It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Thursday, July 02, 2026

SK and KKR Form $1.3 Billion Renewable Energy Platform in South Korea

SK Inc. and private equity firm KKR have agreed to establish what the companies describe as South Korea's largest renewable energy platform, combining solar, wind, and fuel cell assets into a KRW 2 trillion ($1.3 billion) business aimed at supplying clean electricity to the country's rapidly growing industrial sector.

Under definitive agreements announced Tuesday, funds managed by KKR and SK will consolidate renewable energy assets previously owned by several SK affiliates, including SK Innovation, SK ecoplant, and SK eternix, into a single integrated platform. KKR will initially hold management control, while SK will remain an equity investor with the option to pursue control rights in the future.

The platform will launch with approximately 1.7 gigawatts of operating renewable energy capacity and a development pipeline that could expand total capacity to 10 GW. According to the companies, that level of generation would be sufficient to continuously power around 100 large-scale data centers with 100-megawatt capacity each.

The portfolio spans solar, onshore wind, offshore wind and fuel cell projects, excluding hydrogen, and is intended to integrate the full renewable energy value chain from project development and construction to operations and maintenance.

The investment comes as South Korea faces rising electricity demand driven by the expansion of AI data centers, semiconductor fabrication plants and other energy-intensive industries. Growing corporate demand for clean power has also increased interest in renewable generation as companies seek to meet decarbonization targets while securing reliable electricity supplies.

KKR said the investment will be funded primarily through its Asia Pacific infrastructure strategy. The firm has invested more than $31 billion in energy transition and renewable infrastructure globally since 2011 and has backed similar industrial clean energy platforms across the Asia-Pacific region, including India's Serentica Renewables and Australia's CleanPeak Energy and Zenith Energy.

For SK, the transaction forms part of a broader portfolio restructuring designed to improve capital efficiency while strengthening its renewable energy business. The company said combining its renewable assets with KKR's capital and infrastructure expertise would help position the platform to meet long-term demand for clean electricity in South Korea's industrial sector.

The deal also deepens an existing relationship between SK and KKR, which have previously collaborated on multiple investments. Financial terms beyond the platform's overall valuation were not disclosed.

By Charles Kennedy for Oilprice.com

Op-Ed: The decoy effect — how Beijing steers western mining capital

Sometimes the thing everyone is looking at isn’t the thing that matters most. AI-generated stock image by Nicholas Vafeas .

It’s no secret that I, like many, have a habit of assuming that when China makes a policy move, the topic is almost never the goal. It’s a masterclass in misdirection.

Have you ever heard of the Decoy Effect?

Imagine this. You walk into a coffee shop, and you’re presented with two options: a small cup for $2 or a large for $4. You don’t really need that much coffee, so you settle on the small. Then the barista casually mentions there’s also a medium for $3. Suddenly, the medium seems like the sensible choice because it’s only $1 more. But then you think, “well, if I’m already willing to spend $3, I may as well spend $4 and get the large.” See what happened there?

You weren’t really given more choice. Your perception of value was manipulated. It’s a fairly well-known psychological sales technique. Now consider it in geopolitics.

Every time China’s Ministry of Commerce (MOFCOM) updates its export licensing catalogue, expands its dual-use controls, or announces a new regulatory framework, Western media rings the alarm bells. The response from Washington, Brussels, and Canberra is entirely predictable: a reactive rush of state-backed subsidies, emergency stockpiling, defensive capital injections into any project with a halfway decent drilling result, and countless Op-Eds about China’s dominance (the irony is not lost on me).

But what if we’ve been focusing on the wrong problem? What if the threat of scarcity isn’t the strategy at all, but the decoy? Whilst Western governments scramble to defend themselves against the possibility of restricted supply, consumed by “focused discussions” and “strategic talks”, Beijing is busy deploying its real weapon, the one nobody notices: aggressive oversupply.

The asymmetric weapon

The beauty of a good decoy isn’t that you believe it, it’s that it stops you from paying attention to anything else. By periodically rattling the sabre of export restrictions, such as the recent targeting of Western upstream producers like MP Materials and USA Rare Earth, Beijing deliberately keeps geopolitical anxieties at a boil. Governments and investors naturally interpret the problem as one of access, encouraging policies centred on securing raw material supply.

Ignore the regulatory theatre and look at the actual pricing. Across much of the critical minerals midstream, pricing has been under relentless pressure. Lithium, cobalt and nickel prices have fallen sharply from their post-pandemic highs, whilst treatment and refining charges for metals such as copper and nickel have been squeezed as processing capacity has expanded faster than raw material supply. Coincidence?

Figure 1. Price trends for lithium, cobalt, and nickel from mid‑2022 to mid‑2026, showing sharp declines relative to their post‑pandemic highs (Source: Tradingeconomics.com).

Sure, market cycles undoubtedly play a role, but it would also be naïve to ignore the role industrial policy can play in shaping those markets. China has spent decades expanding processing capacity, supporting domestic refiners and backing major overseas projects (from Indonesian nickel to domestic rare earth separation hubs). This raises a more strategic possibility: that oversupply has itself become an instrument of industrial policy.

The decoy (i.e. the loud threat of a ban) keeps the West focused on exploration and securing raw supply. Meanwhile, the reality (persistently weak prices) ultimately starves alternative refining capacity of the private financing it needs to exist in the first place. After all, no private equity fund or commercial bank can honestly justify financing a multi-billion-dollar refinery when a state-backed competitor can comfortably dump refined material onto the market at a whim, well below Western operating costs.

That is market capture 101. This decoy nudges the West to waste its capital on upstream exploration, whilst oversupply ensures that nobody else gets to refine it.

The fallacy of linear substitution

This brings us neatly to the core flaw of the West’s standard defensive response: I call it the “fallacy of linear substitution”. The logic goes something like this: “If we mine one tonne of critical minerals in an allied country, we have successfully replaced one tonne of Chinese supply.” It sounds perfectly reasonable, but it also completely misses the point. Critical minerals are not liquid, generic commodities like crude oil in the 1970s. There is no allied critical minerals “cartel” to help maintain stability and control. They are highly integrated, highly bespoke chemical, metallurgical and manufacturing value chains.

The recent G7 Critical Minerals Alliance meetings in Evian highlighted a rather belated realization that Western projects cannot compete on pure geology or raw operational efficiency when pitted against a state-backed monopoly that sets the reference price.

By the time a mining project has fought its way through the five-to-ten-year permitting, financing and construction process, the Chinese supply machine has already adjusted the global price floor to ensure the new entrant can never service its debt. The hole in the ground becomes a stranded asset before it even achieves commercial scale.

And I’ll give you one guess who picks up that stranded asset for pennies on the dollar. It’s a cycle that has been playing out for years and one which most of us have watched in real time.

Breaking the cycle

If the West wants to escape this scarcity trap, it must stop reacting to Beijing’s administrative theatre and start targeting its economic leverage.

Funding more extraction is a pointless exercise if the resulting material is destined to drown in a flooded, uncommercial global market. Genuine supply chain resilience requires moving beyond basic mining grants toward robust market-insulation mechanisms. “Sew the bag before you collect the marbles”.

Investors must decouple the strategic value of processing capacity from volatile, spot-market commodity prices. The capacity to refine must be valued as long-term security, not a cyclical mining play (granted, this is something that would almost certainly need the support of national policy).

From an industry and societal perspective (this is a personal point of contention), we must become far more serious about material retention. Every gram of refined critical metal already inside the allied economy should be treated as a permanent strategic asset. Once it enters the system, the goal should be simple. Never let it leave!

So, just as you leave that hypothetical coffee shop holding a large cup, feeling rather grand with yourself for spending “only $1 extra”, the West will continue to chase a supply chain mirage until we recognize that China’s primary weapon is the decoy effect. The danger isn’t that China will refuse to sell us these minerals. It’s that it will sell them so cheaply that we never build the capacity to refine them ourselves.

By the time the coffee shop closes, we’ve forgotten how to roast the beans.

* Dr. Nicholas Vafeas is an economic geologist specializing in critical raw materials, mineral value chains, and strategic resource policy.

EU unveils new steel import quotas to protect its industry from overcapacity

Rolls of galvanized steel sheet inside the factory or warehouse. Stock image.

The European Commission unveiled quotas under the new system to limit duty-free steel imports into the EU, in a move designed to protect the bloc’s steel sector and increase its capacity utilization.

Under the new rules, the European Union’s annual tariff-free import quotas are slashed by 47% to 18.3 million metric tons, while an out-of-quota duty of 50% is introduced for 26 categories of steel products imported into the EU.

The rules, which come into effect on Wednesday, seek to increase steel capacity utilization in the bloc to 80%, the Commission said.

European steel association Eurofer, however, said the change in rules may only raise capacity utilization to 73%-75%, up from around 67% now, given slow demand.

EU steelmakers are likely to claw back some 15 million metric tons of production, Axel Eggert, Eurofer’s director general said, about half of what has been lost over the past few years.

Half of the import quotas have been reserved exclusively for free-trade agreement (FTA) partners, with the other half available to all trading partners, including those with an FTA.

Many of those partners will receive country-specific quotas proportionate to their historic volumes, the Commission added.

“Most of the EU’s FTA partners will therefore see a market access reduction significantly lower than the average reduction of 47% foreseen by the Steel Regulation,” it said.

A “significant number” of partners have provisionally agreed with these allocations, the Commission said.

The Commission said the rules were needed to protect the European steel industry from overcapacity elsewhere in the world and dumping practices.

“Persistent global overcapacity in the steel sector remains a serious global problem and continues to distort international markets,” it said.

“The measure restores fair competition in a market affected by distortions linked to overcapacity,” it added.

To have a more significant effect on the steel industry, the measure may need to be extended to downstream sectors, such as companies laminating steel or stamping sheets out for cars, Eggert at Eurofer said.

(By Bart Meijer, Phil Blenkinsop, Inti Landauro and Hugo Lhomedet; Editing by Sudip Kar-Gupta and Susan Fenton)

Europe’s top steelmakers warn against weakening carbon market

The European Union’s biggest steelmakers, including Salzgitter AG and SSAB AB, urged policy makers to avoid weakening the bloc’s flagship emissions market and to support strengthening its carbon border levy.

Dampening the EU Emissions Trading System would erode investment certainty, penalize companies that decarbonize faster and delay the industry’s transition of to clean energy, the steelmakers said in a statement on Tuesday.

The warning — which was also endorsed by Outokumpu Oyj, Saarstahl AG, Dillinger and SHS — comes two weeks before a key reform of the so-called EU ETS 1, which some governments and companies criticize for boosting Europe’s stubbornly high carbon prices and hurting competitiveness.

“The primary pressure on competitiveness comes from high electricity costs due to fossil fuel dependencies, infrastructure gaps and global steel overcapacity, not from carbon prices,” the steelmakers said.

The carbon market review is set to be unveiled by European Commission on July 15 to adjust the ETS to a new 2040 climate goal of reducing emissions by 90% from 1990 levels.

For the steel companies, the reform should preserve the carbon price signal by keeping the pace of annual emission reduction in the system at 4.4% to at least 2035 and avoiding measures to artificially increase the supply of allowances.

They also want the EU to maintain the trajectory for phasing out free allowances when gradually introducing the Carbon Border Adjustment Mechanism, which is meant to ensure a level playing field for local producers against rivals from countries with weaker climate policies.

“A strong ETS1 combined with a robust and fully implemented CBAM can reinforce Europe’s competitiveness, resilience and industrial renewal,” the steelmakers said. “To make this transition investable, revenues must be channeled back into industrial decarbonization, with a particular focus on CBAM sectors.”

(By Ewa Krukowska)

US to suspend some duties on phosphate fertilizer from Morocco

Excavator collects red potassium agricultural fertilizers in warehouse. Stock image.

US President Donald Trump has authorized the temporary suspension of certain duties on phosphate fertilizer imported from Morocco, the White House said on Monday, as farmers grapple with shortages due to the Iran war.

White House economic adviser Kevin Hassett said in March the Trump administration was seeking more sources of fertilizer. Supply from major producers in the Middle East was sharply cut by the closure of the Strait of Hormuz.

“Global supply chains for phosphate fertilizer and fertilizer inputs, including imports of such products into the United States, have been disrupted in recent months by, among other things, conflicts in fertilizer-producing regions as well as trade actions taken by major fertilizer-producing countries,” Trump said in a proclamation released by the White House.

Currently, US production of phosphate fertilizer is insufficient to support domestic agricultural food production after accounting for exports, Trump said in the proclamation.

The Trump administration is working with the private sector to expand domestic fertilizer manufacturing capacity, but those efforts will take time to increase the supply materially, the president said, adding producers in countries like Morocco can supply phosphate fertilizers to the US without disruption at this time.

Trump declared an emergency in the proclamation that he said authorized the temporary suspension of certain anti-dumping and countervailing duties in connection with imports of phosphate fertilizer from Morocco for eight months or until the emergency is terminated, whichever occurred first.

After the US and Israel attacked Iran on February 28 and Iran responded by attacking Israel and Gulf states that host US bases, the conflict severely disrupted fertilizer markets that analysts warned endangered food security for developing countries. Much of the world’s fertilizer is made in the Middle East.

(By Kanishka Singh; Editing by Costas Pitas, Sonali Paul and Neil Fullick)

A bomb apparently targeting Ecuador’s mining regulator blew out several floors of windows at a major government building in the capital of Quito early Monday morning.

The agency, known as Arcom, was attacked “because of the changes being done regarding illegal mining,” Agriculture Minister Juan Carlos Vega said in a voice message. “It also affected public media and the ministry of agriculture,” he added. “And it broke windows in almost the first five floors of the ministry.”

It’s the second blast in recent weeks affecting Arcom offices. A June 12 attack damaged the regulator’s building and nearby homes in Machala, in southwest Ecuador. The government is increasing Arcom’s budget amid a domestic war on drug gangs that are also heavily involved in illegal gold mining.

No people were injured in the blast in Quito’s north-central business district at about 2:50 a.m. local time, Vega said. A car was found engulfed in flames several blocks away at approximately the same time, near a key tunnel that links the area with eastern suburbs, according to local media.

(By Stephan Kueffner)

Ferrari and BMW join Tesla, China in switch from copper to cheaper aluminum

Ferrari and BMW are rolling out new models featuring lightweight, cost-effective aluminum wiring, accelerating a shift away from copper, the dominant material in electric wiring since the invention of the electric battery two centuries ago.

The decisions follow similar moves by Tesla and Chinese EV makers and reflect a broader industry trend forecast to affect around 2% of global copper demand this year, according to JPMorgan.

Even more copper could be switched to aluminum in the coming years because of a structural rise in copper prices, driven by shortages of the metal and with increased demand from the green-energy sector and data centres.

Companies across several sectors are migrating to aluminum because of far lower prices and comparable performance, according to Reuters interviews with 18 carmakers, cable and air conditioning companies, metals producers and consultants. Ferrari and BMW said they chose aluminum in part because of its lighter weight.

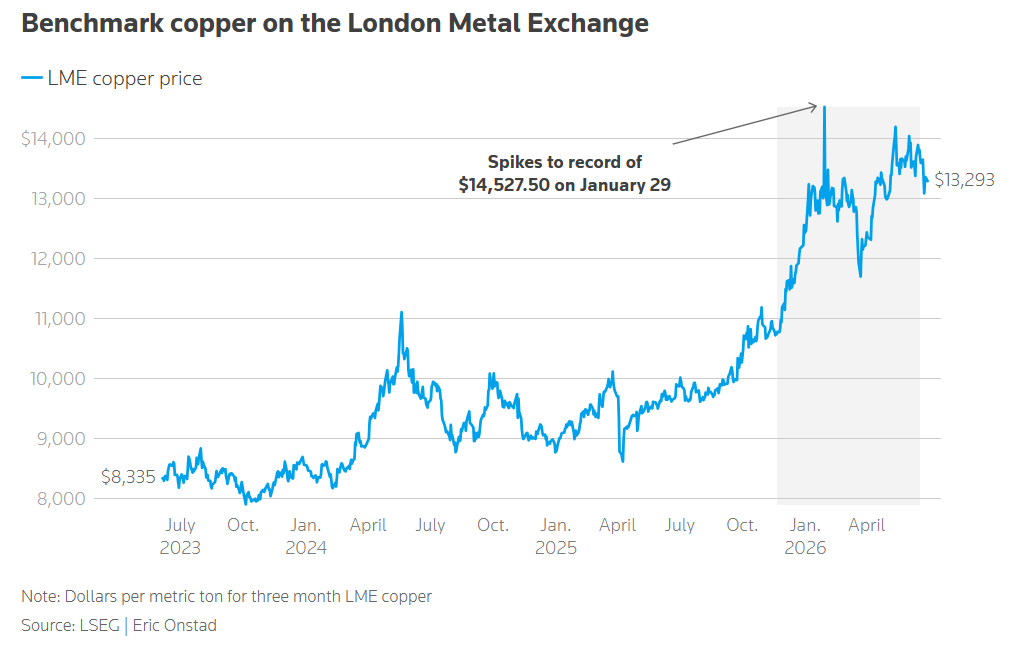

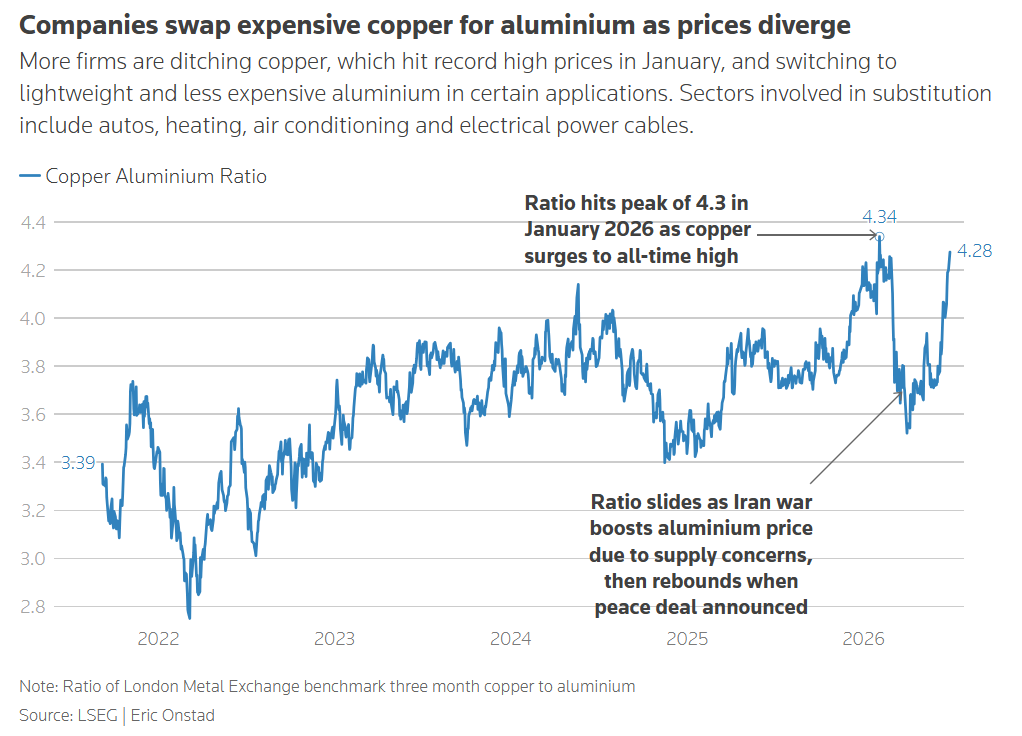

Substitution of aluminum for copper has come in waves over two decades, but record copper prices in late January, peaking close to $15,000 per metric ton, added weight to the case for switching to aluminum. Forecasts for global supply fall short of those for demand for more than the next decade.

Lighter and faster

Ferrari, which already uses aluminum for its bodies, engines and chassis, told Reuters it started using the lightweight metal for power cables on its 296 hybrid sports car last year. Ferrari has since introduced aluminum wiring into other models, including the Luce, its first ever EV launched last month.

The move saves up to 20% of the total wiring weight, said Ferrari communications executive Dario Esposito.

“We are not choosing aluminum because it’s cheaper, we choose the material that has better performance,” he said.

But the metal is, in fact, much cheaper — currently about $3,100 a ton, or about a quarter the price of copper.

Germany’s BMW said it first used aluminum conductors in 2011 in its subcompact 1 series and progressively expanded substitution in hybrids and EVs. Currently, it uses a large number of aluminum cables in both high and low-voltage systems in its latest eDrive EV technology, launched last year.

The world’s fourth-biggest automaker, Stellantis, also recently started swapping copper wiring for aluminum, according to an industry source familiar with the matter. Stellantis declined to comment.

Price versus performance

Chinese EV parts supplier JONVER has seen sales of aluminum wiring products jump this year to about 30% of its sales from about 20% in 2023, said sales director Feng Lu.

Norwegian aluminum producer Hydro said sales of aluminum heating-and-air tubing as a copper substitute have steadily grown in recent years. Hydro CFO Trond Olaf Christophersen said the company expects to gain market share as aluminum rapidly replaces copper in the sector in future years.

Xavier Mathieu at France-based Nexans, the world’s second-biggest cable manufacturer, said manufacturers will still buy copper at higher prices because it performs better in certain applications — but they start buying aluminum when copper prices reach about 3.5 times higher.

Copper prices currently stand at more than 4.2 times the price of aluminum.

Several issues complicate firms’ decisions to swap, including US tariffs and the huge amount of energy needed to produce aluminum , which means more greenhouse gas emissions. In addition, aluminum is cheap but less efficient: It requires more aluminum to conduct the same amount of electricity.

Still, JPMorgan outlined a scenario in which about 6% of annual demand for copper might be replaced by aluminum by 2030, compared to 2% this year.

China EV makers take the lead

The government in the world’s biggest metals consumer, China, encouraged companies to make the switch to aluminum in a March 2025 policy paper seen by Reuters, and many have heeded the call.

Analysts at consultancy Zhuochuang forecast that about 25% to 30% of components currently made from copper, by metal volume, could be switched to aluminum in the power, automotive and home-appliance sectors by 2030.

Chinese EV makers that have switched to aluminum wiring include AVATR, XPeng and Xiaomi, said Terry Woychowski, president at engineering consultancy Caresoft Global, which takes apart vehicles and examines their components.

The three Chinese EV makers and Tesla did not respond to requests for comment.

Lightweight aluminum is especially attractive to EV makers because cutting weight allows for longer driving ranges. And saving money is crucial for EV firms in China, where a price war has left margins razor-thin. And aluminum has ample room to gain ground in autos, where about 85% of electrical wiring busbars, which connect an EV’s battery to its systems, are still copper, according to Hydro.

The Chinese auto industry has benchmarked Tesla, a pioneer in using aluminum for wiring when it introduced its Model Y in 2019, and more recently in its Cybertruck, Woychowski added.

(By Eric Onstad, Amy Lv, Ju-min Park and Kalea Hall; Editing by Veronica Brown and Claudia Parsons)

Seeing the whole picture: Closing notes from Kazakhstan

This is the final dispatch in our Ground View Kazakhstan series.

The first lesson of the northern steppe is that it is flat. On the road from Astana down to Karaganda, the horizon never changes; the steppe makes Kansas look like the Rocky Mountains. And flat is also what gets done to Kazakhstan from a distance. Wedged between Russia and China and newly courted by the West, it flattens in the mind into a splotch on a map or a line in a reserves table, which is roughly how it reads from far away. Up close, it stops flattening, even though the land never does. Sit with the place long enough and one comparison keeps fitting better than any other. It is a jigsaw puzzle.

Start with what should be obvious to any mining analyst. Almost nothing about Kazakhstan was out of reach before arriving in Astana. The reserve figures, the production-sharing history, the long geopolitical balancing act of a landlocked country wedged between Russia and China, the names of the companies and ministries—all of it is available online for anyone patient enough to dig. An office with a decent internet connection and a month of discipline could have collected most of the same pieces.

What no internet search can produce is the picture on the box.

Anyone who has tried to assemble a puzzle without the lid knows the feeling. You have every piece, but with no image to work against, you force the wrong pieces together, mistake sky for sea, and never quite see how the thing is supposed to fit. Going to Kazakhstan was getting the lid. The pieces did not change. The picture they formed did.

Arriving with the wrong lid

There is a harder admission here. The trip did not begin with no picture in mind. It began with the wrong one. The planned story arcs were set before the plane landed. The stories that actually surfaced on the ground were not those. They were an archive, a steelworks and a uranium producer, and the way they fit together looked nothing like the sketch drawn from a desk.

That is not a failure of preparation. It is the whole case for going. From a distance, what was already known had been given the wrong weight because the work was being done against the wrong image. Proximity handed over no secret facts. It corrected the picture the facts were assembled into.

The place where three poles meet

Kazakhstan is the country where three poles of power physically converge, and it is working all three with far more agency than words like buffer or bridge suggest. This is not the passive glue holding rival powers together for their benefit. It is a state that has turned a difficult geographic hand, hemmed in by Russia and China with the West wanting in, into genuine leverage. The evidence is lying around in plain sight, which is exactly the kind of thing you only notice when you are standing in it.

The Russian and Soviet inheritance shows up repeatedly, and rarely with a single message. Two examples could not be more different. One is the geological archive that the National Geological Survey is reopening, a Soviet-era treasury of subsurface data that is suddenly one of the country’s most valuable strategic assets.

The other is Alzhir, the former prison camp, now a memorial, outside Astana, where the Soviet state imprisoned the wives of men it branded traitors. The same history that left Kazakhstan a priceless map of its own ground also left scars it still carries. It is a country metabolizing a past that was both useful and brutal, often in the same breath.

The Western presence sits at Qarmet, the sprawling steelworks that, for nearly three decades as ArcelorMittal Temirtau, supplied much of the steel that built modern Kazakhstan. It also owned the Kostenko mine, where a fire and explosion in October 2023 killed 46 workers in the worst industrial disaster of independent Kazakhstan. The tragedy ended that relationship and returned the works to Kazakh hands. Good and bad, on the same fence line.

The Chinese presence announces itself in the most ordinary way imaginable. On the streets of Astana, half the cars seem to wear brands an American would never recognize, something no supply-chain report captures. The footprint is arriving fast. But a footprint is not the same as value. China’s engagement runs to commerce and extraction, with goods sold in and resources carried out, more than to anything built to stay. Activity everywhere, and little of it left behind.

That is the box lid. Three poles, each pulling its own way and carrying its own contradictions, and a country that has spent its entire independent life learning to stand at their centre rather than be pulled apart. The contradictions read as confusion from a distance. Up close, they fit.

A word about the hosts

None of this picture comes into focus without an openness that was neither expected nor taken for granted. Kazatomprom, Qarmet and the National Geological Survey each offered more than talking points. They opened their doors in the literal sense and answered questions they could comfortably have deflected. Kazatomprom made its chief executive available for an extended interview. Qarmet went further still, not only opening the grounds of its hardest chapter but showing the considerable steps taken since to address it, when steering visitors away would have been the easier course.

Some of what they said deserves critical analysis, which is the highest compliment you can pay people so forthcoming. You do not push back on a closed door. You can only push back on a conversation, and they offered a real one.

True as history, misleading as a forecast

The individual companies are one thing. The message Kazakhstan sends as a whole is another, and it came through again and again, on both the Kazakh and American sides, as a reassurance for anyone weighing critical-minerals investment. American companies are not new here.

Chevron has operated the Tengiz field since 1993, joined by Mobil, later ExxonMobile, in 1996—more than 30 years— through the usual disputes that accompany any partnership between a country and a multinational. On balance, the relationship has worked. Mining, the argument goes, does not need to reinvent the wheel. It can build on three decades of proven structure.

That is half right, and the wrong half gets repeated.

The oil and gas history is real, and it does retire one lazy objection. Kazakhstan is not a greenfield gamble. Western capital has operated here at scale, across political cycles, for a generation, and made it pay. As proof that it can be done, the record is solid. So the precedent is true as history.

It is also misleading as a forecast.

First, the model is proof of concept, not a blueprint. Oil and gas relied on a handful of mega-projects, supermajors and a deep, liquid global market for the output. Critical minerals are more fragmented, rely more on mid-tier and junior capital, and sell into thin markets where the real chokepoint is processing and refining—a stage China dominates. Pulling ore out of Kazakh ground does not capture value unless the midstream and the non-Russian, non-Chinese export routes get built. The precedent proves it can be done. It does not hand anyone a ready-made way to do it.

Second — and this is where the argument sells Kazakhstan short— the country does not sit across the table where it sat in 1993. The early production-sharing deals ran so far in the majors’ favour because a newly independent, capital-starved country with no track record had little choice.

That country is gone.

A local driver put it plainly. Astana was unrecognizable just 10 or 15 years ago. Today’s Kazakhstan has sovereign wealth, national champions that can take equity rather than merely grant it, a credible China alternative if Western terms disappoint, and buyers who now need the minerals more than the country needs any single partner.

Pointing a new entrant back to the 1993 model does Kazakhstan a disservice. It implies a supplicant where the reality is a more established and proven partner. Anyone who arrives expecting 1993 terms will be disappointed. The honest message is not that Kazakhstan is open on the old terms. It is that Kazakhstan is open, proven and increasingly aware not only of its value but of its leverage.

None of it could be sorted out from a distance because facts do not arrive with their weights attached. Context supplies the weights, and context is the one thing a desk cannot download.

That is what Ground View is for.

Not the romance of having been somewhere.

The discipline of seeing enough of the surrounding picture to tell what a fact is worth.

Which is why the column does not stop here. Pakistan is the next puzzle, and like this one it cannot be solved from the box alone. The picture is on the ground, and the ground is the only place to go looking for it.

* Erik Groves is a contributing analyst for MINING.COM and Corporate Strategy and In-House Counsel at Morgan Companies. He recently attended the 16th International Mining and Metallurgy Congress and Exhibition (AMM) in Astana, Kazakhstan. He will be sharing insights gathered at one of Central Asia’s most important mining events.

Canacol gas curbs force Colombia’s Cerro Matoso ferronickel mine to cut output

Cerro Matoso nickel mine – Image courtesy of South32

Colombia’s Cerro Matoso ferronickel mine said on Wednesday it was cutting operations by 25% after Canada’s Canacol Energy reduced natural gas supply to the plant, threatening jobs, supplier contracts and fiscal payments.

Cerro Matoso, owned by CoreX Holding and located in Colombia’s northern Cordoba province, said Canacol cut gas deliveries to 7,000 MMBtu from July 1, a 55% reduction from contracted volumes.

The miner said the cut followed Canacol’s move to seek creditor protection in a Canadian court and request the early termination of several gas supply contracts in Colombia, including Cerro Matoso’s contract, which runs through 2029.

Canacol’s Colombia office declined to respond to a request for comment.

Cerro Matoso said the reduced gas supply would partially suspend some operating processes and could force it within days to halt one of its two production lines if the restriction remains in place or worsens, potentially cutting output by half.

The company said the disruption could affect hundreds of jobs, goods and services contracts, and payments tied to royalties, taxes and local purchases.

Under Colombian law, the final decision on whether the Canadian court ruling can take effect in the country rests with Colombia’s Superintendency of Companies, Cerro Matoso added.

(By Nelson Bocanegra and Luis Jaime Acosta; Editing by Franklin Paul)

MONOPOLY CAPITALI$M

Eni and Mercuria agree to join forces in commodity trading

Italian oil company Eni SpA and commodity merchant Mercuria Energy Group Ltd. signed an agreement to join forces in trading, seeking growth in an area that has seen huge price swings and profit opportunities during the war in Iran.

The two firms will be combining their main trading books for various commodities including oil, liquefied natural gas and biofuels under a new entity headquartered in Geneva, according to statements on Wednesday.

It’s a big move for both companies — integrating Eni’s physical energy supply chains with Mercuria’s trading expertise could potentially allow them to compete more effectively with larger rivals such as Shell Plc or Vitol Group.

“This partnership brings together two highly complementary organizations,” Mercuria chief executive officer Marco Dunand said. The venture will combine “physical energy flows with world-class trading, logistics and risk management capabilities.”

For Eni, the tie-up could allow it to challenge its larger European rivals Shell, BP Plc and TotalEnergies SE, which are among the largest oil and gas traders in the world, buying and selling far more than what’s produced by their own assets.

For Mercuria, which long has trailed rivals like Vitol, Trafigura Group and Gunvor Group in its physical trading volumes, the deal offers an opportunity to supercharge an expansion push, especially in LNG. The fuel is seen by many in the industry as a key growth commodity, but it has faced setbacks, with Steve Hill, a former senior Shell executive whom it hired in 2024, leaving this year.

Eni and Mercuria expect the joint venture to be operational in 2027, with the two firms equally represented at the senior managerial level, according to a spokesperson for the Italian oil giant. Commodity traders won’t be made redundant, the spokesperson added.

Price volatility caused by the Iran war has created opportunities for companies that buy and sell energy in large volumes. Shell and BP posted first-quarter earnings that far exceeded expectations, thanks to a surge in profit from their extensive in-house trading operations.

Mercuria’s first-half profit jumped 88%, putting it on track for one of its best-ever annual results. For several months, the trading house has been doing deals to grow its access to physical commodities and processing assets, including $1.2 billion to help finance the buyout of a copper mining company in Kazakhstan and a deal to buy an oil refinery and petrol stations in Argentina.

Trading activities for both parties will be exclusive to the JV for the identified commodities, except cases that require joint approval, the spokesperson said, adding that Eni does not currently expect refinery assets to form part of the venture.

Talks between Eni and Mercuria to form a joint venture were first reported by Bloomberg in January.

(By Jack Wittels)

Mercuria signs first uranium financing deal with Malawi miner

Kayelekera uranium mine in Malawi. Credit: Lotus Resources.

Trading house Mercuria Energy Group Ltd. signed its first prepayment agreement with a uranium miner, striking a deal with the owner of an operation in Malawi.

Australia’s Lotus Resources Ltd. said last week it has signed a non-binding term sheet with the commodity trader for production from the its Kayelekera mine. If finalized, Mercuria will pay up to $30 million and be able to market 3 million pounds of uranium over 30 months.

The arrangement is Mercuria’s maiden foray into financing uranium miners in return for a portion of their output. The market for the nuclear fuel has recovered in recent years following a lengthy downturn after the 2011 Fukushima disaster, and demand is forecast to grow as multiple countries – led by China – expand their fleet of reactors.

Lotus acquired the Kayelekera asset in 2020, six years after it was shuttered due to weak uranium prices. The company restarted the mine last year and is targeting annual output of 2.4 million pounds of uranium oxide, although earlier this month it announced a temporary pause in production after the Iran war disrupted sulfuric acid supplies.

Mercuria’s funding – which won’t be available until September at the earliest – will provide “significant additional working capital flexibility to progress the project,” Lotus said. That involves repairing the mine’s acid plant.

Under the marketing agreement, Lotus will retain “full control” over who Kayelekera’s production is sold to, including to power utilities that have existing offtake contracts with the mine, the company said.

A spokesperson for Mercuria declined to comment.

(By William Clowes and Archie Hunter)

China restricts some Fortescue iron ore cargoes as talks drag

China’s state iron ore buyer has asked some domestic steel mills not to take delivery of certain portside iron ore products from Fortescue, industry sources said, the latest Australian miner to fall foul of Beijing’s push to increase control over the market.

China Mineral Resources Group (CMRG) notified some mills verbally that from July 15 they must not take delivery of portside cargoes of Fortescue’s Super Special Fines and Fortune Fines, both of which are lower-grade iron ore products, five sources with knowledge of the matter said.

Fortescue declined to comment. Shares of Fortescue were flat at 12:57 GMT on Thursday, even as peers BHP and Rio Tinto fell more than 1%.

Fortescue ships most of its iron ore to China and is still negotiating supply terms with CMRG.

All sources sought anonymity given the sensitivity of the matter. CMRG did not immediately respond to requests for comment outside of working hours on Wednesday.

Stocks of Fortescue’s Super Special Fines at some major Chinese ports stood at 7.22 million tons as of June 30, said a separate trader on condition of anonymity.

That represents nearly 5% of total portside iron ore stocks, according to a Reuters calculation based on data from the consultancy Steelhome.

CMRG last month told some domestic steelmakers not to engage in discussions with Fortescue about a new iron ore product — Fortune Fines — scheduled for shipments from July.

Fortescue’s China president departed in June, just four months after taking the position, the company confirmed last week.

BHP said in mid-April that it had concluded supply contract talks with CMRG, ending a months-long dispute, and Beijing then lifted bans on several of its products.

CMRG was established in 2022 as part of Beijing’s efforts to centralize its iron ore procurement and win better terms from upstream mining giants.

(By Melanie Burton; Editing by Emelia Sithole-Matarise, Kevin Liffey and Tom Hogue)

{kind=link}