It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters)

US President Donald Trump’s tariff blitz has shocked financial markets, but the LME base metals complex got an early preview of the likely mayhem.

The imposition of 25% tariffs on U.S. imports of aluminum has dislocated the light metal’s global supply chain, while the threat of similar levies on copper has generated an unprecedented disconnect in transatlantic pricing.

Micro tariff turbulence is now overlaid with macro tariff turmoil as markets take fright at the risk of a full-blown trade war. The London Metal Exchange’s index of base metals has slumped 6% this week as reciprocal tariffs moved from threat to reality.

Only one metal has escaped the tariff tsunami. Tin continues to out-perform the rest of the LME pack buoyed by its own supply chain chaos.

Supply shocks rock tin

LME three-month tin gained 25% over the first quarter of 2025, eclipsing even gold’s stellar run.

A series of supply shocks has generated a roller-coaster ride for tin traders.

The market sold off on news the giant Man Maw tin mine in Myanmar would restart after an 18-month absence before rebounding when Alphamin Resources announced it was closing its Bisie mine in the Congo due to the escalating insurgency in the east of the country.

The devastating earthquake in Myanmar, throwing fresh doubt on Man Maw’s return, has propelled tin even higher.

Investors have rushed to join the action. Fund long positioning has hit record levels.

LME stocks are sliding and time-spreads tightening, adding to the volatility mix.

Bulls, however, should note that there is no shortage of tin in China. Shanghai Futures Exchange stocks have risen by 47% so far this year and at 9,872 metric tons are the highest since September.

Minding the copper gap

Copper trading has been defined by the threat of U.S. tariffs since February, when Trump ordered a national security investigation into copper imports.

The trade has played out in the arbitrage between the CME US customs-cleared price and the LME global price. It has been a volatile trade as the market tries to second-guess when copper tariffs will come and at what rate.

The record CME premium over LME copper has triggered a mass movement of physical metal to the United States. How much makes it through U.S. customs before tariffs are announced remains to be seen.

Record high CME prices and physical market dislocation initially rekindled bull spirits but LME copper has just slumped below the $9,000-per ton level as concern grows over the negative implications of U.S. reciprocal tariffs for global manufacturing activity.

Aluminum premium action

The CME aluminium contract mirrors the LME’s international product, meaning the tariff trade has played out in regional premiums.

The U.S. Midwest premium widened to more than $900 per ton over the LME basis price last month as the market priced in the lift in U.S. import tariffs from 10% to 25%.

European premiums, by contrast, have fallen sharply, suggesting physical metal is already being diverted from the U.S. market.

Analysts had high expectations for aluminium at the start of the year but the market has generated mixed signals and, like copper, is selling off in reciprocal tariff reaction

Nickel awaits Indonesia

Nickel has spent the first three months of 2025 trapped in a broad $15,000-17,000-per ton range.

The price has been weighed down by ever-rising LME stocks as over-production in Indonesia swamps the refined nickel supply chain.

The amount of Chinese nickel in the LME warehouse network has grown to more than 50% from 11% at the start of 2024. This is metal that has been processed in China from Indonesian raw materials. Indonesia has started producing its own refined metal, which is also turning up in LME sheds.

The nickel price is so low that even Indonesian operators are feeling the margin pinch, but until the country limits its production growth, nickel will remain over-supplied.

The only question is whether the Indonesian flood continues to wash into the refined metal segment of the nickel market or revert to the lower-grade Class II segment.

It all depends on Indonesian processing margins.

Heavy stocks weigh on heavy metal

And talking of high stocks.

Someone cancelled 120,000 tons of LME lead stocks last month but there was little or no reaction from either outright price or time-spreads.

No-one thinks the physical market is short by that much metal. Rather, lead is seeing the sort of LME warehouse arbitrage that comes with over-supply and elevated exchange stocks, which have grown to 331,000 tons from 21,500 tons at the start of 2023.

The lead price has held up well given the inventory overhang but that may be because it is still in better shape than sister metal zinc.

Zinc mine rebound

Zinc has consistently underperformed the rest of the LME pack since the start of the year, even though exchange stocks have fallen steadily.

But the market appears to be trading zinc’s bearish raw materials narrative rather than its more nuanced refined metal dynamics.

Mined zinc production fell by 2.8% year-on-year in 2024, tightening the raw materials supply chain to the point that smelter fees turned negative in the second half of the year.

Restarts and new mines are expected to generate a significant rebound in 2025.

There are signs that this new wave of mine supply is starting to build momentum. Smelter treatment charges, which turned negative due to a shortage of mined concentrates in 2024, have bounced back to $35 per ton on a spot basis.

Zinc demand flat-lined last year and with little prospect of a recovery in global construction, a major end-use sector for zinc, higher mined output is expected to generate over-supply in the refined metal market.

(Editing by Barbara Lewis)

Myanmar’s tin-rich Wa State delays mining resumption meeting after earthquake

Myanmar’s tin-rich Wa State has postponed a meeting to discuss the resumption of mining in the region, a regional spokesman confirmed on Thursday.

The meeting, originally called for Tuesday, was postponed and no alternative date was set, according to a notice dated Monday and confirmed by a Wa State spokesman on Thursday.

The meeting had raised hopes among traders that an almost two-year ban on mining in the region could soon be lifted. Wa State produces 70% of Myanmar’s tin exports. Myanmar is the world’s third-largest producer and China’s biggest supplier.

A tin trader who works for a company that operates in Myanmar, speaking on condition of anonymity, said it was difficult to predict when operations could resume as the extent to which infrastructure and power plants were damaged was unclear.

China’s imports of tin ore from Myanmar more than halved last year, customs data showed.

Increased supply worries as a result of last Friday’s earthquake pushed tin prices on the Shanghai Futures Exchange to 299,220 yuan ($40,999.15) per metric ton on April 2, the highest since May 22, 2022.

Tin prices on the London Metal Exchange (LME) also hit their highest since May 2022, reaching $38,395 a ton.

Investors’ increased interest in near-term LME futures has driven the premium of cash LME over the three-month futures to $264 a ton, signalling supply tightness, and in a stark contrast to the discount of $79 just two weeks ago.

Unlike the majority of Myanmar, which is under the control of the military junta, Wa State maintains its own political system, military, and economy, effectively making it a state within a state.

Wa banned mining in August 2023 to protect its natural resources.

($1 = 7.2982 Chinese yuan renminbi)

(By Violet Li, Lewis Jackson and Shoon Naing; Editing by Barbara Lewis)

Kazakhstan says it has discovered 20-million-tonne rare earth metals deposit

Southeast Kazakhstan. Adobe stock image by Max Zolotukhin.

Kazakh geologists have discovered a rare earth metal deposit with estimated resources of more than 20 million metric tons at a depth of up to 300 metres, the country’s industry and construction ministry said in a statement on Wednesday.

Kazakhstan does not currently feature in the US Geological Survey’s list of countries by rare earth metal deposits. If confirmed, the deposit would place Kazakhstan behind only China and Brazil by size of reserves.

In a statement on Telegram, the ministry said that the Zhana Kazakhstan site, which is 420 km (261 miles) from the country’s capital, contained neodymium, cerium, lanthanum and yttrium, and that its average rare earth metal content is 700 grams per ton.

It did not specify which companies may develop the site, or when.

(By Mariya Gordeyeva and Felix Light; Editing by Louise Heavens)

US tariff blitz bolsters Goldman’s bearish view on iron ore

A cascade of US tariffs announced by President Donald Trump will hurt Chinese steel exports and help to drag iron ore prices below $90 a ton by the end of the year, Goldman Sachs Group said in a note.

Washington’s “reciprocal” levies will hit shipments to top destinations including Vietnam, which has been battered by higher-than-expected duties and will see its own overseas sales crimped as global growth cools, analysts including Aurelia Waltham wrote.

Iron ore has traded in a narrow range from around $100 to $105 a ton over the past month, as the market weighs high Chinese mill utilization rates, impending crude steel production cuts and a likely drop in exports.

Writing after a visit to six private steel mills in China, the analysts said prices would have near-term support, but added the market was likely to go into surplus in the second half and could touch $84 a ton. Goldman expects steel exports will fall by around 15% in 2025, with the surveyed mills expecting domestic demand to decline by as much as 5%.

China’s state-owned iron ore buyer, China Mineral Resources Group, also appears to be helping to reduce volatility in the market. It “appears to be holding a rather sizable inventory at ports — 10-20 million tons — and is selling stock in the onshore market when the market is tight,” the analysts wrote.

Iron ore futures in Singapore were 0.7% lower at $101.15 dollars a ton at 10:52 a.m. local time, declining over 1% from last week. Chinese markets were closed today for a public holiday.

(By Katharine Gemmell)

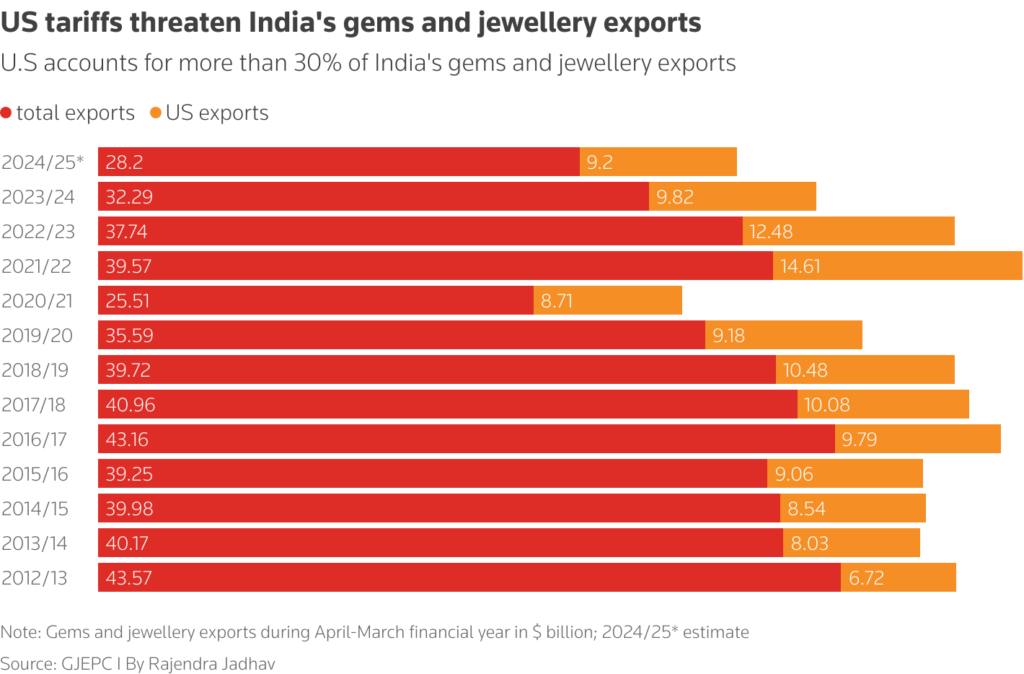

US tariffs set to cripple India’s diamond industry, hurting jobs, exports

A wave of anxiety has gripped India’s diamond polishing hub of Surat, as hefty US tariffs threaten to undermine the country’s gem and jewellery exports, putting at risk the livelihoods of thousands of workers.

The United States, which takes more than 30% of the South Asian nation’s gem and jewellery exports, set a 27% reciprocal tariff on it on Thursday, at a time when demand is softening in other key markets such as China, the Middle East, and Europe.

“Tariffs will hit hard the demand for diamonds in the United States and job losses look inevitable, at least in the short term,” said Dinesh Navadiya, chairman of the Surat-based Indian Diamond Institute.

Surat, the second-largest city in Gujarat, the western home state of Prime Minister Narendra Modi, processes and polishes more than 80% of the world’s rough diamonds, and India accounts for nine in every 10 diamonds processed globally.

Business has ground to a halt in its teeming diamond market, where more than 10,000 traders and brokers gather each day, as the industry tries to figure out how matters will evolve in the coming months.

Conditions are worse than during the 2008 financial crisis, when the industry was plagued by fears of a prolonged recession, said Mansukh Mangukiya, a diamond trader for five decades.

A slowdown in the industry will hit all manufacturers, but smaller players will suffer most, said Sevanti Shah, chairman of Venus Jewels, adding, “Many smaller manufacturers will have no choice but to shut down.”

The United States accounted for nearly $10 billion, or 30.4%, of India’s annual gems and jewellery exports, totalling $32 billion in the fiscal year 2023/24.

Third largest export to US

Gems and jewellery are India’s third largest export to the United States, after engineering and electronic goods, and employ millions of workers, including artisans.

Poorer business prospects also raise questions about the future of the Surat Diamond Bourse, inaugurated by Modi in 2023 to create thousands of new jobs and serve as a trade hub.

Built over 6.6 million square feet, it was touted as the world’s largest office building, surpassing the Pentagon.

The industry will seek alternative markets to compensate for the loss of US demand, but no other country will be able to replace the US market, diamond dealers said.

The sudden decline in US demand would require short-term production adjustments within the industry and could lead to reduced rough diamond imports, said Shaunak Parikh, vice chairman of the Gem and Jewellery Export Promotion Council.

Exporters are making last-minute efforts to ship as much as possible to the United States before its new tariffs take effect, Parikh said, while orders that cannot be delivered earlier may be cancelled or put on hold.

The tariffs would also drive up US prices, crimping demand, said Vipul Shah, managing director of Asian Star, a leading diamond exporter.

An uncertain future lies ahead for Chetan Navadiya, a diamond manufacturer turned job-work contractor.

“I lost my business due to the market slowdown,” Navadiya said. “I took up job work to survive, but even those contracts may not come by now, because of US tariffs.”

(By Rajendra Jadhav and Sumit Khanna; Editing by Mayank Bhardwaj and Clarence Fernandez)

WAIT, WHAT?!

Mining’s king of private capital says governments must intervene

Orion Mine Finance founder Oskar Lewnowski. (Image: LinkedIn)

Oskar Lewnowski has a good claim to be the poster boy for private capital in mining.

A former investment banker who quit the legendary London-based commodity hedge fund Red Kite to start out on his own a decade ago, Lewnowski’s company Orion Resource Partners is now the biggest specialist investor in metals and mining, focused on private equity and private credit.

And yet he’s calling for governments to intervene. A lack of adequate investment in mines means the world is barreling toward a crisis in metals supply comparable to the oil shocks of the 1970s, Lewnowski says. Part of the answer, he argues, would be for states to step in and build strategic mineral stockpiles.

“It’s an extremely big problem,” he said in an interview. “The government needs to certainly be more involved.”

Lewnowski’s comments encapsulate a core paradox facing the mining industry: the sector has suddenly become a top strategic priority, as Europe and the US worry about their future supplies of minerals critical to everything from power and communications infrastructure to defense. And yet the reality of constructing and financing new mines is as tough as it’s ever been, with prices for key metals including nickel and lithium under pressure amid a wave of new supply from Chinese-backed projects.

Lewnowski is not the only counterintuitive source of calls for government intervention in metals. Last week, the chief executive of Trafigura Group said at a conference in Switzerland that western governments should take ownership of struggling smelting assets, including those belonging to his company, to ensure national security.

The comments were jarring coming from one of the biggest players in commodity trading — another sector that’s normally a flag-carrier for free-market capitalism.

“When the oil embargoes started happening and prices started to spike in the fossil fuels, the US created a strategic petroleum reserve,” Lewnowski said. “Something like that will need to happen.”

‘Brutal’ lesson

To understand why Lewnowski is calling on governments to get involved, it’s instructive to look at Orion’s most recent flop.

In 2021, the fund joined forces with Glencore Plc and Egyptian billionaire Naguib Sawiris to back UK-listed Horizonte Minerals Plc to develop a nickel project in Brazil.

The timing seemed good: nickel’s demand was growing rapidly thanks to its use in batteries for electric vehicles, and auto industry executives were worrying about future shortages. Four years later, though, Horizonte has fallen into administration after spending hundreds of millions of dollars on a project that may never be completed. Orion faces significant losses on its investment of about $150 million.

It is an object lesson in how a demand boom doesn’t necessarily make for a good investment: Horizonte lost the faith of its investors when it revealed its construction costs would be nearly double what it had forecast. But the killer blow for the project was the nickel market, where Chinese investment in Indonesia has unleashed a tidal wave of supply.

“It has been brutal,” Lewnowski said. Chinese producers “have driven up supply to a point where prices have collapsed. And it has put a lot of pressure on competitors.”

It’s a trend that governments around the world are gradually waking up to. As Donald Trump rails on the global stage for access to mineral deposits from Ukraine to Greenland, the reality is that China is increasingly dominant. The country processes a vast percentage of everything from copper to gallium, while Chinese mining companies also account for a growing share of total mining investment.

Meanwhile, European banks that traditionally financed mining projects have gradually retreated from the sector and public equity investors have soured on miners — putting an increasing focus on private capital and prompting governments seeking to counter Chinese dominance to put in a call to Lewnowski.

“They’re asking us essentially questions like how big a problem is this?” he said. “How can we catch up to the Chinese on something that they’ve done for 10 years now?”

For Orion, that’s good business. The firm counts sovereign wealth funds among its investors, and just unveiled a $1.2 billion partnership with Abu Dhabi’s ADQ. With its base in New York, it is well positioned to be part of groups seeking to counter Chinese dominance in mineral-rich regions of the world.

Gallows humor

Lewnowski founded Orion in 2013 after leaving Red Kite and his partnership with two of the most famous names in metals trading: Michael Farmer and David Lilley. Originally created to focus on mine financing, Orion now has about $8 billion in assets under management and a business that spans private equity, venture capital and commodity trading.

Investing in mining requires a certain kind of personality, combining boosterish optimism with gallows humor born of regular disappointment – and the 59-year-old son of a fund manager embodies the archetype. At one moment, Lewnowski is predicting never-before-seen copper prices of over $13,000 a ton; the next he is reflecting on his career by echoing Mike Tyson: “You always have a plan until you get punched in the mouth.”

Lewnowski won’t comment on the performance of his funds, but says Orion’s investors have enjoyed solid returns, with less volatility than they’d face in the public markets. A recent investor presentation cited average internal returns since inception of 16.1% before fees for its mine finance funds, according to a person familiar with the document. Recent quarterly reports from investors in some of its more mature funds show they’ve received internal rates of return of about 8% to 9% after fees.

Red Kite was one of the main winners of the commodity supercycle in the early 2000s, notching up eye-watering returns of as much as 188% in a year, as Farmer and Lilley’s contacts in China helped them see that a massive bull market in copper was coming. But while Farmer and Lilley were focused on metals trading and willing to stomach hugely volatile returns, Lewnowski wanted to focus “on the mine-building side of things,” he says.

When they parted ways in 2013, Lewnowski took Red Kite’s most recent mine finance fund and used it to form the basis of his new business.

Orion aimed to focus on the actual building of mines, capturing a 2.5 times uplift in valuation as a project goes from construction through to production, according to a company presentation.

Over time it has added other funds. A hedge fund that aims to trade metals markets as Red Kite did, but without the stomach-churning volatility, rose to become one of the largest commodities funds before suffering investor redemptions and a down year in 2023. As of early 2025, its assets were just $580 million, down from $1.6 billion at the peak, according to an industry report. Lewnowski declined to comment on the figures, but said it suffered from taking too much capital too quickly from the wrong investors, and that it is now growing again.

‘They don’t panic’

While Horizonte was a punch in the mouth, other deals have been more successful. In 2015, Orion struck a deal to buy two Chilean copper mines from Anglo American Plc for $300 million in partnership with John MacKenzie, Anglo’s former head of copper. They converted the ageing assets, which had been exploiting oxide deposits, to mine for sulphides – effectively, building a whole new mine – and slashed costs.

A decade on, with copper prices nearly double where they were when the deal was agreed, Orion has made several times its original investment. It sold a silver stream on the mines as part of a broader $835 million deal with Osisko Gold Royalties Ltd. in 2017, before taking the assets public through a merger with Capstone Mining in 2022. Starting in 2023, it has made nearly $700 million by selling down its shares in the combined entity, Capstone Copper Corp., and still has a stake worth about $470 million.

MacKenzie said that big, generalist private equity funds “haven’t been able to get their heads around” the cyclical and long-term nature of mining investments. That has left Orion and a clutch of other specialist, mining-focused funds that includes the likes of Appian Capital Advisory and Resource Capital Funds as key financiers of the industry.

Still, even for the specialists there are some hair-raising moments. MacKenzie recalls that two of the three funds he had lined up to back the Anglo deal dropped out at the last minute, leaving Orion on the hook for the whole thing. “Even when times are tough, they don’t panic,” he said of Lewnowski and his team.

National security

Apocalyptic predictions about future shortages of metals have become a common refrain in recent years, as bullish investors and mine builders argue that supply will struggle to keep pace with demand for all the batteries, solar panels and high-voltage cables needed for the transition from fossil fuels. Building a mine is harder than ever, as the best deposits have already been exploited, costs have spiralled higher, and permits are hard to get.

Still, the predictions have yet to be proven right, as economic malaise in China, slower-than-expected uptake of electric vehicles, and the waves of new production from Chinese-backed mines have kept shortages at bay.

The result is a paradoxical situation where prices for many metals are relatively low, yet governments outside of China are fretting about security of supply. That’s why Lewnowski is arguing in favor of government stockpiles.

It’s an idea with a long history. The US stockpiled metals critical to its defense industry for decades in the wake of the Second World War, but sold off the large majority of its holdings after the end of the Cold War. In energy, the creation of national stockpiles like the SPR in the aftermath of the oil crises of the 1970s has been credited with mitigating price spikes.

In recent years, the idea of stockpiling critical metals has been gaining traction in some corners. It’s “not going to happen overnight,” Lewnowski said. “But that’s something that the governments need to do.”

Of all countries, however, it’s China that is the most active government stockpiler of metals, regularly buying thousands of tons for its state reserves. That is perhaps ironic, because metals processing is the area where China is most dominant, accounting for more than half of global copper, zinc and aluminum processing and an even higher share of more niche metals like cobalt, lithium and rare earths. Richard Holtum, Trafigura’s CEO, said last week that the west risked outsourcing its smelting industry to China.

“Smelting capacity is a national security issue, and therefore needs to probably have some sort of government ownership or significant government support for it because it is not competitive on an international basis comparing it to the Chinese,” Holtum said, announcing a strategic review of Trafigura’s loss-making Australian lead and zinc smelters.

Lewnowski acknowledges that the mining sector as a whole has disappointed investors.

But he points to forecasts from the International Energy Agency that the world needs to spend more than $300 billion building copper mines by 2040 to ensure enough supply of the metal for all the electrical cables and wiring needed for the transition away from fossil fuels.

It’s not clear where that money will come from, and copper prices will need to rise to $13,000 to $14,000 a ton from the current level of roughly $9,700, to incentivize sufficient investment, Lewnowski says. He also sees future “challenges” for tin, uranium, lithium and cobalt.

“You need that price to incentivize certain kinds of new production” Lewnowski said. “But until you have that price, you can’t invest on the basis of a hypothetical.”

(By Jack Farchy)

China hits back at US tariffs with rare earth export controls

China placed export restrictions on key rare earth elements on Friday as part of its sweeping response to President Donald Trump’s tariffs, potentially squeezing supply to the U.S. and the West of minerals vital to everything from defense to electric cars.

China produces around 90% of the world’s refined rare earths, a group of 17 elements used across the defense, electric vehicle, clean energy and electronics industries. The United States imports most of its rare earths, and most come from China.

China has hit back hard, including not only mined minerals but finished products such as permanent magnets, which will be difficult to replace, analysts said.

“Full-blown export restrictions on high-performance rare earth magnets containing dysprosium and/or terbium will hit foreign industries and defense sectors hard, creating a scramble for access to the limited sources of alternative supply – namely in Japan and South Korea,” said Ryan Castilloux, founder of consultancy Adamas Intelligence.

“In the near-term, importers are holding their breath waiting to see if they will be impacted. The cannons have been loaded but so far no one knows where they’re aimed.”

Seven categories of medium and heavy rare earths, including samarium, gadolinium, terbium, dysprosium, lutetium, scandium and yttrium-related items, will be placed on an export control list as of April 4, according to a Ministry of Commerce release.

The move, which affects exports to all countries, not just the U.S., is the latest demonstration of China’s ability to weaponise its dominance over the mining and processing of the critical minerals.

Seven categories of medium and heavy rare earths, including samarium, gadolinium, terbium, dysprosium, lutetium, scandium and yttrium-related items, will be placed on an export control list as of April 4

Beijing has already imposed outright bans on the export of three metals to the U.S. and slapped export controls on many others.

The moves to restrict heavy rare earths are especially important because China has even tighter control over these elements, said David Merriman at consultancy Project Blue.

“There is currently only one HREE (heavy rare earth element) focused operation outside of China, Myanmar and Laos,” he said, adding that China has close involvement in supply chains from Myanmar and Laos.

That mine, Serra Verde in Brazil, is currently shipping its product to China for processing, Merriman added.

Galvanize West

Friday’s move is likely to galvanize efforts in the West to build alternative supply chains, according to Mercator Institute for China Studies analyst Jacob Gunter.

“The more China pulls this trigger, even if it’s limited to the United States, this will cause European companies and European governments and other countries and their governments to also think about, what’s the risk of us also having these export controls put on us?”

Beijing announced the controls late on Friday as part of a broader package of tariffs and company restrictions in retaliation for U.S. President Donald Trump’s decision to hike tariffs against most Chinese products to 54%.

Roughly three-quarters of the rare earths the U.S. imports came from China between 2019 and 2022, according to the U.S. Geological Survey.

While the export controls stop short of an outright ban, Beijing can throttle shipments by restricting the amount of export licenses it issues. China had exported no antimony to European Union countries as of March after imposing export controls on the metal last September.

China dominates the complex and dirty refining process for rare earths, which are common in the earth’s crust, and controls mining and output via a quota system that it has progressively tightened.

(Reporting by Amy Lv and Lewis Jackson in Beijing, Eric Onstad in London; Editing by Elaine Hardcastle, Jan Harvey, Philippa Fletcher)