AU

Singapore to launch gold clearing with JPMorgan, other banks

Singapore plans to launch a gold-clearing system this year, with banks including JPMorgan Chase & Co. and Deutsche Bank AG set to participate in the city-state’s push to become a hub in the global bullion market.

The Singapore Exchange will establish the over-the-counter clearing mechanism by the end of 2026, with inter-bank trading expected to build up from next year, said Gan Kim Yong, the country’s deputy prime minister and chairman of the Monetary Authority of Singapore.

“We are not seeking to replace established centers of gold trading and liquidity,” he said at the Asia-Pacific Precious Metal Conference on Monday. “Instead, Singapore can serve as a trusted node in the global gold ecosystem – connecting regional demand with global liquidity and supporting market activity during Asian hours.”

Singapore’s latest move intensifies competition with Hong Kong to become a major regional hub for trading gold. In recent months, both cities have advanced plans to capitalize on strong demand for the precious metal, with many banks remaining bullish about the long-term prospects for an asset coveted by investors as an alternative store of wealth.

Hong Kong’s central clearing system is expected to be ready by July and the special administrative region has signed up five Chinese and six international banks.

The new clearing system in Singapore will serve as “a foundational layer for the clearing and settlement of gold flows during Asian trading hours,” said SGX Group chief executive officer Loh Boon Chye. “We are also exploring a physically deliverable gold futures contract to give the market an exchange-based tool for price discovery and risk management.”

In Singapore, DBS Group Holdings Ltd., Oversea-Chinese Banking Corp., United Overseas Bank Ltd. and ICBC Standard Bank Plc, as well as JPMorgan and Deutsche Bank, will take part as clearing members after signing a memorandum of understanding with the Singapore Exchange at the conference on Monday.

“As investor demand for global gold grows, we see Singapore playing a complementary role alongside other major hubs by supporting liquidity across time zones and meeting evolving client needs,” said Wai Mei Hong, JPMorgan’s Singapore senior country officer.

The clearing system will be aligned with the industry-standard London Good Delivery framework for large bars, as well as delivery and settlement standards for kilobars adopted by major exchanges in Chicago and Shanghai.

“The gold market works best when liquidity and infrastructure are connected across regions,” Deputy Prime Minister Gan said. “With an established clearing infrastructure and strong market ecosystem, Singapore can support a more seamless global market across time zones – from Asia, to Europe, to the Americas.”

MAS will also introduce central bank gold vaulting services by October this year, he said, and will allow foreign monetary authorities to actively manage bullion holdings with a select group of banks based in the city-state. Attracting sovereign reserves would significantly boost liquidity in the local market and strengthen Singapore’s standing as a global trading center.

The central bank is also set to expand tax exemptions for eligible funds and family offices investing into physical investment precious metals, Gan said, referring to a specific technical term on the purity and form of gold.

As the government pushes to strengthen Singapore’s gold sector, some local banks are also rolling out products to meet growing demand. DBS, the city-state’s biggest lender, will allow customers to hold tokenized gold in the second half of the year. Meanwhile, institutional and high-net-worth clients of OCBC can now trade and store gold with the bank.

(By Yihui Xie)

London gold market weighs earlier auction to suit Asian traders

The London Bullion Market Association is considering moving its morning gold auction to an earlier time to accommodate traders in Asia.

The potential shift would be “to reflect and to allow price discovery within the Asian time frame,” LBMA chief executive officer Ruth Crowell said on Monday. This is “something that I know the market has asked for for many years, but I think it comes at the right time,” she told the Asia-Pacific Precious Metal Conference in Singapore.

Crowell did not specify a new time or times under consideration, or say when the possible change might occur.

The LBMA Gold Price is currently set twice daily, at 10:30 a.m. and 3:00 p.m. London time, in US dollars on an electronic platform. The price is the benchmark used by miners, refiners, investors and central banks worldwide.

A daily London pricing auction was first introduced in 1919, with a second, afternoon auction added in 1968 to reflect growth in the US market. The current benchmarks replaced the old London Gold Fix, a telephone-based system that was discontinued in 2015.

The potential shift to an earlier London auction underscores the growing weight of Asian demand in the global bullion market. Gold has been thrust into the spotlight as geopolitical tensions and trade uncertainties drive central banks and investors toward the metal as a safe haven, with the spot price soaring to a record earlier high this year before retreating after the outbreak of the US-Iran war.

(By Yihui Xie and Preeti Soni)

Gold fever sends some vintage luxury watches to the melting furnace

Omega’s Constellation watch has been flashed in campaigns, movies and at the Met Gala by stars like George Clooney and Nicole Kidman, turning it into a symbol of luxury and glamour.

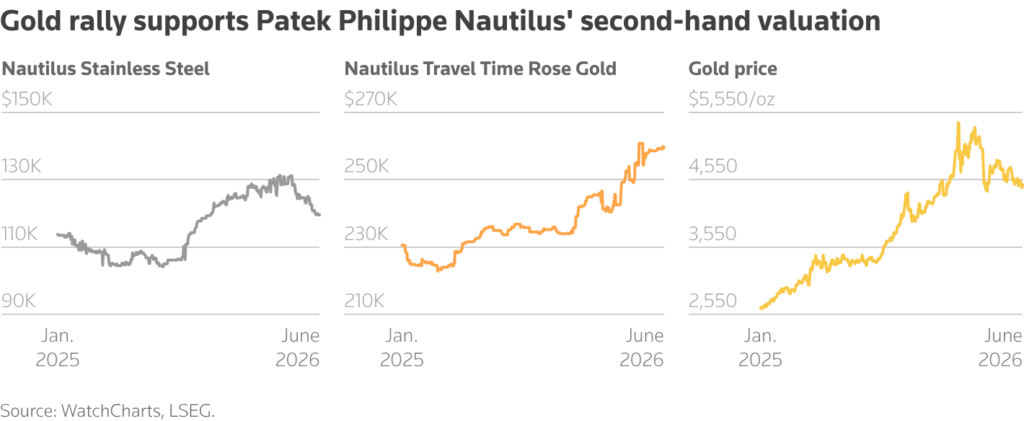

But with gold prices near record highs struck in January, some such classic watches are being melted down as the value of their metal content outstrips their resale worth.

Used models by the likes of Omega and LVMH’s TAG Heuer are most hit by the trend, according to Reuters interviews with over a dozen traders, industry experts, and investment advisers.

British dealer Jon White of Gold Traders melted down an 18-carat late-1970s Constellation in excellent condition in May, one of dozens of mainstream luxury watches he has had scrapped this year as demand for investment gold has risen.

“Beautiful watch. But in reality, had the customer consigned that to auction, what would they have achieved?” White, who also manages an auction house, told Reuters.

The gold content of the Constellation watch, one of many models produced by Swatch-owned Omega, was worth £5,750 ($7,749), 35% more than its estimated £4,000-4,500 auction value, White said.

James Lamdin, founder of Watches of Switzerland’s second-hand unit Analog Shift, said melting was “primarily happening with contemporary pre-owned and also with older vintage watches that are not already collectible.”

Spokespersons for Swatch and Rolex said they would not comment for this story. LVMH, Richemont, Patek Philippe and Audemars Piguet did not respond to requests for comment.

Liquid gold

Gold prices surged to a record $5,600 an ounce in January as geopolitical concerns and trade worries pushed investors towards safe-haven precious metals. Gold now hovers around $4,200 per ounce, almost double its 2024 average.

The market price for used watches has not moved in the same way, however.

“I find it very sad, because obviously once something has been melted, it’s gone forever,” said Adrian Hailwood, a specialist in horological history.

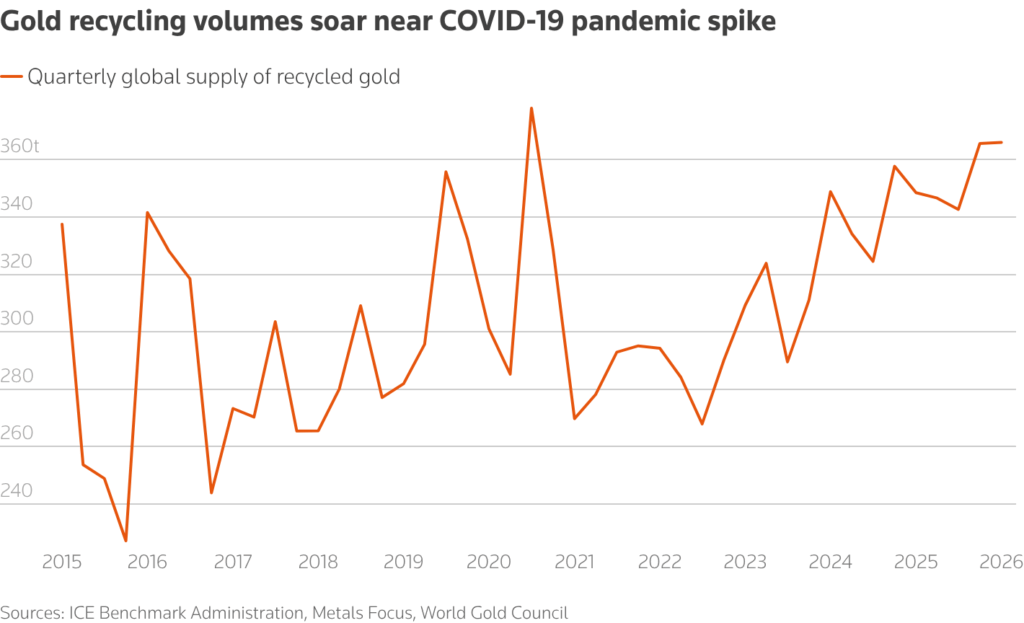

There are no official figures showing how many luxury watches are being melted. World Gold Council data shows overall gold recycling in the first quarter rose 5% to 366 tonnes, while gold jewellery demand rose 31% in value to $47 billion.

Watches can hold anything from a sliver of gold to more than 200 grams, meaning their scrap value can run into tens of thousands of dollars. In an Omega Constellation, the gold can be found in the case and the strap.

With gold expected to reach between $5,400 and $6,300 an ounce this year, the pressure to dismantle some watches will continue, especially as traders that resell them must cover costs and the expense of providing a warranty.

New watches that are over-produced might also be melted down.

“I’ve seen a lot of totally mediocre watches get melted down,” said Lamdin. “There’s a lot of unsold overstock in the Swiss market. And those watches are basically brand new, unworn, and they’re just getting stripped down… they made too many of them.”

“But when you have something that’s vintage and rare and has some story or some patina, that’s where it becomes a short-sighted tragedy.”

The resale trap

High-end brands that tightly manage new production like privately owned Patek Philippe and Rolex command the highest premiums over melt value, three industry experts said.

For some models “the wait lists are astronomical. You’re talking anything from two to eight years,” said Simon Lazarus, head of PR and content at online luxury watch platform Chrono Hunter.

Rolex accounted last year for 61% of the sales value of new Swiss watches priced above 3,000 Swiss francs ($3,770), up from 57% in 2023 despite lower volumes, according to Vontobel.

Less exclusive brands like TAG Heuer, Breitling and Omega struggle to command high new retail prices, however, as buyers can buy a second-hand timepiece for much less.

Models like Omega’s Speedmaster often depreciate sharply once sold, exposing them to scrapping, three experts said.

To sell or not to sell

Higher gold prices motivated retired New York engineer Mitchell Talisman to sell two gold watches and a chain containing a combined 35 grams of gold with 58% purity for $2,660 cash in December.

“I’d had a bunch of stuff sitting in a safety deposit box for over 10 years,” he told Reuters.

For some owners however, the idea of selling a watch only for it to be melted by a dealer is too much to bear.

“It may be a family piece, it may be their first watch,” said Hailwood.

“They don’t like the idea of it being destroyed, so they keep it.”

($1 = 0.7421 pounds)

($1 = 0.7873 Swiss francs)

(By Alessandro Parodi; Editing by Lisa Jucca and Alexandra Hudson)