This Ohio Factory is Trump’s Secret Weapon in the Rare Earth War

The fight for geopolitical supremacy is increasingly a fight over rare earths — the critical elements that power advanced defense systems, high-performance manufacturing, and next-generation energy technologies. REalloys (NASDAQ: ALOY) is already operating in the most strategic segment of that chain, converting heavy rare earth materials into high-performance magnets and alloys inside the United States.

For Washington, the challenge is not geology — it’s processing. Many Western companies are still in early exploration or planning stages. REalloys, by contrast, runs a functioning facility in Euclid, Ohio, where heavy rare earth feedstock is refined and transformed into specialized alloys required for defense and advanced industrial use. By keeping processing onshore, the company eliminates the offshore refining bottleneck, effectively disabling China’s ability to blackmail the U.S.

The very components that determine performance in missiles, aircraft, EV motors, satellites, and critical infrastructure can soon be fabricated in North America. REalloys bridges the gap between separated oxides and the metal inputs required to produce those magnets, already supplying qualified materials under U.S. Department of Defense contracts as domestic sourcing rules tighten.

Rare earth magnets sit at the end of this chain — the high-performance components that enable precision-guided munitions, advanced aircraft systems, EV drivetrains, satellites, and critical industrial infrastructure.

Many of the technologies built by major U.S. manufacturers — including electric vehicle platforms developed by Tesla (NASDAQ: TSLA) and the AI and data-center hardware ecosystem surrounding NVIDIA (NASDAQ: NVDA) — depend on high-performance rare earth magnets that allow motors, cooling systems, and precision components to operate efficiently under demanding conditions

REalloys occupies the pivotal step just before that final assembly, converting separated oxides into the specialized metals and alloys magnet manufacturers depend on. As U.S. sourcing rules tighten, the company is already delivering qualified materials under Department of Defense contracts, positioning it as an operational link in America’s domestic rare earth supply chain.

What the DoD Needs — And Why It's Urgent

The U.S. military is actively partnering with REalloys for rare earth metals and alloys that feed into current operational programs. The company manufactures defense-specification metal and alloy domestically, built to the exact chemistry already embedded in active program supply chains. When procurement rules shift in 2027 and Chinese-origin material is disqualified, REalloys' output stays compliant with zero reformulation required. No other supplier in North America is currently producing the same grade of qualified heavy rare earth metals and alloys.

Heavy rare earths are what allow modern missile and aerospace platforms to perform reliably under punishing conditions. Dysprosium and terbium are blended into magnet alloys specifically to maintain magnetic performance as temperatures climb and vibration intensifies.

This is what makes heavy rare earths indispensable to systems like precision-guided missiles and missile-defense interceptors. Dysprosium and terbium aren't optional additives — they are required inputs for these weapons platforms.

REalloys' Position in the Rare Earth Supply Chain

Cut through the noise, and the domestic rare earth picture narrows quickly. The vast majority of U.S.-based players remain stuck in the early stages — mining, oxide separation, pilot programs, and slide decks. REalloys sits at the opposite end of the value chain, occupying the downstream processing stage where supply chains are either real or they aren't.

The company holds a signed commercial processing and long-term offtake deal with the Saskatchewan Research Council (SRC), anchored to the SRC Rare Earth Processing Facility in Saskatoon. That agreement gives REalloys (NASDAQ: ALOY) access to 80% of the facility's upgraded annual output under a cost-plus pricing structure. Heavy rare earth production from the expanded facility is on track to come online in early 2027 — a milestone that would make REalloys the sole commercial-scale North American source of dysprosium and terbium oxides.

To support that expansion, the company is investing roughly US$21 million to boost heavy rare earth processing throughput by approximately 300%, while also lifting light rare earth (NdPr) capacity by 50%. Target output includes up to 30 tonnes of dysprosium oxide, 15 tonnes of terbium oxide, and 400 tonnes per year of high-purity NdPr metal — with NdPr scaling to 600 tonnes annually once the expansion wraps up. Initial production is expected early next year.

The fight for geopolitical supremacy is increasingly a fight over rare earths — the critical elements that power advanced defense systems, high-performance manufacturing, and next-generation energy technologies. REalloys (NASDAQ: ALOY) is already operating in the most strategic segment of that chain, converting heavy rare earth materials into high-performance magnets and alloys inside the United States.

For Washington, the challenge is not geology — it’s processing. Many Western companies are still in early exploration or planning stages. REalloys, by contrast, runs a functioning facility in Euclid, Ohio, where heavy rare earth feedstock is refined and transformed into specialized alloys required for defense and advanced industrial use. By keeping processing onshore, the company eliminates the offshore refining bottleneck, effectively disabling China’s ability to blackmail the U.S.

The very components that determine performance in missiles, aircraft, EV motors, satellites, and critical infrastructure can soon be fabricated in North America. REalloys bridges the gap between separated oxides and the metal inputs required to produce those magnets, already supplying qualified materials under U.S. Department of Defense contracts as domestic sourcing rules tighten.

Rare earth magnets sit at the end of this chain — the high-performance components that enable precision-guided munitions, advanced aircraft systems, EV drivetrains, satellites, and critical industrial infrastructure.

Many of the technologies built by major U.S. manufacturers — including electric vehicle platforms developed by Tesla (NASDAQ: TSLA) and the AI and data-center hardware ecosystem surrounding NVIDIA (NASDAQ: NVDA) — depend on high-performance rare earth magnets that allow motors, cooling systems, and precision components to operate efficiently under demanding conditions

REalloys occupies the pivotal step just before that final assembly, converting separated oxides into the specialized metals and alloys magnet manufacturers depend on. As U.S. sourcing rules tighten, the company is already delivering qualified materials under Department of Defense contracts, positioning it as an operational link in America’s domestic rare earth supply chain.

What the DoD Needs — And Why It's Urgent

The U.S. military is actively partnering with REalloys for rare earth metals and alloys that feed into current operational programs. The company manufactures defense-specification metal and alloy domestically, built to the exact chemistry already embedded in active program supply chains. When procurement rules shift in 2027 and Chinese-origin material is disqualified, REalloys' output stays compliant with zero reformulation required. No other supplier in North America is currently producing the same grade of qualified heavy rare earth metals and alloys.

Heavy rare earths are what allow modern missile and aerospace platforms to perform reliably under punishing conditions. Dysprosium and terbium are blended into magnet alloys specifically to maintain magnetic performance as temperatures climb and vibration intensifies.

This is what makes heavy rare earths indispensable to systems like precision-guided missiles and missile-defense interceptors. Dysprosium and terbium aren't optional additives — they are required inputs for these weapons platforms.

REalloys' Position in the Rare Earth Supply Chain

Cut through the noise, and the domestic rare earth picture narrows quickly. The vast majority of U.S.-based players remain stuck in the early stages — mining, oxide separation, pilot programs, and slide decks. REalloys sits at the opposite end of the value chain, occupying the downstream processing stage where supply chains are either real or they aren't.

The company holds a signed commercial processing and long-term offtake deal with the Saskatchewan Research Council (SRC), anchored to the SRC Rare Earth Processing Facility in Saskatoon. That agreement gives REalloys (NASDAQ: ALOY) access to 80% of the facility's upgraded annual output under a cost-plus pricing structure. Heavy rare earth production from the expanded facility is on track to come online in early 2027 — a milestone that would make REalloys the sole commercial-scale North American source of dysprosium and terbium oxides.

To support that expansion, the company is investing roughly US$21 million to boost heavy rare earth processing throughput by approximately 300%, while also lifting light rare earth (NdPr) capacity by 50%. Target output includes up to 30 tonnes of dysprosium oxide, 15 tonnes of terbium oxide, and 400 tonnes per year of high-purity NdPr metal — with NdPr scaling to 600 tonnes annually once the expansion wraps up. Initial production is expected early next year.

Building a Diversified Feedstock Pipeline

Letters of intent are already in place covering feedstock supply from Kazakhstan, Brazil, and Greenland

In Kazakhstan, REalloys has locked in a non-binding long-term offtake deal with AltynGroup covering rare earth feedstock that includes both light and heavy elements — dysprosium and terbium among them. Critically, that material flows straight into the company's U.S.-based metals and alloy production rather than being shipped offshore for processing.

On the Brazilian side, a signed offtake memorandum with St George Mining provides potential access to as much as 40% of rare earth output from the Araxá project, pending finalization of definitive terms.

And in Greenland, a 10-year offtake arrangement — currently at the LOI stage — would deliver up to 15% of annual rare earth concentrate production from the Tanbreez project.

All of these supply streams ultimately point toward one customer: the U.S. Department of Defense.

Letters of intent are already in place covering feedstock supply from Kazakhstan, Brazil, and Greenland

In Kazakhstan, REalloys has locked in a non-binding long-term offtake deal with AltynGroup covering rare earth feedstock that includes both light and heavy elements — dysprosium and terbium among them. Critically, that material flows straight into the company's U.S.-based metals and alloy production rather than being shipped offshore for processing.

On the Brazilian side, a signed offtake memorandum with St George Mining provides potential access to as much as 40% of rare earth output from the Araxá project, pending finalization of definitive terms.

And in Greenland, a 10-year offtake arrangement — currently at the LOI stage — would deliver up to 15% of annual rare earth concentrate production from the Tanbreez project.

All of these supply streams ultimately point toward one customer: the U.S. Department of Defense.

The Euclid, Ohio Processing Hub

REalloys' facility in Euclid, Ohio is built to take separated rare earth oxides and reduce them into metal under controlled atmospheric conditions, then alloy the resulting material into compositions suitable for magnet production. The same metallurgical workflow handles both light and heavy rare earths, including dysprosium and terbium. What comes out the other end is pre-alloyed metal — chemistry locked in early in the process and maintained within the narrow tolerances that qualified magnet producers require. Functionally, Euclid occupies the critical space between oxide separation and finished magnet assembly, the exact point where rare earth materials transition from intermediates into production-ready inputs.

The finished product moves through standard commercial channels and feeds directly into magnets and components destined for DoD programs.

REalloys' facility in Euclid, Ohio is built to take separated rare earth oxides and reduce them into metal under controlled atmospheric conditions, then alloy the resulting material into compositions suitable for magnet production. The same metallurgical workflow handles both light and heavy rare earths, including dysprosium and terbium. What comes out the other end is pre-alloyed metal — chemistry locked in early in the process and maintained within the narrow tolerances that qualified magnet producers require. Functionally, Euclid occupies the critical space between oxide separation and finished magnet assembly, the exact point where rare earth materials transition from intermediates into production-ready inputs.

The finished product moves through standard commercial channels and feeds directly into magnets and components destined for DoD programs.

Rebuilding a Lost Capability Under Pressure

For the first time in a generation, the United States is attempting to reconstruct its rare earth processing infrastructure — and it's doing so while China actively squeezes the processed materials that underpin both weapons systems and industrial output.

The core problem is deceptively simple: outside of China, virtually no one can convert rare earth oxides into finished metal at industrial scale. That conversion step is precisely where Western supply chains went dark decades ago.

That bottleneck doesn’t only affect defense programs. It also threatens supply chains tied to some of the largest technology and industrial companies in the United States, including the electric vehicle manufacturing ecosystem around Tesla and the rapidly expanding AI infrastructure market driven by chips from NVIDIA.

The Center for Strategic and International Studies (CSIS) has flagged rare earth metallization and alloying as the weakest and hardest-to-restore link in any non-Chinese supply chain. In CSIS's assessment, metal and alloy production represents an experience-based bottleneck — a capability that resists shortcuts, even when capital is abundant. Metallization expertise is accumulated through sustained operational history, not assembled on a timeline. Reaching consistent, magnet-grade quality can take years, sometimes decades. You can fast-track a mine. You cannot fast-track metallization.

This is exactly where REalloys operates. While the rest of the Western rare earth sector largely tops out at oxide production or pilot-stage separation, the Euclid facility is running the conversion process that CSIS singles out as the most difficult to replicate. Oxides go in, metal comes out, alloys are formulated, and chemistry stays within specs that downstream buyers have already qualified. This isn't a future capability — it's an active one, running inside a U.S. facility and feeding usable material into defense and magnet supply chains today.

That kind of operational capability is scarce precisely because the country walked away from it a generation ago, and reconstituting it demands time that no amount of funding can compress. It's here now, at Euclid, and it defines the outer boundary of what America's rare earth rebuild — and by extension, its defense and industrial capacity — can actually deliver.

By. Josh Owens

For the first time in a generation, the United States is attempting to reconstruct its rare earth processing infrastructure — and it's doing so while China actively squeezes the processed materials that underpin both weapons systems and industrial output.

The core problem is deceptively simple: outside of China, virtually no one can convert rare earth oxides into finished metal at industrial scale. That conversion step is precisely where Western supply chains went dark decades ago.

That bottleneck doesn’t only affect defense programs. It also threatens supply chains tied to some of the largest technology and industrial companies in the United States, including the electric vehicle manufacturing ecosystem around Tesla and the rapidly expanding AI infrastructure market driven by chips from NVIDIA.

The Center for Strategic and International Studies (CSIS) has flagged rare earth metallization and alloying as the weakest and hardest-to-restore link in any non-Chinese supply chain. In CSIS's assessment, metal and alloy production represents an experience-based bottleneck — a capability that resists shortcuts, even when capital is abundant. Metallization expertise is accumulated through sustained operational history, not assembled on a timeline. Reaching consistent, magnet-grade quality can take years, sometimes decades. You can fast-track a mine. You cannot fast-track metallization.

This is exactly where REalloys operates. While the rest of the Western rare earth sector largely tops out at oxide production or pilot-stage separation, the Euclid facility is running the conversion process that CSIS singles out as the most difficult to replicate. Oxides go in, metal comes out, alloys are formulated, and chemistry stays within specs that downstream buyers have already qualified. This isn't a future capability — it's an active one, running inside a U.S. facility and feeding usable material into defense and magnet supply chains today.

That kind of operational capability is scarce precisely because the country walked away from it a generation ago, and reconstituting it demands time that no amount of funding can compress. It's here now, at Euclid, and it defines the outer boundary of what America's rare earth rebuild — and by extension, its defense and industrial capacity — can actually deliver.

By. Josh Owens

US pours $1B into into Latin America critical minerals

The United States has poured more than $1 billion into critical minerals investments across Latin America since January 2025, signalling a more assertive effort by Washington to secure supplies of lithium, copper and rare earths vital to energy, defence and advanced technology.

The spending surge under the second Trump administration reflects a broader shift in how governments view mining, with critical minerals increasingly treated as matters of national and energy security rather than simply commodities tied to the energy transition, according to a report by law firm White & Case.

The law firm’s global head of mining and metals Rebecca Campbell and project financing partner Fernando J. de la Hoz say projects in Brazil and Argentina are drawing direct interest from US agencies and multilateral lenders through loans, equity stakes and structured offtake agreements designed to channel output into US-aligned supply chains.

“Development of rare earth and critical minerals projects is no longer just a matter of energy transition, but rather, energy security,” Tiago Abreu, chief development officer of Brazilian Rare Earths, told delegates at a mining summit in Belo Horizonte in June 2025.

Recent financing underscores the trend. The Inter-American Development Bank approved a $100 million loan for a $2.5 billion lithium project in Argentina, while the US Development Finance Corporation is considering a $465 million investment to expand Serra Verde’s rare earth operations in Brazil’s Goiás state.

Latin America sits at the centre of the strategic push, holding roughly 60% of the world’s lithium reserves.

Lithium momentum

Brazil and Argentina have emerged as focal points for critical minerals development, driven by vast reserves, government policy and rising foreign investment.

Brazil hosts the world’s second-largest rare earth reserves after China and has seen growing interest in Minas Gerais, where a cluster of projects has earned the nickname “Lithium Valley.” Despite holding about 23.3% of global rare earth reserves, the country accounts for only about 0.02% of production, highlighting the scale of potential growth.

Argentina has moved aggressively to attract investment. The Incentive Regime for Large Investments, or RIGI, launched in July 2024, offers tax, customs and foreign exchange stability for projects worth more than $200 million. Rio Tinto (ASX, LON: RIO) became the first company approved under the framework in May 2025 for a $2.5 billion lithium project in Salta.

The country already hosts Latin America’s largest number of lithium projects, with seven operating. National lithium output capacity rose from 75,500 tonnes per year in 2023 to about 186,000 tonnes in 2025, and the government expects it to reach 658,000 tonnes by 2035.

Market conditions are also improving after a prolonged downturn. Battery-grade lithium carbonate traded near $18,200 per tonne in early January 2026, rebounding as grid-scale energy storage systems expand even as the global energy transition progresses more slowly than early projections suggested.

Geopolitical balancing

While US investment is accelerating project development, Latin American governments continue to balance geopolitical interests between Washington and Beijing.

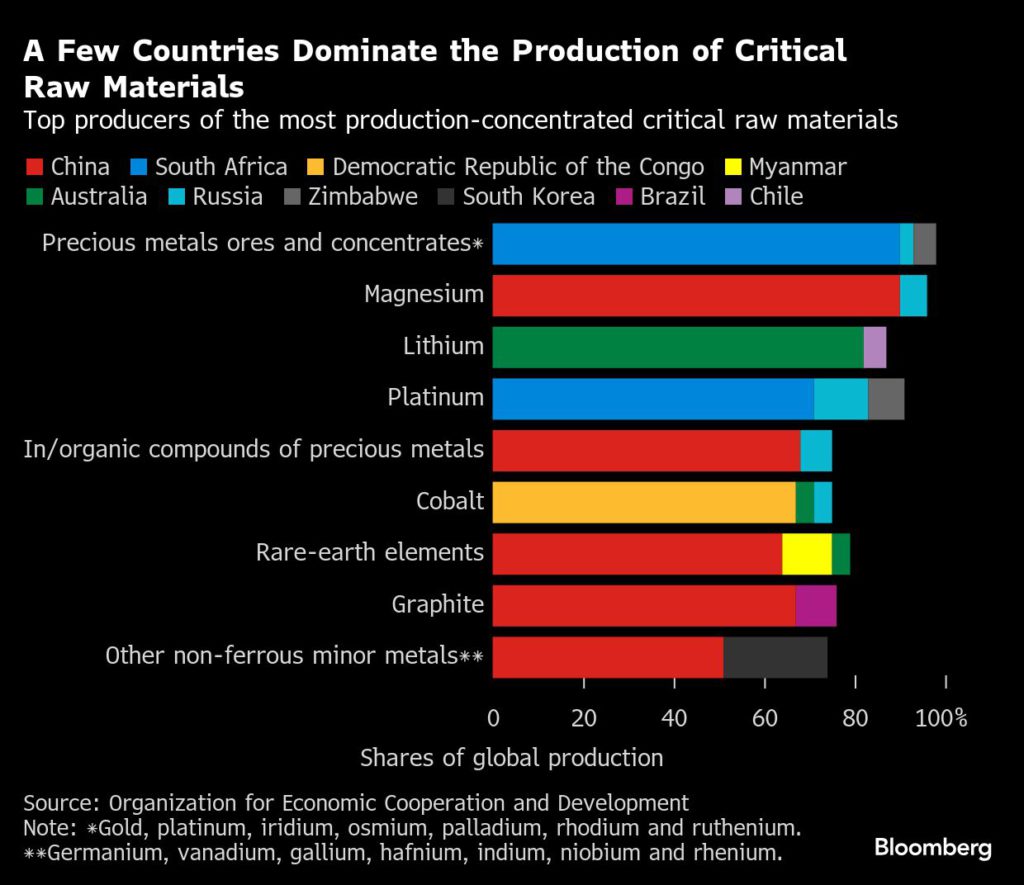

Chinese companies remain dominant in mineral processing, particularly rare earths, where more than 90% of global processing occurs in China. Campbell and de la Hoz say governments across the region remain pragmatic, welcoming investment from both sides as they seek capital and technical expertise to develop mineral resources.

Inter-American Development Bank president Ilan Goldfajn said in December that countries across the political spectrum are focused on building domestic processing capacity to capture more value from their resources.

“We are hearing from countries from left to right, independent of political inclination, that this is the moment to increase the value added to their critical minerals,” Goldfajn told the Financial Times.

Geopolitics is increasingly influencing mining transactions and regulatory approvals. Campbell and de la Hoz point to MMG’s proposed acquisition of Anglo American’s nickel assets in Brazil, now undergoing a Phase II merger review by European regulators, as an example of how decisions in Brussels or Washington can shape mining deals thousands of kilometres away.

Critical minerals are also gaining strategic importance beyond clean energy. Defence, aerospace and advanced technology sectors are driving demand for secure supply chains, prompting some mining companies in Latin America to align projects with US strategic priorities to secure financing and long-term markets.

Domestic policy changes are also reshaping the investment landscape. Argentina has moved quickly to simplify regulations and attract foreign capital, while Brazil’s reforms have been more incremental and in some cases have increased compliance requirements.

Political risk and community engagement remain key factors shaping project timelines. Resource nationalism, environmental permitting and bureaucratic hurdles continue to influence development schedules even as government-backed financing reduces some investment risk.

Copper in driver’s seat

Copper is expected to remain the primary driver of mining investment across Latin America. Chile and Argentina are advancing major copper projects as global demand for the metal — essential for electrification and power grids — is projected to nearly double by 2035.

Several copper projects in Chile alone are expected to begin operating next year with combined investment exceeding $7 billion, reinforcing the metal’s central role in regional mining strategies.

For Campbell and de la Hoz, the surge in lithium and critical minerals investment reflects a broader shift in the global mining landscape, where geology, government policy and geopolitical strategy increasingly determine where projects move forward.

———

Latin America is heading into 2026 with resources at the centre of a growing global power struggle, as governments and investors focus on who controls critical minerals and the supply chains behind them. If the region matters to you, don’t miss MINING.COM’s new series tracking the geopolitical forces reshaping it and why markets are increasingly driven by global alliances as much as local politics.

US critical minerals talks advance with EU, Japan on price floor

The US, Japan and the European Union are set to announce plans in the coming weeks to lay the foundation for a trade agreement in critical minerals, according to people familiar with the preparations.

The Office of the US Trade Representative, which has led negotiations with Brussels and Tokyo on the framework, will also head talks for a trade deal that is set to include a price floor and tariffs for the materials to counter any market distortions by China, said the people, who spoke on the condition of anonymity.

Global efforts to diversify critical minerals supply chains intensified after Beijing last year imposed sweeping export controls, including on rare earths and critical minerals, in response to President Donald Trump’s so-called Liberation Day tariffs, which set a 10% levy on nearly all American imports.

Beijing has threatened it would retaliate against the formation of a bloc that would target its exports.

The supply crunch has eased somewhat since its worst point last summer and fall, but companies still complain that they don’t receive the quantities they need and have ordered from Chinese suppliers.

US Trade Representative Jamieson Greer is aiming to start negotiations for a trade agreement with the EU and Japan in critical minerals in April, shortly after a comment period for stakeholders to weigh in ends on March 19, according to the people.

A price floor would set a minimum price for producers to incentivize investment and prevent any efforts to undercut the deal with cheaper exports from China. The Defense Advanced Research Projects Agency is lending expertise to USTR’s efforts to help come up with a pricing mechanism, the people said.

The announcement of the US-Japan plan could coincide with Japanese Prime Minister Sanae Takaichi’s visit to White House March 19, one of the people said. The EU’s timing is still being worked out but Brussels and Tokyo are closely coordinating on the contents of the plans.

The topic is also on the agenda for this year’s Group of Seven summit, the people said.

A USTR spokeswoman and Japan’s Trade Ministry declined to comment. EU spokesman Olof Gill said “the work to develop this action plan is ongoing, and the Commission is working closely with Japan, while remaining also in close contact with other global partners.”

Mexico is so far the only country that signed an action plan with the US in early February. The two sides agreed within 60 days to “discuss the feasibility and development of coordinated trade policies and mechanisms, including border-adjusted price floors for critical minerals imports, focusing in the first instance on certain select critical minerals to be determined,” according to the plan.

Provisions may include technical and regulatory cooperation, investment promotion and screening, research and development of new critical minerals technologies and coordinated stockpiling, among others.

The action plans between the EU, Japan and the US will closely resemble the document signed by Mexico, the people said.

In a joint press statement on Feb. 4, the European Commission, the Trump administration and the Japanese government said: “Such a plurilateral trade initiative could include exploring the development of coordinated trade policies and mechanisms, such as border-adjusted price floors, standards-based markets, price gap subsidies, or offtake-agreements.”

The scope of the agreement and which countries will join the push is still to be determined. Officials are assessing which critical minerals to start with and then build upon that agreement to eventually expand the scope to most or all of the minerals, the people said.

The US State Department has pursued separate bilateral memorandums of understanding with countries, including the EU and Japan.

(By Jenny Leonard)

No comments:

Post a Comment