By Metal Miner - Feb 12, 2025

Steel mills are pushing for price increases following a weak fourth quarter, but whether this momentum continues is uncertain due to potential tariffs and demand fluctuations.

While manufacturing data suggests a recovery, the threat of tariffs could increase material costs and weigh on demand, further complicating the steel market's outlook.

The 2025 steel market is expected to be optimistic overall, driven by factors like onshoring and infrastructure investments, but it is unlikely to reach the peak prices seen in 2020 and 2021.

![]()

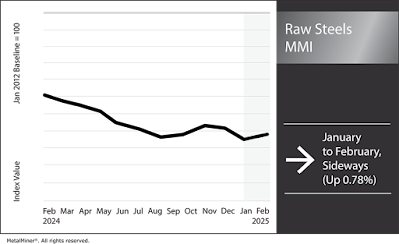

The Raw Steels Monthly Metals Index (MMI) remained sideways, with a modest 0.78% increase from January to February. However, steel prices could still be in for significant volatility.

Mills Push for Price Increases After Weak Q4

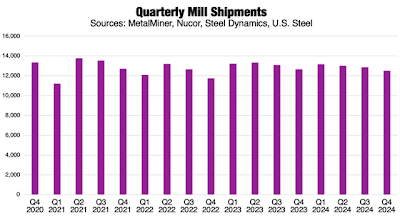

As Q4 financial results started to pour in, they reflected a challenging end to 2024. While data from Cliffs has yet to be published, total combined shipments from Nucor, SDI and U.S. Steel hit their lowest level in two years. U.S. Steel described the quarter as “a sequentially weaker average selling price and demand environment.” However, Nucor noted that “market conditions are starting to improve.”

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

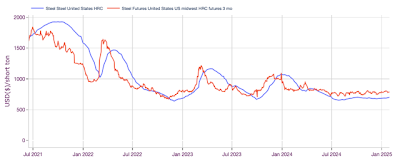

By the start of 2025, U.S. steel prices started to perk up. As of Feb. 7, hot rolled coil prices hit their highest level since June at $719/st. Friday’s price marks a 9.77% increase from their 2024 low in late July. A number of mills began issuing price hikes, as buyers reported mills were increasingly less willing to negotiate prices.

Will the Steel Price Uptrend Continue?

Whether mills will be able to maintain upside momentum remains in question. With the threat of 25% tariffs on imports from Mexico and Canada paused, market concerns over an impending supply disruption started to dissipate. Some believed the delay signaled a deal could be reached to avoid those tariffs altogether.

By Sunday, Feb. 9, however, concerns reappeared. Trump told reporters he plans to announce 25% tariffs on all steel and aluminum imports. While he did not indicate when those duties would be applied, he stated they would be applied to all importing countries.

Aside from new trade barriers, demand conditions will remain a driving force behind steel prices. On that side of the coin, the ISM Manufacturing PMI returned to growth for the first time since April 2024 in January, hitting its highest level since August 2022.

While such support could signal the nascent signs of recovery following a protracted recession in the U.S. manufacturing sector, it is unclear whether market conditions can maintain this trend. Tariffs would substantially increase material costs, which could weigh on demand.

Production Levels Remain Suppressed

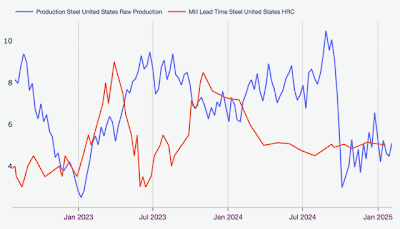

Meanwhile, steel producers continue to suppress production levels, holding output well beneath trend levels from the first half of 2024. According to U.S. raw steel production data from the American Iron and Steel Institute, falling prices forced mills to keep a significant amount of capacity offline following planned maintenance outages throughout Q3 2024. Despite capacity discipline, mill lead times have yet to reflect a meaningful shift in the market balance.

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

As of early February, HRC lead times remained sideways. Longer lead times would suggest tightening supply conditions, which typically triggers a steel price uptrend. One mill source noted that while demand appeared steady, buyers were waiting to see consistently longer mill lead times before placing large orders.

Buyer caution could derail the upward price momentum witnessed in recent weeks. However, tariffs risk spooking manufacturers into committing to larger purchases, which in turn, would cause lead times to lengthen.

2025 Steel Price Outlook

As mills await a demand rebound, the coming months appear somewhat uncertain. HRC three-month futures continue to trend sideways. This indicates that markets do not yet expect an impending steel price uptrend, as HRC futures historically serve as a leading indicator for HRC price trend shifts. However, announcements from Trump could significantly shift market conditions, which would have knock-on impacts on steel prices.

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

Meanwhile, Nucor’s Q1 outlook appeared cautious. The mill told investors, “We expect earnings in the steel mills and steel products segments to be similar in the first quarter of 2025 as compared to the fourth quarter of 2024.” Considering the challenging market conditions that plagued mill earnings during the final quarter of last year, Nucor’s statements do not suggest particularly bullish expectations.

The Next Bull Market May Not Hit Peaks Seen in 2021

Although it might get off to a slow start, 2025 appears optimistic overall. According to SDI CEO Mark Millet, “We believe the market dynamics are in place to support increased demand across our operating platforms in 2025. Steel pricing has stabilized, and customer optimism continues to be solid across our steel operations, as demand continues to be steady.”

Strong demand fundamentals served to underpin the positive forecast. As Millet stated, “The continued onshoring of manufacturing businesses, combined with the expectation of significant fixed asset investment to be derived from public funding related to the U.S. Infrastructure, Inflation Reduction Act, and Department of Energy programs, will competitively position the domestic steel industry.”

While rising demand will support prices, shortages and extreme tightness are not expected to materialize, which will cap future gains. Currently, constrained steel output means mills have significant capacity to spare when market conditions meaningfully rebound.

While producers will likely aim to maintain control over the supply-demand balance to maintain an uptrend, the next bull market will likely fall far short of what was seen throughout 2020 and 2021, which saw HRC prices reach an all-time high of $1,929/st.

By Nichole Bastin

Steel mills are pushing for price increases following a weak fourth quarter, but whether this momentum continues is uncertain due to potential tariffs and demand fluctuations.

While manufacturing data suggests a recovery, the threat of tariffs could increase material costs and weigh on demand, further complicating the steel market's outlook.

The 2025 steel market is expected to be optimistic overall, driven by factors like onshoring and infrastructure investments, but it is unlikely to reach the peak prices seen in 2020 and 2021.

The Raw Steels Monthly Metals Index (MMI) remained sideways, with a modest 0.78% increase from January to February. However, steel prices could still be in for significant volatility.

Mills Push for Price Increases After Weak Q4

As Q4 financial results started to pour in, they reflected a challenging end to 2024. While data from Cliffs has yet to be published, total combined shipments from Nucor, SDI and U.S. Steel hit their lowest level in two years. U.S. Steel described the quarter as “a sequentially weaker average selling price and demand environment.” However, Nucor noted that “market conditions are starting to improve.”

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

By the start of 2025, U.S. steel prices started to perk up. As of Feb. 7, hot rolled coil prices hit their highest level since June at $719/st. Friday’s price marks a 9.77% increase from their 2024 low in late July. A number of mills began issuing price hikes, as buyers reported mills were increasingly less willing to negotiate prices.

Will the Steel Price Uptrend Continue?

Whether mills will be able to maintain upside momentum remains in question. With the threat of 25% tariffs on imports from Mexico and Canada paused, market concerns over an impending supply disruption started to dissipate. Some believed the delay signaled a deal could be reached to avoid those tariffs altogether.

By Sunday, Feb. 9, however, concerns reappeared. Trump told reporters he plans to announce 25% tariffs on all steel and aluminum imports. While he did not indicate when those duties would be applied, he stated they would be applied to all importing countries.

Aside from new trade barriers, demand conditions will remain a driving force behind steel prices. On that side of the coin, the ISM Manufacturing PMI returned to growth for the first time since April 2024 in January, hitting its highest level since August 2022.

While such support could signal the nascent signs of recovery following a protracted recession in the U.S. manufacturing sector, it is unclear whether market conditions can maintain this trend. Tariffs would substantially increase material costs, which could weigh on demand.

Production Levels Remain Suppressed

Meanwhile, steel producers continue to suppress production levels, holding output well beneath trend levels from the first half of 2024. According to U.S. raw steel production data from the American Iron and Steel Institute, falling prices forced mills to keep a significant amount of capacity offline following planned maintenance outages throughout Q3 2024. Despite capacity discipline, mill lead times have yet to reflect a meaningful shift in the market balance.

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

As of early February, HRC lead times remained sideways. Longer lead times would suggest tightening supply conditions, which typically triggers a steel price uptrend. One mill source noted that while demand appeared steady, buyers were waiting to see consistently longer mill lead times before placing large orders.

Buyer caution could derail the upward price momentum witnessed in recent weeks. However, tariffs risk spooking manufacturers into committing to larger purchases, which in turn, would cause lead times to lengthen.

2025 Steel Price Outlook

As mills await a demand rebound, the coming months appear somewhat uncertain. HRC three-month futures continue to trend sideways. This indicates that markets do not yet expect an impending steel price uptrend, as HRC futures historically serve as a leading indicator for HRC price trend shifts. However, announcements from Trump could significantly shift market conditions, which would have knock-on impacts on steel prices.

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

Meanwhile, Nucor’s Q1 outlook appeared cautious. The mill told investors, “We expect earnings in the steel mills and steel products segments to be similar in the first quarter of 2025 as compared to the fourth quarter of 2024.” Considering the challenging market conditions that plagued mill earnings during the final quarter of last year, Nucor’s statements do not suggest particularly bullish expectations.

The Next Bull Market May Not Hit Peaks Seen in 2021

Although it might get off to a slow start, 2025 appears optimistic overall. According to SDI CEO Mark Millet, “We believe the market dynamics are in place to support increased demand across our operating platforms in 2025. Steel pricing has stabilized, and customer optimism continues to be solid across our steel operations, as demand continues to be steady.”

Strong demand fundamentals served to underpin the positive forecast. As Millet stated, “The continued onshoring of manufacturing businesses, combined with the expectation of significant fixed asset investment to be derived from public funding related to the U.S. Infrastructure, Inflation Reduction Act, and Department of Energy programs, will competitively position the domestic steel industry.”

While rising demand will support prices, shortages and extreme tightness are not expected to materialize, which will cap future gains. Currently, constrained steel output means mills have significant capacity to spare when market conditions meaningfully rebound.

While producers will likely aim to maintain control over the supply-demand balance to maintain an uptrend, the next bull market will likely fall far short of what was seen throughout 2020 and 2021, which saw HRC prices reach an all-time high of $1,929/st.

By Nichole Bastin

No comments:

Post a Comment