Carney offers Italy priority access to Canada’s critical minerals

Canadian Prime Minister Mark Carney has offered Italy priority access to Canada’s critical mineral reserves as the two countries expanded cooperation on supply chains, defence and energy during talks at the G7 summit in France.

The meeting with Italian Prime Minister Giorgia Meloni in Évian builds on a year of growing bilateral engagement centred on critical minerals. Recent developments include Italian energy company Eni’s nearly C$100 million investment to secure graphite from Nouveau Monde Graphite’s (TSX-V: NMG)(NYSE: NMG) Matawinie project in Québec, Italy’s entry into the Critical Minerals Production Alliance and a series of trade and investment initiatives between the two countries.

“Italy’s intention to collaborate with Canada to stockpile critical minerals will catalyze further partnerships between our countries in energy and industry,” the Canadian government said in a statement.

Meloni thanked Carney for his decision to grant Italy priority access. The statement added the Canadian move would help safeguard supply chains.

Core supplier

The agreement highlights Canada’s efforts to position itself as a strategic supplier of minerals essential to battery manufacturing, defence technologies and industrial production as Western allies seek alternatives to concentrated global supply chains. The move also strengthens economic ties between Ottawa and Rome at a time when G7 countries are working to secure access to critical resources and reduce geopolitical vulnerabilities.

The leaders also launched negotiations for Canada’s purchase of Leonardo M-346 advanced jet trainer aircraft. Ottawa said the proposed acquisition would strengthen the Royal Canadian Air Force’s training capabilities while advancing its Defence Industrial Strategy through partnerships with trusted allies. Carney also highlighted plans for a new Defence, Security and Resilience Bank aimed at financing long-term defence and security projects.

Beyond economic and defence cooperation, Carney and Meloni reaffirmed support for Ukraine and agreed on the need to maintain pressure on Russia to achieve a lasting peace. The leaders also discussed developments in the Middle East and agreed to remain in close contact.

INSIGHT: Trump’s critical minerals pricing plan faces skeptical G7, divided industry

The Trump administration’s push to boost critical minerals production by regulating prices is facing skeptical G7 allies and a divided mining industry, with negotiations for a Western trading bloc stumbling over concerns about the plan’s cost and governance, according to diplomatic sources and a Reuters analysis of corporate policy recommendations.

First proposed by US Vice President JD Vance in February, the trading bloc aims to help the West wean itself off China, which became the world’s largest minerals producer by operating at a loss and dampening prices for the building blocks of semiconductors, computer servers, military equipment and myriad other products.

Artificially low prices for cobalt, lithium, nickel and other minerals have made it harder for Western mining rivals to compete, inhibiting new development and driving some companies out of business — a tactic Beijing has used repeatedly in other industries.

The trade bloc, as envisioned, would explore price supports, market standards, subsidies, or guaranteed purchases to encourage and financially underpin production across multiple countries. The measures could be enforced by “adjustable tariffs to uphold pricing integrity,” Vance said at the time.

At present, many niche minerals critical to tech and defense are traded over-the-counter with minimal transparency and linked to Chinese prices, which de facto set the global market due to China’s dominant production.

Since Vance’s announcement, G7 members have pushed back against US Trade Representative Jamieson Greer in private negotiations and cooled on the idea of the bloc relying on a price scheme derived from a Pentagon AI model, three sources told Reuters.

Key concerns center around who would pay a premium for minerals, how far down the supply chain those subsidies should go and how governance would work, according to European officials.

The US mining industry is divided on what steps Greer should push allies to support, a disagreement that is clear from more than 230 public submissions sent to Greer’s office by a range of miners, refiners and their customers reviewed by Reuters.

Allied and corporate concerns underscore the complexity of reinventing the way minerals are bought and sold. Yet how and whether the trade bloc ultimately shapes out could influence minerals markets for years to come, more than a dozen analysts and consultants told Reuters.

“It is a very hard thing to do, and I’m happy I’m not the one doing it,” said Ashley Zumwalt-Forbes, a minerals investor who ran the US Department of Energy’s batteries and critical minerals portfolio under former President Joe Biden.

The topic will be a key talking point as G7 members meet this week in France. Western countries face the difficult task of building up a supply chain from mine to end product all at once to diversify away from China.

The draft US proposal, crafted using an AI pricing program created by the Pentagon’s Defense Advanced Research Projects Agency (DARPA), has been delivered to the White House and the National Security Council and US representatives are expected to brief G7 allies on its contents in the upcoming meeting, according to a US official.

European and industry officials said they want to study the impact of price supports on the medium and long-term rather than commit to quick deals — at odds with the faster-paced Americans.

The Trump administration, meanwhile, is reluctant to embrace the idea pushed by France of a permanent administrative secretariat within the International Energy Agency (IEA) or OECD to track G7 initiatives on critical minerals as presidencies rotate, the sources added.

Adding to complications, Canada and France — which holds the G7 presidency — want to develop a trading bloc led by the G7 whereas the United States wants to avoid multilateral negotiations and forge fast concrete bilateral deals, and later expand them, three sources familiar with the matter said.

The push for a bilateral approach from Washington appears to indicate a shift in strategy from the plan first outlined by Vance earlier this year.

“What we’re trying to do is take some of these approaches and turn them into an agreement,” Greer told reporters in early June at the Organisation for Economic Co-operation and Development (OECD) ministerial meeting in Paris.

The United States, Greer said, would use price supports “to protect production of critical minerals and derivative products. … We want to phase it in. … If other countries want to join us in that, they’re welcome to do that.”

Washington aims to present a proposal for binding bilateral agreements to Japan and the European Union before the end of June, two sources familiar with the matter said. The proposal would be the first concrete step built on action plans announced earlier this year, one with Japan and the other with the EU.

The first binding agreement could extend to five to 10 minerals, the sources said. The minerals under consideration include heavy rare earths, antimony, graphite and tungsten, all subject to Chinese export bans or restrictions.

Price setting

The Trump administration aims to set prices using the US Department of Defense’s Open Price Exploration for National Security (OPEN) AI metals program, which was created by DARPA and aims to calculate what a metal should be priced at when labor, processing and other costs are factored in, while alleged Chinese market manipulation is factored out.

But European allies so far are opposed to the idea of using an AI pricing system developed by Washington, one source said, citing concerns about the US having too much sway over the bloc’s pricing.

Another person added that Europeans want a broad set of tools and “agile governance” around how best to deploy these measures for any given mineral and its value chain.

“For Europe, it would be better to have a price index based on real deals in the European market. The question is whether we can make these opaque pricing mechanisms more transparent, more market-driven, and less prone to manipulation,” Nicola Beer, who oversees minerals financing at the EU-controlled European Investment Bank, told Reuters.

“Different parts of supply chains and products across sectors are shaped by very different pricing mechanisms, which adds to the complexity.”

As a possible alternative to OPEN, an EU-funded agency called EIT RawMaterials is working with digital platform Metalshub to create indexes outside Chinese government-led pricing to give foreign investors clearer signals on profitability. The indexes could be broader than Europe and include the United States, Australia, Canada or Britain.

Enforcement on any trading bloc could be complicated by the fact that many Western nations import very few minerals in their raw or lightly processed form. Lithium carbonate, for example, is not routinely imported to the US, though cell phones made from it are.

“There’s a very mixed message coming out of the US right now on battery metals,” said James Willoughby, a metals analyst at the WoodMac consultancy.

Corporate disagreement

In a statement, Greer told Reuters he was using the submissions sent by miners and their clients to “help guide policy for continued negotiations” with Washington’s allies.

The submissions show respondents broadly agree that the bloc should focus on niche minerals rather than copper or other widely traded metals and that it should also focus on downstream products, including cell phones and laptops.

Yet they disagree on how minerals prices could be regulated, with several prominent companies and mining trade groups recommending against price setting.

“There’s nervousness from all sides about what to do and how different actions could affect different parts of the supply chain,” said Blake Harden, a managing director focused on trade policy at the EY consultancy.

Divergent proposals came from General Motors, which is building North America’s largest lithium mine with Lithium Americas, recycler Umicore, platinum miner Sibanye Stillwater, the US Chamber of Commerce, and rare earths company MP Materials — which last July became the only company to receive a financial backstop for its rare earths in which Washington funds the company if prices fall below a certain level. Lynas Rare Earths and Serra Verde have received off-takes for part of their rare earths production from the US government at a set price, although they did not receive the financial backstop.

The National Mining Association, the US industry trade group, advised Greer to steer away from too much price-fixing and instead focus on tax credits and other incentives.

“While market interventions such as pricing mechanisms may play a role in certain circumstances, incentive-based approaches … are better suited to addressing challenges facing the domestic mining industry,” said Rich Nolan, the trade group’s CEO.

(By Julia Payne, Ernest Scheyder, Leigh Thomas, David Lawder and Jarrett Renshaw; Editing by Veronica Brown and Claudia Parsons)

Op-Ed: Scripted to fail — Europe’s critical minerals blind spot

Europe’s ambitions for critical raw materials are clear. The continent wants to become acceptably self-sufficient in mining, processing, and recycling. Yet, when confronting global competition, the narrative is invariably self-defeatist: “We lack China’s mineral processing capacity.” “We lack America’s investment trade leverage.” “We lack the vast resource endowment of Africa, Australia, and South America.”

If Europe finds itself struggling to secure the materials required for the energy transition, the narrative often tends toward simply being outmatched.

But this explanation is fundamentally flawed. Europe’s critical minerals bottleneck is not a crisis of capability. It is a systemic choice. Europe has the tools, it simply chooses not to deploy them.

Let’s call it what it is: Scripted Innovation Each year, the European Union spends approximately €380 billion annually on research and development (R&D). There is ample evidence to show that every euro invested generates up to 1100% in total economic return.

As home to world-class universities, research institutes, engineers, and scientists, Europe certainly has the intellectual capital needed to compete. Yet despite this, Europe repeatedly finds itself reacting to technological and industrial developments rather than shaping them.

The question is why?

Part of the answer lies in how Europe chooses to fund innovation. Over the past two decades, European research funding has become increasingly mission-oriented, directing funding strictly toward predefined objectives: climate action, energy efficiency, digital transformation, circular economy initiatives, and other strategically important goals.

Of course there is nothing inherently wrong with this approach, and in many respects, it has been highly successful. But mission-oriented funding excels at solving recognised problems. The thing is, truly transformative innovations almost always emerge from problems that have not yet been recognised (it’s the very definition of novelty). By forcing innovation to stay safely within preferred thematic boundaries, Europe creates a framework that struggles to accommodate the unpredictable, out-of-the-box experimentation where real novelty is born.

Case in point: Looking at recent innovations in sodium-ion batteries, which are attracting massive industrial interest as a way to bypass lithium constraints. Imagine proposing a major sodium-ion battery program twenty years ago, when lithium-ion technology was already emerging as the dominant pathway for energy storage. Many evaluators would have reasonably questioned the logic of investing in an “inferior alternative” to lithium.

From the perspective of the time, such scepticism would have been entirely rational. The problem is that innovation does not operate according to today’s assumptions. Technologies that look redundant or commercially irrelevant suddenly become strategic lifelines when geopolitics shift, supply chains become concentrated or market conditions change.

Efficiency vs. optionality

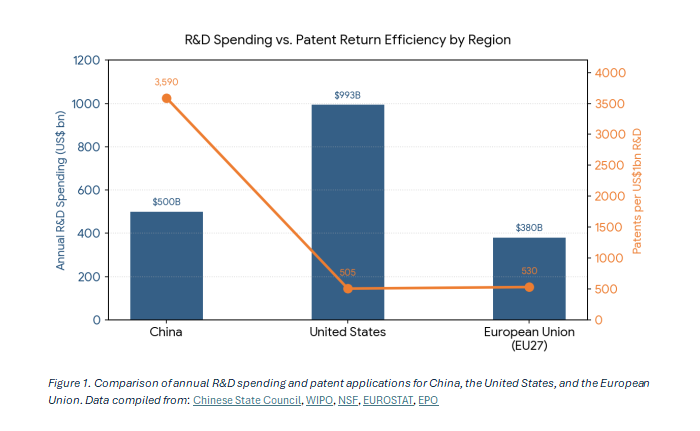

This structural divergence between Europe’s scripted alignment and a more open-ended approach is laid bare in global patent and R&D data (Figure 1). The numbers expose the literal cost of choosing efficiency over optionality.

On an equivalent R&D spend of roughly $500 billion, China’s ecosystem shatters the curve, yielding nearly 1.8 million patent applications. That translates into more than 3,500 patents per $1 billion invested in R&D, or 250% more than the European Union and United States combined!

Naturally, critics like to dismiss this towering patent volume as a symptom of low-quality, low-scrutiny filings. Speak to any researcher, and they can point to the relentless trove of suspicious journal invitations and mass-produced papers in their spam folder as proof of this volume-first approach.

It is easy to look at that noise and assume the patents are no different. But dismissing this as mere “low-quality padding” is a massive (and expensive) strategic error. When viewed through the lens of industrial strategy, this metric tells us something else entirely. It is the literal cost that every taxpayer pays for optionality.

For China, it’s a clear numbers game. Absorb the economic inefficiency of thousands of speculative, redundant filings to ensure that when a global shift occurs, you already hold the keys to success. In contrast, by forcing research to pass through rigid policy filters, Europe may clear away speculative “waste”, but it accidentally filters out the very redundancy needed to catch tomorrow’s surprise bottlenecks.

The reality of control

Critical raw materials provide perhaps the ultimate proof of this blind spot. Two decades ago, graphite processing, rare earth separation, lithium refining, and battery precursor supply chains occupied almost no space in mainstream European policy discussions. Today, they sit at the absolute centre of industrial strategy, defence planning, and geopolitical competition.

China invested heavily in many of these capabilities long before they became fashionable. Europe largely did not. As a result, Europe became highly innovative in technologies that use critical raw materials, whilst China became highly innovative in technologies that control them.

The distinction matters. Control over supply chains rarely comes from discovering a new metal. More often, it comes from investing in capital-intensive engineering challenges like processing, refining, separation and recycling. These activities aren’t always viewed as glamorous, and they certainly don’t fit traditional definitions of “breakthrough innovation”, but innovation itself is a dynamic concept that changes with need.

The bottom line

This raises an uncomfortable question for European policymakers. Have we become too focused on funding what appears innovative today, whilst overlooking the foundational capabilities that may become strategically decisive tomorrow?

Europe does not suffer from a lack of talent, scientific excellence, or capital. It suffers from a narrowing definition of innovation itself. Millions of brilliant minds working on a script written by a few.

In a game where every investment yields truly exponential economic returns, the real winners will not necessarily be those who best solve today’s problems, but those who buy enough optionality to recognize tomorrow’s unscripted opportunities.

Dr. Nicholas Vafeas is an economic geologist specializing in critical raw materials, mineral supply chains, and energy policy.

No comments:

Post a Comment