It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Friday, August 22, 2025

Tianqi open to renegotiating lithium refinery deal with IGO

China’s Tianqi Lithium is open to renegotiating joint venture partner IGO’s stake in the troubled Kwinana lithium refinery in Western Australia state, CEO Frank Ha said on Wednesday.

The refinery, the first lithium hydroxide plant to be built in Australia, has been grappling with operational issues and production delays amid a lithium price slump.

IGO, which owns a 49% stake, wrote down the loss-making refinery and said it had low confidence the asset could be improved when it reported last month.

“I am open to any of their proposals that we can discuss, but until now we have not received any official proposals from them,” Ha said during a media briefing.

“If they do not want to be a partner, they have to come to me, I’m open,” he said.

IGO did not immediately respond to emailed questions from Reuters.

Both companies also share ownership of the Greenbushes lithium mine, one of the world’s best lithium assets.

Asked whether Tianqi would consider IGO exiting Kwinana but staying invested in Greenbushes, Ha said the two assets were a package.

Tianqi would also not consider other partners in the Kwinana refiner, said Ha.

“It’s like a marriage … It’s against my rules that I start to find a new partner.”

Efficiency at the Kwinana was improving, according to Ha, and the company had no plans to shut down the refinery, which had a clear pathway to its full nameplate capacity of 24,000 tons per year.

The company was aiming for 65% capacity in the next year, Ha added.

(By Lewis Jackson and Melanie Burton; Editing by Jacqueline Wong and Michael Perry)

Column: A last swing of the LME aluminum stocks roundabout?

The aluminum market has just seen another big stocks rotation with 156,000 metric tons of metal flowing into London Metal Exchange warehouses over the last six weeks.

But it’s starting to look like the endgame of the stocks battle that has characterized LME aluminum trading for over a year.

Financiers, traders and warehouses are tussling over a diminishing volume of metal. Just about all the aluminum just delivered onto LME warrant was drawn down from existing LME off-warrant stocks in the same Malaysian location.

The Port Klang stocks shuffle has had little impact on the bigger inventory picture. Total LME stocks, both registered and off-warrant, are still down by almost 300,000 metric tons from the start of the year at 717,000 tons.

The absence of significant fresh deliveries in the most recent inventory churn helps explain why LME time spreads have failed to loosen despite the run of apparent “arrivals” showing up in the exchange’s daily inventory reports.

It also offers a clue as to why LME-registered storage capacity at Port Klang has been steadily shrinking.

LME aluminum stock movements at Malaysia’s Port Klang

Port Klang roundabout

The aluminum stocks battle has been raging since May 2024, when 650,000 tons of metal were dumped into LME warehouses in Port Klang.

The seller, reportedly trade house Trafigura, could earn more money from a rent-sharing deal with an LME warehousing company, in this case ISTIM UK Ltd, than any physical sale in an oversupplied market.

The good news for the buyers was that this was Indian and not Russian metal, which had just been placed under US and UK sanctions. The bad news was that the only way of breaking the pre-negotiated storage deal was to cancel the metal and transfer it to another warehouse operator.

The subsequent rush to move aluminum generated a load-out queue reminiscent of those that plagued the LME in the 2010s.

The queue at ISTIM’s Port Klang warehouses stretched to 293 days at its peak in August 2024 and only disappeared in May this year.

The latest stocks churn, occasioned by a squeeze on short-position holders in April-May, has ended back in ISTIM warehouses.

But the volume is much reduced from last year and largely comprises Indian metal returning from off-warrant storage. Total stocks at Port Klang are up by just 41,000 tons since the end of May, despite the daily noise of the LME’s stock reports.

ISTIM doesn’t seem to be expecting much more any time soon. The company has reduced the number of exchange-listed warehouse units in the Malaysian port from 22 to 13 over the last year.

Although other operators have increased their presence, total LME storage capacity in Port Klang has shrunk by 15% since the start of 2025 and is half what it was in 2021, when ISTIM was storing over 800,000 tons of warranted aluminum.

LME aluminum stocks on and off warrant

All change, no change

LME time spreads have barely reacted to the daily warranting action. The benchmark cash-to-three-month period continues to trade either side of level, unchanged from where it was two months ago.

That’s because nothing much has changed in the bigger scheme of things. Total LME inventory, both registered and off-warrant, rose by a modest 36,500 tons over June and July, barely denting a downtrend that has been running since May last year.

Stocks continue to hover around three-year lows, and it’s evidently going to take a bigger cash premium to halt the steady erosion of what was once an inventory mountain.

The lack of fresh inflow may be down to the greater opportunities in a physical market that is adjusting both to a European phase-out of Russian imports and the hike in US import tariffs to 50%.

Regional premiums are diverging, and physical arbitrage offers more lucrative options than LME storage, particularly since warehouse operators such as ISTIM now lack the huge storage revenues that allow them to compete for fresh metal with physical buyers.

It’s also possible that there is simply not much freely available aluminum to fight over as China steps up imports. The country sucked in 1.25 million tons of primary metal, mostly Russian, in the first half of the year, with the pace of arrival accelerating further in July.

Whatever the reason, the LME warehouse roundabout is losing momentum and will continue doing so until operators can draw more metal out of the physical supply chain.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by Rod Nickel)

South Africa set to open first underground gold mine in 15 years

Members of the technical team entering the Qala Shallows underground area. (Image: West Wits)

South Africa is set to open its first new underground gold mine in 15 years – an increasingly rare event for a country that was once the world’s largest producer of the precious metal.

West Wits Mining Ltd. plans to start production next year at Qala Shallows on the western fringe of Johannesburg, a city founded during the gold rush that followed the discovery of the Witwatersrand reef in the 1880s. The Australia-listed company will mine ore during the three-year construction period to take advantage of sky-high bullion prices.

“We are really the only formal company trying to start a new mine” in South Africa’s gold industry, chief executive officer Rudi Deysel said in an interview.

The $90 million investment by West Wits will yield a mine with a modest annual output of 70,000 ounces, but it’s a bright spot for the nation’s dwindling gold sector. After topping the global rankings for decades, South African production has slumped by more than 70% over the past 20 years as its deep, high-cost mines struggle to compete with other producing countries.

“The demise of South Africa’s gold industry is usually told as a kind of morality tale about bad domestic politics, but the crucial development was the worldwide expansion stimulated by soaring gold prices in the 1970s and 1980s,” said Duncan Money, a mining historian who studies the sector. This provided the option to mine gold elsewhere “without the enormous and expensive technical challenges,” he said.

South Africa’s gold industry now employs just under 90,000 people, less than a fifth of the number that used to power the apartheid economy during the 1980s. That contraction has come as higher wages and electricity prices combined with the difficulty of running the world’s deepest mines. The economic and social impact on the nation is magnified as every gold miner supports between five and 10 dependents, while creating two jobs elsewhere.

Qala Shallows will have a maximum depth of 850 meters (2,788 feet), far less than some South African mines that extract gold from more than 3 kilometers (1.9 miles) beneath the surface.

Gold One Group Ltd.’s Modder East, which opened in 2009, and Burnstone, which operated briefly from 2010 and was subsequently bought by Sibanye Stillwater Ltd., were the last underground mines to enter production.

Other companies specialize in recovering gold from the numerous dumps of mining waste that litter the Witwatersrand Basin or want to restart abandoned underground operations.

Gold has enjoyed a record-breaking rally, with prices rising about 27% this year after a similar gain in 2024. That has revived international deal-making across the sector and spurred investment in new production.

“It was always good, but with these prices, where gold has gone, this project just became better and better,” said Deysel, whose company secured its mining rights from the South African government four years ago.

Contractors mobilized to the site in June as the project moved into the execution phase.

Qala Shallows – a previously untapped section of a concession that was closed in 2000 after operating for more than a century – is projected to generate $2.7 billion over its 17-year life, with costs of less than $1,300 an ounce, according to its feasibility study. Gold traded at about $3,340 an ounce as of 9:27 a.m. in London.

State-owned Industrial Development Corp. and commercial bank Absa Group Ltd. have agreed to lend West Wits about $50 million to construct the mine. It will send ore to a nearby processing facility owned by Sibanye.

“We don’t need to build a plant, we can utilize the capacity that’s available,” Deysel said. “So that’s a big tick.”

(By William Clowes and Antony Sguazzin)

Brazil Potash secures offtake agreement with Keytrade AG subsidiary

The South American nation ships in more than 85% of its fertilizer demand. (Stock Image)

Brazil Potash (NYSE: GRO) announced Thursday a commercial offtake agreement between its subsidiary Potássio do Brasil Ltda. and Keytrade AG, one of the world’s leading fertilizer trading companies.

The binding agreement establishes a 10-year take-or-pay commitment for Keytrade to purchase up to 900,000 tons of potash annually from Brazil Potash’s Autazes project, representing about 30% to 37% of the mine’s annual production.

After facing headwinds due to some opposition by Indigenous groups, the state of Amazonas granted Brazil Potash last year the license to build the Autazes project, pegged to be the largest fertilizer mine in Latin America within the Amazon rainforest.

“This agreement with Keytrade is a major milestone in Brazil Potash’s commercial development,” Brazil Potash CEO Matt Simpson said in a news release.

Combined with the existing take-or-pay agreement with Amaggi Exportacão E Importacão Ltda., the company now has binding commitments for 1.45 million tons of its planned 2.4 million tons of annual production.

“These long-term contracts provide the revenue certainty essential for securing project financing and advancing construction,” Simpson added.

“This collaboration with Brazil Potash is a strategic step toward reducing Brazil’s reliance on imports and fostering economic growth in the Amazon region,” Keytrade Fertilizantes Brasil CEO Anthony Jezzi added.

With the Keytrade agreement finalized, Brazil Potash said it has secured binding offtake agreements covering approximately 60% of planned production and is also in advanced discussions with a prospective partner that would increase total volumes to about 91% of its annual capacity.

SHADOW TRADE

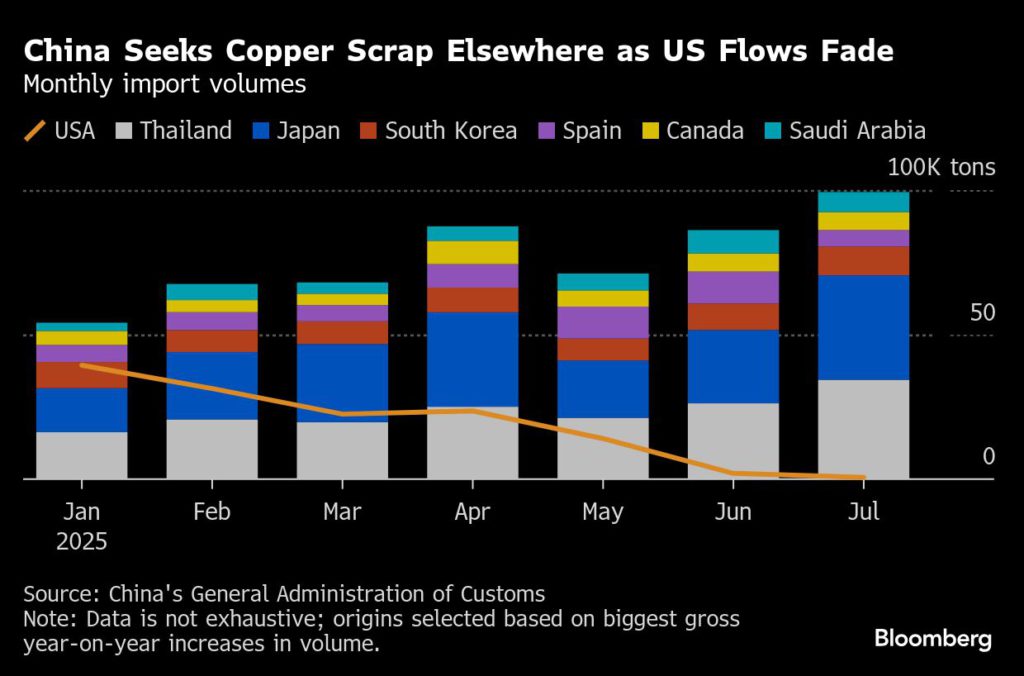

Scrap copper traders redirect metal to sidestep China levies

Some US metal dealers are redirecting China-bound shipments of scrap copper through countries including Canada, Mexico and Vietnam in a risky move to avoid 10% import tariffs, according to people familiar with the matter.

The rerouting underscores growing stress building up in the global metals supply chain due to the trade war between the US and China. US scrap is a vital source of raw material for China’s copper smelters and refiners, which account for about half of the world’s output of the finished metal. Prolonged disruption to that supply threatens to ripple across global markets.

While the full extent of the transshipments remains unclear, the rerouting shows how creative metals dealers are getting to avoid higher costs from trade barriers to find a home for America’s surplus scrap. The US is the world’s largest supplier of waste copper — metal recovered from auto parts, electric wires and electronics — but the domestic market consumes just 40% of that output, according to BMO Capital Markets.

“It’s not surprising that these companies come up with clever ways to move materials around,” said Xiaoyu Zhu, a trader at StoneX Financial Inc. “The 10% tariff has put the scrap companies at a disadvantage in terms of pricing, not to mention the financing pressure from high interest rates.”

China was typically the largest export destination for the US until Washington’s trade war with Beijing disrupted flows. Beijing has imposed 10% counter-tariffs on all American imports, including copper scrap, since May.

Officially, Chinese imports of copper scrap from the US have plunged this year, falling from 39,373 metric tons in January to below 600 tons in July, the lowest monthly total according to Chinese customs data going back to 2004. Shipments from other nations have largely filled the gap, since China’s overall imports of 190,000 tons last month was little changed from the start of the year. Shipments from Japan and Thailand have more than doubled since January, while imports from Canada climbed 29%.

US export data, meanwhile, shows that Thailand, India and Canada were the top three destinations for American scrap copper in the second quarter.

The sudden, large increases in Chinese imports from countries other than the US suggests at least some rerouting, according to the people familiar with the workaround, who asked not to be identified because they weren’t authorized to publicly discuss the practice.

To dodge Chinese tariffs, US scrap copper is put in containers, tagged with the owner’s name, and shipped out to a third country, the people said. When the cargo reaches its stopover, the owner tag is switched with another carrying a different name and country of origin, and the container then continues its journey to China, they said.

Risky business

Reloading shipments en route and changing the origin is fraud, as is importing into a country and declaring it the origin before sending on to the final destination, according to Emmanouil Xidias, managing director at ship-broking firm Ifchor North America LLC. The party involved in changing the origin and re-exporting is liable, he said.

“Whether the buyer or the seller shoulders the risk depends on the contract terms,” Xidias said. For example, if terms cover cost of goods, insurance and freight, the risk is transfered to the buyer when goods are unloaded at their destination. “If it’s Free on Board, then the buyer takes the risk the moment the materials are loaded to the container.”

Chinese importers caught engaging in illegal transshipping or origin fraud — across a range of goods — have faced hefty fines and criminal charges in the past decade. During US President Donald Trump’s first term, when China also imposed tariffs on US goods, some copper scrap importers were fined when Chinese customs detected their efforts to buy rerouted cargoes.

For American scrap traders, they’re left with a choice between sitting on the material or shipping it overseas to get cash. Some choose to take their chances on foreign buyers, though moving the metal is slow and traders still face so much secondary copper they can’t find a market for.

The situation is reflected in the price of so-called No. 2 copper — a grade of recycled material that can be cheaper substitute for the primary metal — which at the end of July touched the largest discount relative to futures contracts in data going back to 2015, according to Fastmarkets. The discount has faded this month after Trump’s copper tariffs excluded cathode and caused the Comex contract to plunge, narrowing the price differential. The discount was 47.50 cents a pound as of Wednesday, according to Fastmarkets.

“The disruptions in mined supply and loss-making processing fees makes scrap more valuable, so I wouldn’t be surprised if the industry is getting creative on trade routes,” Bloomberg Intelligence analyst Grant Sporre said.

Sandvik to supply 32-unit underground equipment fleet for Botswana copper mine

Sandvik is supplying 12 Toro TH663i trucks like this one, plus 20 more pieces of underground equipment, to Khoemacau copper mine in Botswana. Credit: Sandvik Mining.

Chinese mining contractor JCHX has selected Sandvik Mining to supply a 32-unit underground equipment fleet at MMG’s Khoemacau copper mine (KCM) in Botswana.

The order includes 12 Toro TH663i trucks, 10 Toro LH621i loaders, eight Sandvik DD422i development drills, one Sandvik DL432i longhole drill, and one Sandvik Rhino 100 raise borer. Deliveries will continue through the second quarter of 2026.

The contract also includes remote monitoring service, providing critical information to improve fleet performance.

Located in Botswana’s Kalahari copper belt, Khoemacau is a major underground operation with significant expansion underway. Since acquiring the mine in March 2024, operator MMG has advanced plans to increase annual copper production from current levels to 60,000 tonnes within two years, leveraging the existing 3.7 million t/y process plant and targeting higher-grade zones through improved mine access and flexibility.

Longer term, MMG aims to increase total output to 130,000 tonnes of copper in concentrate per year by constructing a new 4.5 million t/y process plant, expanding Zone 5 production and developing nearby deposits. Early works for the expansion project have commenced, with construction expected to begin in 2026 and first concentrate anticipated in 2028.

“We’re proud to partner with Sandvik for this important contract,” said Xiancheng Wang, chair of JCHX. “Sandvik’s reputation for high-performance equipment and strong aftermarket support was key in our decision. This fleet will play a vital role in helping us deliver operational excellence and meet the ambitious production targets set for the Khoemacau site.”

“Our advanced underground technologies and digital solutions will help enable efficiency and performance as the site ramps up production in the coming years,” Mats Eriksson, president of Sandvik, said in a news release.

Tailings could meet much of US critical mineral demand – study

Tailings dam. (Reference image by Ian Cochrane, Flickr.)

A new study from the Colorado School of Mines has found that the United States could meet much of its demand for critical minerals by recovering materials currently discarded in mining waste.

Published this week in Science, the analysis shows that nearly all critical minerals used in clean energy technologies, electronics, and defense applications are already present in ore processed at US mines. However, the majority of these materials end up in tailings and other waste streams rather than being refined for use.

The analysis highlights cobalt and germanium as prime examples. Recovering less than 10% of the cobalt already mined and processed but lost to waste streams would be sufficient to supply the entire US battery market, the authors assert. For germanium, reclaiming under 1% from existing zinc and molybdenum operations would eliminate the need for imports altogether.

The study examined 70 elements across US mining operations. Aside from platinum and palladium, the researchers found that all could theoretically be sourced domestically with improved recovery methods.

Elizabeth Holley, associate professor of mining engineering at Colorado School of Mines and lead author of the study, described mine tailings as a significant untapped resource. “We’re already mining these materials,” she said.

“The question is whether we capture them or throw them away.”

The team combined production data from federally permitted US mines with ore concentration data from the US Geological Survey and other international sources to estimate the amount of critical minerals lost in waste streams.

The findings highlight both a strategic opportunity and a challenge. While recovering minerals from tailings could reduce US dependence on foreign sources and lower the environmental footprint of mining, the researchers note that current market conditions often make byproduct recovery uneconomic. They suggest that additional research, development, and policy incentives will be needed to make large-scale recovery viable.

The study comes as the Trump administration is seeking to secure supplies of critical minerals needed for the energy transition, amid concerns about China’s dominant position in mineral production and processing.

US seeks to stockpile cobalt for first time in decades

Cobalt is used in rechargeable batteries, particularly lithium-ion ones, and in superalloys for high-performance applications. (AI generated Stock image by Ai Inspire.)

The US Defense Department is seeking to buy cobalt for its strategic stockpiles for the first time in decades, the latest move to bolster domestic supplies of critical metals.

The Defense Logistics Agency is seeking offers for up to 7,500 tons of cobalt over the next five years in a contract worth up to $500 million, according to tender documents published this week. It’s the first time the DLA has sought to buy cobalt since 1990, according to a person familiar with the purchase.

Demand for cobalt has risen dramatically in recent years because of its use in batteries, but it is also crucial for a range of applications in military systems. Cobalt-based alloys are used in munitions and jet engines, while the metal is also critical for making magnets used in flaps, landing gear and the flight control surface on an airplane.

The Pentagon’s purchase highlights a shift in government thinking about such metals and would be a major intervention in the cobalt market, accounting for about one sixth of non-Chinese supply of alloy-grade cobalt, according to a Bloomberg calculation. It comes after prices have already been driven higher by an export ban from the metal’s top producer, the Democratic Republic of Congo.

For many years, the DLA was a seller rather than a buyer of cobalt, as budget cuts in the 1990s and 2000s led it to sell off what had once been a giant stockpile of the metal built up during the Cold War.

In recent years, however, securing supply chains for metals like cobalt has become a political priority, as officials seek to reduce reliance on China. Beijing dominates processing of cobalt and other battery metals, and has built up a significant state stockpile of its own through the National Food and Strategic Reserves Administration, more commonly known as the State Reserve Bureau.

The Pentagon did not immediately respond to a request for comment.

In its tender documents, which were first reported by Fastmarkets, the DLA said it was seeking offers for alloy-grade cobalt supplies from only three producers: units of Vale SA in Canada, Sumitomo Metal Mining Co. in Japan, and Glencore Plc’s Nikkelverk plant in Norway. It asked suppliers to propose fixed prices for the supplies over five years.

Traders said the move was likely to drive prices of cobalt higher, particularly for alloy-grade metal, which is a small subset of the overall market. Cobalt has jumped 42% this year after the government of the Democratic Republic of Congo imposed an export ban to prop up prices.

Still, it wasn’t clear whether the DLA would be successful in buying the full 7,500 tons. Traders said there were very few suppliers that would be able to meet the DLA’s requirements. The tender documents stated that the government was intending to spend a minimum of $2 million and a maximum of $500 million on the contract. At current prices, 7,500 tons of cobalt is worth about $313 million.

The solicitation for cobalt comes amid a flurry of published tenders by the Pentagon in less than a month, an indication that the department’s arm that handles critical supply chain purchases is charging ahead with its newly minted spending power authorized under President Donald Trump’s signature tax-and-spending legislation. That fiscal package appropriated about $2 billion for the Defense Logistics Agency to purchase materials the US deems essential and critical to national security.

The Biden administration had also sought to bolster procurement of critical minerals, and in late 2023 Congress passed a new National Defense Authorization Act which gave the DLA greater freedom to make long-term purchases without the congressional approval it had previously needed. It also guaranteed $1 billion a year in funding.

The cobalt tender is one of more than a half a dozen tenders for critical materials published since July 30, and includes niobium, graphite and antimony — industries dominated by China.

The Defense Department has published more tenders to acquire materials this fiscal year than during any since the Cold War ended.

(By Jack Farchy, Joe Deaux and Annie Lee)

Vulcan Elements enters US rare earth magnet manufacturing race

When US-based rare earth magnet manufacturer Vulcan Elements announced this week it signed a supply deal with ReElement Technologies, the financial terms were undisclosed, but the companies said that the price is “significantly below” the floor of $110 per kilogram that the US Department of Defense guaranteed to MP Materials last month.

Rare earth metals are essential in heavy magnets that power electric vehicles, consumer electronics and military applications, and MP Materials is the only US producer, out of its Mountain Pass mine in California.

While China dominates the global rare earth industry, controlling the vast majority of the world’s rare earth processing and refining capacity, Vulcan Elements’ vision is to provide domestic supply with pricing viable in the US market and beyond.

“This pricing will enable Vulcan to be competitive in global markets,” Vulcan CEO John Maslin told Reuters. “We wanted to make sure the unit economics made sense.”

Last week, the privately-held North Carolina-based start up unveiled it has raised $65 million in Series A funding to scale up its planned buildout of a commercial-scale facility in Durham.

That announcement came only a day after Vulcan posted on its website that its domestic rare earth magnet manufacturing capability won the Advanced Manufacturing Innovation for Maritime Readiness Challenge with support from the US Department of Defense’s Defense Industrial Base Consortium.

Over 400 manufacturing companies competed for the award, but Vulcan has, until now, avoided the spotlight.

“We’ve been fairly quiet intentionally, and that’s because we want to put our money where our mouths are,” Vulcan Elements CEO John Maslin told MINING.com in an interview.

“We want to execute. And now that we’re doing that, we have a lot of additional work to do where we have to execute much further at a much larger scale,” he said. “We want to show and not just tell. So now is the right time.”

Vulcan Elements CEO John Maslin at the opening of Vulcan’s small-scale facility. Credit: Brighid Uddyback | Ox Images Photography.

The company is specifically producing neodymium iron boron magnets – and boron is a big blind spot in the US market. As with many other critical minerals, efforts are underway to re-shore supply to the US.

Maslin, a former supply chain officer with the Navy’s nuclear energy program, saw the gap working across nuclear shipbuilding and submarine programs.

“My job was effectively working with the government and appropriations and then taking that and helping finance and procure materials and components for nuclear reactors,” Maslin said.

“I was thinking a lot about the critical components that were going to be fundamental, not just for defense, but for critical economic industries, the 21st century technology race – semiconductors, batteries, rare earth magnets,” Maslin remembered.

“The way that we think about it internally is if you think about your own body, a semiconductor is like your brain, a battery is like your heart, and a rare earth magnet is like your spine. It converts electricity into motion. Everyone was focused on semiconductors and batteries at the time.

“No one was thinking about the third leg of that stool, which is a rare earth magnet. The next generation technologies, either commercially or defense related, drones, data centers that enable AI, robotics, hybrid electric vehicles, et cetera, satellites, aerospace applications, you need all three.”

“But functionally, we knew that China made over 90% of the global supply and that the US made less than 1% and that the demand for these magnets was going exponential, and there needed to be diversity and resiliency in the West.”

Maslin said that all of Vulcan Elements’ materials, whether rare earths or the electrolytic iron or the boron or ferroboron, have traceability down to the mine where that’s coming from, and that feedstock is sourced from US and allied partners.

One of the first rare earth magnetics labs in the US in decades

Maslin met Vulcan’s co-founder, Peter Kulik, who hadopened one of the first rare earth magnetics labs in the US in two decades at the University of Central Florida.

“We said, this is a problem that is too important not to address. We went to the Department of Energy, and we validated our own chemistries with their scientists,” Maslin said. “We made several different grades of magnets, then built a pilot facility.”

The plan was to have the plant online by Q1 2025, fully decoupled from China down to the equipment, software, and material level.

“We opened our doors on March 31st of this year,” Maslin said. “It is a blend of defense and commercial across several different verticals and industries. We have started to deliver and qualify magnets with customers. 100% of our material is US or allied. We either get it from recycled end-of-life magnets, or directly from miners in the US and Canada and Australia, parts of Africa, parts of South America. Nothing from an entity of concern.”

The company is now moving to large-scale commercial, doing a multi-state site search.

“We’re going to go to several hundred tons over the next 18 to 24 months. The goal is to have several thousand tons online by the end of this decade,” Maslin said.

Vulcan is currently producing a mix of samples and low-volume production.

“A lot of it right now is qualification, making sure that we’re hitting the grades that we’re actually delivering the products that customers need. We’re at the point where we’re getting to actually do that with our customers who are very eager to have resilience in their supply chain.

“We have a lot of work to do to deliver even higher performing grades – but we’re moving with the speed and seriousness that this mission and this moment need.”