In persisting with its high rates policy, the Fed is acting like James Dean in the famous “chicken run” auto race in Rebel Without a Cause.

July 14, 2024

Source: Institute for New Economic Thinking

man look red 3d arrow broke the floor

On June 13th, financial markets discovered they had overestimated the likelihood that the Federal Reserve would soon be cutting interest rates. Federal Reserve Chair Jerome Powell’s remarks at his press conference and the Federal Open Market Committee’s freshly updated quarterly “Summary of Economic Projections” pointed forcibly to the conclusion that the Fed would likely cut rates only once before the end of 2024.

In the midst of their own historic surge, US financial markets could mostly afford just to sigh. Reactions elsewhere were less sanguine: Some international commentators worried that higher for longer US rates would make repaying foreign dollar loans harder and accelerate a movement of capital out of the developing world. But even in the US, a chorus of misgivings welled up about disappointing retail sales, slumping home construction, the effects of prolonging elevated interest rates on ordinary consumers, weaknesses in commercial real estate held by many banks, and other signs of a slowly tightening squeeze on the economy. Economist Claudia Sahm summed up many of these misgivings when she warned of slowly rising unemployment, commenting, “My baseline is not recession…but it’s a real risk, and I do not understand why the Fed is pushing that risk. I’m not sure what they’re waiting for…The worst possible outcome at this point is for the Fed to cause an unnecessary recession.”

The Fed has a ready answer: It fears that the U.S. inflation rate will remain elevated for some time to come. Overall inflation remains high, mostly because of the stubbornness of services inflation. As the Bureau of Labor Statistics reported, the Consumer Price Index (CPI) rose by 3.3% (year-over-year) in May, but service inflation, excluding energy services, rose by 5.3% year-over-year.

Many observers blame the ‘sticky’ services inflation on nominal wages, which are rising as workers strive to catch up with inflation. Chilling out services inflation would thus be socially very costly: it would require considerably more monetary tightening by the Fed and cause a spike in unemployment. Although the Fed is not (yet) willing to go down this road, the stubbornness of services inflation means that U.S. interest rates will remain elevated to achieve the Fed’s 2% inflation target.

But this answer, sanctified as it is by generations of warnings from inflation hawks about wage/price spirals, is too easy.

More than a year ago, we analyzed the wave of inflation that was rolling over most of the world. We forecast that efforts to cure inflation in the United States by raising interest rates could not succeed at anything remotely resembling acceptable cost. The problem at its starkest is this: services inflation is heavily driven by surging increases in consumer spending on restaurants, travel, healthcare, and other higher-priced services.

Most of this spending comes from the very rich: affluent, often older, Americans who have benefited from the outsized gains in the U.S. housing and stock markets in recent years. Record increases in household wealth have given the rich confidence to increase their spending, which is a big reason why the American economy has defied expectations of a slowdown in the face of considerably higher interest rates. This wealth effect is a major driver of persisting services inflation.

Let us look more closely at the relevant facts. Spurred on by the ultra-low interest rates set by the Fed, average U.S. house prices rose by 47% between the first quarter of 2020 and the first quarter of 2024 and reached another record in recent days. As a result, the value of household owners’ equity in real estate increased by $13.4 trillion. Stock prices, as measured by the S&P 500 index, are more than 80% higher than they were five years ago, adding trillions of dollars to household wealth. As a result, U.S. household wealth has shot up by a record $47 trillion during 2020Q1-2024Q1 and, recently topped out again.

The wealth gains are hardly universal. The wealthiest 1% of American households captured 30% of this spectacular rise in financial wealth, while the wealthiest 10% garnered 59% of the wealth gains (amounting to $21.7 trillion). The bottom 50% of the wealth distribution, in contrast, received a pitiful 5% of the recent aggregate increase in household wealth. Wealth is also disproportionately held by older Americans and, of course, whites. People aged 55 and over own nearly three-quarters of all household wealth. However, many older Americans face significant financial challenges: one-quarter of Americans over age 50 have no retirement savings (according to a survey by the AARP).

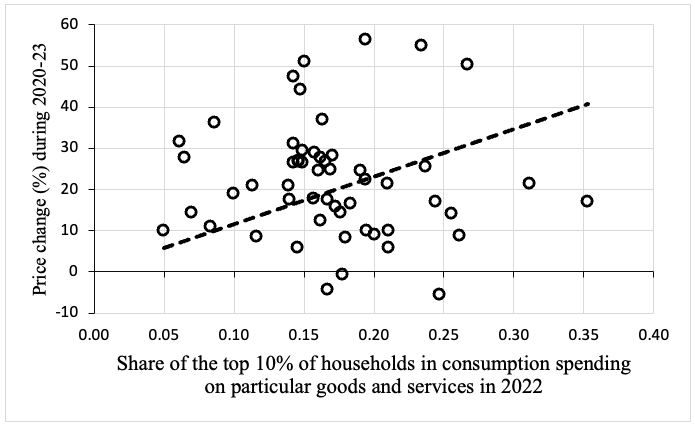

It is reasonable to expect that some part of this increase in household wealth will impact household consumption, especially spending by the wealthiest 1% or 10% of U.S. households, and through that, affect inflation. Our recent study relies on very conservative estimates of the effect of a $1 increase in household wealth on consumer spending to estimate the size of those effects: we find that the wealth effect accounts for almost all of the recent rise in American consumer spending. Economists at Moody Analytics and Visa concur, reporting similar impacts of higher household wealth on spending. In support of our argument, the figure (below) shows that prices have increased significantly faster during 2020-2023 for goods and services purchased by the richest 10% of U.S. households.

The Fed’s monetary tightening reinforces the dual nature of the American economy. On the one hand, a minority of very rich Americans who own houses, stocks and cars, remain relatively unaffected by the higher interest rates. Their spending is relatively immune to the Federal Reserve’s push to slow growth and tame inflation through higher borrowing rates, because it rarely requires borrowing and because their ability to provide collateral secures them preferential rates when they do add debt.

Prices have increased more for goods and services bought by the rich

Source: Ferguson and Storm (2024).

By contrast, the majority of Americans are enduring a combination of unaffordable house prices, increasing rents, high mortgage rates, and (despite many widely advertised claims to the contrary) stagnating (even declining) real wages, that make it close to impossible to buy a house unless you already own one. This bifurcation of the U.S. economy feeds on the increasing economic heft of the superrich, which is quickly transforming America’s economic structure: jobs in high-end restaurants were flourishing, while low-paid work in nursing homes, childcare, or education dries up. The outcome is not just distributionally regressive, but also plainly irrational.

In persisting with its high rates policy, the Fed is acting like James Dean in the famous “chicken run” auto race in Rebel Without a Cause. It is embarrassed by its failure to foresee the extent of inflation and is determined to control inflationary expectations. So, it persists in a policy that many analysts recognize is increasingly risky (or “data-driven” in the jargon, meaning that the Fed is sailing far beyond the Pillars of Hercules).

The problem is that sticking with the policy will send the economy over the cliff since the Fed refuses to recognize the link between the wealth effect, consumption spending by the rich, and inflation. Higher interest rates simply cannot cure this problem save through a Volcker-like tightening of monetary policy drastic enough to kill off the wealth effect. This would almost certainly throw the U.S. economy into a major recession, with no end of profound effects. Right now, the Fed is simply looking for something to turn up, while it persists with the current high interest rates and hopes for the best.

The sad truth is that this policy conundrum has been created by the Fed itself. It is time to take away the keys in this chicken run. We cannot rely on the Fed to get the economy out of this mess. We need fiscal and other policies, including serious efforts to regulate industries such as electricity production and transmission in the public interest, to address the underlying problems, not futile interest rate squeezes on the rest of the economy.

man look red 3d arrow broke the floor

On June 13th, financial markets discovered they had overestimated the likelihood that the Federal Reserve would soon be cutting interest rates. Federal Reserve Chair Jerome Powell’s remarks at his press conference and the Federal Open Market Committee’s freshly updated quarterly “Summary of Economic Projections” pointed forcibly to the conclusion that the Fed would likely cut rates only once before the end of 2024.

In the midst of their own historic surge, US financial markets could mostly afford just to sigh. Reactions elsewhere were less sanguine: Some international commentators worried that higher for longer US rates would make repaying foreign dollar loans harder and accelerate a movement of capital out of the developing world. But even in the US, a chorus of misgivings welled up about disappointing retail sales, slumping home construction, the effects of prolonging elevated interest rates on ordinary consumers, weaknesses in commercial real estate held by many banks, and other signs of a slowly tightening squeeze on the economy. Economist Claudia Sahm summed up many of these misgivings when she warned of slowly rising unemployment, commenting, “My baseline is not recession…but it’s a real risk, and I do not understand why the Fed is pushing that risk. I’m not sure what they’re waiting for…The worst possible outcome at this point is for the Fed to cause an unnecessary recession.”

The Fed has a ready answer: It fears that the U.S. inflation rate will remain elevated for some time to come. Overall inflation remains high, mostly because of the stubbornness of services inflation. As the Bureau of Labor Statistics reported, the Consumer Price Index (CPI) rose by 3.3% (year-over-year) in May, but service inflation, excluding energy services, rose by 5.3% year-over-year.

Many observers blame the ‘sticky’ services inflation on nominal wages, which are rising as workers strive to catch up with inflation. Chilling out services inflation would thus be socially very costly: it would require considerably more monetary tightening by the Fed and cause a spike in unemployment. Although the Fed is not (yet) willing to go down this road, the stubbornness of services inflation means that U.S. interest rates will remain elevated to achieve the Fed’s 2% inflation target.

But this answer, sanctified as it is by generations of warnings from inflation hawks about wage/price spirals, is too easy.

More than a year ago, we analyzed the wave of inflation that was rolling over most of the world. We forecast that efforts to cure inflation in the United States by raising interest rates could not succeed at anything remotely resembling acceptable cost. The problem at its starkest is this: services inflation is heavily driven by surging increases in consumer spending on restaurants, travel, healthcare, and other higher-priced services.

Most of this spending comes from the very rich: affluent, often older, Americans who have benefited from the outsized gains in the U.S. housing and stock markets in recent years. Record increases in household wealth have given the rich confidence to increase their spending, which is a big reason why the American economy has defied expectations of a slowdown in the face of considerably higher interest rates. This wealth effect is a major driver of persisting services inflation.

Let us look more closely at the relevant facts. Spurred on by the ultra-low interest rates set by the Fed, average U.S. house prices rose by 47% between the first quarter of 2020 and the first quarter of 2024 and reached another record in recent days. As a result, the value of household owners’ equity in real estate increased by $13.4 trillion. Stock prices, as measured by the S&P 500 index, are more than 80% higher than they were five years ago, adding trillions of dollars to household wealth. As a result, U.S. household wealth has shot up by a record $47 trillion during 2020Q1-2024Q1 and, recently topped out again.

The wealth gains are hardly universal. The wealthiest 1% of American households captured 30% of this spectacular rise in financial wealth, while the wealthiest 10% garnered 59% of the wealth gains (amounting to $21.7 trillion). The bottom 50% of the wealth distribution, in contrast, received a pitiful 5% of the recent aggregate increase in household wealth. Wealth is also disproportionately held by older Americans and, of course, whites. People aged 55 and over own nearly three-quarters of all household wealth. However, many older Americans face significant financial challenges: one-quarter of Americans over age 50 have no retirement savings (according to a survey by the AARP).

It is reasonable to expect that some part of this increase in household wealth will impact household consumption, especially spending by the wealthiest 1% or 10% of U.S. households, and through that, affect inflation. Our recent study relies on very conservative estimates of the effect of a $1 increase in household wealth on consumer spending to estimate the size of those effects: we find that the wealth effect accounts for almost all of the recent rise in American consumer spending. Economists at Moody Analytics and Visa concur, reporting similar impacts of higher household wealth on spending. In support of our argument, the figure (below) shows that prices have increased significantly faster during 2020-2023 for goods and services purchased by the richest 10% of U.S. households.

The Fed’s monetary tightening reinforces the dual nature of the American economy. On the one hand, a minority of very rich Americans who own houses, stocks and cars, remain relatively unaffected by the higher interest rates. Their spending is relatively immune to the Federal Reserve’s push to slow growth and tame inflation through higher borrowing rates, because it rarely requires borrowing and because their ability to provide collateral secures them preferential rates when they do add debt.

Prices have increased more for goods and services bought by the rich

Source: Ferguson and Storm (2024).

By contrast, the majority of Americans are enduring a combination of unaffordable house prices, increasing rents, high mortgage rates, and (despite many widely advertised claims to the contrary) stagnating (even declining) real wages, that make it close to impossible to buy a house unless you already own one. This bifurcation of the U.S. economy feeds on the increasing economic heft of the superrich, which is quickly transforming America’s economic structure: jobs in high-end restaurants were flourishing, while low-paid work in nursing homes, childcare, or education dries up. The outcome is not just distributionally regressive, but also plainly irrational.

In persisting with its high rates policy, the Fed is acting like James Dean in the famous “chicken run” auto race in Rebel Without a Cause. It is embarrassed by its failure to foresee the extent of inflation and is determined to control inflationary expectations. So, it persists in a policy that many analysts recognize is increasingly risky (or “data-driven” in the jargon, meaning that the Fed is sailing far beyond the Pillars of Hercules).

The problem is that sticking with the policy will send the economy over the cliff since the Fed refuses to recognize the link between the wealth effect, consumption spending by the rich, and inflation. Higher interest rates simply cannot cure this problem save through a Volcker-like tightening of monetary policy drastic enough to kill off the wealth effect. This would almost certainly throw the U.S. economy into a major recession, with no end of profound effects. Right now, the Fed is simply looking for something to turn up, while it persists with the current high interest rates and hopes for the best.

The sad truth is that this policy conundrum has been created by the Fed itself. It is time to take away the keys in this chicken run. We cannot rely on the Fed to get the economy out of this mess. We need fiscal and other policies, including serious efforts to regulate industries such as electricity production and transmission in the public interest, to address the underlying problems, not futile interest rate squeezes on the rest of the economy.

No comments:

Post a Comment