Jerome Powell, Vladimir Putin, and Mohammed bin Salman are on the verge of throwing the entire world into a massive depression.

[Federal Reserve Chair] Powell’s interest rate increases are compounded by the action taken this morning by Russia and Saudi Arabia, leading the OPEC+ meeting in Vienna, to cut oil production by 2 million barrels a day.

These two leaders of OPEC+ have a visceral hatred of both President Joe Biden and democracy itself — and throwing oil prices to or above $100 a barrel and gas prices above $6/gallon here in the US will have massive political repercussions, handing a sword to Republican partisans who also openly hate democracy.

It will also fuel inflation, provoking even more wrong-headed rate increases by Powell. And it’s not like there aren’t credible voices telling Powell he’s playing with fire.

What, for example, do the United Nations’ Conference on Trade and Development (UNCTAD), former Labor Secretary Robert Reich, and the corporate accountability group Accountable.us all know that Powell and his mostly-Republican colleagues at the Fed fail to understand?

In a nutshell, it’s pretty straightforward: Today’s inflation is caused in large part by the one-off confluence of rebound from two years of depressed demand hitting highly monopolized and fragile supply systems.

To compound the problem, this situation has become an excuse for the world’s largest corporations — particularly the fossil fuel industry giants and their patrons in Russia and Saudi Arabia — to extract the largest profits in history from the rest of us.

Two weeks ago the World Bank warned us, as The Wall Street Journal headline noted, that fixing inflation by raising interest rates alone would be a disaster: “World Bank Warns of Global Recession Next Year if Central Banks Lift Interest Rates Too High.”

This week it’s the United Nations, as noted again by The Wall Street Journal in an article published Monday and titled: “U.N. Calls On Fed, Other Central Banks to Halt Interest-Rate Increases.”

The UNCTAD report, issued the same day as the Journal article reported on it, is blunt in its assessment. The lead paragraph on their report’s home page says it clearly:

The world is headed towards a global recession and prolonged stagnation unless we quickly change the current policy course of monetary and fiscal tightening in advanced economies.

The reason world bodies are talking about the US Fed and American interest rates is that when the US Fed raises interest rates here, other countries have to do the same or their currencies will begin to sink against the dollar.

Rapid devaluation like that can be very destructive to their economies, so what the Fed does, interest-rate-wise, the world must do.

And the world, increasingly, thinks this is going to be a disaster, particularly when combined with Russia and Saudi Arabia’s new actions today designed to destabilize western democracies.

A Fixed Idea of a Fix

But the Fed persists. Instead of heeding the warnings of “liberals” like the World Bank, the United Nations, corporate watchdog groups, and wise elders (and Ph.D. economists) like Reich, Republican bankster Powell and many of his colleagues around the world are exclusively using the sledgehammer of interest rate increases to try to tamp down inflation.

Raising interest rates has already crippled the American housing market; mortgage companies are laying off employees and going bankrupt in ways we haven’t seen since the Bush Crash of 2008. Refinance applications are down 45 percent in just six months, and houses are sitting on the market longer and longer every week.

Amazon just laid off 100,000 employees, and both Netflix and Google have announced hiring freezes. The signs of impending recession are all around us. Technically we’re already in one, as GDP has contracted for two straight quarters.

But Powell and the Fed are on course for more interest rate increases. Meanwhile, some of our largest and most profitable corporations are on a price-gouging binge that is exploding inflation.

As Accountable.us notes in a report this week, US gasoline prices are up 13 percent for the year, while oil prices have only increased 1.2 percent. In other words, they are screwing us.

Today’s OPEC+ took about 2 percent of the world’s crude oil off the market, a radical action that will explode oil prices and send gas prices spiraling up just in time for the November election.

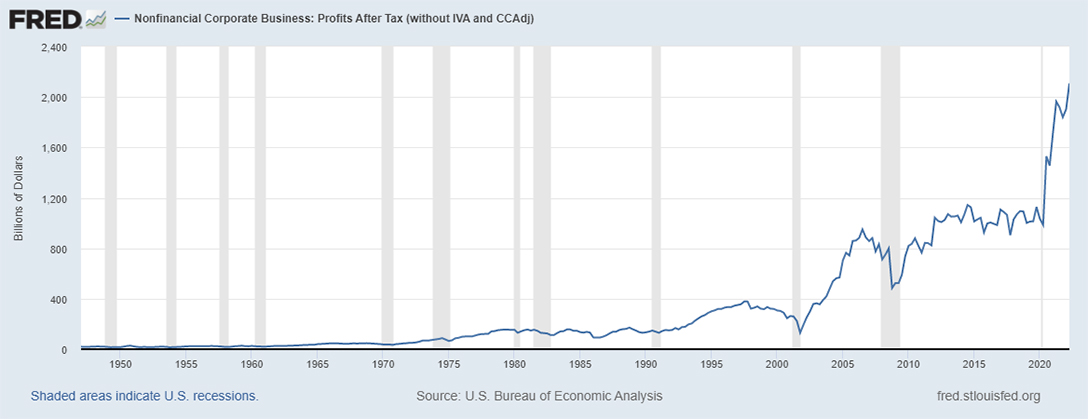

Meanwhile, corporate profits across the board are higher than any time in American history, as the Federal Reserve documents:

The explosion in after-tax corporate profit. Graph courtesy of the St. Louis Federal Reserve. Photo credit: FRED

As Reich notes in his excellent Substack newsletter:

Yet the Fed isn’t paying attention. Minutes of the Fed’s July 26-27 policy meeting reveal seven mentions of ‘wage’ or ‘wages’, 17 of ‘labor market’, eight of ‘job’ or ‘jobs’, and not one of ‘profit’.

Inflation and Oligopoly

Inflation isn’t particularly mysterious: It’s simply what happens when prices go up or there’s a decline in the purchasing power of money.

It can be driven by supply shocks — shortages of essential commodities — as it was in the 1970s by the Arab Oil Embargo. It can be driven by fiscal irresponsibility, as we’ve seen in developing countries. Or it can be driven by an economy that no longer responds to competitive pressures.

Supply shocks arguably began today’s inflation, but it’s the lack of competition that’s sustaining and driving it today.

In an unregulated capitalist system, the first imperative of business is to eliminate competition. This can be done by offering a better product or the same product at a lower price. It can be accomplished through innovation and invention. It can be accomplished by better marketing and promotion.

But the easiest way to eliminate competition is to create monopolies. As I lay out in The Hidden History of Monopolies (forward by Ralph Nader), this is the path that American companies had chosen for them by Ronald Reagan when, in 1983, he directed the Department of Justice, the Securities and Exchange Commission, and the Federal Trade Commission to essentially stop enforcing our nation’s antitrust laws.

The immediate result was an explosion of mergers and acquisitions, what people old enough to remember the era knew as the “M&A Mania.” Michael Milken, “Chainsaw Al” Dunlap, Michael Douglas in the movie Wall Street were all singing the same tune: Smash together all the medium-sized companies into giant behemoths that would never again have to worry about real or meaningful competition.

By the turn of the century we’d achieved a state of oligopoly, a situation where every industry in America was finally dominated by a handful of companies that worked together like cartels to monopolize markets.

When one airline raises prices a hundred bucks, for example, every other one does the same five minutes later. When one brand of potato chips downsizes their bags by an ounce, all its “competitors” do the same the next day.

As a result, the average American pays — every year — $5,000 more in total for everything from cell service to drugs to internet access than do the citizens of countries that still enforce antitrust laws, like Canada and most of Europe.

And now these corporate giants, throwing millions into this fall’s elections on behalf of Republican candidates, are using their monopolistic positions to squeeze more and more profits out of the American consumer.

The UN Conference on Trade and Development has a simple and straightforward solution to the problem of corporate price gouging driving inflation. They are explicitly calling on:

…[g]overnments to deploy a pragmatic strategy, including price controls, antitrust measures and windfall taxes on excessive corporate profits and to use these funds to support the most vulnerable.

The Economic-Political Convergence

Instead, the Republican at the head of our Fed is planning to further increase interest rates, provoking the first serious recession during the administration of a Democratic president since Jimmy Carter was bushwhacked by the Reagan campaign late in 1980.

They say the Fed and its chair are immune from political pressure. It’s BS.

In 1965, President Lyndon Johnson famously pulled his Fed chairman, Bill Martin, into the Oval Office and slammed him up against a wall, warning him to stop raising interest rates. Martin had just announced a rate hike coming up and he followed through, but that was it: He didn’t repeat his error for the next three years.

The month after LBJ announced he wasn’t going to seek reelection, however, Martin raised interest rates by a full point. The political pressure was off and Martin reacted.

I’m not suggesting that Biden should slam Powell against a wall, but going hard on the UN’s suggestions is an easy alternative, particularly given the coming explosion in gasoline prices.

When, back in March, Biden tried to reach out to our allies Saudi Arabia and the UAE to ask them to restore the production they’d cut under threat from Trump in 2020, both refused to take his call, according to press reports.

Meteor Blades reported at Daily Kos that The Wall Street Journal laid it out:

The Saudis have signaled that their relationship with Washington has deteriorated under the Biden administration, and they want more support for their intervention in Yemen’s civil war, help with their own civilian nuclear program as Iran’s moves ahead, and legal immunity for Prince Mohammed in the US, Saudi officials said. The crown prince faces multiple lawsuits in the US, including over the killing of journalist Jamal Khashoggi in 2018.

The Emiratis share Saudi concerns about the restrained U.S. response to recent missile strikes by Iran-backed Houthi militants in Yemen against the UAE and Saudi Arabia, officials said. Both governments are also concerned about the revival of the Iran nuclear deal, which doesn’t address other security concerns of theirs and has entered the final stages of negotiations in recent weeks.

The outcome was predictable. Saudi Arabia and Russia are cutting oil production to keep oil prices and profits high, while Biden is attacked from every direction in the US for high prices at the pump.

Republican politicians grandstand on the issue and hammer it daily into the news, blaming the increased price of gasoline on a president who’s trying to both get Iranian oil back on the market and increase Saudi production.

The high price of gas and diesel, meanwhile, keep jacking up US inflation, giving the GOP another lead pipe to hit Democrats over the head with.

The United Kingdom — run by a Conservative government — just put into place a windfall profits tax on their fossil fuel industry: Biden, House Speaker Nancy Pelosi (D-CA), and Senate Majority Leader Chuck Schumer (D-NY) should do the same and push it through Congress via reconciliation right after the election.

Similarly, Biden could instruct his DOJ, FTC, and SEC to begin comprehensive analysis of those sectors of the American economy where monopoly and oligopoly are making it easy to price gouge American consumers.

Big Oil, banks, airlines, internet service providers, Big Pharma, cell companies, media operations, and pharmaceuticals are all good places to start.

History shows it is possible to slow — and even stop — inflation without producing a recession. It also shows that overzealous Fed activity, such as Powell is currently risking, can produce a disaster.

Let’s repeat the best of history rather than the worst.

Reprinted from The Hartmann Report with the author’s permission.

Thom Hartmann is a four-time Project Censored-award-winning, New York Times best-selling author of 34 books in print and the #1 progressive talk show host in America for more than a decade.

No comments:

Post a Comment