By Michael Hudson

March 11, 2026

Source: Democracy Now!

Transcript

This is a rush transcript. Copy may not be in its final form.

AMY GOODMAN: This is Democracy Now!, democracynow.org. I’m Amy Goodman, with Juan González.

“The US/Israeli Attack Was to Prevent Peace Not Advance It.” That’s the headline of a new article in CounterPunch by the economist Michael Hudson, who details how President Trump opted to attack Iran despite progress made during last week’s U.S.-Iran negotiations in Geneva. In the piece, Hudson writes about the significance of these comments by Oman’s Foreign Minister Badr Albusaidi, who appeared on CBS’s Face the Nation Friday, one day before the U.S. attack.

BADR ALBUSAIDI: If the ultimate objective is to ensure forever that Iran cannot have a nuclear bomb, I think we have cracked that problem through these negotiations by agreeing a very important breakthrough that has never been achieved anytime before.

AMY GOODMAN: We’re joined now by the economist Michael Hudson, president of the Institute for the Study of Long-Term Economic Trends, distinguished research professor of economics at University of Missouri-Kansas City.

Thanks so much for being with us, Michael. I mean, it seems that the Oman foreign minister flew to Washington so he could directly address this issue, saying more progress had been made and that the deal was going to be one better than Obama’s. He didn’t trust President Trump’s envoys, Jared Kushner and as well as — he didn’t trust Kushner to convey the level of progress that had been made, so he spoke directly himself to the American people through the U.S. press. Your response?

MICHAEL HUDSON: The fact that progress was being made, and that Iran negotiators had agreed not to only — not to have an atom bomb, but to reduce their refined uranium, to shift the refined uranium outside of the country, and to submit to an unprecedented degree of oversight, made it urgent that the United States attack Iran immediately, because what happened was that after the Iranian negotiators went back to Iran, Khamenei and his religious leaders and the military leaders sat down to have a meeting to draft their reply accepting the U.S. demands.

But none of this was about an atom bomb to begin with. The whole reason that America has attacked Iran has nothing to do with its getting an atom bomb, because it wasn’t getting an atom bomb. The aim was to control Near Eastern oil by the United States. And General Petraeus, years ago, had outlined this whole plan in saying, “Well, we’re going to conquer seven Near Eastern countries, culminating in Iran.” Well, actually, the plans go way back to 1974, when OPEC quadrupled the prices, and the United States said, “Well, you can quadruple the prices, but we need to control the world’s oil trade, because oil is a chokepoint. Every country needs oil for its industry, for its transportation, for its electricity, to heat the home. And if we can control the world’s oil trade, then we can use that as an arm of U.S. diplomacy. And we don’t have to own the oil. We don’t have to overthrow the OPEC countries like we did the Iranian government in 1953 when they wanted to nationalize oil. You OPEC countries can nationalize your oil. You can take control of Aramco and the other countries. But you have to make an agreement that all of your profits and rents from the oil will be lent back to the United States, recycled in the United States, priced in dollars and invested in U.S. Treasury securities, U.S. bonds and U.S. stocks, so that the money, the vast dollar inflows from your oil exports, will all be part of the U.S. economy.”

I sat in on meetings in the White House in 1974 when this was discussed, because I had been the specialist at Chase Manhattan for the U.S. balance of payments and specifically for the oil industry. And from the very beginning, the U.S. foreign policy was based on if we can control the world’s oil trade, then we really have control of the world’s economy. But in order to do this, we have to prevent other countries from buying oil from countries not controlled by the United States — first by Iran after the shah was overthrown; then you can’t let them buy from Russia after 2022, so you had the sanctions against Russia and the destruction of the oil pipeline; then the sanctions against Venezuela to prevent countries from buying from Venezuela; and now back to Iran to prevent Iran from selling its oil to China. Eighty percent of Iran’s oil exports had gone to China.

So, the whole idea from the beginning was to consolidate the U.S. ability to control oil, and thereby to give Trump and the U.S. administration the ability to turn off the lights, to turn off the power, to turn off the electricity to other countries if they did not agree to follow U.S. foreign policy, to maintain sanctions against other oil countries, against Russia, China also and Iran, and follow the —

AMY GOODMAN: Michael Hudson, we’re going to continue this conversation and post it online at democracynow.org. Michael Hudson, economist, we’ll link to your article, “The US/Israeli Attack Was to Prevent Peace Not Advance It.” Michael Hudson, president of the Institute for the Study of Long-Term Economic Trends.

I’m Amy Goodman, with Juan González. I’ll be in Savannah, Georgia, on Saturday. Check our website at democracynow.org.

Trump And Netanyahu’s Iran War Could Trigger A New Economic Crisis

By Grace Blakeley

March 12, 2026

Source: DiEM 25

President Donald Trump and Israeli Prime Minister Benjamin Netanyahu shake hands after joint press conference, Monday, September 29, 2025, in the State Dining Room of the White House. (Official White House Photo by Joyce N. Boghosian)

The Iran war could lead to rising food and fuel prices, supply chain shocks, and currency crises. And it’s happening just as the shadow banking system looks set to implode…

Donald Trump and Benjamin Netanyahu’s war has already caused untold damage to the global economy. The closure of the Strait of Hormuz, combined with Iranian attacks on fossil fuel infrastructure across the Middle East, has created a shock to global supply chains not seen since the Russian invasion of Ukraine.

Yet, so far, the market reaction has been relatively muted. In part, this is down to Trump fatigue. Investors have learned to price in a certain amount of volatility regarding Trump’s policy decisions. They know he is a febrile character, prone to making rash decisions before events force him to back down – just look at the trade war, or his threats to invade Greenland.

In short, investors don’t expect this war to last very long. But even if it doesn’t, the consequences of the conflict so far will be lasting. If the salvo continues over the next week, the impact on global supply chains would be significant. If it lasts any longer than that, we would be looking at an economic shock far larger than 2022.

For as long as the markets can kid themselves that this war will be over quickly, the reaction will remain relatively contained. But reality will sink in soon enough. The damage caused over the last week can’t be undone overnight. In fact, this latest conflict will add to the challenges facing an already weakened global economy.

Because the war hasn’t been the only thing moving markets this week. We’re also facing a crisis in private credit markets. Shadow banks like Blue Owl have been making huge and complex loans to tech companies, backed by cash from pension funds and retail investors. But investors have started asking for their money back, and Blue Owl hasn’t been able to honour its promises. If this crisis continues to spread, we could be looking at a shadow banking crisis.

The future looks bleak. The war will lead to rising prices for basic essentials like energy and food. Ongoing trade tensions and shipping delays will push up prices across the economy. Rising inflation will mean higher interest rates for longer. Disposable incomes will fall thanks to rising prices and borrowing costs.

Uncertainty and fear – combined with higher borrowing costs – could dampen trade and investment. Scared consumers may try to pay down debts and build up savings, reducing demand even further. Eventually, overzealous markets will come crashing down – and contagion will spread in unexpected ways. And our corrupt, unaccountable governments will be too busy spending billions on bombs to do anything about itEmail

Grace Blakeley

Grace Blakeley is a staff writer at Tribune, and the author of Stolen: How to Save the World from Financialisation.

Thank God for Global Capitalism

March 12, 2026

David Schultz

Photograph by Nathaniel St. Clair

Oil prices are gyrating and global markets are panicking as the two-week war with Iran goes badly. According to Bloomberg and the Financial Times, Donald Trump is already having second thoughts about the conflict. That development invites an unusual reaction. Thank God for global capitalism.

If the American political system cannot restrain Trump, apparently oil traders and bond markets can. Global capitalism is once again doing what the Republican Congress, American public opinion, and the U.S. electoral system have so far failed to do. It is disciplining Donald Trump. Markets are succeeding where democratic institutions have not.

We have seen this movie before. Last year Trump announced sweeping tariffs and declared what amounted to a new economic nationalism. Markets responded exactly as markets do when profits appear threatened. Stocks dropped sharply, investors fled, and within days the administration quietly rolled back much of the policy.

Capitalism spoke and Trump listened. Commentators jokingly called it “TACO Don.” Trump Always Chickens Out. But the nickname slightly misreads the story. Trump does not suddenly discover humility or prudence. He backs down because markets force him.

Now the same drama is unfolding with Iran. Trump appeared to believe the war would be easy. A few days of bombing, the regime decapitated, and grateful Iranians rushing into the streets thanking the United States for liberating them from the Ayatollah. It is the same fantasy that surrounded the invasion of Iraq in 2003, when Americans were told that Iraqis would greet U.S. troops with flowers.

Two weeks into the Iran conflict, reality has intruded again. The regime has not collapsed, regime change appears nowhere in sight, and American public opinion is skeptical while traditional allies offer little enthusiasm. None of that, however, appears to matter much to Trump. He dragged the United States into the war without Congress and without meaningful public debate.

American casualties are beginning to mount and the administration still cannot articulate what victory actually means. At times Trump hints at escalation and even the possibility of committing ground troops. Despite the mounting problems, backing down has proven difficult politically. What may finally force reconsideration is not democratic accountability but something far more powerful: capitalism.

Oil prices are rising, financial markets are shaking, and gasoline prices in the United States are climbing sharply. The stock market has slipped while unemployment edges upward, and economists are beginning to whisper about stagflation and recession. Those economic realities may be the only thing capable of forcing Trump to reconsider his adventure. Call it the discipline of capitalism.

The United States has always been intertwined with capitalism. The year 1776 produced both the Declaration of Independence and Adam Smith’s Wealth of Nations. Yet the United States also operates within what sociologist Immanuel Wallerstein called a world capitalist system. That system has its own logic and its own enforcement mechanisms.

Contrary to the mythology surrounding Trumpism, Trump is not an isolationist. Trumpism is the highest and latest form of imperialism. Trumpism is better understood as a form of predatory capitalism on a global scale. It uses the power of the American economy and its central position in global finance to intimidate other states and extract concessions. The rules-based international order the United States helped construct after 1945 becomes something much cruder under Trumpism: economic coercion backed by military threat.

Ironically, this strategy depends on the very global interconnectedness Trump claims to despise. A truly isolationist economy could not wield the financial leverage he tries to deploy. Now that same global system appears to be pushing back. Trump’s geopolitical ambitions are colliding with the basic imperatives of global markets.

Economic historian Karl Polanyi argued in The Great Transformation that the interconnected European financial system once functioned as a stabilizing force in international politics because bankers had incentives to prevent wars that destroyed profits. Today we are seeing a similar logic at work. Global capitalism can act as a political constraint. Political scientist Charles Lindblom once described capitalism as a “great punishing machine,” one that disciplines governments that stray too far from market expectations.

Markets discipline and they punish. Push too far against the logic of capitalism and it pushes back. Investors pull money, prices surge, and economic pain spreads quickly. Call it a capitalist veto or perhaps even a capitalist coup.

Trump may now be confronting that disciplinary force. His attempt to use American economic dominance as a geopolitical weapon is colliding with the deeper imperatives of global capitalism. Over the next few weeks, we may see the familiar pattern repeat itself: markets tremble, oil prices climb, economic warnings multiply, and suddenly the White House “reconsiders.” Cue the return of TACO Don.

But again, the nickname slightly misreads the story. Trump is not chickening out. He is being forced to retreat by the logic of the very capitalist system he seeks to dominate.

The larger question remains whether he has already gone too far. Markets can discipline behavior, but they cannot easily undo the damage once instability spreads. Financial systems shaken by war do not instantly recover, nor can markets resurrect soldiers killed in a conflict launched without a clear strategy.

If this war continues to unravel, Trump will eventually need to explain the casualties and define what victory actually means. Democratic institutions have not restrained him. Congress has not restrained him. Elections and public opinion have not restrained him.

For the moment only one force appears capable of doing so. Global capitalism. Thank God for it.

David Schultz is a professor of political science at Hamline University. He is the author of Presidential Swing States: Why Only Ten Matter.

Photograph by Nathaniel St. Clair

Oil prices are gyrating and global markets are panicking as the two-week war with Iran goes badly. According to Bloomberg and the Financial Times, Donald Trump is already having second thoughts about the conflict. That development invites an unusual reaction. Thank God for global capitalism.

If the American political system cannot restrain Trump, apparently oil traders and bond markets can. Global capitalism is once again doing what the Republican Congress, American public opinion, and the U.S. electoral system have so far failed to do. It is disciplining Donald Trump. Markets are succeeding where democratic institutions have not.

We have seen this movie before. Last year Trump announced sweeping tariffs and declared what amounted to a new economic nationalism. Markets responded exactly as markets do when profits appear threatened. Stocks dropped sharply, investors fled, and within days the administration quietly rolled back much of the policy.

Capitalism spoke and Trump listened. Commentators jokingly called it “TACO Don.” Trump Always Chickens Out. But the nickname slightly misreads the story. Trump does not suddenly discover humility or prudence. He backs down because markets force him.

Now the same drama is unfolding with Iran. Trump appeared to believe the war would be easy. A few days of bombing, the regime decapitated, and grateful Iranians rushing into the streets thanking the United States for liberating them from the Ayatollah. It is the same fantasy that surrounded the invasion of Iraq in 2003, when Americans were told that Iraqis would greet U.S. troops with flowers.

Two weeks into the Iran conflict, reality has intruded again. The regime has not collapsed, regime change appears nowhere in sight, and American public opinion is skeptical while traditional allies offer little enthusiasm. None of that, however, appears to matter much to Trump. He dragged the United States into the war without Congress and without meaningful public debate.

American casualties are beginning to mount and the administration still cannot articulate what victory actually means. At times Trump hints at escalation and even the possibility of committing ground troops. Despite the mounting problems, backing down has proven difficult politically. What may finally force reconsideration is not democratic accountability but something far more powerful: capitalism.

Oil prices are rising, financial markets are shaking, and gasoline prices in the United States are climbing sharply. The stock market has slipped while unemployment edges upward, and economists are beginning to whisper about stagflation and recession. Those economic realities may be the only thing capable of forcing Trump to reconsider his adventure. Call it the discipline of capitalism.

The United States has always been intertwined with capitalism. The year 1776 produced both the Declaration of Independence and Adam Smith’s Wealth of Nations. Yet the United States also operates within what sociologist Immanuel Wallerstein called a world capitalist system. That system has its own logic and its own enforcement mechanisms.

Contrary to the mythology surrounding Trumpism, Trump is not an isolationist. Trumpism is the highest and latest form of imperialism. Trumpism is better understood as a form of predatory capitalism on a global scale. It uses the power of the American economy and its central position in global finance to intimidate other states and extract concessions. The rules-based international order the United States helped construct after 1945 becomes something much cruder under Trumpism: economic coercion backed by military threat.

Ironically, this strategy depends on the very global interconnectedness Trump claims to despise. A truly isolationist economy could not wield the financial leverage he tries to deploy. Now that same global system appears to be pushing back. Trump’s geopolitical ambitions are colliding with the basic imperatives of global markets.

Economic historian Karl Polanyi argued in The Great Transformation that the interconnected European financial system once functioned as a stabilizing force in international politics because bankers had incentives to prevent wars that destroyed profits. Today we are seeing a similar logic at work. Global capitalism can act as a political constraint. Political scientist Charles Lindblom once described capitalism as a “great punishing machine,” one that disciplines governments that stray too far from market expectations.

Markets discipline and they punish. Push too far against the logic of capitalism and it pushes back. Investors pull money, prices surge, and economic pain spreads quickly. Call it a capitalist veto or perhaps even a capitalist coup.

Trump may now be confronting that disciplinary force. His attempt to use American economic dominance as a geopolitical weapon is colliding with the deeper imperatives of global capitalism. Over the next few weeks, we may see the familiar pattern repeat itself: markets tremble, oil prices climb, economic warnings multiply, and suddenly the White House “reconsiders.” Cue the return of TACO Don.

But again, the nickname slightly misreads the story. Trump is not chickening out. He is being forced to retreat by the logic of the very capitalist system he seeks to dominate.

The larger question remains whether he has already gone too far. Markets can discipline behavior, but they cannot easily undo the damage once instability spreads. Financial systems shaken by war do not instantly recover, nor can markets resurrect soldiers killed in a conflict launched without a clear strategy.

If this war continues to unravel, Trump will eventually need to explain the casualties and define what victory actually means. Democratic institutions have not restrained him. Congress has not restrained him. Elections and public opinion have not restrained him.

For the moment only one force appears capable of doing so. Global capitalism. Thank God for it.

David Schultz is a professor of political science at Hamline University. He is the author of Presidential Swing States: Why Only Ten Matter.

Winning and Losing in the New American World

John K. White

March 11, 2026

Photograph by Nathaniel St. Clair

According to Donald Trump, the United States is “bigger, better, richer, and stronger” since he became president, lifting his new-and-improved MAGA slogan straight from the Olympics motto of “faster, higher, stronger.” If one is to define excellence by standard of living, healthcare, or life expectancy, however, the US falls short. Counting 2026 Olympic medals, the US (33) even finished second behind Norway (41), whose population is 60 times smaller, while many other competing countries also beat the US in medals per population (US 349 million, 33), including Italy (59, 30), Germany (84, 26), and Switzerland (9, 23).

For the world’s richest country by GDP, the US oddly fails in many basic categories: household and national debt (1), healthcare costs (1), and press freedom (57) as noted by European Commission VP Kaja Kallas. Inequality is also drastic: ten Americans (Musk, Zuckerberg, Bezos, Ellison, Page, Brin, Balmer, Huang, Buffett, Dell) have 50 million times more wealth ($2 trillion) than the average American annual income. All are men – the ultimate boys’ club lording protected privilege over all others. No wonder money is at the root of politics. Winning an election these days is expensive.

Sadly, the dividers characterize success by one word – winning – typically defined by money, no matter that winning comes in many forms, some not easily labelled and often holistically gleaned in prior loss. The American figure skater Alysa Liu dropped out of skating for two years, unable to enjoy her life, returning better for the break, and ultimately achieving success in Milan; not by an Olympic gold medal, but by finding joy again. As Liu noted, winning and losing is “just something that happens. It’s the outcome. But what matters is the input and the journey.”

The US men’s and women’s (ice) hockey teams excelled in their Olympic gold-medal pursuits, both beating Canada in hard-fought 2-1 overtime finals. In his typical louche way, Trump derided the women’s achievement, offering another casual misogynist remark about having to invite the women’s team to the White House after the men’s stunning victory. He then announced a presidential Medal of Freedom for men’s goalie Connor Hellebuyck, the difference-maker (42-28 shots) in an intense end-to-end final game.

But why not say good things about both teams and award the women’s captain Hilary Knight along with Hellebuyck? A five-time Olympic medalist (2 gold, 3 silver), Knight has captained the US team since 2023, has the most ever Olympic goals and assists of any American player, and scored the equalizer in the final against Canada with 2 minutes to play. Why not reward her, unless exclusion is the goal? The boys’ club again, a subset of the bankers’ club, the round table of elites. Privileged misogyny normalized once more.

Regardless of Trump’s policies, incoherent as they are, one must also question their purpose and validity when the delivery is so angry, insulting, and cruel. Unless cruelty is the goal. Illegal immigration can be curbed, but not with the loss of basic civil rights. Trade imbalances can be addressed, but not by illegal tariffs that raise prices for everyone.

Instead of calling on our best selves, Trump reaches for the worst, reducing humanity to a constant game of winners and losers, threatening those who won’t play by his own made-up rules. Money skews every decision, reducing the joy of life to a series of heartless transactions that represents not justice but a flawed psyche. The grade-school invective is depressing, comical, and sad on every level.

Oxfam’s 2026 “Resiting the Rule of the Rich” report noted that global billionaire wealth rose to $18.3 trillion in 2025, growing three times faster since Donald Trump’s 2024 election. while at the same time 50% of the world lives in poverty. In the US, the wealth of one person, Elon Musk, alone approaches $1 trillion. But at what price is wealth accumulation rewarded when democracy is eroded, social spending diminished, and militarism expanded? In a supposed Christian-based western world, must we ever be reminded that to gain the world is to lose one’s soul? Lies work only if we continue to believe what we don’t see.

Are we embarking on a post-modern anarchic state, where lawlessness goes unpunished? Which laws apply if they are unequally applied and easily sidestepped by those with money? Crime is crime, whether insider trading, off-shore tax dodges, or common everyday theft. The old order is lying to protect itself. If the E Files (E-T Files?) were a success, wouldn’t Trump have claimed his win in the longest-ever State of the Union address. Nothing, nada, zilch.

And now, the horrors of war that melts the minds of sane humans everywhere, struggling to pay bills, feed loved ones, and share free time. When a US president pressures Ukraine and warmly welcomes a Russian leader up to his eyeballs in corruption, election fraud, and malevolence, can anyone doubt the cruelty? When a US president launches an illegal attack on a country of 93 million people, which killed over 100 schoolgirls in the first few hours, how do old moral codes continue to hold sway? The world is being wrapped in terror.

No one should be surprised when a liar lies about the one thing that sets him apart – no wars. In the words of Trump’s mentor and former chief counsel to Joseph McCarthy, New York lawyer Roy Cohn: 1) “Attack, attack, attack,” 2) “Admit nothing, deny everything,” 3) “Claim victory, never admit defeat.” With Trump in full-on attack mode, the US is winning in extrajudicial killings, military interventions, and foreign coups. Number 1 in military budget, weapons sales, and missile strikes. Behind Hollywood films, violence is the number-1 US export. Welcome to an American world of indiscriminate bombing, playing “Russian roulette” with the quick and the dead. Praise the Lord.

British writer George Orwell coined the word “doublespeak” in his 1949 novel 1984, perfectly applicable to Trump’s everyday utterances: belligerent Nobel-prize winners, Board of Peace missile strikes, Liberation Day tax-raising illegal tariffs, democracy coups. More craven are “peace” negotiations interrupted by pre-planned military attacks, exposing duplicitous diplomacy as self-serving lies (non-existent WMDs, non-existent drugs, non-existent “imminent threats”). In Trumpspeak, diplomacy is called “strategic ambiguity.”

And now, a daily dose of mangled Trumpisms for all to behold. To be seen is to be heard, as the self-appointed royal arbiter of right and wrong subjects the world to more flat-earth, wake-and-shake nonsense, showing once again there is no bad press, only screen time to fill our distracted minds. Compliance is a cudgel, threatening those who won’t play along, in particular, British prime minister Keir Starmer, who initially refused US military access to the Chagos Islands, and Spanish prime minister Pedro Sánchez, who refused access to two Andalucian military bases, and emphatically said “no to war.”

Everybody knows dialogue is preferred to conflict – take your pick from Francis of Assisi to Benjamin Franklin to a kindergarten teacher dolling out timeouts to disruptive children. Today, dialogue is even more important, given the destructive ease of push-button, computer-controlled, video-game command consoles in distant, detached “situation” rooms. In that war, the earth is seen only as real estate (including “nice” gold drapes), narrated with shocking frat-boy language (“We play for keeps”). Obscenity is now kindness.

Nor does anyone doubt the curses to be released by such artless dealings, funded by a $1 trillion-plus US Department of War budget: more anger, regional instability, and financial uncertainty. But we are horrified anew by the destruction and fallout in yet another high-stakes game of medieval Realpolitik. Iran: The Sequel. “May you live in interesting times” is a wish some crave. May you not die in the same turbulence.

And with more war comes more ecocide and more environmental degradation delivered at the end of a million-dollar missile, ensuring those on the receiving end keep paying the price long after the dust settles. With war comes the obvious destruction of homes and habitats along with the fouling of air, earth, and water with more chemical toxins, stressing ecosystems beyond repair. Even without war, we were on our way to destabilizing planetary climate. A 2015 One Earth study found that the earth’s climate “is now departing from the stable conditions that supported human civilization for millennia” as feedback loops and tipping dynamics threaten us with “long-lasting and potentially irreversible consequences.”

War is the ultimate expression of control by a government over its citizens, powerless to stop the senseless slaughter in their names. In Herman Melville’s great American novel, Moby-Dick, Captain Ahab exposed the true motivation for his quest: revenge. Trump is similarly deluded by his desire to embark on another revenge-filled “whaling voyage,” which he believes is “part of the grand programme of Providence that was drawn up a long time ago.” Land Ho! Once more into the breach. Win another one, boys.

No one can tame nature, let alone the myriad different directions of human activity. If we can’t find our humanity in the slowly darkening world, we are already dead. Are we now seeing the end of our winning ways?

John K. White, a former lecturer in physics and education at University College Dublin and the University of Oviedo. He is the editor of the energy news service E21NS and author of The Truth About Energy: Our Fossil-Fuel Addiction and the Transition to Renewables (Cambridge University Press, 2024) and Do The Math!: On Growth, Greed, and Strategic Thinking (Sage, 2013). He can be reached at: johnkingstonwhite@gmail.com

Trump’s Crazy Stock Returns Won’t Finance Your Retirement

Dean Baker

March 13, 2026

We all know how Trump likes to make up crazy numbers, which his lackeys then repeat. He has $18 trillion in foreign investment coming into the country. He won the 2020 election by millions of votes. He is lowering drug prices by 1,500 percent.

We can usually just laugh these off as the ramblings of an old man suffering from dementia. But there is one crazy Trump number that it is important people know should not be taken seriously. This is the claim on stock returns that lackeys like Treasury Secretary Scott Bessent and Commerce Secretary Howard Lutnick tout when telling people how much money their newborn kid can get from their Trump Accounts.

In their telling, the $1,000 that the government is putting into the Trump accounts, starting this year, will grow to more than $590,000 when the kid reaches retirement age. If their families are able to put the full $5,000 allowed into the account, they will have more than $2.5 million when they reach retirement, and that assumes no further contributions. (They can put up to $5,000 a year into the account.)

That’s a serious chunk of money, even if we cut it by four to adjust for projected inflation over this period. It’s also serious nonsense. The problem is that there is no plausible story whereby the stock market can provide the 10 percent nominal return the Bessent-Lutnick gang is pushing. In their story, price-to-earnings ratios would have to go through the roof.

John K. White

March 11, 2026

Photograph by Nathaniel St. Clair

According to Donald Trump, the United States is “bigger, better, richer, and stronger” since he became president, lifting his new-and-improved MAGA slogan straight from the Olympics motto of “faster, higher, stronger.” If one is to define excellence by standard of living, healthcare, or life expectancy, however, the US falls short. Counting 2026 Olympic medals, the US (33) even finished second behind Norway (41), whose population is 60 times smaller, while many other competing countries also beat the US in medals per population (US 349 million, 33), including Italy (59, 30), Germany (84, 26), and Switzerland (9, 23).

For the world’s richest country by GDP, the US oddly fails in many basic categories: household and national debt (1), healthcare costs (1), and press freedom (57) as noted by European Commission VP Kaja Kallas. Inequality is also drastic: ten Americans (Musk, Zuckerberg, Bezos, Ellison, Page, Brin, Balmer, Huang, Buffett, Dell) have 50 million times more wealth ($2 trillion) than the average American annual income. All are men – the ultimate boys’ club lording protected privilege over all others. No wonder money is at the root of politics. Winning an election these days is expensive.

Sadly, the dividers characterize success by one word – winning – typically defined by money, no matter that winning comes in many forms, some not easily labelled and often holistically gleaned in prior loss. The American figure skater Alysa Liu dropped out of skating for two years, unable to enjoy her life, returning better for the break, and ultimately achieving success in Milan; not by an Olympic gold medal, but by finding joy again. As Liu noted, winning and losing is “just something that happens. It’s the outcome. But what matters is the input and the journey.”

The US men’s and women’s (ice) hockey teams excelled in their Olympic gold-medal pursuits, both beating Canada in hard-fought 2-1 overtime finals. In his typical louche way, Trump derided the women’s achievement, offering another casual misogynist remark about having to invite the women’s team to the White House after the men’s stunning victory. He then announced a presidential Medal of Freedom for men’s goalie Connor Hellebuyck, the difference-maker (42-28 shots) in an intense end-to-end final game.

But why not say good things about both teams and award the women’s captain Hilary Knight along with Hellebuyck? A five-time Olympic medalist (2 gold, 3 silver), Knight has captained the US team since 2023, has the most ever Olympic goals and assists of any American player, and scored the equalizer in the final against Canada with 2 minutes to play. Why not reward her, unless exclusion is the goal? The boys’ club again, a subset of the bankers’ club, the round table of elites. Privileged misogyny normalized once more.

Regardless of Trump’s policies, incoherent as they are, one must also question their purpose and validity when the delivery is so angry, insulting, and cruel. Unless cruelty is the goal. Illegal immigration can be curbed, but not with the loss of basic civil rights. Trade imbalances can be addressed, but not by illegal tariffs that raise prices for everyone.

Instead of calling on our best selves, Trump reaches for the worst, reducing humanity to a constant game of winners and losers, threatening those who won’t play by his own made-up rules. Money skews every decision, reducing the joy of life to a series of heartless transactions that represents not justice but a flawed psyche. The grade-school invective is depressing, comical, and sad on every level.

Oxfam’s 2026 “Resiting the Rule of the Rich” report noted that global billionaire wealth rose to $18.3 trillion in 2025, growing three times faster since Donald Trump’s 2024 election. while at the same time 50% of the world lives in poverty. In the US, the wealth of one person, Elon Musk, alone approaches $1 trillion. But at what price is wealth accumulation rewarded when democracy is eroded, social spending diminished, and militarism expanded? In a supposed Christian-based western world, must we ever be reminded that to gain the world is to lose one’s soul? Lies work only if we continue to believe what we don’t see.

Are we embarking on a post-modern anarchic state, where lawlessness goes unpunished? Which laws apply if they are unequally applied and easily sidestepped by those with money? Crime is crime, whether insider trading, off-shore tax dodges, or common everyday theft. The old order is lying to protect itself. If the E Files (E-T Files?) were a success, wouldn’t Trump have claimed his win in the longest-ever State of the Union address. Nothing, nada, zilch.

And now, the horrors of war that melts the minds of sane humans everywhere, struggling to pay bills, feed loved ones, and share free time. When a US president pressures Ukraine and warmly welcomes a Russian leader up to his eyeballs in corruption, election fraud, and malevolence, can anyone doubt the cruelty? When a US president launches an illegal attack on a country of 93 million people, which killed over 100 schoolgirls in the first few hours, how do old moral codes continue to hold sway? The world is being wrapped in terror.

No one should be surprised when a liar lies about the one thing that sets him apart – no wars. In the words of Trump’s mentor and former chief counsel to Joseph McCarthy, New York lawyer Roy Cohn: 1) “Attack, attack, attack,” 2) “Admit nothing, deny everything,” 3) “Claim victory, never admit defeat.” With Trump in full-on attack mode, the US is winning in extrajudicial killings, military interventions, and foreign coups. Number 1 in military budget, weapons sales, and missile strikes. Behind Hollywood films, violence is the number-1 US export. Welcome to an American world of indiscriminate bombing, playing “Russian roulette” with the quick and the dead. Praise the Lord.

British writer George Orwell coined the word “doublespeak” in his 1949 novel 1984, perfectly applicable to Trump’s everyday utterances: belligerent Nobel-prize winners, Board of Peace missile strikes, Liberation Day tax-raising illegal tariffs, democracy coups. More craven are “peace” negotiations interrupted by pre-planned military attacks, exposing duplicitous diplomacy as self-serving lies (non-existent WMDs, non-existent drugs, non-existent “imminent threats”). In Trumpspeak, diplomacy is called “strategic ambiguity.”

And now, a daily dose of mangled Trumpisms for all to behold. To be seen is to be heard, as the self-appointed royal arbiter of right and wrong subjects the world to more flat-earth, wake-and-shake nonsense, showing once again there is no bad press, only screen time to fill our distracted minds. Compliance is a cudgel, threatening those who won’t play along, in particular, British prime minister Keir Starmer, who initially refused US military access to the Chagos Islands, and Spanish prime minister Pedro Sánchez, who refused access to two Andalucian military bases, and emphatically said “no to war.”

Everybody knows dialogue is preferred to conflict – take your pick from Francis of Assisi to Benjamin Franklin to a kindergarten teacher dolling out timeouts to disruptive children. Today, dialogue is even more important, given the destructive ease of push-button, computer-controlled, video-game command consoles in distant, detached “situation” rooms. In that war, the earth is seen only as real estate (including “nice” gold drapes), narrated with shocking frat-boy language (“We play for keeps”). Obscenity is now kindness.

Nor does anyone doubt the curses to be released by such artless dealings, funded by a $1 trillion-plus US Department of War budget: more anger, regional instability, and financial uncertainty. But we are horrified anew by the destruction and fallout in yet another high-stakes game of medieval Realpolitik. Iran: The Sequel. “May you live in interesting times” is a wish some crave. May you not die in the same turbulence.

And with more war comes more ecocide and more environmental degradation delivered at the end of a million-dollar missile, ensuring those on the receiving end keep paying the price long after the dust settles. With war comes the obvious destruction of homes and habitats along with the fouling of air, earth, and water with more chemical toxins, stressing ecosystems beyond repair. Even without war, we were on our way to destabilizing planetary climate. A 2015 One Earth study found that the earth’s climate “is now departing from the stable conditions that supported human civilization for millennia” as feedback loops and tipping dynamics threaten us with “long-lasting and potentially irreversible consequences.”

War is the ultimate expression of control by a government over its citizens, powerless to stop the senseless slaughter in their names. In Herman Melville’s great American novel, Moby-Dick, Captain Ahab exposed the true motivation for his quest: revenge. Trump is similarly deluded by his desire to embark on another revenge-filled “whaling voyage,” which he believes is “part of the grand programme of Providence that was drawn up a long time ago.” Land Ho! Once more into the breach. Win another one, boys.

No one can tame nature, let alone the myriad different directions of human activity. If we can’t find our humanity in the slowly darkening world, we are already dead. Are we now seeing the end of our winning ways?

John K. White, a former lecturer in physics and education at University College Dublin and the University of Oviedo. He is the editor of the energy news service E21NS and author of The Truth About Energy: Our Fossil-Fuel Addiction and the Transition to Renewables (Cambridge University Press, 2024) and Do The Math!: On Growth, Greed, and Strategic Thinking (Sage, 2013). He can be reached at: johnkingstonwhite@gmail.com

Trump’s Crazy Stock Returns Won’t Finance Your Retirement

Dean Baker

March 13, 2026

We all know how Trump likes to make up crazy numbers, which his lackeys then repeat. He has $18 trillion in foreign investment coming into the country. He won the 2020 election by millions of votes. He is lowering drug prices by 1,500 percent.

We can usually just laugh these off as the ramblings of an old man suffering from dementia. But there is one crazy Trump number that it is important people know should not be taken seriously. This is the claim on stock returns that lackeys like Treasury Secretary Scott Bessent and Commerce Secretary Howard Lutnick tout when telling people how much money their newborn kid can get from their Trump Accounts.

In their telling, the $1,000 that the government is putting into the Trump accounts, starting this year, will grow to more than $590,000 when the kid reaches retirement age. If their families are able to put the full $5,000 allowed into the account, they will have more than $2.5 million when they reach retirement, and that assumes no further contributions. (They can put up to $5,000 a year into the account.)

That’s a serious chunk of money, even if we cut it by four to adjust for projected inflation over this period. It’s also serious nonsense. The problem is that there is no plausible story whereby the stock market can provide the 10 percent nominal return the Bessent-Lutnick gang is pushing. In their story, price-to-earnings ratios would have to go through the roof.

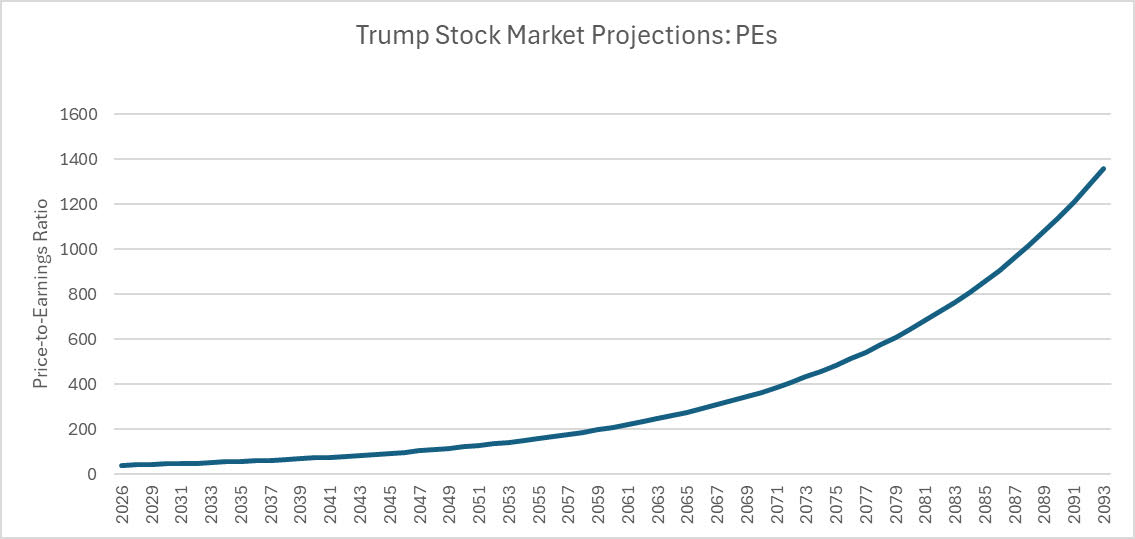

By 2093, when our newborn kid plans to cash out the fortune in their Trump Account, their 10 percent compounded returns would imply a price-to-earnings ratio (PE) of almost 1,400. The problem is that will the Trump accounts are growing at the rate of 10 percent a year, the economy and corporate profits are only growing at a bit less than 4.0 percent annually. This causes the PE to go through the roof.

This is not an old problem. Some of us have been trying to point this one out to arithmetic fans ever since the Social Security privatization debates of the 1990s. While the stock market has historically provided returns that were higher than the economy’s rate of growth, this was possible because the PE in the stock market has averaged around 14 to 1. It is currently close to 40 to 1.

The simplest way to calculate the real rate of return consistent with a stable PE is to simply take the reciprocal of the PE ratio. When the PE ratio is 14, the sustainable real rate of return is 7.1 percent. Adding in inflation that has averaged close to 3.0 percent gets the 10.0 percent that we can see going back 100 years.

But with the current PE close to 40, this sort of rate of return is not possible unless the PE gets ever higher. The sustainable real rate of return would be just over 2.5 percent. Adding in projected inflation of 2.3 percent gets us to 4.8 percent, well below the Bessent-Lutnick promise.

The moral of this story is that just as no one in their right mind would take health advice from RFK Jr., no one in their right mind should take financial advice from the Bessent-Lutnick gang. As the saying goes, do your own research.

Cracking Down on Corporate Tax Scams

Dean Baker

March 12, 2026

Photograph by Nathaniel St. Clair

With the country in the middle of a needless war and Trump making plans to end democracy, it seems a bit of a sidetrack to be talking about corporate tax policy, but sometimes we need a diversion. And the Trump sleaze is getting so extreme, it deserves some comment.

The latest are plans by the administration to greenlight a series of tax avoidance strategies that will cost an estimated $100 billion in revenue over the next decade. To be clear, this is not big bucks in terms of the federal budget. It is a bit more than 0.1 percent of projected expenditures over the next decade, but the scams raise the bigger issue of corporate tax avoidance/evasion.

The legislated corporate tax rate is 21%. In the first three quarters of 2025 (the period for which we have data), corporations paid 19.4% of their profits in taxes. The gap between the legislated rate and what they paid came to roughly $50 billion at annual rate for last year, or five times the size of the avoidance issues highlighted in the Washington Post piece.

And the problem is likely much larger. The Biden administration had actively tried to crack down on corporate tax avoidance. The tax share of corporate profits had fallen as low as 15.3% in 2018. It’s likely that the tax share will be headed downward with the Trump administration again controlling rulemaking and enforcement at the I.R.S. It’s also worth noting that some avoidance takes the form of companies that are effectively corporations, instead operating as partnerships, which don’t pay the corporate income tax at all.

There is actually an incredibly easy fix to corporate tax avoidance. We can simply require companies to give the government a percentage of non-voting shares, equal to the targeted corporate tax rates. This means if we want a 25% tax rate, then we require all corporations to turn over non-voting shares that are equal to 25% of their total shares.

These shares would be treated just like any other shares, apart from voting privileges. If the company pays a dividend of $5 a share, then each of the government shares get a $5 dividend. If it buys back 5% of its shares at $100 a share, then it buys back 5% of the government’s shares at $100 a share.

The neat aspect of this approach is that the only way companies can cheat the government is if they also cheat their shareholders, which would get some very rich people very angry. This not only gets the government the tax revenue it is targeting; it also puts the parasitic tax-gaming industry out of business.

Currently thousands of tax lawyers and accountants earn big bucks developing tax scams that allow corporations to avoid paying taxes. If companies are required to instead hand over non-voting shares to the government, these people would have to do honest work for a living; a big victory for economic efficiency.

Partnerships raise another set of issues. Partnerships do not pay income tax. Their profit goes back to the partners, who are then responsible for paying individual income taxes on the money. Until the 1950s, partnerships generally did not have limited liability like corporations, which meant that the individual partners were fully responsible for any liabilities of the partnership if it went bankrupt.

There was effectively a quid pro quo. If a company wanted the benefit of limited liability, and other benefits of corporate status, it had to pay the corporate income tax. However, this has largely broken down as it has become increasingly common for partnerships to gain limited liability, even without paying the corporate income tax.

There is little rationale for separating limited liability status from the corporate income tax. Obviously, partnerships would prefer limited liability without having to pay the corporate income tax, but there is no reason to design the tax code around the preferences of partnerships. Many partners in private equity companies, hedge funds, and real estate investment trusts are among the richest people in the country. They don’t need special treatment.

This reflects a larger problem with designing the tax code. Many corporations have adopted complicated accounting practices, largely to avoid taxes, but sometimes for other dubious purposes. They then demand Congress and/or the I.R.S. adjust tax law to accommodate these practices.

This is 180 degrees opposite of the way tax law should work. It is the responsibility of companies to accommodate themselves to the law, not the other way around. If there is a provision in the law that really does impede normal business practices, then it should be changed. But it doesn’t make sense to adjust the law to make it easier to avoid taxes or get around other laws.

Allowing partnerships to get limited liability without paying the corporate income tax is perhaps the most extreme example of this sort of accommodation, but it is a far more general problem. The point of the corporate income tax is to raise revenue from corporations, not to provide a playground for clever tax lawyers and accountants.

The issue with increasing the amount of revenue from business tax is the political will to impose higher taxes on politically powerful groups, not any technical obstacles to having an enforceable tax code.

The Winning and Losing Countries From High Oil Prices

Dean Baker

March 11, 2026

Photo by Waldemar Brandt

There has been a lot of sloppy commentary from people who should know better about who is being hit hardest by the runup in oil and natural gas prices since the start of the war in Iran. There’s a simple story where the countries in Europe and East Asia are the big losers, because they produce relatively little of their own oil. By contrast, the United States is supposedly relatively well-off since we are largely self-sufficient and in fact a net exporter of natural gas.

While the point about the US having large oil and gas production is important, it distorts the impact in important ways. The simplest way to think about the surge in oil and natural gas prices is as a big tax on consumers of these products.

When people pay $3.50 at the pumps, instead of the $2.80 we paid a month ago, this would be the same thing to consumers as if the government imposed a 70 cent a gallon gas tax. There would be a similar story with higher prices for home heating oil or natural gas. From the standpoint of consumers, the price increases are the same as if they just got hit with a big tax increase.

The difference is that instead of the money going to the government, as it would with a tax, it’s going to the oil and gas industry, Donald Trump’s campaign contributors. In principle, for a country like the United States, which is largely self-sufficient in oil and gas, if we could just rebate the money people paid in higher prices back to consumers, all would be fine.

But that sort of rebate would require big taxes, like a windfall profit tax, on the oil and gas industry. Since this industry is very powerful politically, this sort of recycling of higher revenue is not very likely. Therefore, for those of us who don’t have a lot of stock in oil and gas companies, the impact of higher prices is what we pay at the pump or for heating our homes. It doesn’t make a great deal of difference whether the people getting that money live in Houston or Saudi Arabia, it’s not going to us.

From that vantage point, if we do a cross-country comparison of the hit from higher oil and gas prices, it really just depends on how much of the stuff we consume relative to our income. By this measure, the United States does not fare especially well.

US oil consumption per unit of GDP is pretty much in the middle of the pack for wealthy countries. We use slightly less oil per dollar than Spain and Japan, and far less than Canada. South Korea uses more than twice as much oil per dollar of GDP than the United States.

By contrast, the other European countries use less oil per unit of GDP. Italy and Germany both use somewhat less oil per unit of GDP, while France uses about one-third as much, and the UK just over half as much. Both China and India using considerably more oil per unit of GDP, with India using more than twice as much.

The story with natural gas is somewhat more complicated. Here, domestic production does matter, since natural gas is far more expensive to ship overseas. Prices in Europe and Asia can be two to four times higher than in the United States. Therefore, the loss of natural gas from the Middle East will be a big hit to Europe and Asia, while having limited impact on the US.

Most European countries use considerably less natural gas per unit of GDP than the US. Italy uses roughly a quarter less, while Germany, Spain, and the UK all use about half as much. France only uses about a third as much natural gas as the United States.

In East Asia, Japan uses about 30 percent less per unit of GDP, while South Korea uses about 20 percent more. China uses about 25 percent less, while India uses half as much.

In terms of who gets the biggest hit by the flow and oil and gas from the Middle East being cut off, it seems clear that the East Asian countries will see the worst effects. Japan, and especially South Korea, will be hard hit by both higher oil and higher gas prices.

Consumers in European countries will mostly see less of an impact from the rise in oil prices than consumers in the United States. On the other hand, since natural gas prices are likely to rise much more outside the US, Europe and Asia are likely to see much more impact, as the huge domestic production limits the impact in the United States.

The cutoff of oil from the Middle East is a huge blow to the world economy and will likely cause a recession if it lasts for a long period of time. The takeaway here is that while the large amount of natural gas production in the United States insulates it from the impact seen in European and East Asian countries, greater domestic oil production does not do much to help consumers paying more at the pump.

This first appeared on Dean Baker’s Beat the Press blog.

Dean Baker is the senior economist at the Center for Economic and Policy Research in Washington, DC.

No comments:

Post a Comment