The Iran war exposes fiscal fragility around the world

The Iran war has arrived at the worst possible fiscal moment for most of the world's major economies. Governments that spent heavily through Covid, ramped up defence budgets in response to Russia's invasion of Ukraine, and then borrowed again to cushion the energy shock of 2022 are now being asked to absorb a second major energy shock with balance sheets that have never fully recovered from the first.

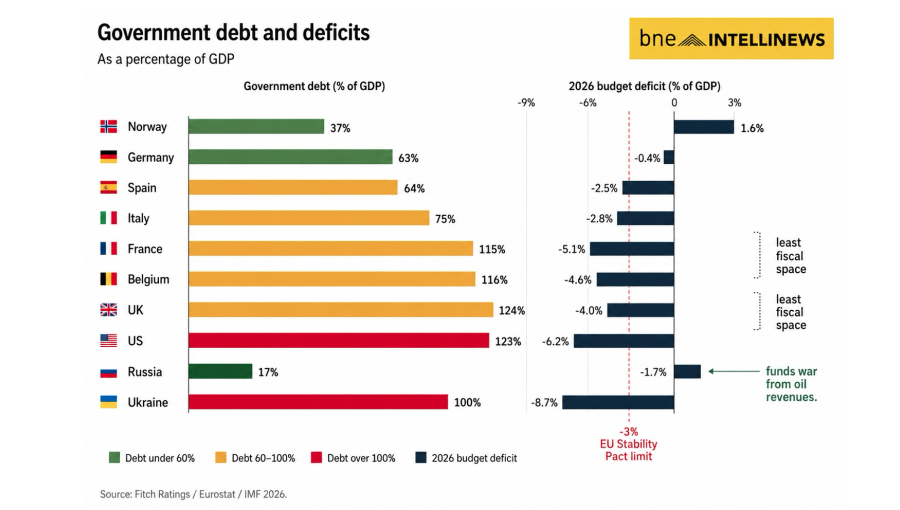

The verdict from a recent Fitch Ratings note is blunt: fiscal space across most of the developed world is limited, and in several major economies it is effectively exhausted.

Ireland, Greece, Portugal, the Netherlands and Scandinavia: The strongest fiscal positions within the EU belong to a counterintuitive group — the countries that were most brutally forced into austerity during the sovereign debt crisis of the early 2010s and have since maintained disciplined fiscal management through successive shocks. They have, in theory, the most room to respond to the current crisis, though Fitch notes that even these governments face pressure to avoid sharp deterioration in their debt and deficit positions. The lesson of a decade of consolidation is a floor of credibility that their peers have not preserved.

Germany: Additional outlays on defence and infrastructure investment will continue under the Merz government's historic €500bn spending programme, financed through the newly suspended debt brake. Fitch notes that further measures would add pressure to the deficit but would likely be offset by savings elsewhere, since extraordinary spending falls under fiscal rules that require compensation. The challenge for Germany is less about financing and more about growth: how the latest energy shock affects an already stagnant industrial economy dependent on cheap gas is the central question. Two consecutive years of GDP contraction before the Iran war have left Berlin with less economic cushion than its fiscal position implies, says Fitch.

Spain: Has been at the forefront of household and business support measures, announcing programmes equivalent to 0.5% of GDP. Fitch places Spain in the category of countries that have run deficits of around 3% in recent years — on the margin of the EU's fiscal rules, but with enough credibility and growth momentum to absorb modest additional measures. Spain's heavy investment in renewables and its relatively lower industrial gas intensity also give it more structural insulation from the energy shock than northern European peers.

Italy: Deficits have been moderating and are approaching 3% of GDP, but unlike Germany or Spain, Italy's combination of high debt and elevated financing costs severely constrains its ability to provide fiscal support. Fitch notes that the Meloni government's strong commitment to fiscal prudence reinforces this constraint rather than fighting it. The main vulnerability is economic: Italy's industrial sector is heavily gas-dependent, and the inflationary impact of the energy shock on an already low-growth economy is the primary credit concern. Targeted measures with offsetting mechanisms are the most likely government response.

Belgium, France and the UK: These three governments share the most exposed fiscal position in the developed world outside of Japan. All three carry deficits above the EU's 3% limit — France at 5.1%, Belgium at 5.2% — and all three carry government debt above 100% of GDP. Fitch identifies them as the governments with the least room to finance additional support measures, with rising financial pressures acting as an important limiting factor particularly in the UK, where gilt market sensitivity to fiscal credibility has been demonstrated painfully in recent years. Modest support programmes with likely offsetting measures are the expected response — not the open-ended transfers that the scale of the energy shock might otherwise justify.

The United States: Washington faces its own version of this fiscal constraint, albeit from a structurally different position. Fitch maintains a Stable Outlook on the United States' AA+ rating and notes that the Iran war alone is unlikely to put pressure on the sovereign, given limited expected downside for the economy from higher defence expenditure in isolation. But the compounding effect of the conflict with an already stretched fiscal picture is significant. The Pentagon has called for an additional $200bn in military funding this year through a supplemental budget request; the administration is seeking nearly $440bn in additional defence spending in the fiscal year 2027 budget, partly offset by cuts to other discretionary spending. Fitch has incorporated only $50bn of each request into its current projections — a signal of significant upside fiscal risk if Congress approves the full amounts. Under an adverse war scenario in which oil prices remain elevated and equity markets deteriorate, Fitch estimates US growth would be reduced by 1.2 percentage points by the fourth quarter of 2026, core CPI inflation could run 1.4 percentage points above the baseline, and the general government deficit could rise well above 8% of GDP — with the debt-to-GDP ratio rising well above Fitch's current end-2027 forecast of 122%.

Asia: Asian emerging markets are collectively the most exposed to a prolonged Hormuz disruption, given their structural dependence on Middle Eastern energy. Fitch identifies India, the Maldives, Pakistan, the Philippines and Thailand as large net fossil fuel importers facing the most direct terms-of-trade deterioration. China is less immediately vulnerable due to its large energy reserves, though it is far from immune. The credit risk channels beyond energy include exchange-rate depreciation, tighter financing conditions and shifts in remittances — all of which compound the direct fiscal impact of higher import bills. The median government debt-to-GDP ratio for Asia-Pacific has risen to 50.5% in 2026 from 37.8% in 2019, and more than 70% of sovereigns in the region still carry higher fiscal deficits than before Covid. Governments have responded unevenly: Pakistan, the Philippines and Thailand have raised fuel prices, sometimes combined with targeted household relief; Indonesia and India have kept prices broadly stable, absorbing the fiscal cost directly.

Malaysia and Mongolia: Stand apart as net energy exporters and are in a stronger structural position than regional peers. But Fitch cautions that even Malaysia — which has recently reformed fuel subsidies — still faces spending pressures from high oil prices and cannot be expected to benefit materially from the conflict at the sovereign credit level.

The common thread running through Fitch's analysis across all three regions is a world in which the fiscal resources to absorb major external shocks have been steadily depleted over five years of consecutive crises — pandemic, energy shock, Ukraine war, now Iran — without a corresponding period of rebuilding. The governments that maintained fiscal prudence through that sequence have options. Those that did not are now discovering the limits of what debt markets will finance.

No comments:

Post a Comment