Reuters | June 20, 2024 |

Glencore currently operates 26 mines in 21 thermal and coking coal mining complexes across Australia, Colombia and South Africa. (Image courtesy of Glencore.)

Coal is doomed, or so the energy thesis goes. Many banks, insurers and investors have backpedalled from or abandoned the carbon-belching fossil fuel, prompting companies that excavate it to complain they cannot get mainstream or affordable financing. One corner of the industry, however, is burning strongly: the coking, or metallurgical, variety used to make steel. For sellers, it’s a diamond underneath the growing pile of mining M&A. Buyers, however, are in a race against low-emissions alternatives to justify their strategies.

The black rock’s lingering sparkle is good news for Anglo American boss Duncan Wanbland. His company’s Australian coal operation probably will be offloaded soon as part of the overhaul designed to help thwart rival BHP’s unsolicited $49 billion takeover attempt last month. Recent transactions suggest there will be no shortage of suitors.

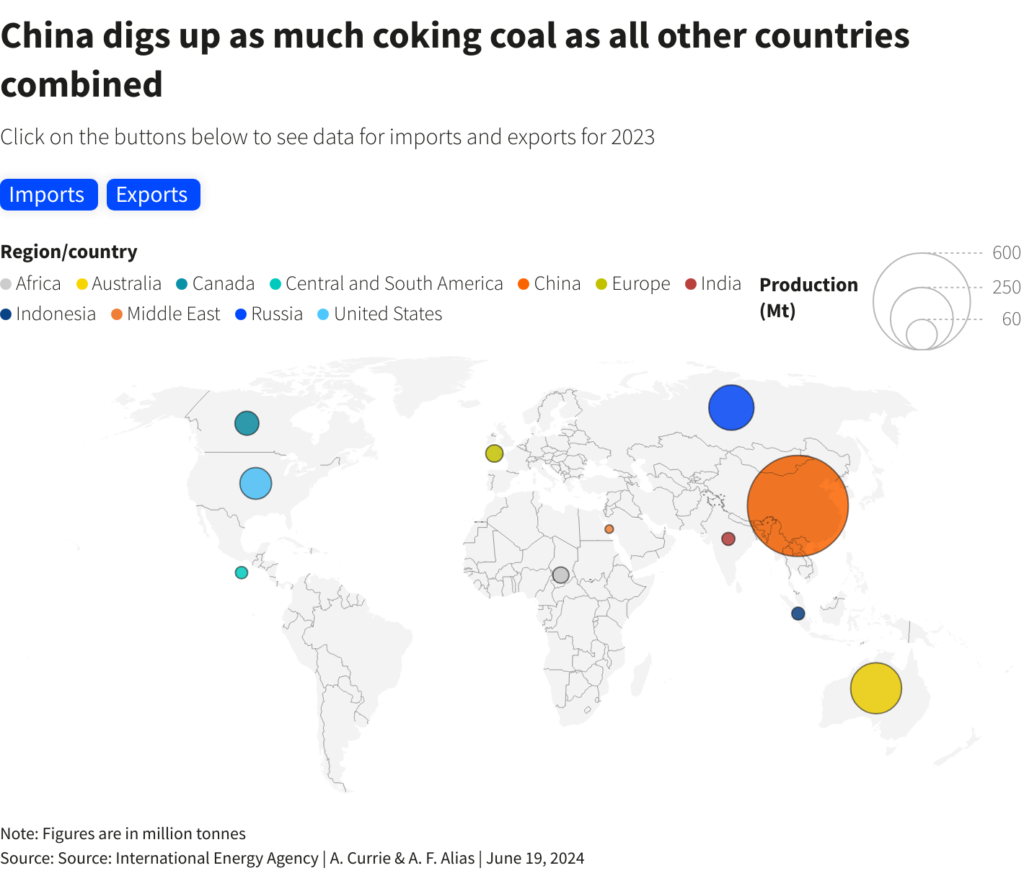

Glencore is in the process of acquiring 77% of Teck Resources’ coal business in a deal that values the enterprise at $9 billion, or more than 4 times next year’s estimated EBITDA, according to LSEG data. In Australia, which accounts for roughly half of all coking coal exports, there is more activity. A BHP-Mitsubishi Corp joint venture, for example, just sold two mines for about 3 times EBITDA, or $3.2 billion, to Whitehaven Coal, which may flog a minority stake to a steelmaker.

Coking coal has what for now is a unique pitch. It provides the heat and carbon necessary for blast furnaces to turn iron ore into molten iron, used to produce about 70% of the world’s 1.8 billion tons of steel each year. The rest comes from scrap metal refashioned in electric-arc furnaces, like ones at the heart of Nippon Steel’s fraught plan to buy United States Steel. This lower-energy process, whose furnaces use less if any coal, is projected to become as much as half the market by 2050. The dirtier method is set to keep growing in India and other parts of Southeast Asia, where production could jump 50% over the same span, according to Wood Mackenzie analysts.

The open secret, however, is that coking coal is more toxic than what gets shovelled into power plants. Thermal coal accounts for about a fifth of the world’s greenhouse gas emissions, double what steelmaking spews. But coking coal, which is responsible for most of the metal’s pollution, does so with just a fifth of the tonnage mined. Its significant methane content means toxins emitted from pits alone are almost three times higher than from thermal coal, Wood Mackenzie has estimated.

There are also no functional alternatives in the same way that solar, wind and other renewable sources are supplanting fossil-fuel power stations. Plenty are in the works, however. Green hydrogen is one, heavily funded by Andrew Forrest’s iron ore miner Fortescue and others. Rival Rio Tinto is also working on using biomass and microwave energy. Boston Metal – backed, among others, by BHP, steelmaker ArcelorMittal and German carmaker BMW – aims to commercialize the molten oxide electrolysis process.

These options may not be ready to compete at a significant level for a decade. This helps explain the reduced stigma attached to unearthing coking coal compared to its electricity-generating thermal cousin.

It’s also why the recent increase in deals does not seem to be particularly contentious. Even BHP boss Mike Henry touted coal mines as one of Anglo American’s main attractions after having spent four years as CEO pivoting to “future facing commodities” such as copper. The basic idea is that Anglo’s mines mostly hold the same premium-grade hard coking coal as BHP’s remaining pits just down the road. The variety has fewer impurities and usually lower emissions.

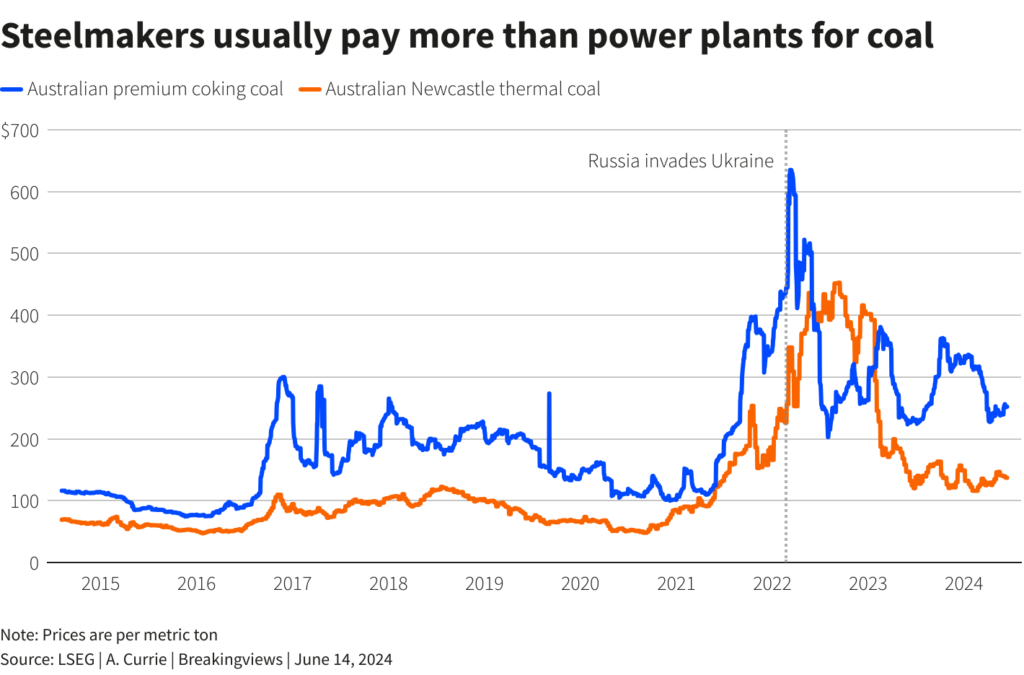

Profitability helps, too. Premium hard coking coal sells for around $250 a metric ton, with BHP spending roughly $100 and Anglo $115 to dig it up. Soft coking coal sells for around a third less. Thermal coal, meanwhile, fetches less than $140 a ton, with costs ranging from $50 to more than $100.

Small wonder that thermal coal producers were the buyers in the two largest coking coal deals. Of the 113 million tons of coal Glencore excavated last year, less than a tenth was destined for blast furnaces. Teck’s met coal unit will double that proportion and contribute a third of revenue, based on last year’s figures. The idea is that combined, the business will be worth more in a spinoff planned by Glencore CEO Gary Nagle.

With BHP-Mitsubishi’s volume, Whitehaven will more than double its overall production and catapult the top-line contribution from met coal to about 70% from less than 10%. The merger also should boost its EBITDA margin and eventually inspire investors to value the enterprise at more than just 3 times those expected earnings over the next 12 months, per LSEG data. The deal also takes the company tantalizingly close to the threshold – 25% of revenue from thermal coal – that can make it easier to tap mainstream banks and insurers.

Some of the deals look like steals, at least on paper. Glencore’s return on its mooted Teck investment could be as high as 19%, based on last year’s showing. And if BHP were to pay, say, $5 billion to buy Anglo’s coal mines, or around 4 times 2025 EBITDA per Visible Alpha data, and then cut its target’s costs by a tenth, it might generate 14% on its capital, Breakingviews calculates.

All else being equal, Glencore might recoup its outlay in just five years, far sooner than even the chirpiest projections for green hydrogen and other technology to compete. A putative BHP acquisition of Anglo’s metallurgical assets would take seven years to pay off.

If coal prices drop by a third to their pre-Ukraine war band, though, a crude calculation indicates the deal payback timeline would roughly double. That’s assuming costs don’t rise. Many mines in Australia’s chief coking coal region already have been hurt directly or indirectly from flooding worsened by climate change. Such events will increase as more fossil fuel emissions are pumped into the atmosphere.

The more such disasters, the greater impetus there may be to curb pollution, putting a bigger target on steelmaking. BHP and others anticipating that premium coal will be more durable sound optimistic: Teck has pointed out that increasing hard coking coal’s volume in the furnace to 70% from 50% reduces carbon emissions by less than 7%.

Moreover, climate-linked import duties, including Europe’s carbon border adjustment mechanism, will be fully up and running before long. Dealmaking is stoking the embers of coking coal, but also the chase against cleaner replacements.

(By Antony Currie; Editing by Jeffrey Goldfarb and Aditya Srivastav)

No comments:

Post a Comment