Iran Hits Bulker off Qatar and Targets Kuwait and UAE as it Responds to US

In actions, which can probably best be interpreted as an attempt to maintain pressure on the United States in the context of ongoing negotiations, on Sunday, Iran launched limited attacks against three Gulf countries.

The Kuwaiti Army intercepted two inbound drones early on Sunday, May 10. It did not indicate from which direction the drones had come from, but in a previous attack on April 25, two drones launched at northern border posts had been launched from Iraq, presumably by militias owing allegiance to Iran and at Iran’s initiative.

Also, early on Sunday, a drone struck a cargo vessel in Qatari waters northeast of Doha, causing a fire on board. The vessel was en route from Abu Dhabi to the port of Mesaieed, and the crew managed to put out the fire and to complete the passage. UKMTO reported the incident, as did the Qatari Ministry of Defense, but did not name the vessel that had been hit. The only bulk carrier recorded as having arrived in Mesaieed on May 10 is the Liberian-flagged bulk carrier the MV Laya (IMO 9272864).

Earlier in the day, a loaded Marshall Islands-flagged LNG carrier, Al Kharaitiyat (IMO 9397327), was reported to have successfully transited the Strait of Hormuz using the Tehran-approved northern route and is expected in Port Qasim, Pakistan, on May 11. The Al Kharaitiyat (113,845 dwt) is managed by Nakilat Shipping Qatar for QatarEnergy. The transit was clearly made with permission from the Iranian authorities, probably as a concession to Pakistan for its part in hosting Iranian-US negotiations. Pakistan is desperately short of LNG imports.

The UAE’s Ministry of Defense reported that the UAE too had been attacked by two drones fired from Iran, which were intercepted and destroyed before they were able to cause any injuries or damage.

Iran’s IRNA news agency reported on Sunday that it had sent its response to the latest U.S. proposal to Pakistan.

These attacks, and the contradiction whereby a Qatari-bound vessel is attacked while a Qatari-owned LNG tanker is allowed transit, are clearly part of an IRGC-led strategy to apply pressure on the Gulf states, so that they in turn will pressure U.S. negotiators to grant Iran concessions in the current round of negotiations. While this may have been the IRGC’s intention, the tactic is equally likely to backfire and provoke GCC states to adopt a more aggressive attitude towards Iran.

Iranian Shadow Fleet Tanker Ablaze off Jask

In imagery taken by the Sentinel-2 satellite on May 9, the sanctioned Iranian-flagged dark fleet tanker Sevda (IMO 9172040) appears to be damaged and on fire, but still afloat, 11.5 nm south-east of the Bandar-e Jask headland. This position is 4.5nm due south of the regular Iranian Navy (Nedsa) base at Jask, which was opened in January 2025 and is home to the headquarters of the Nedsa’s 2nd Naval Region.

From imagery taken on May 9, smoke is coming from the rear of the ship, and accepting the limitations of the low resolution imagery available, the ship does not appear to be sinking. But the heat of the fire is sufficiently intense to show up as a heat spot in NASA FIRMS infrared imaging also captured today.

The four tankers affected, with the Jask naval base to the north circled in green (Sentinel-2/CJRC)

To the north-west of the burning Sevda, some 1.6nm distant, is a second, larger vessel, 312 meters long and probably a VLCC tanker, which also appears to be in trouble. From the low-resolution imagery available, the tanker is giving off a small amount of smoke, or is suffering from a leak at the stern. In the same area of the Jask bight, there are two other vessels (likely VLCCs) standing off, with one of the two giving off a small smoke plume and a more pronounced oil leak and the other not apparently in distress. There are no visible rescue craft assisting any of the tankers.

For the last few years, the Sevda appears to have been plying its trade with its AIS system switched off. But when it has been visible, it has been making trips to Zhoushan in China, close by to Shanghai. The 1999-built Sevda was sanctioned by the US Treasury’s Office of Foreign Assets Control in 2012.

These reports accord with news released by CENTCOM that on May 6 and May 8, US Navy F/A-18 Super Hornets attacked the Sevda and two other Iranian-flagged and OFAC sanctioned VLCCs, the tankers Hasna (IMO 9212917) and Sea Star III (IMO 9569205) with 20mm cannon fire and precision-guided munitions, with the intention of disabling propulsion and steering systems without sinking the vessels.

Meanwhile, on the other side of the Bandar-e Jask peninsula, the Single Buoy Mooring (SBM) off the Kooh Mobarak crude oil export terminal was imaged successively on three days between May 6-8. On each occasion the SBM was empty of a tanker but was apparently leaking crude oil – suggesting the SBM has a technical fault.

Iran War Threatens Gulf Investment Boom in Central Asia

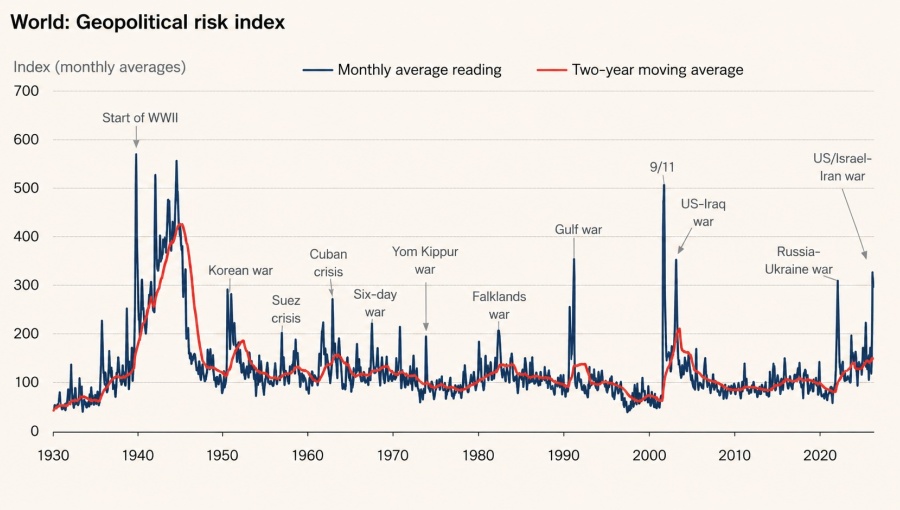

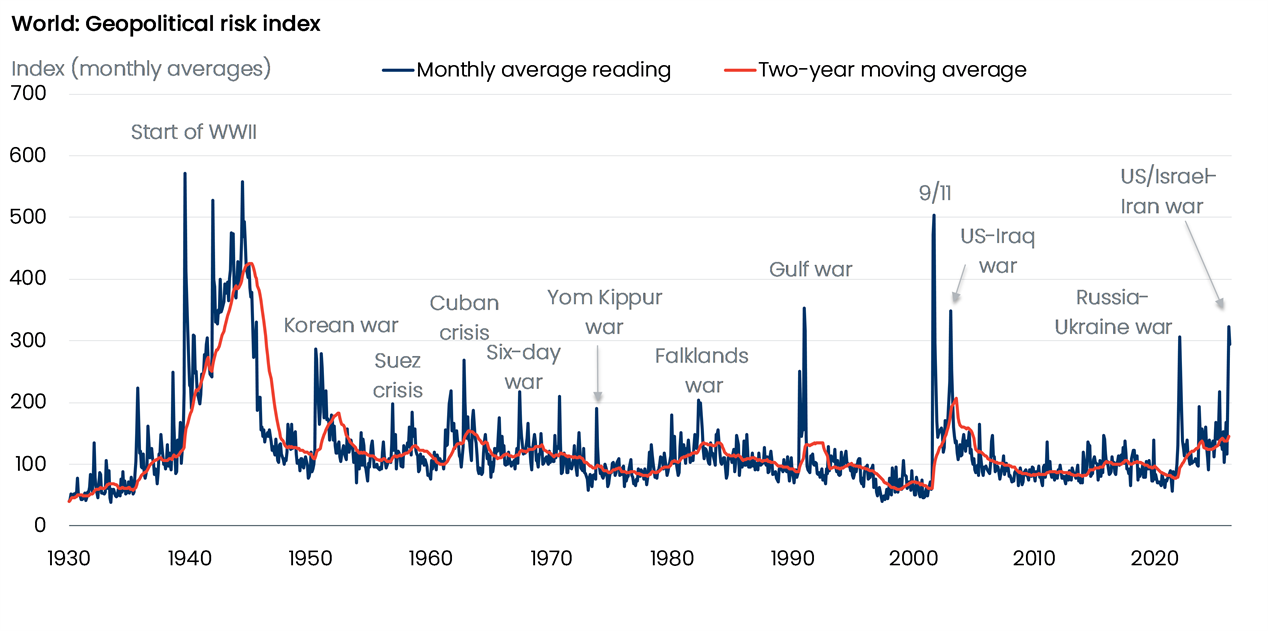

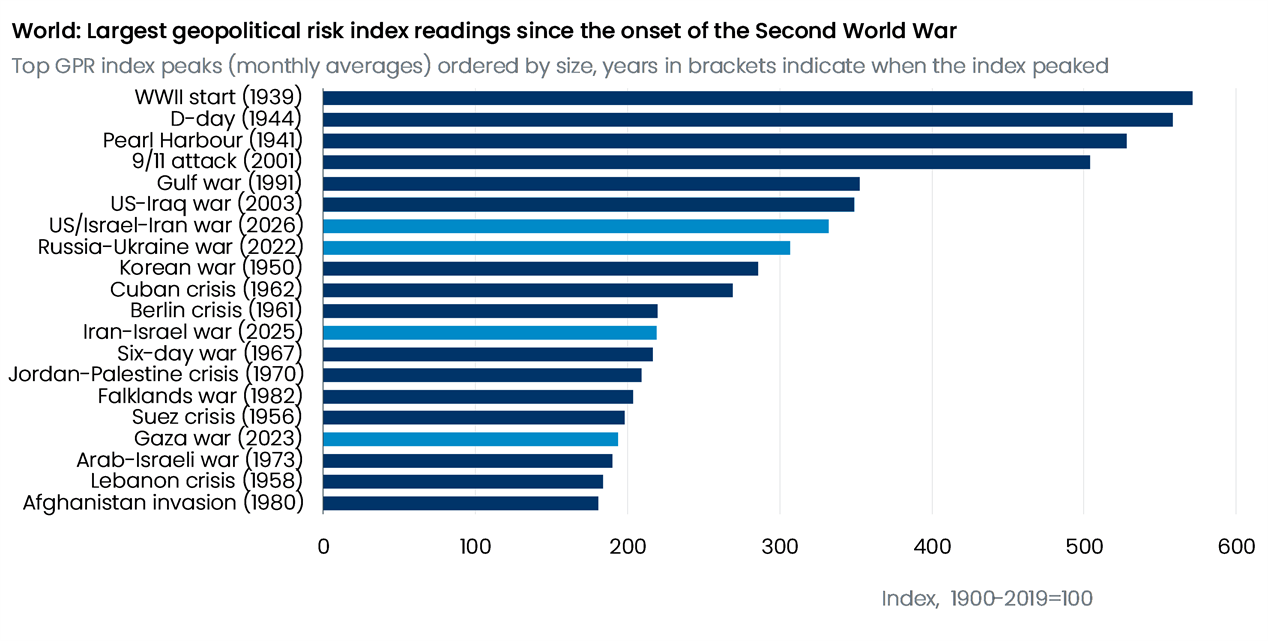

- The 2026 Iran war and Strait of Hormuz disruption are forcing Gulf states to reconsider overseas spending.

- Gulf sovereign wealth funds had committed more than $16 billion to Central Asia before the conflict, backing major energy, infrastructure, logistics, and banking projects in Kazakhstan, Uzbekistan, and Tajikistan.

- As Gulf capital becomes more constrained, China could emerge as the biggest beneficiary, expanding its already dominant economic influence across Central Asia while regional governments seek alternative investors and trade routes.

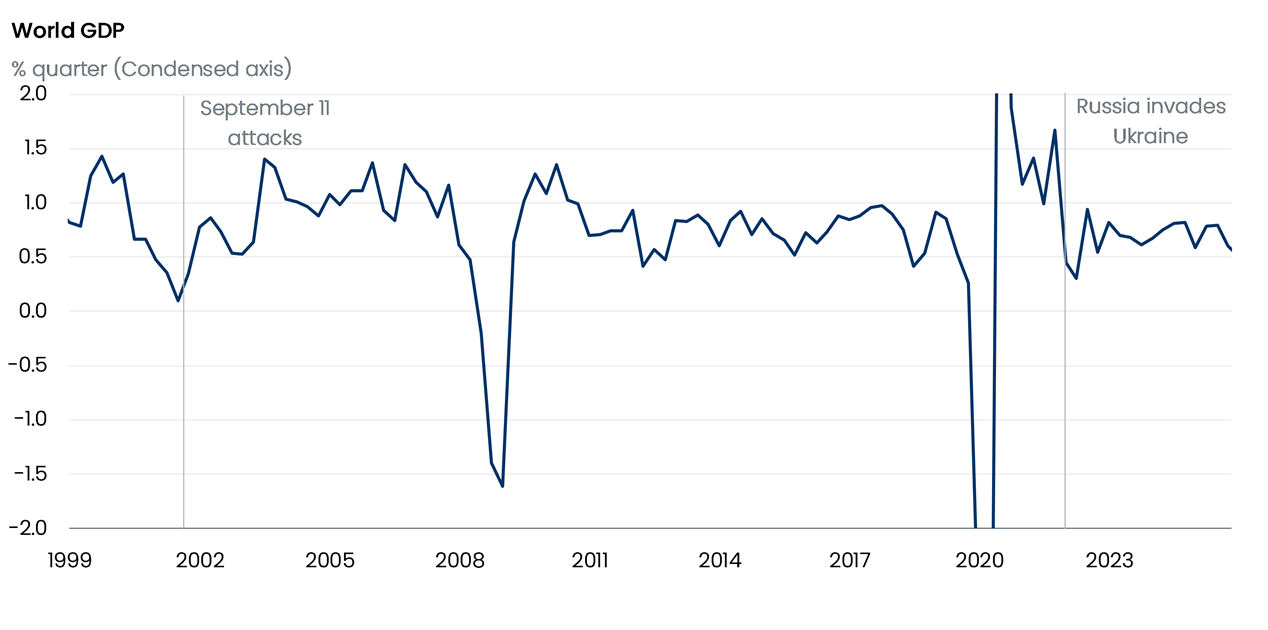

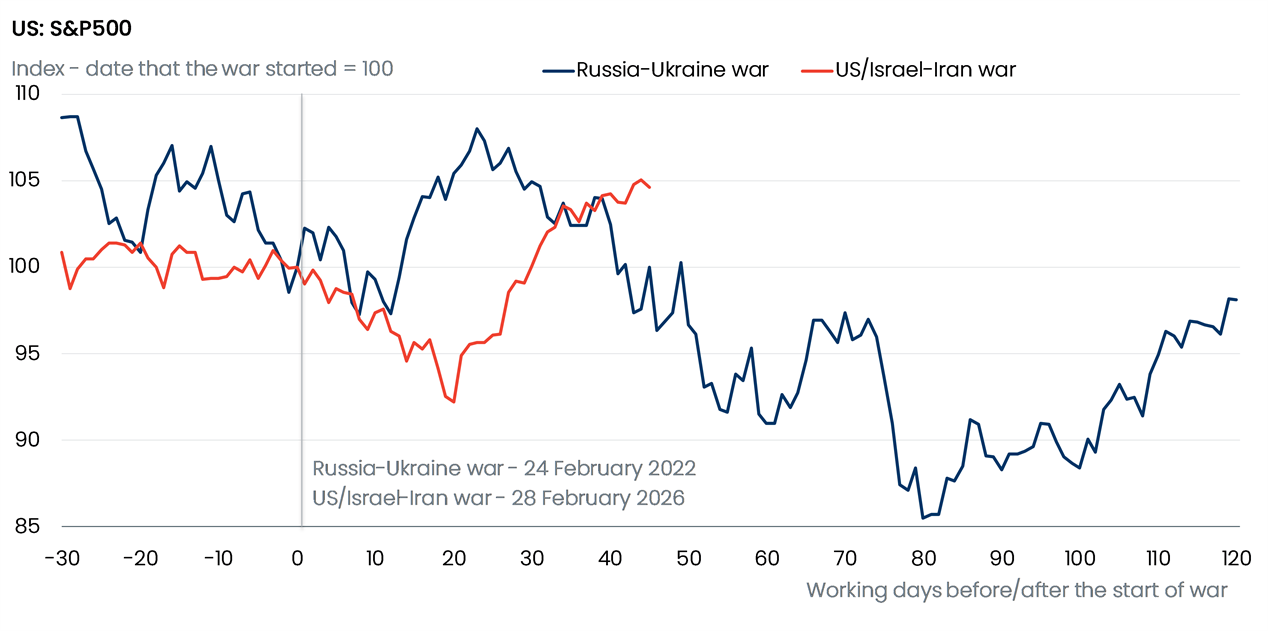

The 2026 U.S.-Israel war on Iran, the Ramadan War, which began with airstrikes on 28 February 2026 and involved Iranian retaliation via missiles, drones, and a blockade of the Strait of Hormuz, has indirectly but significantly constrained investment plans by Persian Gulf petrostates, primarily Saudi Arabia, the United Arab Emirates, and Qatar, along with other Gulf Cooperation Council (GCC) members, in Central Asia.

These petrostates were not direct belligerents but suffered economic fallout from Iranian strikes on their energy infrastructure, ports, aviation, tourism, and logistics, plus the near halt of roughly 20% of global oil and liquified natural gas (LNG) flows through Hormuz.

Goldman Sachs projects GDP hits of up to 14% for Qatar and Kuwait, 5% for the UAE, and 3% for Saudi Arabia if disruptions persist. The United Nations Development Programme estimates the war “may cost economies in the region from 3.7 to 6.0 percent of their collective Gross Domestic Product (GDP)” or US$120-194 billion and exceeds the cumulative regional GDP growth achieved in 2025.”

War damages have forced a broader fiscal rethink, with at least three GCC governments reviewing trillions in sovereign wealth fund (SWF) deployments, potential pledge reversals, divestments, and sponsorship deals to offset losses and prioritize domestic recovery, defense, and infrastructure hardening. Saudi Arabia has ended its partnership with the Metropolitan Opera in New York City and the LIV Golf, but the real consequences will come from reduced investments in transport, energy, and water projects in Asia and Africa, not image-building projects targeted at well-off consumers in high-income countries

Pre-War Context

Before the conflict, Gulf petrostates had been expanding investments in Central Asia, primarily Kazakhstan, Uzbekistan, and Turkmenistan, as part of economic diversification away from oil, resource-seeking (e.g., uranium, rare earths, gas), and geopolitical hedging, totaling US$16.2 billion by late 2025. Examples included UAE logistics and energy deals, Saudi mining and infrastructure, and broader GCC engagement in post-Soviet markets. These were modest relative to Gulf investments in the U.S., Europe, or Africa but aligned with Vision 2030-style strategies and alternatives to Russian and Chinese influence, which also suited Washington’s interests.

Direct Impacts on Investment Plans

No cancellations of specific Central Asia projects have been officially announced so far, but the war’s economic shock has created clear headwinds through several channels:

Capital constraints and SWF recalibration. GCC SWFs (managing ~$5 trillion) may shift towards domestic needs, e.g., repairing damaged facilities, bolstering defense, and supporting local economies, at the expense of overseas foreign direct investment (FDI). This may signal the end of the era of “big spenders,” with reviews explicitly targeting global pledges, including those 2025 commitments to U.S. president Donald Trump worth US$2 trillion. Central Asia investments, being non-core compared to U.S./Europe or immediate neighbors, are likely to be deprioritized or delayed.

Higher risk premiums and investor caution. The Gulf’s image as a stable “safe haven” has been damaged, raising costs of capital and making ambitious foreign expansions less attractive. This affects not just inbound FDI to the Gulf but also the Gulf states’ outbound investment plans.

Ripple effects on Central Asia. The Hormuz blockade and Iranian route disruptions raised trade and logistics costs for landlocked Central Asian states (which rely on Iranian territory for Gulf access), driving inflation, shortages, and slower growth. This makes the region less attractive for large-scale Gulf investment in the short term, though it has accelerated interest in alternative, such as the Middle Corridor, though the latter has limited utility for trade with South and West Asia.

Specific deals from 2023 to 2025 highlight the momentum that may be endangered:

UAE: First Abu Dhabi Bank financed Uzbekistan’s 500 MW Zarafshan Wind Power Project (Central Asia’s largest renewable project at the time) and supported bond placements. UAE sovereign funds and entities were major players in renewables and re-exports.

Saudi Arabia: ACWA Power and other entities pursued clean energy and infrastructure deals with Kazakhstan and Tajikistan, and US$30 million in concessional loans for Tajikistan’s Kulob Ring Road). The Saudi Arabia-based Islamic Development Bank has financed energy, transport, and agriculture projects in Central Asia.

Qatar: Lesha Bank acquired Kazakhstan’s Bereke Bank (a full bank takeover, the first by a Gulf investor) for US$134 million in 2024. The Qatar Fund for Development committed US$50 million to Tajikistan’s Rogun Hydropower Project and announced plans to participate in gas processing and hydropower ventures in Kazakhstan and Turkmenistan.

Uzbekistan and Kazakhstan (largest economy) have seen the biggest inflows of Gulf investment.

The investments went hand-in-hand with high-level diplomacy. The first GCC–Central Asia Summit was held in Jeddah, Saudi Arabia in July 2023, and a second was planned for Samarkand, Uzbekistan in May 2025 but has been indefinitely delayed. Ongoing ministerial meetings have focused on transport, communications, energy, trade, economic, and cultural exchanges.

In April 2026, Kazakhstan’s foreign minister met his UAE counterpart in Abu Dhabi and delivered a message from Kazakh president, Kassym-Jomart Tokayev, to the UAE’s president, Sheikh Mohamed bin Zayed Al Nahyan. In March 2026, Uzbekistan’s foreign minister and first deputy foreign minister met separately with the ambassadors of Qatar, Saudi Arabia, the UAE, Kuwait, and Oman.

Potential Shifts or Opportunities

There are some countervailing dynamics, but they appear limited by fiscal strain:

Alternative connectivity focus: The Hormuz crisis has validated (and accelerated) Gulf investments in bypass infrastructure (e.g., pipelines, GCC rail projects) and partnerships like China-Pakistan Economic Corridor/Gwadar Port to create land corridors linking the Gulf to Central Asia via Pakistan or the Caspian. This could open niche opportunities for Gulf capital in Middle Corridor logistics or energy links, positioning the petrostates in multipolar trade routes.

Supply diversification: Central Asian states are seeking alternative suppliers (including from the Gulf) for goods previously routed via Iran, which could sustain or modestly expand targeted trade/investment ties—though Gulf exporters are themselves strained.

Energy diversification tailwinds: The Hormuz crisis has highlighted Gulf vulnerabilities, accelerating interest in overland/non-Gulf routes. China is pressing Turkmenistan and Uzbekistan to increase natural gas production, and the crisis may see the revival of discussions on Central Asia-to-China Line D capacity expansion.

Central Asia’s neutrality and lower direct exposure make it a safer diversification play for any residual GCC capital once the ceasefire stabilizes. Kazakhstan, Uzbekistan, and Turkmenistan have welcomed the truce and emphasized peaceful resolution.

Overall, the net effect has been a slowdown or scaling-back of planned Gulf investments in Central Asia. Pre-war momentum has been dented by the need to conserve capital at home amid the worst economic shock to GCC states since the early 1990s (or even the COVID pandemic). Long-term diversification goals remain, but near-term execution is more cautious, with resources funneled toward resilience and core priorities. The situation remains fluid amid the tense ceasefire between Iran and the U.S./Israel, so further shifts could occur if Hormuz disruptions ease or escalate.

Cui bono?

If Gulf capital dries up, other potential investors are Europe, the U.S., Russia, Japan, Turkey, India, or South Korea. The big winner may be China, as the American administration is likely expecting to be the recipient, not the source of, Central Asia investment. (In November 2025, Trump announced over US$ 100 billion in investment and contracts from Uzbekistan and Kazakhstan.)

China has invested about US$89.3 billion in Central Asia and Beijing may see an opportunity to expand its influence in the region, and to drive better terms if it doesn’t have to compete with Gulf investors, though local leaders will have to consider increased public skepticism of Chinese investment.

By James Durso for Oilprice.com

U.S. Navy Remains Poised in the Arabian Sea

An unexpected release of up-to-date Sentinel-2 satellite imagery covering the Arabian Sea and CENTCOM area on May 6 and 7 has enabled analysts to gain a better understanding of how the U.S. Navy is operating its blockade of the Strait of Hormuz and positioning itself against the threat posed by Iran’s IRGC Navy. Since February 28, access to commercial satellite imagery has often been time-lagged or restricted in coverage, but the recent release has enabled open-source analysts, led by the doyenne of the community MT Anderson, to draw some useful deductions.

In recent days, the U.S. Navy has sent Arleigh Burke destroyers, and probably other craft as well, through the Strait of Hormuz and then back out again, indicating that the 6th Fleet has confidence to counter the IRGC Navy’s threat, at least for short periods of time and when it wants to. This suggests that the U.S. Navy's defensive shield against drones and cruise missiles, as well as underwater threats, remains intact. But it also implies that the U.S. Navy has a good understanding of where mines might be, or has the means to clear a mine-free path when it chooses to do so. On balance, given that a number of ships have also made solo runs through the southern half of the Strait in recent days, it appears that very few, if any, mines have been laid. The Royal Navy of Oman also does not appear to hesitate before moving through these waters to come to the aid of ships in distress.

U.S. Navy ships do not linger in the Strait, and a number of merchant vessels have been hit by the IRGC Navy in recent days, which implies that the IRGC Navy still has a credible anti-ship capability, based mostly on drones and anti-ship missiles fired from mobile launchers, but also from armed fast attack craft indistinguishable from the trader speedboats, which are very common in these waters.

Cognizant of this threat, but also seeking to maintain a blockade targeted specifically against Iranian ships and ports, the U.S. Navy is maintaining a blockade plan that is familiar to students of the Napoleonic wars. For most of the period 1793 to 1815, the Royal Navy maintained a blockade of French ports to strangle French trade and restrict the activities of the French fleet. The blockade was maintained by an inshore squadron of fast and light ships off each port, with a heavier fleet presence held further back, ready to react to any attempted breakouts reported by the inshore squadrons.

Surveillance technologies have made the art of blockading a somewhat simpler business nowadays, but a similar pattern can be seen in the Arabian Sea on May 6. The main blockade line, including at least one of the two Nimitz Class aircraft carriers under CENTCOM and the San Antonio Class flat top USS New Orleans (LPD-18), also with F-35s aboard, is holding east of a line between Ras Al Hadd in Oman and the Iran/Pakistan border at Chah Bahar. The blockade line is thickened up with probably more than just the two Arleigh Burke destroyers, which can be identified. Others are probably hidden behind cloud cover. Inshore, at either end and forward of the blockade line, are two distinctively-shaped Independence Class Littoral Combat Ships, which are optimized for just this role. This laydown allows the blockade to be maintained without overmuch vulnerability to short-range IRGC drone and cruise missile attacks, giving time and space to disrupt any such attacks, but also enables short-duration forays forward into the Strait and, where necessary, to seize blockade runners.

MT Anderson’s analysis of US Navy ship deployments in the Arabian Sea, May 6 (@MT_Anderson)

A separate tranche of imagery on May 7 also shows a busy lagoon at the Diego Garcia Naval Support Facility, with an Arleigh Burke destroyer present, and also the distinctive 193-meter MV Ocean Trader (IMO 9457218), which serves as a support base for the mounting of special force operations. The presence of MV Ocean Trader, carrying a key strategic capability, is normally an indicator and warning of a particular strategic focus and often of impending operations. An unidentified 130m long vessel is tied up at the jetty, possibly an Independence Class Littoral Combat Ship, or the cargo vessel Ship SLNC Star (IMO 9415325), which makes regular resupply runs from Singapore to Diego Garcia. Also present in the lagoon, as is normal, is one 291-meter long vessel, and hence either a Bob Hope or Watson Class replenishment ship of the Maritime Pre-positioning Ship Squadron 2 (MPSRON-2). On the South Ramp is a slightly smaller contingent of aircraft than is now normal: two US Navy P-8 surveillance aircraft, four KC-135 refuellers, and two large transport aircraft, but possibly with fighter aircraft in the four hangars.

The Diego Garcia lagoon on May 7, with three ships at anchor and approximately eight aircraft on the South Ramp (Sentinel-2/CJRC)

There is no sign in the lagoon of any impounded dark fleet tanker. The WANA news agency, which is associated with a particular hardline faction of the IRGC intent on sabotaging any peace deal, claimed with no credibility on May 5 that two seized tankers were en route to Diego Garcia, whilst also admitting that the AIS systems of both these two ships were switched off. Without AIS information, it is difficult to understand how the WANA news agency would know where these two tankers were. In any case, they appear presently not to be in Diego Garcia, and are unlikely to arrive there while Lord Hermer remains the UK’s Attorney General, given his particular internationalist credentials.

Iran Diverts and Seizes a Tanker Linked to its Own Oil Industry

The government of Iran claims to have seized a sanctioned tanker with longstanding ties to its own oil industry.

For reasons unknown, Iranian forces claim to have captured and detained the tanker with IMO number 9255933 (currently trading as the Jin Li, previously the Ocean Koi, Cimarron, Daisy 2 and Tania). IMO 9255933 has been involved in moving Iranian HFO and condensate exports for years, according to the U.S. Treasury, and has been part of Iran's shadow fleet since 2020. The vessel was sanctioned in February 2026, along with Shanghai-based owner Ocean Kudos Shipping Co Ltd. Her flag registration with the Barbados registry ceased last year, and she is currently operating as a stateless vessel, as is increasingly common in the shadow fleet.

Treasury's allegations have been independently confirmed. Consultancy TankerTrackers.com told the New York Times that over the last five years, the IMO 9255933 has made at least 16 voyages laden with Iranian petroleum - half of which began with a ship-to-ship transfer, a standard procedure for Iran's covert oil shipping network.

Windward assesses that the vessel's seizure is likely "performative," since the ship is linked to Iran's own energy exports. The Iranian Navy's announcement of the seizure provided few specifics about the reasons for capturing and detaining a previously-friendly vessel.

"Implementing the decision of the Supreme National Security Council and with a judicial ruling, the Army Navy seized the oil tanker Ocean Koi, which was carrying Iranian oil and tried to take advantage of the situation in the region to harm and disrupt the oil exports and the interests of the Iranian nation," Iran's military said in a statement to state-run IRNA News.

Mystery Deepens Over Explosion and Fire on HMM Vessel as Iran Denies Attack

There is a growing mystery over the cause of the explosion and fire on HMM’s new general cargo ship, HMM Namu, which was reported on Monday. As the vessel was anchored off the UAE port of Umm Al Quwain, reports immediately associated it with new attacks from Iran, but now uncertainties are arising, including suspicions that the fire was the result of a mine explosion.

The ship, which was delivered to HMM at the beginning of the year, is a general cargo vessel. It is 38,314 dwt and is registered in Panama. It has been inside the Persian Gulf since the start of the war. Earlier reports put the vessel at Saudi Arabia’s Dammam Port.

The ship was rocked by a powerful blast in its engine room, followed by a fire late on Monday. The fire burned for hours, but HMM reported by Tuesday that it was extinguished and the 24 crewmembers aboard were safe.

Donald Trump wrote on social media that Iran had “taken some shots” at a South Korean vessel. He called on South Korea to get involved in the efforts to reopen the Strait of Hormuz.

UKMTO, however, reported the cause of the fire was “unknown,” while Iran’s Press TV supported the claims that Iran had attacked the ship. It cited the navigation restrictions on the Strait of Hormuz. Iran’s embassy in South Korea, however, released a statement saying Iran “firmly rejects and categorically denies any allegations” regarding its involvement in the incident.

The head of the South Korean maritime union, Jeon Jeong-geun, speaking with reporters on Thursday, offered a new theory. He asserts there is no visible hull damage. His theory is that the ship was hit by a shock wave, possibly from a mine or other explosion, and that affected the engine room’s fuel system and caused the fire. He rejects the suggestion that it was an onboard equipment malfunction.

The report notes that there were warnings of possibly drifting mines, and Iran has said it is not sure of the location of all the mines placed by the IRGC. The UAE had also reported that it came under attack around the same time as the explosion on the ship.

Neighboring ships to the HMM Namu in the anchorage reported a loud blast. As a precaution, those ships repositioned away from the HMM vessel, fearing an external attack.

For its part, the South Korean government is reserving judgment. South Korea’s National Security Adviser is noting that there was no flooding or loss of stability. South Korea dispatched a team of seven to investigate, and they arrived in Dubai this morning, May 7. Included in the team are representatives from the Maritime Safety Tribunal and the Korean Register.

HMM reports a tug was dispatched to the HMM Namu, which is disabled, and it was reaching the vessel on Thursday morning. They said it would take several hours to attach a tow line to the ship and test the equipment. It will be towed approximately 40 miles to Dubai, where it is expected to arrive on Friday morning, and the ship will be put in a dry dock for an inspection.

An official with South Korea’s Foreign Ministry in Seoul said they first needed to “determine the facts,” and then they would be able to identify the cause. The official said decisions on future responses should come after the investigation.