that had been shut for decades to help sate the global demand for fossil fuels caused by the closure of the Strait of Hormuz shipping lane.

Two of Labour’s main political opponents – Reform UK and the Conservatives – have both vowed to overturn the ban, in a move they say would help increase the UK’s tax take and inoculate it from any acute supply shocks.

The ban, which the government claims will help Britain off the “roller-coaster of fossil fuel markets”, has also drawn criticism from the US’s ambassador to the UK, who has used multiple interviews to urge Britain to make more of its reserves.

Shadow energy secretary Claire Coutinho accused her opposite number Ed Miliband of being “utterly deluded” for seeking to put the ban into the statute book.

“He is not making us more independent. He is making us more reliant on foreign imports,” she said.

South Africa has regained competitiveness in mining because of partnerships between the public and private sector to tackle regulatory issues and structural bottlenecks, according to billionaire Patrice Motsepe.

Policy uncertainty together with vandalism, power outages and logistics bottlenecks have weighed on South Africa’s mining industry for more than a decade. President Cyril Ramaphosa’s government partnered with business groups including B4SA to address the nation’s sub-standard transport and energy infrastructure and operations.

“They’ve done very well over the last few years in ensuring” South Africa becomes a destination for investments, Motsepe said at the sidelines of a conference in Kenya’s capital, Nairobi. “Part of what should take place in those partnerships is for the CEOs of the mining industry to keep telling the government what are the changes, the improvements and the areas that will ensure that South Africa is a globally competitive destination.”

The end of rotational blackouts and improvement in transport logistics have put South Africa in a better place to capitalize on higher commodity prices. Johannesburg’s industrial metals and mining gauge has climbed 30% this year, compared with just a 2.4% increase in the benchmark FTSE/JSE All Share Index.

Still, South Africa’s investment in mineral exploration dropped for a seventh straight year, despite the government’s ambitions to arrest the decline.

Exploration spending in South Africa fell 5.3% to 738 million rand ($44.8 million) in 2025, according to data published in March by the government’s statistics agency using 2015 constant prices. Investment in prospecting has slumped more than 85% in the past three decades, the data show.

Motsepe, South Africa’s wealthiest Black person who made his fortune in gold mining in the 1990s and 2000s, said his company plans to invest several billion dollars in the country’s mining sector, without providing any time line.

His African Rainbow Minerals Ltd. has interests in coal, iron ore and platinum group metals. The firm also owns 10% of Harmony Gold Mining Co., a top producer of the precious metal in his home nation.

Motsepe is the South African president’s brother-in-law.

(By Prinesha Naidoo and Jennifer Zabasajja)

Zambia eases ban on sulphuric acid exports to Congo as stocks recover

Zambia has cleared two copper producers to resume sulphuric acid exports to Democratic Republic of Congo, according to the country’s trade minister, as the country eased curbs on the mining input.

Smelters in Zambia – Africa’s No.2 producer of copper – generate about 2 million metric tons of sulphuric acid a year, mostly as a byproduct used by local mines. Any surplus is shipped to neighboring Congo.

In the central African copperbelt, sulphuric acid is used to extract cobalt and copper, in demand for the green energy transition, from oxide ores.

Zambia banned sulphuric acid exports in September followed by a permit policy in March after weak domestic output and global disruptions linked to the Iran war tightened the supply of leaching chemicals.

In response, miners in Congo, the world’s biggest cobalt producer and No. 2 in copper, cut usage and considered output reductions.

However, Zambia’s Commerce, Trade and Industry Minister Chipoka Mulenga told Reuters on Thursday that the government has authorized Chambishi Copper Smelter and Mopani Copper Mines to resume sulphuric acid shipments after local stocks recovered.

They will export a “limited quantity to ensure the local market does not suffer,” Mulenga said, without specifying volumes.

The minister said Zambia could widen export permissions if supply conditions continue to improve.

A document seen by Reuters showed the ministry has also authorized chemicals trader Alliswell Investment Limited to ship 5,000 metric tons of sulphuric acid.

An industry source, speaking on condition of anonymity because of the sensitivity of the issue, said Mopani had yet to receive its export permit.

Neither Mopani, Chambishi Copper Smelter nor Alliswell responded to requests for comment.

Congo chemicals imports declined

Congo’s imports of processing chemicals fell sharply in the first quarter, data from commodities logistics and warehousing group Access World showed.

Mulenga said the resumption of exports reflected improved availability. “We allowed them to export because local stocks have risen and these companies have [miners] that they need to supply in Congo.”

Mopani will supply Glencore, while CCS will export through three Chinese mines in Congo, Mulenga added, without naming the firms.

Glencore declined to comment.

(By Chris Mfula and Maxwell Akalaare Adombila; Editing by Barbara Lewis)

Larvotto Resources reports recoverable antimony, gold from tailings at Hillgrove

Hillgrove project is located 23 km east of Armidale in northern New South Wales. Credit: Larvotto Resources

Larvotto Resources (ASX: LRV) said Thursday results from its initial metallurgical flotation testwork on material from tailings storage facility 1 (TSF1) at its 100%-owned Hillgrove antimony-gold project in New South Wales.

Initial flotation testwork on TSF1 tailings achieved 80–95% antimony and 40–75% gold recoveries, the company said.

The results confirm that residual antimony and gold within the approximately 1.4 million tonne legacy tailings facility are recoverable using the same conventional flotation methods being deployed in the Hillgrove plant, scheduled to commence production in August 2026.

TSF1 was used to store tailings produced over an ~20-year period from a plant designed for the recovery of antimony. As such, the TSF1 material contains significant quantities of gold and tungsten, in addition to minor antimony.

“These results are a genuine milestone for Hillgrove. The testwork confirms that the legacy tailings contain commercially meaningful grades of antimony and gold, and that they respond well to the same flotation methods we are deploying in the upgraded plant,” managing director Ron Heeks said in a news release.

“The pathway is becoming very clear; reprocess the tailings, recover the metals, and simultaneously rehabilitate a facility that sits adjacent to a 500-metre gorge,” Heeks said.

“That environmental outcome matters both to the project and to the broader community. We are now moving quickly through the cleaner flotation work and resource estimation process.”

Last year, the company reported 90% tungsten recovery with a 16X increase in feed grade delivered in metallurgical testwork, which it said also indicates a simple and cost-effective processing circuit would produce a saleable tungsten concentrate.

The global copper market enjoyed one of its best years in 2025. The threat of US tariffs on the industrial metal and its elevated status as a critical mineral, together with major supply disruptions globally, all played a part to help to lift prices 40% last year.

That run extended into 2026, as expectations of surging AI-driven demand and persistent supply constraints drove prices to a record of $14,500 a tonne in January. This week, copper is nearing another record.

The prospect of higher mining costs due to rising energy prices and a shortage of sulfuric acid, which is used in a fifth of the global copper production, is considered the next big catalyst for copper prices, a Sprott analyst recently said.

Goldman Sachs is also optimistic of copper surging higher again, due to the supply-side disruptions. The International Copper Study Group recently outright abandoned its previous surplus projections, now forecasting a 150,000-tonne deficit for 2026.

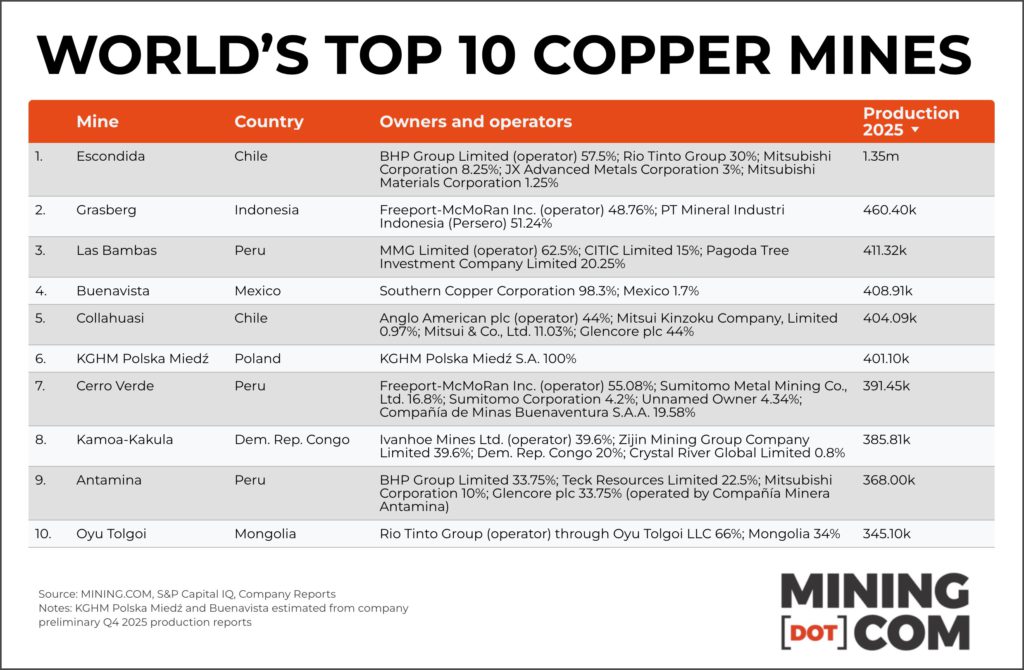

The top 10 mines, many of which have been in production for decades (some even trace roots back to the late 1800s) are responsible for more than a fifth of total global mined production – producing 4.9 million tonnes in 2025.

And surprisingly, after only recently being surpassed by BHP as the world’s number one copper producer on an attributable basis, Chile’s state owned Codelco does not have any of its operations qualify for the top 10.

As last year amply showed disruption at these giant operations (like the Grasberg and Kamoa-Kakula accidents that saw 100s of thousands of tonnes taken off the market,) can have a big impact on copper prices.

1. Escondida

Escondida in Chile, a joint venture between BHP, Rio Tinto, Mitsubishi, and JX Advanced Metals holds the top spot, producing 1,347.6 kts of copper metal in 2025. Escondida has long ranked the world’s biggest copper mine, but BHP’s operational review for the nine months to March 31 pointed to record material mined and concentrator throughput.

Las Bambas mine in Peru, owned jointly by China’s MMG, CITIC and Pagoda Tree Investment Company, churned out 411.3 kts in 2025. The mine was plagued by protests in 2024, but protesters agreed to lift a road blockade on a key Peruvian transport route, and operations resumed in April 2025.

4. Buenavista

Southern Copper’s Buenavista mine in Mexico moves up in this year’s ranking to fourth place with 409.4 kts produced. Copper has been mined at the historic site, 22 miles south of the US border, since 1899.

5. Collahuasi

Chile’s Collahuasi mine, a joint venture between Glencore, Anglo American and Mitsui produced produced 404.1 kts. In April this year, contractors finished building a system that will carry water from the coastal town of Punta Patache to the Ujina deposit, more than 4,400 meters above sea level, as part of a $1 billion infrastructure improvement project.

Cerro Verde in Peru, a joint venture between Freeport-McMohRan, Sumitomo and Buenaventura takes seventh place, producing 391.5 kts. The Peruvian government first mined Cerro Verde’s oxide ores and built one of the world’s first SX/EW facilities in 1972.

8. Kamoa-Kakula

The Kamoa-Kakula complex in the Democratic Republic of Congo, owned jointly by Ivanhoe Mines, Zijin Mining, Crystal River and the DRC government drops from third place last year to seventh — it produced 385.8 kts. Ivanhoe halted operations for three weeks in 2025 after seismic activity severely flooded the underground mine. In April, Ivanhoe slashed near-term production guidance, citing a shift toward underground development, rehabilitation and access work that will constrain ore delivery over the next 18 to 24 months.

9. Antamina

Antamina in Peru, co-owned by BHP, Glencore, Teck and Mitsubishi, moves up to ninth from 10th place, producing 368 kts. Last year, Antamina’s operators forecasted an almost 20% boost in cooper output.

10. Oyu Tolgoi

Oyu Tolgoi, a joint venture between Rio Tinto and the Mongolian government, churned out 345.1 kts. The government, which holds a 34% stake through state-owned Erdenes Mongol LLC., this year demanded earlier profit payments and a larger share of revenue, reopening negotiations over the $18-billion project’s commercial terms.

Honorable mentions: Morenci in Arizona, USA (313,100 tonnes), Quellaveco in Peru (309,900 tonnes), Los Pelambres in Chile (295,400 tonnes)

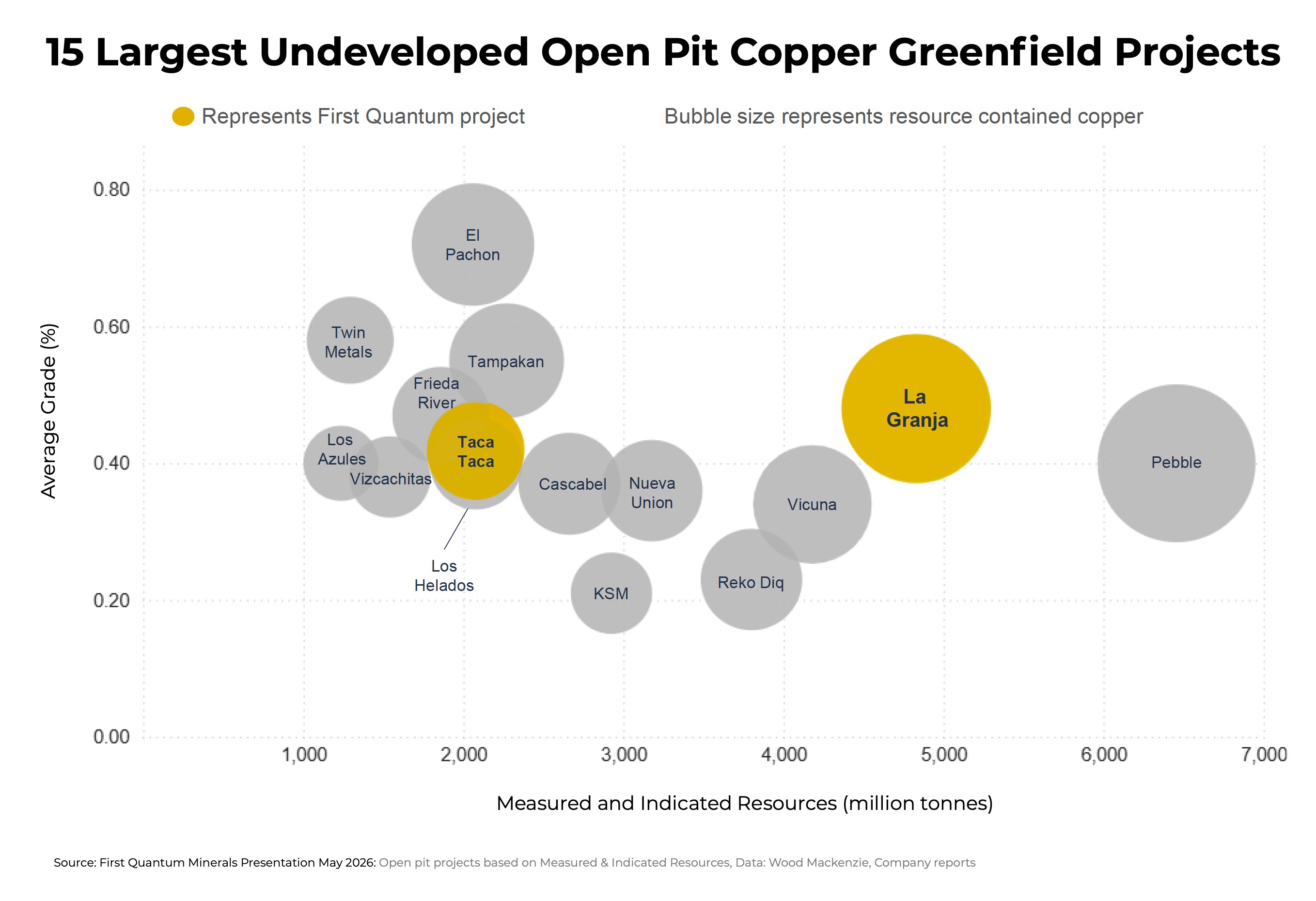

CHART: First Quantum’s Peru project joins ranks of copper giants

First Quantum has completed 370,000 metres of drilling at La Granja. Image: First Quantum Minerals.

First Quantum Minerals (TSX: FM) has filed a new NI 43-101 technical report for its La Granja project in the Cajamarca region of northern Peru it holds with Rio Tinto, outlining one of the copper sector’s largest undeveloped deposits.

First Quantum, said according to La Granja’s (meaning “the farm”) updated mineral resource, the orebody contains 4.8 billion tonnes of measured and indicated resources grading 0.48% copper, equal to 23.0 million tonnes of contained copper.

A further 5.2 billion tonnes grading 0.40% copper sits in the inferred category, containing another 20.7 million tonnes of copper, setting La Granja up as a tier-1, multigenerational asset, in the words of the company.

That places La Granja second among undeveloped copper projects in terms of measured and indicated resources behind only Northern Dynasty’s Pebble in Alaska and when including operating assets, also behind Kamoa-Kakula, the Ivanhoe Mines complex in the Democratic Republic of Congo.

First Quantum acquired the majority stake for only $105 million and has since spent $70 million out of a committed $546 million to advance the project.

Engineering challenges

In an interview conducted last year, First Quantum CEO Tristan Pascall said while the La Granja deal “wasn’t up there in the deals in terms of dollars, in terms of copper in the ground is one of the largest deals done in the last 10, 20 years.”

“Rio Tinto saw in First Quantum a partner that could want a challenging project, because it’s challenging from an engineering perspective, and particularly around deleterious elements like arsenic,” Pascall said. “We had a development hypothesis that we went to Rio with, and really that revolved around dealing with the orebody in a different manner.”

First Quantum says the drillhole database for La Granja now consists of a whopping 832 diamond holes totalling a whopping 370,000 metres, with more planned. The deposit remains open at depth with further exploration targets, according to the company.

Last month, ahead of the latest mineral resource estimate, Pascal told a group of reporters during a tour of its Zambian mines the company has spent the last three years of drilling validating this hypothesis:

“Our view was that it [the arsenic] wasn’t disseminated, that it was discreet and we could package it. That means you have assayable concentrate through a conventional flow sheet, and you don’t need any exotics in order to deal with arsenic.”

La Granja in Peru. Image: First Quantum Minerals

Water and tailings

La Granja’s pit optimization was based on a copper-only cut-off using a $4.00 a pound copper price (versus today’s price of $6.65 per pound, or $14,450 a tonne). Silver, gold and molybdenum should provide by-product upside, which may well lure streaming companies.

Other challenges at La Granja (and most sites in the South American copper belt) include water and tailings management. Unlike many copper projects in the Andean belt, La Granja sits at a moderate elevation between 2,000m and 2,800m above sea level.

First Quantum plans to carry out comminution near the pit, then move material by pipeline through a 7 km access tunnel to a flatter, arid Pacific coastal plain about 100 km from the mine where processing and tailings management would be located.

First Quantum said primary water supply would come from desalinated seawater, with site contact water captured and reused in processing to reduce impacts on local environmental flows.

Next up for La Granja is permitting, and progressing baseline environmental and social studies and continuing community engagement – a process that would take several years under Peru’s strict Environmental and Social Impact Assessment (ESIA) regulations.

A prior Peruvian government estimate put La Granja’s required investment at more than $2.4 billion. First Quantum is also advancing its Haquira project in the Apurímac region of southern Peru.

Annual output over the first 10 years at Taca Taca, which has qualified under Argentina’s fast-tracking program, is pegged at 291,000 tonnes of copper and 133,000 oz. of gold at cash costs of 97¢ per pound. Production over the mine’s life is projected at 209,000 tonnes of copper and 96,000 oz. gold at cash costs of $1.26 per pound.

Appian deepens Namibia push with $400M copper mine buy

Appian Capital Advisory has acquired Omico Copper in a deal giving the mining-focused private equity firm a 95% stake in Namibia’s Omitiomire copper project as it expands its exposure to a metal expected to face surging demand growth.

The mining-focused private equity firm plans to spend more than $400 million to develop Omitiomire into a mine producing about 30,000 tonnes of copper annually over a 15-year mine life, with first production targeted within three years.

The project, about 140 km northeast of Windhoek in Namibia’s Otjozondjupa Region, is considered one of the country’s most advanced undeveloped copper assets. Appian did not disclose the acquisition price for the asset, which was sold by Guernsey-based private equity fund Greenstone Resources LP and Australian mining company International Base Metals Ltd.

“Omico Copper is a technically robust development opportunity that aligns with Appian’s investment philosophy,” CEO Michael Scherb said in a statement. “The project complements our portfolio, offering near-term production alongside long-term growth potential.”

Scherb told Bloomberg News the firm could announce two more copper acquisitions before year-end involving projects at similar stages of development in South America, North Africa and southeastern Europe.

Mining investors are increasingly targeting copper assets amid expectations supply will struggle to meet rising demand from electric vehicles, renewable energy systems, power grids and AI infrastructure. S&P Global forecasts copper demand will climb 50% to more than 42 million tonnes by 2040 from 28 million tonnes last year.

The metal, crucial to electrification, is once again trading near a record high above $14,000 a tonne as a squeeze on Middle Eastern sulfur supplies threatens some operations, compounding disruptions at major mines elsewhere around the world.

Building a copper pipeline

Appian’s latest acquisition also builds on a broader strategy to expand its mining portfolio across Africa and Latin America. In October 2025, the firm established a $1 billion partnership with the International Finance Corp., the World Bank’s private-sector arm, to support mining investments in the regions.

The fund has already backed the development of an underground operation at the Santa Rita nickel mine in Brazil and the expansion of Asante Gold Corp.’s mines in Ghana, Scherb said. Namibia remains one of several “tier-one jurisdictions” where Appian is actively seeking investments alongside Morocco, Ivory Coast, Botswana and Zambia

The firm’s current portfolio includes operations producing about 480,000 ounces of gold annually, along with 55,000 tonnes of zinc and 19,000 tonnes of nickel.