It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Myanmar’s junta takes desperate measures to stem capital flight

The hard-hit middle class is searching for a place to park what’s left of their assets after three years of war.

A commentary by Zachary Abuza 2024.06.16

Illustration by Amanda Weisbrod/RFA

The rumors were everywhere: A politically connected crony, U Thein Wai, better known as Serge Pun, was called in for questioning.

While he was not arrested, the military’s questioning of the CEO of Yoma Bank and eight directors of other subsidiaries under his control is another indicator of just how dire Myanmar’s economic situation is.

The 71-year old Sino-Burmese tycoon sits atop a massive business empire of some 50 different interrelated companies. The most important of these are First Myanmar Investment Company (FMI), Serge Pun and Associates (SPA), and, of course, Yoma Bank.

While largely invested in real estate through Yoma Land, SPA is one of the largest conglomerates in the country, with investments in real estate, construction, banking and financial services, Suzuki automobile assembly, the KFC franchise and healthcare.

Yoma Bank is one of the largest private banks in Myanmar and has been in important overseas conduit, especially after the US government sanctioned two state banks in June 2023.

Yoma Bank has ties to the military, lending to both the military-owned Mytel and Pinnacle Asia, which is owned by Min Aung Hlaing’s daughter, Khin Thiri Thet Mon.

Yoma Bank CEO U Thein Wai, also known as Serge Pun, smiles as electronic trading commences during the opening day of trading at Yangon Stock Exchange, March 25, 2016. (Gemunu Amarasinghe/AP)

In November 2022, the State Administrative Council, as the junta is formally called, bestowed on him the honorific Thiri Pyanchi, granted for outstanding performance.

Pun’s ties to the military are deep enough that the World Bank’s International Finance Corporation divested their 4.55% equity stake in Yoma Bank in December 2022, selling it to FMI.

This is not to say that Pun has been completely pro-military. Compared to other cronies, he’s been much less so. He’s hedged his bets and incorporated holdings in Singapore and Hong Kong. Arguably he would be a lot wealthier were it not for the coup, but he’s worked within the reality of the coup.

So what prompted the Office of the Chief of Military Security Affairs, the feared military intelligence service, to come calling?

In short, facilitating capital flight.

Real estate roadshow

In late May, a group of five executives of a real estate firm, Minn Thu Co., held an unauthorized roadshow, selling Bangkok condominiums. Minn Thu had allegedly established unauthorized bank accounts in Thailand to facilitate the sales.

Thai real estate is being pitched to Burmese as a safe investment at a time when the kyat has fallen to a record low of over 5,000 kyat per dollar, while soaring inflation eats into the currency’s purchasing power.

Gold has reached record rates: 5.8 million kyat per tical (15.2 grams, .54 oz) – 4.5 times the pre-coup rate of 1.3 million kyat. Over 20 gold dealers have been arrested recently, accused of engaging in speculation.

The beleaguered middle class is desperately searching for a place to park what’s left of their assets after more than three years of conflict.

Four of the five businessmen who staged the roadshow have been arrested, and one other executive is at large.

A customer waits to withdraw money at Yoma Bank in Yangon, June 17, 2013. (Soe Zeya Tun/Reuters)

To serve as a deterrent to others, the junta arrested three people who purchased the condos, having illegally transferred assets overseas.

Yoma Bank is believed to have assisted in financing the purchases by transferring assets to Bangkok in violation of the junta’s currency controls.

Military intelligence officials are also investigating whether Yoma Bank is offering what are de facto mortgages for overseas real estate, as an investment vehicle, in contravention of Myanmar law.

In recent days, the junta has expanded their investigation into over 100,000 private bank transfers.

Capital flight began immediately after the coup. Radio Free Asia reported the purchase of THB2.5 billion (US$69 million) and THB 3.7 billion (US$100 million) in Thai real estate in 2022 and 2023, respectively.

In the first quarter of 2024, Burmese were the second largest group of foreign nationals to invest in Thai real estate, according to the Bangkok Post, having purchased at least 384 units, worth THB2.2 billion ($60 million).

Estimates, though, are far higher, as many properties are believed to have been purchased using Thai nominees.

Focus on funds

And of course, the revelation that junta leader Min Aung Hlaing’s own children have moved their own assets to Thailand was a huge embarrassment for the regime. Aung Pyae Sone owns a condominium worth around $1 million in Bangkok, while Khin Thiri Thet Mon has two accounts at Siam Commercial Bank.

Reports are emerging that Khin Sri Thet Mon purchased a condo in the ultra swank SCOPE Langsuan, which was completed in May 2023, and where a three bedroom unit sells for $4.2 million to over $15 million.

The SAC has deployed uniformed personnel to both public and private banks since mid-2021 to block transfers to the civil disobedience movement, the National Unity Government, and ethnic resistance organizations. But soon after that, they also began monitoring capital flight.

The junta is increasingly cracking down on the informal banking sector, known as hundi, that is used by at least 40 percent of overseas workers.

In early June, the regime froze the accounts of 39 additional hundi dealers, following the crackdown on 20 others in January.

The hundi system keeps desperately needed foreign exchange out of the formal banking system, where people and companies are forced to convert it to kyat at artificially low exchange rates.

Given the state of the economy, capital flight is the rational choice for Burmese with the means..

Myanmar junta chief Senior Gen. Min Aung Hlaing and his wife, Kyu Kyu Hla, visit a Buddhist monastery in Thailand in February 2018. (Myanmar military)

The World Bank has reported on the dire state of the economy, which has shrunk by nearly 20% since the coup. The poverty rate is now 32%, while 2024 GDP growth estimates have been halved to 1%.

The NUG estimates that the junta has printed 30 trillion kyat (US$11.5 billion) since the coup, a leading – though not the only – cause of inflation, which is now at 30%. The kyat has lost 22% of its value.

Public debt is soaring. Currently at 63% of GDP, compared to 42% under the ousted Aung San Su Kyi government, and it is expected to worsen as revenue collection is collapsing.

A recent report by the Special Advisory Council-Myanmar shows that only one of 51 townships that have border crossings is under stable junta control, with four more under their proxy militias, which has led to a loss of significant amounts of customs duties.

Pinching trade

More importantly, the junta has restricted the volume of trade that can be transacted in local currencies. The World Bank reported that exports fell by 13% and imports by 20% in the first six months of 2024, but that cross border exports, except for gas, fell by 44%, while imports fell by 71%.

Military losses have forced the Ministry of Oil and Gas Enterprise to abandon two oil fields. Oil and gas production generates some $1.5 billion, half of the regime’s foreign exchange earnings.

Meanwhile, attempts to increase the number of tourists have largely faltered.

A vendor sells food from her stall during an electricity blackout in Yangon on April 26, 2024. (Sai Aung Main/AFP)

The junta has burnt through its foreign exchange reserves to support its war effort.

At the time of the coup, those reserves stood at $6.8 billion. Immediately after the coup, the United States government froze $1.1 billion. The NUG estimates reserves to be just over $3 billion, further imperiling any hope of macroeconomic stability.

The dire state of the economy comes as the military needs additional resources to build up their arsenal, induct 5,000 conscripts a month, and recruit demobilized soldiers, in order to resume the offensives in the next dry season.

Lacking an economy to support a sustained conflict, the junta appears set to match its desperate crackdown on tycoons with drastic steps to dramatically turn the military tide.

Under the Tatmadaw doctrine, this means intensified targeting of civilians.

Zachary Abuza is a professor at the National War College in Washington and an adjunct at Georgetown University. The views expressed here are his own and do not reflect the position of the U.S. Department of Defense, the National War College, Georgetown University or Radio Free Asia.

Sunday, April 06, 2025

We're not jerks': Flight attendants on deportation planes say disaster is 'only a matter of time' Photo by Etienne Jong on Unsplash

Unexpected Role: Flight attendants were told they would fly rock bands, sports teams and sun-seekers. Then Global Crossing Airlines started expanding into federal deportation flights.

Human Struggles: Some flight attendants said they ignored orders not to interact with detainees. “I’d say ‘hola’ back,” said one flight attendant. “We’re not jerks.”

Safety Concerns: Flight attendants received training in how to evacuate passengers but said they weren’t told how to usher out detainees whose hands and legs were bound by shackles.

These highlights were written by the reporters and editors who worked on this story.

The deportation flight was in the air over Mexico when chaos erupted in the back of the plane, the flight attendant recalled. A little girl had collapsed. She had a high fever and was taking ragged, frantic breaths.

The flight attendant, a young woman who went by the nickname Lala, said she grabbed the plane’s emergency oxygen bottle and rushed past rows of migrants chained at the wrists and ankles to reach the girl and her parents.

By then, Lala was accustomed to the hard realities of working charter flights for Immigration and Customs Enforcement. She’d learned to obey instructions not to look the passengers in the eyes, not to greet them or ask about their well-being. But until the girl collapsed, Lala had managed to escape an emergency.

Lala worked for Global Crossing Airlines, the dominant player in the loose network of deportation contractors known as ICE Air. GlobalX, as the charter company is also called, is lately in the news. Two weeks ago, it helped the Trump administration fly hundreds of Venezuelans to El Salvador despite a federal court order blocking the deportations, triggering a showdown that experts fear could become a full-blown constitutional crisis.

In interviews with ProPublica, Lala and six other current and former GlobalX flight attendants provided a window into a part of the deportation process that is rarely seen and little understood. For migrants who have spent months or years trying to reach this country and live here, it is the last act, the final bit of America they may experience.

All but one of the flight attendants requested anonymity or asked that only a nickname be used, fearing retribution or black marks as they looked for new jobs in an insular industry.

Because ICE, GlobalX and other charter carriers did not respond to questions after being provided with detailed lists of this story’s findings, the flight attendants’ individual accounts are hard to verify. But their stories are consistent with one another. They are also generally consistent with what has been said about ICE Air in legalfilings, newsaccounts, academic research and publicly released copies of the ICE Air Operations Handbook.

That morning over Mexico, Lala said, the girl’s oxygen saturation level was 70% — perilously low compared with a healthy person’s 95% or higher. Her temperature was 102.3 degrees. The flight had a nurse on contract who worked alongside its security guards. But beyond giving the girl Tylenol, the nurse left the situation in Lala’s hands, she recalled.

Lala broke the rule about talking to detainees. The parents told Lala their daughter had a history of asthma. The mom, who Lala said had epilepsy, seemed on the verge of her own medical crisis.

Lala placed the oxygen mask on the girl’s face. The nurse removed her socks to keep her from further overheating. Lala counted down the minutes, praying for the girl to keep breathing.

The stories shared by ICE Air flight attendants paint a different picture of deportations from the one presented to the public, especially under President Donald Trump. On social media, the White House has depicted a military operation carried out with ruthless efficiency, using Air Force C-17s, ICE agents in tactical vests and soldiers in camo.

The reality is that 85% of the administration’s “removal” flights — 254 flights as of March 21, according to the advocacy group Witness at the Border — have been on charter planes. Military flights have now all but ceased. While there are ICE officers and hired security guards on the charters, the crew members on board are civilians, ordinary people swept up in something most didn’t knowingly sign up for.

When the flight attendants joined GlobalX, it was a startup with big plans. It sold investors and new hires alike on a vision of VIP clients, including musicians and sports teams, and luxury destinations, especially in the Caribbean. “You can’t beat the eXperience,” read a company tagline.

But as the airline grew, more and more of its planes were filled with migrants in chains. Some flight attendants were livid about it.

Last year, an anonymous GlobalX employee sent an all-caps, all-staff screed that ricocheted around the startup. “WHERE IS THE COMPANY GOING?” the email asked. “YOU SIGNED A 5 YEAR CONTRACT WITH ICE? ... WHAT HAPPENED TO THIS BECOMING A PRESTIGE CHARTER AIRLINE?”

One flight attendant said he kept waiting for the sports teams his new bosses had talked about as he flew deportation routes. “You know, the NFL charters, the NBA charters, whatever the hockey one is …” he said.

A second said his planes’ air conditioning kept breaking — an experience consistent with at least two publicly reported onboard incidents — and their lavatories kept breaking, something another flight attendant reported as well. But the planes kept flying. “They made us flush with water bottles,” he said.

But the flight attendants were most concerned about their inability to treat their passengers humanely — and to keep them safe. (In 2021, an ICE spokesperson told the publication Capital & Main that the agency “follows best practices when it comes to the security, safety and welfare of the individuals returned to their countries of origin.”)

They worried about what would happen in an emergency. Could they really get over a hundred chained passengers off the plane in time?

“They never taught us anything regarding the immigration flights,” one said. “They didn’t tell us these people were going to be shackled, wrists to fucking ankles.”

“We have never gotten a clear answer on what we do in an ICE Air evacuation,” another said. “They will not give us an answer.”

“It’s only a matter of time,” a third said, before a deportation flight ends in disaster.

Lala didn’t think she had a chance at a flight attendant job. She hadn’t, in truth, remembered applying to GlobalX until a recruiter called to say the startup was coming to her city. “But I guess I did apply through LinkedIn?” she said. She’d been working an office job — long hours, little flexibility — and was looking for something new.

The job interviews were held at a resort hotel. The room was packed with dozens of aspirants when Lala showed up. After the first round, only about 20 were asked to stay. She couldn’t believe she was one of them. After the second round came a job offer: $26 an hour plus a daily expense allowance. Soon Lala got a uniform: a blue cardigan, a white polo shirt and an eye-catching scarf in cyan and light green.

For part of her Federal Aviation Administration-mandated four-week training, her class stayed in a motel with a pool at the edge of Miami International Airport. Just across the street, on the fourth floor of a concrete-clad office building ringed by palm trees, was GlobalX’s headquarters.

“In the beginning, we were told that because it’s a charter, it’s only gonna be elites, celebrities,” Lala said. “Everybody was really excited.”

But flying was not going to be all glitz. The real reason for having flight attendants is safety. GlobalX was certified by the FAA as a Part 121 scheduled air carrier, the same as United or Delta, and it and its crew members were subject to the same strict standards.

“We’re there to evacuate you,” one recruit told ProPublica. “Yes, we make good drinks, but we evacuate you.”

Lala’s class practiced water landings in the pool at the nearby Pan Am Flight Academy. They practiced door drills — yelling out commands, shoving open heavy exit doors — in a replica Airbus A320 cabin. They learned CPR and how to put out fires. They took written and physical tests, and if they didn’t score at least 90%, they had to retake them.

They were reminded, over and over, that their job was a vocation, one with a professional code: No matter who the passengers were, flight attendants were in charge of the cabin, responsible for safety in the air.

Lala’s official “airman” certificate arrived from the FAA a few weeks after training was done. She was cleared to fly, ready to see the world.

But what she would see wasn’t what she signed up for. The company was growing beyond glamorous charters. GlobalX was moving into the deportation business.

Her bosses delivered the news casually, she recalled: “It was like, ‘Oh yeah, we got a government contract.’”

The new graduates were offered a single posting: Harlingen, Texas. Deportation flights were five days a week, sometimes late into the night. Lala went to Guatemala, Honduras, Colombia and, for refueling, Panama.

A standard flight had more than a dozen private security guards — contractors working for the firm Akima — along with a single ICE officer, two nurses, and a hundred or more detainees. (Akima did not respond to a request for comment.) The guards were in charge of delivering food and water to the detainees and taking them to the lavatories. This left the flight attendants, whose presence was required by the FAA, with little to do.

“Arm and disarm doors, that was our duty,” Lala said.

The flights had their own set of rules, which the crew members said they learned from a company policy manual or from chief flight attendants. Don’t talk to the detainees. Don’t feed them. Don’t make eye contact. Don’t walk down the aisles without a guard escorting you. Don’t sit in aisle seats, where detainees could get close to you. Don’t wear your company-issued scarf because of “safety concerns that a detainee might grab it and use it against us,” Lala said.

“You don’t do nothing,” said a member of another GlobalX class. “Just sit down in your seats and be quiet.” If a detainee looked at him, he was supposed to look out the window.

A rare public statement from the company about life aboard ICE Air came in a 2023 earnings call with GlobalX founder and then-CEO Ed Wegel, when he discussed the company’s work for federal agencies like ICE. GlobalX employees “essentially don’t do much on the airplane,” Wegel said. “Our flight attendants are there in case of an emergency. The passengers are monitored by guards that are placed on board the airplane by one of those agencies.”

Fielding a question about how GlobalX ensures passengers are treated humanely, Wegel continued: “There have been threats made to our crew members, and they’re especially trained to deal with those. But we haven’t seen any mistreatment at all.”

Flight attendants said they had little to do but sit in their jumpseats after delivering the preflight safety briefing in English to the mostly Spanish-speaking passengers. Above 10,000 feet, the two in the rear usually moved to passenger rows near the cockpit, then sat again. Some did crosswords. Others took photos out the window. On a deportation to Guatemala, one saw his first erupting volcano.

Lala had been scared before her first deportation flight, worried that violence might break out. But fear soon gave way to discomfort at how detainees were treated. “Not being able to serve them, not being able to look at them, I didn’t think that was right,” she said.

Some flight attendants, drawn to the profession because they liked taking care of people, couldn’t help but break protocol with passengers. “If they said ‘hola’ or something,” one said, “I’d say ‘hola’ back. We’re not jerks.”

Another recalled taking a planeload of children and their escorts on a domestic transfer from the southern border to an airport in New York. He tried to slip snacks to the kids. “Even the chaperones were like, ‘Don’t give them any food,’” he said. “And I’m like, ‘Where is your humanity?’” (A second flight attendant said that children on a New York flight were fed by their escorts.)

While flight attendants were allowed to interact with the guards, the dynamic was uncomfortable. It came down to a question of who was in charge — and which agency, ICE or the FAA, ultimately held sway. (The FAA declined to comment on this story and directed questions to ICE.)

The guards often asked flight attendants to heat up the food they brought from home. They asked for drinks, for ice. “They treated us like we were their maids,” said Akilah Sisk, a former flight attendant from Texas.

“In their eyes, the detainees are not the passengers,” another flight attendant said. “The passengers are the guards. And we’re there for the guards.”

Some guards thumbed their noses at the FAA safety rules that flight attendants were supposed to enforce while airborne, multiple flight attendants recalled. “One reported me because I asked him to sit down in the last 10 minutes,” Sisk said. “But you’re still on a freaking plane. You gotta listen to our words.”

Flight attendants said that if they told guards to fasten seatbelts during takeoff or stow carry-ons under a seat, they risked getting reported to their bosses at GlobalX, who they said wanted to keep ICE happy. The guards would complain to the in-flight supervisor, Sisk said, and eventually it would get back to the flight attendant.

“We’d get an email from somebody in management: ‘Why are you guys causing problems?’” another flight attendant recalled. “They were more worried about losing the contract than about anything else.”

Nothing bothered flight attendants more than the fact that most of their passengers were in chains. What would happen if a flight had to be evacuated?

Most of the migrants crowding the back seats of ICE Air’s planes have not been, historically, convicted criminals. ICE makes restraints mandatory nonetheless. “Detainees transported by ICE Air aircraft will be fully restrained by the use of handcuffs, waist chains, and leg irons,“ reads an unredacted version of the 2015 ICE Air Operations Handbook, which was obtained by the Center for Constitutional Rights, a legal advocacy group.

The handbook allows for other equipment “in special circumstances, i.e., spit masks, mittens, leg braces, cargo straps, humane restraint blanket, etc.” Multiple lawsuits on behalf of African asylum-seekers concern the use of one such item, known as the Wrap, a cross between a straight jacket and a sleeping bag. A flight attendant said detainees restrained in the device are strapped upright in their seats or, if less compliant, lengthwise across a row of seats. Getting “burritoed, I call it,” the person said.

The Department of Homeland Security’s Office for Civil Rights and Civil Liberties investigated the asylum-seekers’ complaints and found ICE lacked “sufficient policies” on the Wrap, but how the immigration agency addressed the finding is not publicly known. ICE responded to one lawsuit by saying detainees were not abused; it said another should be dismissed, in part because it was filed in the wrong place. The cases are pending.

Use of the Wrap continues. A video from Seattle’s Boeing Field taken in February shows officers and guards carrying a wrapped migrant into the cabin of a deportation plane.

Neither the ICE Air handbook, nor FAA regulations, nor flight attendant training in Miami explained how to empty a plane full of people whose movements were, by design, so severely hampered. Shackled detainees didn’t even qualify as “able-bodied” enough to sit in exit rows.

To flight attendants, the restraints seemed at odds with the FAA’s “90-second rule,” a decades-old manufacturing standard that says an aircraft must be built for full evacuation in 90 seconds even with half the exits blocked.

Lala and others said no one told them how to evacuate passengers in chains. “Honestly, I don’t know what we would do,” she said.

The flight attendants are not alone in voicing concerns.

In an interview with ProPublica, Bobby Laurie, an airline safety expert and former flight attendant, called the arrangement on ICE Air flights “disturbing.”

“Part of flight attendant training is locating those passengers who can help you in an evacuation,” Laurie told ProPublica. That would have to be the guards. “But if they have to help you,” who is helping the detainees, Laurie wondered.

According to formal ICE Air incident reports reviewed by Capital & Main, the deportation network had at least six accidents requiring evacuations between 2014 and 2019. In at least two cases, both on a carrier called World Atlantic, the evacuations were led not by flight attendants but by untrained guards. Both took longer than 90 seconds, though not by much: two-and-a-half minutes for the first, “less than 2 minutes” for the next. But in a third case, it took seven minutes for 115 shackled detainees to escape a smoke-filled jet.

In one of the World Atlantic incidents, part of the landing gear broke, a wing caught fire and the smell of burning rubber seeped in, according to investigative records obtained by the University of Washington Center for Human Rights. In an email to ICE Air officials, an agency employee aboard the plane later wrote that flight attendants made no emergency announcements for passengers. The flight attendants simply got themselves out.

The ICE officer, guards and nurse were “confused on what to do and in which direction to exit during distress,” the officer wrote. He said that other than the flight crew, “no one has received any training on emergency evacuation situations.”

The University of Washington’s collection does not include findings or recommendations from ICE based on what happened, and ICE did not say what they were when asked by ProPublica. The National Transportation Safety Board said that after the accident, World Atlantic launched a campaign to reinspect landing gear, gave employees and contractors further training, and revised its procedures for inspections. The airline did not respond to questions from ProPublica.

Other reports obtained by the University of Washington mention fuel spills, loss of cabin air pressure and a “large altercation” on ICE Air after 2019 but no more evacuations, at least as of June 2022. More recent incidents that have been mentioned in the press include an engine fire last summer on World Atlantic and a failed GlobalX air conditioning unit that sent 11 detainees to the hospital with “heat-related injuries.”

The rare guidance some flight attendants said they received on carrying out ICE Air evacuations came during briefings from pilots. What they heard, they said, was chilling and went against their training.

“Just get up and leave,” one recalled a GlobalX pilot telling him. “That’s it. … Save your life first.”

He understood the instructions to mean that evacuating detainees was not a priority, or even the flight attendants’ responsibility. The detainees were in other people’s hands, or in no one’s.

When asked if they got similar guidance from pilots, three flight attendants said they did not, and one did not answer. Two more, like the first, said pilots gave them instructions that they took to mean they shouldn’t help detainees after opening the exit doors.

“That was the normal briefing,” said a flight attendant from Lala’s class. “‘If a fire occurs in the cabin, if we land on water, don’t check on the immigrants. Just make sure that you and the guards and the people that work for the government get off.’”

“It was as if the detainees’ lives were worthless,” said the other.

The day the girl collapsed on Lala’s flight, the pilot turned the plane around and they crossed back into the United States.

The flight landed in Arizona. Paramedics rushed on board and connected the girl to their own oxygen bottle. They began shuttling her off the plane. Her parents tried to join. But the guards stopped the father.

Shocked, Lala approached the ICE officer in charge. “This is not OK!” she yelled. The mom had seizures. The family needed to stay together.

But the officer said it was impossible. Only one parent could go to the hospital. The other, as Lala understood it, “was going to get deported.”

Most of the flight attendants who spoke with ProPublica are now gone from GlobalX. Some left because they found other jobs. Some left even though they hadn’t. Some left because the charter company, as it focused more and more on deportations, shut down the hub in their city.

Lala eventually left because of the little girl and her family, because she couldn’t do the deportation flights anymore. Her GlobalX uniform hung in her closet for a time, a reminder of her career as a flight attendant. Recently, she said, she threw it away.

She never learned whether the little girl lived or died. Lala just watched her mom follow her off the plane, then watched the dad return to his seat.

“I cried after that,” she said. She bought her own ticket home.

Thursday, August 07, 2025

Challenging the neoliberal narrative

AUGUST 5, 2025

Stealth tax, wealth tax, land tax, or reduce tax: these are just some questions facing the left. Steve Laughton offers his opinion.

Some us who grew up in the Keynesian era, when economic growth was higher and inequality far less than it is today, remember that income tax rates on the highest incomes were up to 90%. As a result of the post-war Keynesian consensus, taxes were used to achieve greater levels of equality than capitalism achieved before or since.

The thirty-year post-war epoch also enjoyed high levels of growth with those on median incomes experiencing rising living standards. From 1979 on, the era of fiscal dominance was replaced by the Washington consensus: taxes must be reduced, and interest rates must be used to control demand and inflation.

Unfortunately, much of the left in Europe and in UK has failed to reverse this neoliberal economic narrative. The result has been a steady drift to right wing populism.

As illustrated by some articles on Labour Hub, the UK left has tended not to propose a return to these high marginal rates of tax and has also stuck with the narrative that governments need to issue bonds to cover deficit spending. For fear of bond markets, the left proposes wealth taxes to enable the government to spend.

The belief that governments are impotent to spend without persuading or forcing the wealthy to hand over their money persists. So, how much does the UK government need to spend to end poverty?

Figures vary depending on how poverty is measured, but let’s take a figure of an extra £90 billion per year, which has been calculated to end pensioner poverty and child poverty, and rebuild the health service.

How much could a wealth tax raise?

Here the economists diverge. John Trickett’s wealth tax report estimated that when coupled with a policy of equalising capital gains tax rates to income tax rates and closing tax loopholes, around £100 billion a year might be raised!

Which brings us to the question, will wealth taxes be avoided? Summers and Sarin (2020) suggest estate taxes have a 60% rate of avoidance. Others argue they will encourage capital flight which will reduce our real wealth. Some countries, such as France and Spain, repealed their wealth taxes because they didn’t work. They are administratively complex and therefore expensive and thus a costly way of ‘raising revenue’.

Richard Murphy opposes a wealth tax on the grounds that wealth is notoriously difficult to measure, that some aspects of it would meet huge resistance, not just from the wealthy but householders, and points out it would create costly disputes creating income for lawyers and accountants. Labour Hub published an extract from his 2024 Taxing Wealth Report, in which he suggests a raft of achievable proposals, that could raise £90 billion per year, and I’d recommend reading the full 2024 Taxing Wealth Report.

Özlem Onaran suggests wealth taxes might raise between £46 billion and £78 billion per year, depending on levels of avoidance.

Experience in Europe is mixed, with Switzerland, ironically, collecting over 3% of its revenue through a wealth tax. More typical is France’s experience: the net wealth tax raised about US $2.6 billion annually but led to significant capital flight (for example, $125 billion in assets left France). Tax evasion via offshore accounts was rampant.

Studies have shown 20% tax evasion among wealthy French and Scandinavians. The French tax was repealed under President Macron due to its economic damage and low revenue (about 0.2% of GDP). The IFI wealth tax just taxes real estate and was narrower and less controversial but still generates limited revenue.

Other options

If we want a form of wealth tax, surely land tax which is impossible to avoid and fairly simple to administer offers an achievable option. Raising capital gains tax to the level of income tax would also simplify the system, reducing costs. Some estimates show that the accountancy sector advising the wealthy on how to legally avoid taxes, uses a lot of human labour, amounting in the USA to between 15% and 30% of GDP! A simpler tax system would shrink this industry, releasing labour for other purposes: let’s say, healing the sick or designing new renewable energy technology.

A wealth tax on all assets is intuitively appealing: it is absurd that the top 5% of the world’s wealthiest people can use their money to fund neoliberal thinktanks and persuade public opinion that they are the wealth producers, as opposed to wealth siphoners, and that we must do what they know to be best for us. But the current proposals for a wealth tax tend to hover around taking 1% to 2% of wealth. Ignoring any problems of measurement, disputes, costs and enforcement, this is still not going to address inequality or reduce the power and influence of the top 1%.

We need far higher marginal rates of taxation to dent the power of extreme wealth. The top 5% could probably claw back the 2% wealth tax in an afternoon!

Greater taxation of wealth and high income is a way of reducing inequality. But must we wait for this before we can spend? The neoliberal belief that a country must attract private foreign investment and that capital flight is a real danger prevents the left from allowing governments to spend the money required to end poverty and achieve full employment. Free movement of capital is embedded in EU law and leaves governments in hock to private capital.

Governments have the power to control capital. For example, Malaysia, against the advice of all the neo-Keynesian economists and the IMF, did so and survived the 1997-98 Far Eastern Financial Crisis better than similar economies that took the IMF’s advice. Malaysia avoided austerity.

The Liz Truss ‘bond crisis’, when correctly understood, demonstrates the power of the government which through Parliament sets the rules under which the Bank of England operates. As soon as the BoE stepped in to buy bonds, the crisis stopped.

A correct understanding of markets shows that after the Great Financial Crash, governments have the power to control markets. The left has been led to believe that the US Fed’s lending of dollars to UK banks after the GFC proved that the UK was dependent on capital flows – the dollar liabilities of the banks had to be defended and the UK would have collapsed if the US hadn’t lent us the dollars to do so.

In fact, what led the US to lend dollars, was its desire to see lower interest rates in the USA, because the USA uses LIBOR as its benchmark for interest rates. To lower interest rates, it set up swap lines to shore up banks’ supplies of dollars round the world. This was the US state stepping in to save the US and get the lower interest rates it wanted. The UK was not insolvent, and if banks had gone bust without the swap lines, their shareholders should have taken the brunt, and the banks nationalised. But no, we stick with the neoliberal narrative.

Tax and spending

Which brings us to the all-important question: we can use taxes to reduce inequality but can we use them to enable the government to spend more? This depends on the level of unused capacity in the UK economy. How much slack is there in UK factories and in our supply chains? What percentage of the population is unemployed or underemployed? If there is slack, then increasing taxes will increase unemployment, as taxation deprives the economy of money that has already been spent into existence.

If we have spare capacity and unemployment, we need to reduce taxes. Given our desire to reduce inequality, it follows that hefty taxes on the wealthy, should be accompanied by greater tax reductions on the rest of us. Otherwise wealth taxes will turn the Reeves-induced austerity-lite stagnation into greater stagnation.

If we have a lack of resources, we should also note that spending on education, science and training creates resources. If, even after such spending, a careful analysis of supply chains, of firms’ mark-ups and of labour force surveys reveal we are running at full stretch, then tax rises on the private sector will be needed to release resources to achieve our goals. Given that the very wealthy save, whereas the poor have to spend all their income, taxing the very wealthy when the economy is overheating and resources are scarce, is less efficient at reducing the overheating than increasing taxes on the less well off.

It follows that if we need to reduce parts of the private sector so that labour and technology can be used to build designated priorities, such as climate change technology, and health spending, then prior to job losses in the sectors we reduce in size, we must make it clear that new jobs are available. It’s the familiar argument: you shouldn’t close down an industry without offering alternative opportunities.

The hegemonic narrative

Every ruling elite organises to maintain hegemony, starting with ideology with which to frame and justify government policy. In the UK the ideological position is that free markets are best, that we must ensure that our policies do not frighten the wealthy off, because we need them. Government is poor at running companies or choosing where to invest and should get out of the way: we must always placate the wealthy and their markets.

We should reject these assertions.

The money we spend to train doctors and pay carers comes directly from the Treasury which can never run out of pounds. The ability of the government to spend is not limited by capital flight: Bank of England reserves are a monopoly: no one else can create them. The left should stop rescuing the finance sector and the very wealthy and instead focus on the rest of us.

A close analysis of central bank operations reveals that the government funds its spending before it taxes and it is the implications of this on which the UK left disagrees.

The danger of government spending is that it may cause inflation and/or devaluation. If we do not have the real resources to build and provide the goods and services we want, then spending more will indeed just bid up prices.

Currently in the UK, despite claimed shortages of labour, heterodox economists and the Social Market Foundation (SMF), a UK‑based think tank, estimated that in 2024 there were around five to six millionworking‑age UK individuals who were not in the workforce but who would work if decent work were available. And labour shortages in certain areas, both geographic and sectoral, need to be addressed by skills training and decent wages. That will ease inflationary pressure, not increase it. If this is true, then the UK has spare human resources and can expand government spending without increasing taxation and without risking inflation.

And the final fear: a run on the pound. The reason why the West, including Germany and the USA, are not growing as fast as they want, is because the dollar, the pound and the euro are overvalued in relation to far eastern currencies. Secondly, the trade surplus countries are suppressing labour costs, and in the eurozone they are forcing Spain, Italy and others into private sector debt which they use to buy the exports of the trade surplus countries. This is unsustainable in the long run. To cap it all, the suppression of government spending – as per the neoliberal narrative – is locking the EU into stagnation and causing a lack of strategic long-term planning coupled with insufficient Research and Development.

As for devaluation phobia: provided markets know governments will not be browbeaten, they bet against a currency at their own risk: the US dollar and Canadian dollar undergo considerable volatility and the Canadian government is sanguine. If the pound plunges, and the UK government doesn’t jack up interest rates to try and defend it, UK assets become good value and the pound moves back up again.

The left should not be intimidated and should confront neo-liberal free market beliefs.

Steve Laughton Dip Econ/ MA Econ has been in the Labour Party since 1981. He was the Political Education Officer of Bournemouth East and Bournemouth West Labour for several years. He is a member of Momentum. Recently he has devoted his time to economics, and remains an independent philosophical economist, who believes current economic wisdom is deeply flawed and that centrist politicians who follow it are paving the way for their own demise.

Image: c/o Labour Hub.

Saturday, August 02, 2025

Capital, power and war: The crisis of Russia’s peripheral accumulation regime

Neither of us denies the importance of either economics or ideology in shaping state policy; and both of us agree that political outcomes emerge from the complex and dynamic interaction between the two. As we concluded, the key lies in understanding the balance between structural economic determinants and the more contingent role of political decisions. Economics sets the parameters and long-term trends; politics intervenes in specific conjunctures, tipping the scales toward one outcome or another.

In his essay “Once Again on the Trade Unions, the Current Situation and the Mistakes of Trotsky and Bukharin,” Vladimir Lenin presents what may appear to be two contradictory claims: (a) politics is a concentrated expression of economics, and (b) politics must take precedence over economics — an assertion he calls “an ABC of Marxism.” Far from a contradiction, this is a dialectical formulation.

In general, economic relations define the limits and terrain within which politics operates. Yet under certain historical conditions — especially during revolutionary ruptures — politics becomes the vehicle through which those economic relations are transformed. Subjective factors such as class consciousness, political organisation and leadership can gain decisive importance. In this sense, politics can “lead” economics by organising class forces in ways that alter the very economic structures from which they emerged.

This dialectical reversal — where the superstructure acquires relative autonomy and, in specific conjunctures, reshapes the base — is a recurring theme in Marxist thought. Lenin’s position echoes Karl Marx’s analysis of the Paris Commune, a political event whose significance lay in its potential to transform the economic foundations of society. As Marx wrote in The Eighteenth Brumaire of Louis Bonaparte, people make their own history, but not under conditions of their own choosing — a formulation that captures the unity of structural constraints and political agency.

While acknowledging the important role of politics and ideology, it remains crucial to analyse how Russia’s model of capitalist accumulation created the structural conditions — the framework — within which subsequent political decisions were made. That is the focus of this article.

What kind of capitalism is Russia?

The accumulation regime that dominated Russia from the early 2000s until roughly 2013-14 — before slipping into stagnation — is best understood through the lens of Regulation theory, which emphasises the organic interdependence between economic structures, institutional forms and modes of reproduction. According to this approach, capitalism is not a single, uniform model but a historically specific configuration of accumulation and regulation. Each regime is defined by a coherent (if often temporary) alignment between how profits are generated (the accumulation regime) and how social and institutional structures support or contain this process (the mode of regulation).

Drawing on Robert Boyer’s typology of post-socialist accumulation regimes, Russia — along with Ukraine — fits squarely within the category of oligarchic or rentier capitalism. In this model, the economy is heavily dependent on raw material exports, while capital accumulation is deeply entangled with political power and rent distribution. Unlike developmental or export-oriented regimes, where capital is reinvested into expanding production, the Russian model channels surplus rent toward elite consumption, asset protection abroad and politically-mediated redistribution.

This model also bears the deeper structural imprint of peripheral capitalism, as theorised by Boris Kagarlitsky in Empire of the Periphery and Restoration in Russia: Why Capitalism Failed. Kagarlitsky argues that Russia’s capitalist development after the Soviet collapse was not oriented toward internal industrial transformation or the creation of a self-sustaining national economy. Rather, it was shaped by the requirements of the global capitalist centre, especially in Western Europe and North America.

Russia emerged as a provider of cheap raw materials and a destination for capital outflows into real estate and financial safe havens. Its integration into the world-system was therefore subordinate, driven by external demand and the reproduction of global inequalities rather than domestic developmental needs. In this sense, Russia’s position more closely resembles that of a peripheral capitalist formation, structurally dependent on rent extraction and external capital circuits.

This regime relied on the extraction of resource rents — primarily from oil, gas, and metals — that became the foundation of foreign exchange earnings, fiscal revenues, and elite enrichment. But accumulation followed a political, not competitive, logic. Access to rents was governed by proximity to the state. Contracts, licenses and control over public assets — not entrepreneurial innovation — determined wealth and influence. In this sense, Russian capitalism conforms to Max Weber’s notion of political capitalism, in which the means of enrichment are shaped by privileged access to political power rather than market dynamics.

Branko Milanović has argued that this kind of capitalism thrives not through production but rent-seeking. Volodymyr Ishchenko notes in the Ukrainian context (which mirrors the Russian experience), the boundaries between business and politics are porous: capitalist accumulation depends less on autonomous institutions and more on informal networks, clientelist ties, and shifting elite coalitions. Kagarlitsky similarly describes Russian capitalism as a system in which class power is exercised through a fusion of economic and administrative control, with state elites doubling as capitalists.

Why did Russia’s capitalism run out of steam?

Despite its apparent stability during the commodity boom years, Russia’s accumulation regime began to falter by the mid-2010s. Its decline was driven by a set of interrelated internal and external contradictions that gradually eroded its capacity to reproduce capital on an expanded scale.

The first and most immediate sign of strain was a profitability crisis. While the natural resource sectors continued to yield substantial rents, much of the rest of the economy — particularly manufacturing and services — faced stagnating productivity and falling returns. Marx observed that capital must expand or perish. In Russia’s case, the expansionary impulse was not exhausted due to a shortage of capital, but rather because the regime failed to generate sustained internal dynamism.

Figure 1: Business Financial return indicators in Russia, 2000-2024. Source: Author’s presentation based on the Federal State Statistics Service of the Russian Federation, https://rosstat.gov.ru/statistics/finance#

This crisis of profitability is evident in key financial return indicators (Figure 1). Both return on assets (ROA) and return on sales (ROS) declined steadily from the mid-2000s until the mid-2010s. ROS, which had hovered around 13–14% in the early 2000s, dropped to just over 8% by 2015. ROA fell even more dramatically, from a peak above 12% in 2006 to just 3% in 2015. This prolonged decline reflected not only the structural limits of rent-based accumulation, but also the mounting constraints imposed by Russia’s deteriorating external environment, particularly following the 2014 annexation of Crimea.

Yet starting around 2015–2016 — precisely as Russia began to “flex its muscles” geopolitically — profitability indicators began to recover. This resurgence was not the result of productive diversification or reinvestment, but stemmed from a combination of import substitution, state-directed spending and militarisation. The spike in ROS in about 2021–22 signals a wartime reprieve, driven by rising commodity prices and emergency fiscal measures. However, the recovery was uneven: ROA remained well below its pre-crisis peaks, suggesting that profitability in Russia is still dependent on external rents and state interventions, rather than structural competitiveness.

Closely tied to the profitability dynamic was the question of domestic investment. Russian capitalists have long preferred to safeguard their wealth abroad, and this behaviour persisted even during the boom years. Structural barriers — including weak property rights, politicised courts, elite factionalism and the chronic absence of institutional trust — made Russia a high-risk environment for long-term reinvestment. Even when capital was available, flight remained the rational option.

The consequences of capital aversion are starkly reflected in the growth pattern of investment in fixed assets between 2011–20. After reaching more than 20% in 2012, the growth rate steadily declined, falling to just 5.5% by 2020. This sustained slowdown mirrored the erosion of profitability, with both trends bottoming out around the same time.

The close alignment of these trajectories reinforces the structural link between profitability and investment: from Marxian, Keynesian and Kaleckian perspectives alike, falling profit rates provoke an “investment strike,” as capitalists respond by scaling back expansion and postponing capital commitments. Empirically, this is supported by a moderate to strong correlation (r between 0.66 and 0.67) that is statistically significant at the 1% level between investment growth and both ROA and ROS, confirming that declining returns materially shaped investment behaviour in this period.

Figure 2: Annual growth of investment in fixed assets. Source: Author’s presentation based on the Federal State Statistics Service of the Russian Federation, https://rosstat.gov.ru/folder/14304#

After 2021, a dramatic — but involuntary — reversal occurred. The annual growth of investment in fixed assets surged to more than 22% in 2022 and remained elevated in the years that followed. This sharp reactivation was not driven by renewed investor confidence but by a fundamentally altered operating environment. Capital controls, international sanctions and Russia’s financial decoupling from the West restricted traditional avenues for capital flight. Simultaneously, the state expanded military and infrastructure procurement and imposed sweeping import substitution mandates. Wartime fiscal expansion boosted returns in key protected sectors, reigniting investment not through incentives, but through necessity.

Yet, this rebound should not be misread as a sign of systemic strength. Capital remained within Russia not due to an improved investment climate, but because escape routes were closed. What appears as investment-led recovery is better understood as the redirection of surplus under siege: coerced, managed and politically orchestrated, rather than market-driven or strategically planned.

This dynamic underscores a broader analytical point: in peripheral political capitalism, accumulation is shaped less by market logic than by political constraints and structural dependencies. The correlation between profitability and investment in Russia is real — but it is mediated through a framework of elite behaviour, capital controls and geopolitical isolation.

In addition to these internal contradictions, the post-2014 rupture also severed key external linkages. Russia’s integration into global capitalism had always been subordinate: petrodollars were recycled into Western financial markets, while the domestic economy remained dependent on imported technology, components, and credit. The sanctions regime drastically curtailed these flows, undermining the very architecture of accumulation without offering a viable alternative.

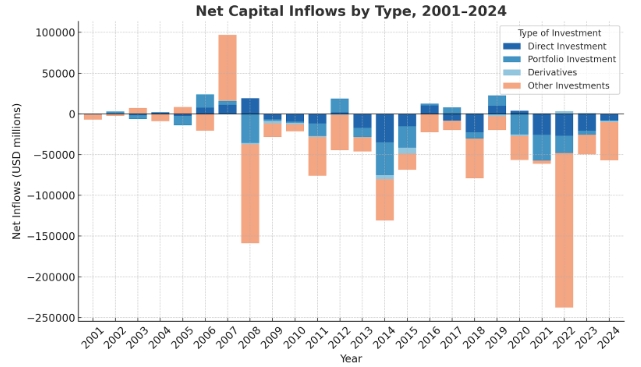

Capital flight remained a defining feature of the Russian accumulation regime even after 2014, despite tightening sanctions and capital controls. As the chart above shows, net capital outflows not only persisted but, in many cases, intensified, particularly in the form of other investments — a broad residual category that includes trade credits, intercompany loans, and bank deposits. These channels are often used for discreet or informal capital flight, especially when formal mechanisms are restricted. The share of other investments has on average remained high throughout the period, accounting in some years for up to 80% of all capital flows.

The huge capital outflow recorded in 2022 — driven by geopolitical uncertainty, emergency withdrawals and systemic disruptions in cross-border financial relationships — confirms the regime’s structural dependence on external financial circuits. However, the dynamics in 2023–24 suggest a partial reversal: outflows from other investments decreased significantly, and similar declines were observed across other categories, indicating a temporary containment of capital flight. Still, this shift should be interpreted cautiously — as a response to restricted exit routes and wartime controls, not as evidence of improved investor confidence or a structurally sound accumulation environment.

Finally, the end of the global commodity super-cycle in the mid-2010s eroded the fiscal foundation of the rentier model. Falling prices undercut both budget revenues and external surpluses. The temporary post-2022 rebound — driven by war-related price spikes and emergency spending — has not resolved these long-term vulnerabilities. If anything, it has exposed the fragility of a model that remains dependent on rents, repression, and reactive policy interventions.

Russia’s war-driven accumulation regime

The Russian economy has undergone a profound transformation since the escalation of the war in Ukraine in 2022. While the outlines of this transformation could already be discerned in the aftermath of the 2014 annexation of Crimea, it is only in the wake of the full-scale invasion and the unprecedented scale of Western sanctions that a new accumulation regime has coherently taken shape.

This section builds on the previous discussion of post-2014 and post-2022 trends — especially the decline of foreign direct investment, the reversal of net primary income flows and the reorientation of trade patterns — to outline the logic of the emergent model of capital accumulation. As I argue in my LINKS article “Russia’s Delinking from the West: The Great Equaliser,” this model represents a rupture from the previous globalist framework, centred instead on war-driven expansion and domestic reproduction.

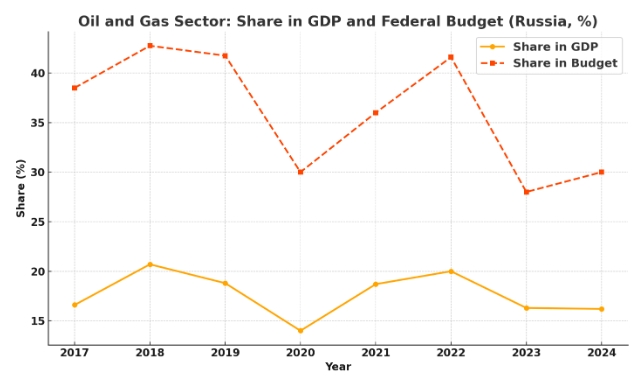

Yet how profound is this transformation in structural terms? Despite the regime’s pivot toward military-industrial expansion and sanctioned self-reliance, the basic logic of peripheral capitalist accumulation — rooted in natural resource exports, particularly hydrocarbons — remains intact (Figure 4). After the COVID-induced contraction in 2020, when the oil and gas sector’s share in GDP dropped to 14%, there was a sharp recovery, peaking in 2022 at 20%, as global energy markets responded to the war with panic-driven price spikes. By 2023 and 2024, the share returned to around 16%, nearly identical to its 2017 level. This cyclical pattern suggests continuity rather than rupture: the export sector remains central to the Russian economy, and no genuine diversification or structural upgrading has occurred.

A similar pattern holds for the share of oil and gas revenues in the federal budget. Although this share declined in 2023 and 2024 — to 28% and 30% respectively, down from 41.6% in 2022 — the drop is not unprecedented. Comparable levels were observed during the 2020–21 period, reflecting earlier price and demand shocks. Whether the recent decline signals a sustained reduction in fiscal dependency or merely another phase in the commodity cycle remains to be seen. What is clear, however, is that the state budget remains structurally dependent on hydrocarbon rents, with oil and gas revenues consistently contributing between one-quarter and nearly half of federal income across the past decade.

The so-called “new” accumulation regime may therefore reflect a reorganisation of rent distribution and elite composition, but it does not alter the extractive foundation on which Russian capitalism rests.

Since 2022, Russia’s accumulation regime has become increasingly reliant on what could be termed “military Keynesianism,” a state-led effort to stimulate economic growth through huge defense spending, infrastructure development and industrial policy directed from above — the features analysed by Ishchenko, Matveev and Oleg Zhuravlev. The war effort and Western sanctions have largely displaced foreign investment and external trade as key sources of accumulation, replacing them with state demand, procurement contracts, and strategic subsidies.

Import substitution has intensified, not merely as a policy slogan but as an enforced reality. With Russia partially delinked from Western markets and supply chains, domestic industries have stepped in to fill the void, often under the shelter of high tariffs, financial controls and generous state support. These industries — ranging from agro-processing and logistics to basic manufacturing and chemicals — are not exposed to global competition; instead, they are protected and stabilised by predictable state contracts and informal rent-sharing arrangements.

This transformation has created new patterns of profitability, as illustrated by the chart tracking the evolution of profitability over time, particularly the rising trend since 2014 (Figure 1). Capitalists positioned in sectors aligned with state priorities — especially construction firms, arms manufacturers, and logistics companies — have seen profits rise even amid macroeconomic uncertainty.

For this cohort, the war has become not a disruption but a condition of accumulation. Any form of peace agreement that reopens Russia to global competition and winds down public investment in military and reconstruction sectors would likely erode these profits and restore the stagnation characteristic of the late 2010s. Thus, peace — particularly under Western terms — represents not an opportunity but a threat to the new accumulation regime.

Although sanctions have inflicted damage in specific areas, particularly finance, technology and high-end manufacturing, Russian capitalism has, to a surprising extent, adapted to the new constraints. Many of the sanctions have been partially endogenised: they are no longer experienced simply as external shocks, but as part of the system’s operating logic.

Domestic producers have gained from the elimination of foreign competition, particularly in sectors where they were previously unable to compete. Capital and currency controls, imposed by the state in response to financial sanctions, have managed to stabilise outflows and preserve the ruble’s value. Parallel import schemes via China, Turkey, Central Asia and the Gulf have restored access to essential goods, including advanced technological components. In many cases, the state has absorbed the burden of adjustment, redistributing rents through subsidies and nationalisations that preserve elite interests.

War as an engine of regime stability

Sergey Aleksashenko, Vladislav Inozemtsev and Dmitry Nekrasov point out in their report Dictator’s Reliable Rear that the resilience of the Russian economy under sanctions and wartime pressure is not accidental but structurally grounded in a model of capital accumulation that functions increasingly well under conditions of confrontation. They highlight that profits in Russia today are not derived primarily from productivity gains or global competitiveness, but from state-controlled rent flows, preferential access to protected sectors, and the political consolidation of key industries. The war economy, in this view, has become internally coherent — one in which predictable returns, subdued elite rivalry and regime stability are tightly bound to the continuation of hostilities.

This logic creates strong structural disincentives for the cessation of conflict, especially under terms that would require territorial concessions, liberalisation or re-integration into Western-led institutions. Unlike the globalist accumulation model of the 2000s and early 2010s — which was premised on access to Western capital markets, real estate and offshore financial networks — the current regime is relatively insulated from Western volatility. For those now in command of state-connected enterprises, logistics monopolies and import-substituting industries, a prolonged or low-intensity conflict is not an existential threat but a stabilising condition.

This shift is rooted in a broader transformation of Russia’s class structure. The oligarchic elite that emerged in the 1990s and consolidated during the 2000s — reliant on Western capital, real estate and offshore havens — has been partially sidelined. Some lost access to their wealth through sanctions; others were absorbed into domesticated, state-aligned ventures. Their influence over accumulation strategies has diminished.

In their place, a new elite has taken shape: defense contractors, construction tycoons, sanctioned technocrats managing import-substituting sectors and regional bosses profiting from reconstruction in occupied territories. These actors are not embedded in global circuits of capital. Their fortunes depend on loyalty to the regime and continued access to wartime rents. A temporary truce — even one imposed by the Donald Trump administration — might reduce geopolitical risk, but it would also destabilise the domestic economic order that sustains them. The war has made them rich; peace could make them irrelevant.

The war has also taken on a broader function in the consolidation of political power. It serves not merely as an instrument of foreign policy, but as a domestic mechanism of elite cohesion and regime legitimation. Within this logic, support for the war becomes a loyalty test: political actors, businesspeople and even cultural figures are expected to demonstrate alignment with the state’s goals or face exclusion and repression.

War justifies authoritarian centralisation, suppresses dissent and allocates capital to favoured groups. It disciplines the elite and eliminates or neutralises internal competitors. In this context, even the idea of a “frozen conflict” that deescalates hostilities without resolving territorial issues may be seen as destabilising. It could reopen elite competition, embolden alternative factions — including the remnants of the pro-Western oligarchy — and undermine the ideological cohesion that the war effort currently supplies.

At the ideological level, the war has been framed by the regime as both a defensive measure against Western imperialism and a civilisational mission. This narrative has been deeply institutionalised, from media and education to official speeches and symbolic politics. Any concession — even one that does not involve formal territorial retreat — risks being read as betrayal. Such a move could demobilise supporters, invigorate nationalist hardliners and set a precedent for future Western demands regarding Crimea or other territories. Furthermore, even if sanctions relief were secured in exchange for a settlement, its long-term reliability is suspect. A future US administration may reverse any détente, as previous episodes of sanctions relief and rollback have shown.

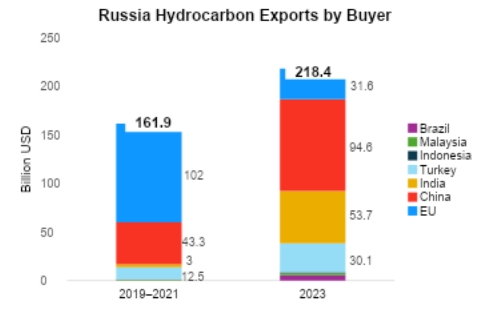

Finally, the war economy is no longer dependent on Western capital or markets for its reproduction. Russia’s external orientation has shifted decisively toward China, India, Turkey and the broader Global South. Trade volumes with these partners have expanded significantly, particularly in the energy sector. Figure 5 shows hydrocarbon exports to China, India and Turkey surged between 2019–21 and in 2023, while exports to the European Union collapsed. Energy flows have been re-routed eastward and southward, with China now absorbing nearly as much as the EU once did, and India and Turkey emerging as key buyers.

At the same time, Russia has increased its participation in BRICS and alternative financial and political forums. These ties offer not only economic lifelines but also new arenas of accumulation, investment and diplomatic recognition. Western markets and institutions are no longer the sole gateway to growth and reproduction. This diversification reduces the strategic leverage of the West — even if it were united in offering sanctions relief — in influencing the behaviour of the Russian capitalist class.

At first glance, this eastward turn might suggest a transition toward the kind of delinking envisioned by Samir Amin — an attempt to restructure the economy around domestic reproduction rather than dependency on the global core. In my earlier article, I proposed (somewhat provocatively) that elements of the wartime economy — such as the expansion of basic industrial production and a degree of downward redistribution — appeared to carry pro-poor features, potentially signaling the beginnings of a self-centred development path.

However, research that Kagarlitsky and I subsequently conducted — building on Minqi Li’s methodology of tracking cross-border value transfers — suggests a more sobering reality. While the redirection of trade flows from the West to the East has reduced the scale of net value transfers out of Russia, these transfers remain persistently negative. The bulk of surplus value that once flowed to the West now accrues to China, Russia’s new central trading partner.

Importantly, this reorientation trend predates the full-scale war. In 2018, Russia’s oil exports to China nearly doubled following the commissioning of the second leg of the Eastern Siberia–Pacific Ocean (ESPO) oil pipeline, raising capacity from approximately 15 to 30 million tons annually. Meanwhile, exports to the West stagnated. The later launch of the Power of Siberia natural gas pipeline in December 2019 — designed to reach a capacity of 38 billions of cubic metres by 2025 — further institutionalised the eastward flow of strategic commodities

Kagarlitsky and I argue, following Giovanni Arrighi, that this is not a case of delinking but of re-Orientation: a shift in dependency from one centre to another. Rather than escaping the structural logic of global capitalism, Russia has re-embedded itself within a different core–periphery dynamic — this time with China at the centre. Moscow may aspire to become a hub in an “alternative globalisation,” but economically it remains on the receiving end of unequal exchange.

Aleksashenko and his colleagues note that Russia is not simply “falling into China’s embrace” (already evident, as China accounted for 33.8% of Russia’s foreign trade turnover in 2023 — a share comparable to that of the EU in the mid-2010s). Rather, Moscow is transforming into a centre of an “alternative model of globalisation,” operating outside the frameworks of Western-controlled institutions and established rules.

The very features that make the present system seemingly unsustainable from a Western or liberal economic viewpoint — lack of investment, technological stagnation, exclusion from Western capital — are what allow the regime to control the flow of capital, suppress internal dissent, and sustain elite loyalty. War spending functions as a tool of internal redistribution, channeling rents to politically compliant actors and crowding out autonomous capitalist initiatives.

De-escalation would, paradoxically, destabilise this arrangement by reintroducing competition, restoring the political relevance of marginalised oligarchs, and weakening the ideological glue that now binds the state and capital. Vladimir Medinsky, Kremlin’s chief negotiator with Ukraine, has recently invoked Peter the Great’s 21-year war with Sweden to stress that Russia is prepared to fight “forever” in Ukraine.

It is therefore unsurprising that more voices in Ukraine (such as General Valerii Zaluzhny) and the West (for example, former NATO Secretary General Jens Stoltenberg) now speak in terms of a protracted conflict lasting not months but years — or even decades. While some actors may indeed see benefits in a prolonged standoff, such as expanded military-industrial activity or renewed geopolitical relevance, most view this trajectory with deep concern.

Paradoxically, however, many — including not only elites in Moscow but also observers in Western capitals — now perceive a low-intensity, contained conflict as more manageable and less destabilising than an unpredictable peace. Some Western analysts argue that the Russian economy will eventually succumb to fiscal exhaustion and demographic decline, while Ukrainian political and military elites increasingly recognise that the objective of a rapid and decisive military victory is no longer tenable. In this emerging consensus, strategic patience — through prolonged pressure, containment and attritional warfare — is seen as the most viable path forward.

This logic is mirrored in Moscow as well. As long as the economy avoids overheating and sanctions continue to be partially endogenised (as discussed earlier), the Russian leadership has little incentive to seek reconciliation. A controlled, relatively low-intensity war offers clear political and economic advantages: it sustains regime legitimacy, keeps Western pressure at bay, and consolidates the loyalty of the newly ascendant elite class. The material conditions of the war, rather than undermining the system, have been metabolised by it.

In this light, the war is not merely a geopolitical blunder or an ideological crusade. It has become a structurally functional component of Russia’s current capitalist order — serving as a mechanism of class cohesion, rent distribution and geopolitical realignment. As long as these functions remain intact and the costs contained, structural incentives will continue to favor prolonged confrontation over peace.

War as a structural feature, not a strategic mistake

This article has argued that Russia’s war in Ukraine is not simply a geopolitical miscalculation or ideological excess, but a structurally embedded feature of its capitalist accumulation regime. Faced with declining profitability, capital flight and external constraints, the system adapted through war-driven restructuring. A new elite emerged — rooted in defense, construction and import-substituting sectors — whose fortunes depend on continued conflict, not peace. Military Keynesianism, capital controls and rent redistribution stabilised accumulation and elite cohesion under siege conditions.

Rather than representing a rupture, this transformation refunctionalised existing features of Russian capitalism. The war economy absorbed sanctions and repurposed constraints into sources of domestic accumulation. Peace, especially under Western terms, would threaten this balance by reviving competition, weakening elite discipline and undermining the political legitimacy built on wartime mobilisation.

These findings challenge the liberal expectation that capitalism promotes peace through integration. The Russian case shows peripheral political capitalism can stabilise itself through confrontation, not despite it. War becomes not an interruption, but a mechanism of accumulation, class realignments and regime survival.

This does not mean that ideology and irrationality play no role. But as Kagarlitsky cautions in The Long Retreat: Strategies to Reverse the Decline of the Left, even when leaders appear to act irrationally, their madness “does not appear of its own accord, but develops as a side effect of the functioning of the system. Different social systems, cultures and political practices give rise to different manias.” In other words, political misjudgments — even extreme ones — are systemically conditioned. They emerge not outside of structure, but from within it.

In this sense, Russia may not be exceptional. Other states facing similar crises — sanctioned, marginalised or stagnating — may also turn to war as a political and economic strategy. The Russian experience should serve not only as a warning but as a framework for understanding how capitalism can endure, and even thrive, under conditions of sustained conflict.