It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Friday, October 10, 2025

Maduro Offered Venezuela’s Oil to Trump to Avoid Conflict with U.S.

The administration of Venezuelan leader Nicolás Maduro has offered to open up Venezuela’s oil and gold projects to U.S. companies in an attempt to appease the Trump Administration and avoid conflict, the New York Times reported on Friday, quoting multiple sources close to the discussions.

Over several months, officials of the Maduro regime have negotiated with U.S. officials offers of Venezuela’s natural resources and proposed to end some deals with Iran and Russia, in an attempt to avoid increased confrontation with the United States.

Maduro has reportedly offered the Trump Administration to open all Venezuelan oil and gold projects to U.S. companies, NYT reports. The regime in Venezuela was also ready to offer preferential contracts to American firms, re-direct Venezuela’s oil exports from China to the U.S., and reduce energy and mining deals with companies from Iran, China, and Russia.

However, the proposal from Maduro was apparently rebuffed by the U.S. Administration, which was instructed by President Trump to cut off diplomatic efforts with Venezuela, another NYT report said earlier this week.

The cut-off of the diplomatic outreach effectively killed a possible deal, at least for now, according to NYT’s sources close to the discussion.

In recent weeks, the U.S. has sent warships to the Caribbean and has targeted small boats off Venezuela alleging they were transporting drugs.

Meanwhile, the U.S. Treasury authorized this week Shell and the government of Trinidad and Tobago to work on and develop an offshore gas field in Venezuela that is planned to supply gas to Trinidad, whose maritime border with Venezuela is close to the field.

The U.S. authorization is structured in three stages, Trinidad’s attorney general John Jeremie said on Thursday. The first stage allows Shell and Trinidad to negotiate the project with Venezuela and its state oil and gas firm PDVSA. But the authorization makes the inclusion of U.S. firms in the project development mandatory.

“You have to hit commercial targets for U.S. companies. We don't think those targets are hard to meet. They are reasonable,” Jeremie said at a press conference, as carried by Reuters.

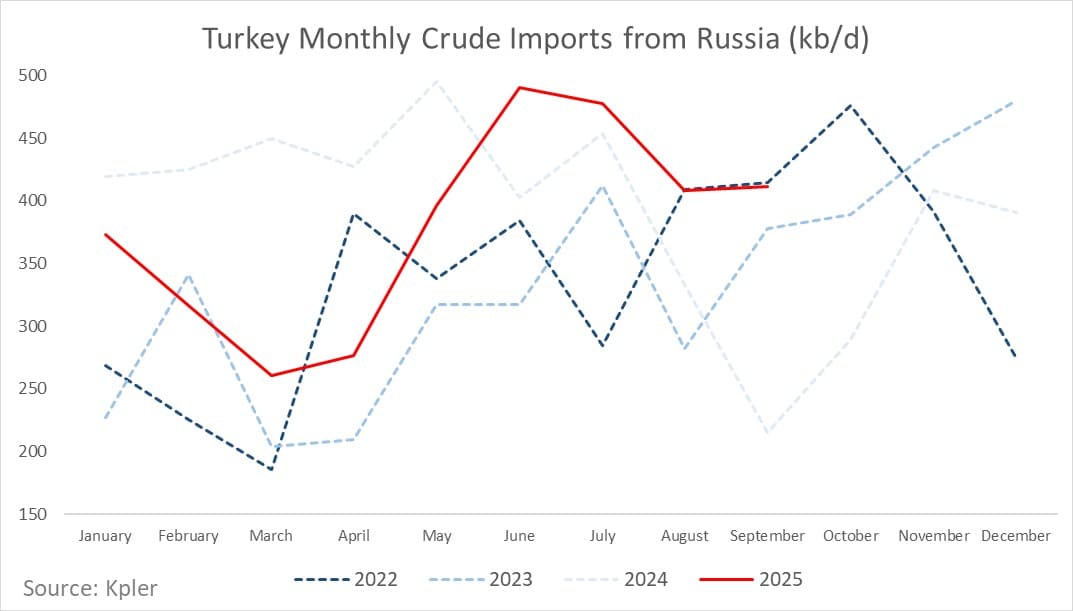

Turkish imports of Russian crude have been rising in recent months, defying political pressure from the Trump administration.

Considering how cheap Russian crude is, there is no real alternative to replace it in Turkish refineries, even if Kurdish exports start ramping up.

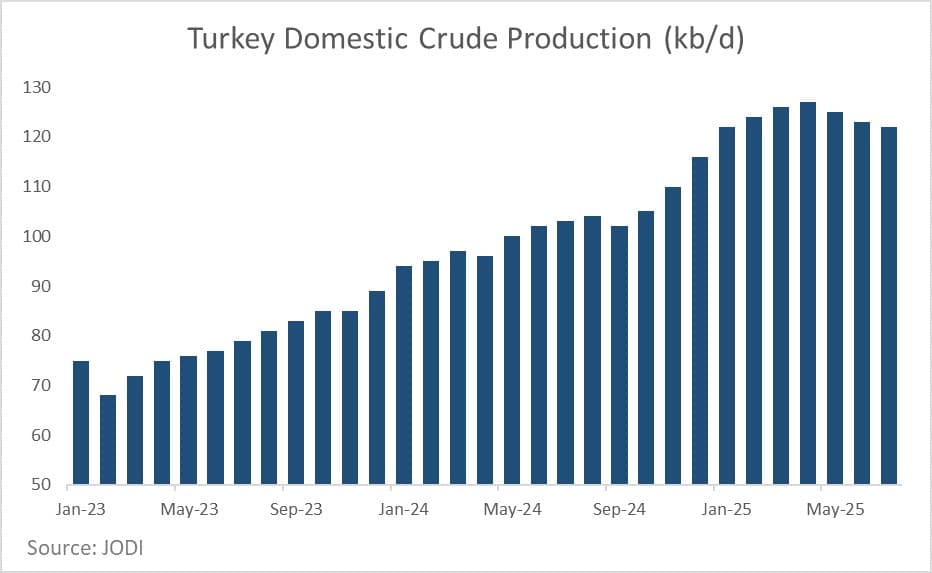

Turkey’s own oil fields have been churning out increasing amounts of crude, limiting the need to buy more from the market.

Midway through autumn 2025, Russian crude oil continues to dominate Turkey’s refinery feedstock, defying both geopolitical pressure and the Trump administration’s assertive diplomacy. September import data show Russian volumes flowing to Turkey above monthly averages at 410,000 b/d, extending a pattern that began in early summer and shows little sign of reversing.

On 25 September, when US President Donald Trump met his Turkish counterpart Recep Tayyip Erdo?an at the White House for the first time in six years, the conversation predictably turned toward energy. Trump urged Ankara to curb its imports of Russian oil – a politically charged message delivered at a time when Turkey’s dependence on Moscow’s barrels is at a four-year high. Yet the Turkish government quickly deflected any responsibility. The country’s energy minister reminded the press that crude procurement is a “commercial decision made by private refining companies”, and not a matter of state policy. Turkey’s refiners – the state-controlled Tüpra? (Türkiye Petrol Rafineleri A.?.) and Azerbaijan’s Socar-owned Star Rafineri A.?. – are the backbone of Turkey’s energy system and the principal buyers of Russian Urals crude.

Since the start of summer 2025, Russian crude imports to Turkey have averaged around 410,000 b/d, roughly 20% higher year-on-year. The reason lies as much in refinery design as in economics. Turkish refineries were built to process heavier, sour grades such as Russia’s Urals – a crude with a 29–30 degrees API gravity and higher sulphur content than lighter Middle Eastern or U.S. grades. Urals isn’t the only sour crude available in the Mediterranean market but finding a viable substitute that matches both quality and price has proven difficult. The challenge has only grown since a series of Ukrainian drone strikes disrupted operations at Russian refineries, curbing domestic throughput and pushing more Urals crude onto export routes. Russia’s seaborne exports have surged to 3.4 million b/d, the highest level since the spring of 2024 – a wave that Turkey, among others, has eagerly absorbed. In the first week of October alone, five Russian tankers arrived from Primorsk and discharged cargoes at Turkish oil terminals.

One theoretically promising substitute is Iraq’s Kirkuk crude, a heavy grade now flowing back to the market after a two-year pause. Iraq recently restarted northern exports to Turkey, potentially offering regional refiners an alternative to Russian barrels. The oil passes through the Kirkuk–Ceyhan pipeline, carrying 400,000–450,000 b/d before its 2023 shutdown. Current plans call for only 190,000 b/d to be sent to Iraq’s state marketer SOMO for export via Ceyhan, with an additional 50,000 b/d reserved for domestic use in the Kurdish region. But Kirkuk’s comeback faces challenges. SOMO intends to sell Kirkuk at the official selling prices, meaning they would be priced at a premium to Brent ($1.25 per barrel in October). Faced with difficulties in selling the first Kirkuk cargoes from Ceyhan, this might be too optimistic as reported spot prices have been more than $1 per barrel below Brent. Moreover, even if flows rise, refiners note that Kirkuk’s volatile quality make it a supplement, not a replacement, for Urals.

Another potential feedstock, Kazakhstan’s Kebco (similar in specification to Urals), is not under EU sanctions and thus commands strong demand across the Mediterranean. But that popularity carries a cost: Kebco trades at a $2.75-per-barrel premium to Dated Brent, compared with an assumed Russian Urals’ $7-per-barrel discount as of early October. Price alone ensures that Russian barrels remain hard to resist. While the return of Kirkuk has diminished Kebco’s premium slightly, market watchers attribute the shift more to expectations of higher Urals supply than to Iraq’s renewed presence. For refiners squeezed by narrow margins, Russian crude still offers the most attractive economics – even amid political risk.

Complicating the picture further is Turkey’s own rising crude production. Newly discovered oilfields – ?ehit Esma Çevik (SEC) and ?ehit Aybüke Yalç?n (SAY), announced in 2022 and 2023 – have lifted national production from 70,000–75,000 b/d in early 2023 to 120,000–125,000 b/d in 2025. Unlike Turkey’s traditional output, a 12 degrees API ultra-heavy crude, the new fields produce a lighter Gabar grade of 40 degrees API, significantly improving the quality of domestic supply. But there’s a catch. Turkish law prohibits the export of domestically produced crude, meaning all output must be refined at home. And since Turkish refineries are configured for heavier blends, lighter domestic oil needs to be blended with heavier grades – most conveniently, Urals. In effect, Turkey’s rising production reinforces (rather than reduces) its reliance on Russian feedstock.

The new fields also carry geopolitical baggage. Both SEC and SAY are located in the restive Kurdish southeast, a region long marred by insurgency and instability. Yet production has been steady, and the oil must find its way into the domestic system – blending Turkish light and Russian heavy crudes in a marriage of necessity. Turkey’s position illustrates the collision of politics, economics, and refinery configuration. Washington’s calls to curtail Russian oil imports may resonate diplomatically, but they clash with the realities of Turkey’s refining infrastructure and cost structure. Alternative supplies – whether from Iraq, Kazakhstan, or the domestic market – remain either too expensive, too limited, or too light to fully displace Urals. As of early autumn, with imports above average and Russian crude still offering the best value per barrel, Ankara shows no urgency to change course. For all the political heat surrounding its choices, Turkey’s energy calculus remains coldly pragmatic: in a world of heavy blends and light politics, Russian oil still fits the Turkish outlook best.

By Natalia Katona for Oilprice.com

Key Russian Refinery Unit Halted After Strike, Tightening European Fuel Supply

In a new operational blow to Russia’s refining capacity, the Kirishi complex has reportedly shut down its CDU-6 crude distillation unit, the largest processing block at the plant, following damage from a Ukrainian drone strike.

According to Reuters, the refinery’s core capacity is now offline, though this has not been confirmed officially by Moscow.

The CDU-6 unit historically accounts for most of Kirishi’s processing output, and its halt means a significant drop in daily refined product volumes. Two industry sources cited in the Reuters report estimate the shutdown could last approximately one month.

While exact daily loss estimates remain unconfirmed, the halt could take up to 160,000 barrels per day off the market for a month, considering that Kirishi’s total crude-processing capacity is around 360,000 bpd, with CDU-6 handling approximately half of that capacity.

That shutdown comes as Russia signals plans to raise output by 137,000 bpd at the upcoming OPEC+ virtual meeting to stabilize prices later this month. The Kirishi cut now undermines that buffer, constraining flexibility in an already volatile market.

European fuel markets are also paying close attention here. The shutdown tightens supplies of diesel and middle distillates, which are already under pressure from sanctions, logistical bottlenecks, and other disruptions. Even if other Kirishi units or nearby refineries partially offset the loss, refiners will face a steeper margin squeeze.

Meanwhile, Ukraine claimed responsibility for a separate strike overnight on the Feodosia oil terminal in Crimea, a key transshipment hub distinct from Kirishi that serves as a rail-sea fuel interchange for Russian military logistics. Kyiv’s defense forces said the terminal’s storage infrastructure sustained “significant damage.”

President Vladimir Putin recently warned that removing Russian crude or curbing its refined output could push prices “well above $100 per barrel”.

Surgutneftegaz, owner of the KINEF-Kirishi complex, has not yet issued a statement confirming the scope of the outage or estimated repair timeline. Market observers are tracking product flows and satellite imagery for signs of disruption as refiners and trading desks reassess exposure to Russia’s shrinking refining network.

By Charles Kennedy for Oilprice.com

China Vows to Protect Its Firms amid Fresh US Oil Sanctions Barrage

China vowed on Friday to protect the rights and interests of Chinese companies after the U.S. unleashed on Thursday a new sanctions package on Chinese entities for importing crude oil from Iran.

The U.S. Treasury on Thursday blacklisted around 100 individuals, vessels, and companies—including China’s Shandong Jincheng Petrochemical Group, a Shandong teapot refinery accused of buying millions of barrels of Iranian crude since 2023. Also sanctioned were the Rizhao Shihua Crude Oil Terminal at Lanshan Port, accused of handling Iran’s “shadow fleet” tankers—like the Kongm, Big Mag, and Voy—that quietly move sanctioned barrels across Asia.

In response to a question from Bloomberg at Friday’s regular press conference, China’s Foreign Ministry spokesperson Guo Jiakun said that “China will do what is necessary to ensure its energy security and safeguard the lawful rights and interests of Chinese companies and citizens.”

“China opposes unilateral illicit sanctions that have no basis in international law or authorization of the UN Security Council. We urge the U.S. to abandon the wrong practice of arbitrarily resorting to sanctions,” the spokesperson said.

“Countries’ normal cooperation with Iran within the framework of international law is legitimate and justified,” the official added.

Thursday’s sanctions were the fourth U.S. round this year targeting China-based buyers of Iranian oil, with Treasury Secretary Scott Bessent vowing to degrade “Iran’s cash flow by dismantling key elements of its export machine.”

UAE-based and Hong Kong-based tanker operators and a number of shell companies in various jurisdictions were also sanctioned.

The sanctions would even impact Sinopec, the Chinese refining giant, as they designate the Rizhao Shihua Crude Oil Terminal Co. Ltd, analysts and industry executives told Reuters.

The terminal is half-owned by a logistics unit of Sinopec’s and handles about a fifth of the refining giant’s crude oil imports, according to Reuters’ sources.

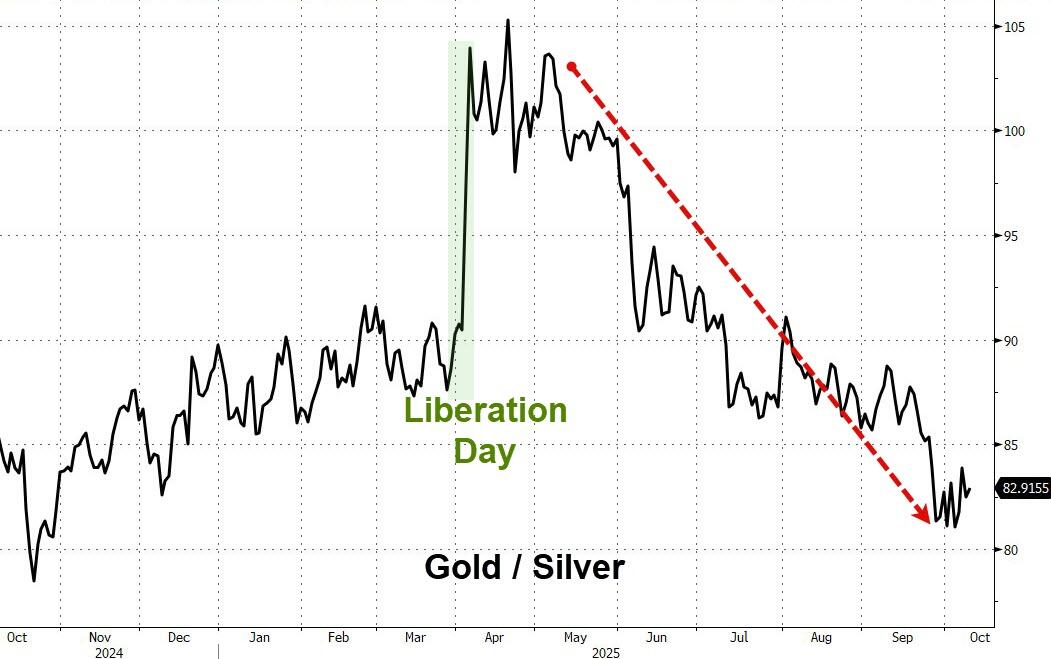

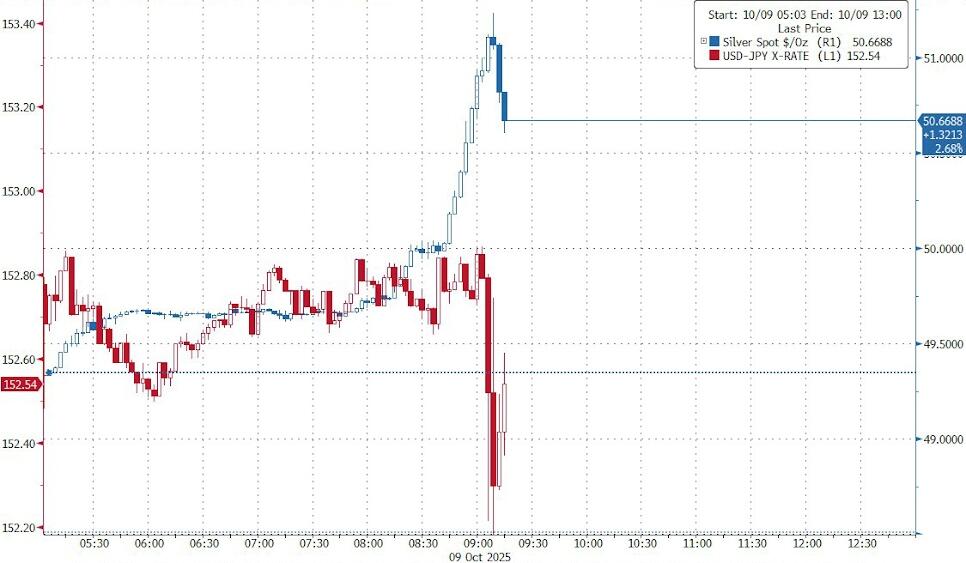

Silver reached the $50-an-ounce level for the first time in decades on Thursday as surging demand for safe-haven assets led to a squeeze on the already-tightened London bullion market.

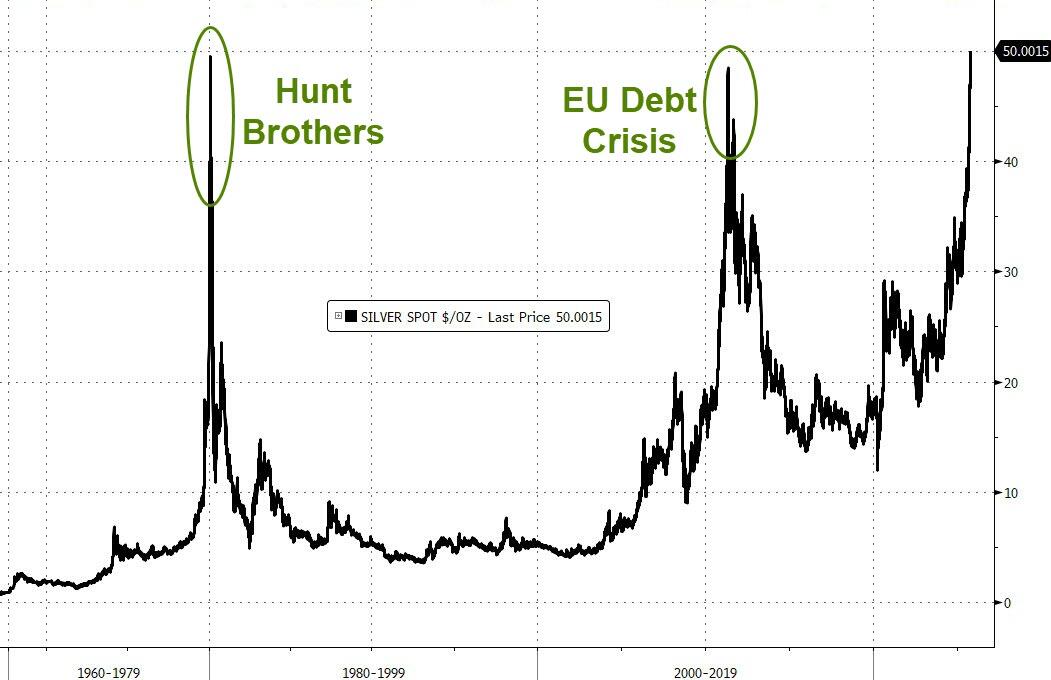

Spot silver traded as high as $51.23 per ounce, the highest since a notorious squeeze orchestrated by the billionaire Hunt brothers in 1980, as investors continued to pile into precious metals.

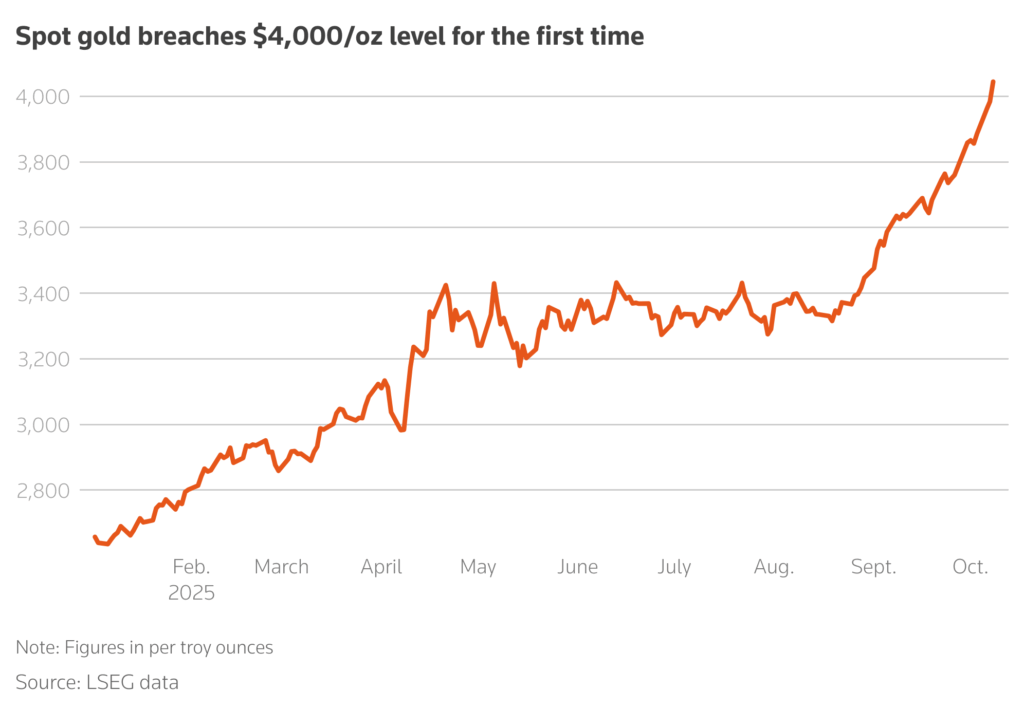

This takes silver’s year-to-date gains to nearly 70%, even surpassing that of gold, which scaled record highs 40 times in 2025 and recently hit the $4,000-an-ounce milestone.

The precious metals rally comes amid rising demand for haven assets sparked by US fiscal risks, an overheating stock market and threats to the Federal Reserve’s independence. These uncertainties have boosted the so-called “debasement trade” — characterized by a reallocation away from fiat currencies and into “harder” assets.

“The conversation around debasement, irrespective of its realities, has ignited investors’ enthusiasm towards gold and silver to the point where regression analysis gives way to something more akin to how investors view AI or the technology sector,” Kieron Hodgson, commodity analyst at Peel Hunt, said in a note to Bloomberg.

Market in deficit

Behind silver’s fast rise is its dual role as both an investment asset and an industrial input. The metal is a key ingredient in solar panels and wind turbines, which collectively account for more than half of its demand.

This year, demand for the metal is expected to exceed supply for the fifth consecutive year, according to Silver Institute forecasts.

“I think the deficits are the slow burn,” said Philip Newman, director of consultancy Metals Focus. “Just the size of the deficits have been so remarkable, and it takes time for that to manifest itself in the price.”

London constraints

Meanwhile, the silver market in London has also tightened to an almost unprecedented degree, with sky-high borrowing costs for the metal. This year, fears that the US could label the metal as a critical mineral and levy tariffs spurred a dash to ship the metal into New York, drawing down inventories in London.

Much of the stock of silver in London is held in vaults backing exchange-traded funds, and therefore not available to buy or borrow on the market.

“I think when you look at above-ground stocks of silver in London you are looking at an increasingly small share, which is not allocated against ETFs,” Newman said.

However, TD Securities recently said that this massive silver squeeze is approaching its “end game” as the London market begins to restore its liquidity.

Silver volatility

While silver often moves in tandem with gold, sharing its strong negative correlation with the US dollar and interest rates, it is much more volatile than its more expensive sister metal.

The metal also has a stronger cult following among retail investors, who view silver as being suppressed by large banks and institutions.

That impassioned following has helped drive sharp rallies in silver in 2011 and 2020, when it surged 140% in less than five months. Over the following year, Redditors jumped on board, while #silversqueeze rapidly gained momentum on social media.

In 1980, it was the Hunt brothers, Texan oil billionaires and notorious speculators, whose fear of inflation and belief in the metal as a store of wealth prompted them to try to corner the global market. They stockpiled more than 200 million oz. of silver, driving the price above $50 before it crashed below $11.

That makes silver one of only a small handful of markets whose record highs from the commodity spikes of the 1970s and 1980s have yet to be surpassed. In inflation-adjusted terms, silver’s new high is only worth approximately one quarter of its 1980 peak, according to Bloomberg.

Gold has reached record highs above $4,000, driven by investors seeking safety in alternative assets amidst a "debasement trade" and a perceived shift in monetary regimes.

Silver has significantly outperformed gold, with its price topping $50, echoing its 1980 highs and potentially linked to the forced closing of silver and yen shorts.

The silver market faces tightening conditions due to industrial demand exceeding supply for the fifth consecutive year, high borrowing costs in London, and fears of U.S. tariffs.

The last few months have seen gold soar to record highs above $4,000 amid the so-called “debasement trade,” with investors flocking to the perceived safety of alternates while pulling away from major currencies.

However, quietly on the side, silver has been outperforming gold...

Source: Bloomberg

Citadel's Ken Griffin said investors are starting to view gold as a safer asset than the dollar, a development that's "really concerning" to the billionaire investor.

“The conversation around debasement, irrespective of its realities, has ignited investors enthusiasm towards gold and silver to the point where regression analysis gives way to something more akin to how investors view AI or the technology sector,” said Kieron Hodgson, commodity analyst at Peel Hunt Ltd.

And now that is spreading to bitcoin and silver as the white metal topped $50 this morning...

Silver's surge takes it back to the highs from 1980...

...when the Hunt brothers, Texan oil billionaires and notorious speculators, whose fear of inflation and belief in the metal as a store of wealth prompted them to try to corner the global market. They stockpiled more than 200 million ounces, driving the price above $50 an ounce before it crashed below $11.

Notably, silver in yen really snapped higher this morning...

With a break in the relationship as silver topped $50 - Something's going on there... Were silver shorts being funded with Yen shorts? It appears that forced closing of silver shorts led to forced closing of yen shorts?

The white metal is used around the world as an investment asset, but also has industrial applications including in solar panels and wind turbines, which collectively account for more than half of the silver sold. Demand is set to exceed supply for the fifth consecutive year in 2025.

“I think the deficits are the slow burn,” said Philip Newman, director of consultancy Metals Focus Ltd.

“Just the size of the deficits have been so remarkable, and it takes time for that to manifest itself in the price.”

Additionally, Bloomberg reports that the silver market in London has tightened to an almost unprecedented degree, with sky-high borrowing costs for the metal.

This year, fears that the US could levy tariffs on silver have spurred a dash to ship the metal to the US, drawing down inventories in London and reducing the amount of material available to borrow.

Much of the stock of silver in London is held in vaults backing exchange-traded funds, and not available to buy or borrow on the market.

“I think when you look at above-ground stocks of silver in London you are looking at an increasingly small share, which is not allocated against ETFs,” Newman said.

As we detailed earlier in the week, it appears the so-called "debasement trade" - driving investors to bet more on gold, silver, and bitcoin - is set to continue with Gold remaining Goldman Sachs' highest-conviction long commodity recommendation because of the:

Additional price upside in our base case (driven by structurally higher central bank gold demand)

Large upside risks to our price forecast from potential additional private sector diversification

Attractive portfolio hedging properties in downside (tail) scenarios that .are less favorable for equity-bond portfolios than our base case (e.g. global growth slowdown, rising market concerns about DM macro policy)

This price hike is likely to trigger more fears from Citadel's Griffin who warned, during and interview with Bloomberg's Francine Lacqua, that "we're seeing substantial asset inflation away from the dollar as people are looking for ways to effectively de-dollarize, or de-risk their portfolios vis-a-vis US sovereign risk."

By Zerohedge

GRAPHIC:

Gold’s rush above $4,000 cements status as global bellwether

Gold’s unprecedented ascent this week to the $4,000 an ounce milestone and beyond puts it on course for its best year since the Iranian Revolution in 1979, solidifying its status as a barometer for global geopolitics and the economy.

Bullion’s 53% gain so far this year follows a stellar 27% rise in 2024.

The steady upward trajectory has been driven by a rush to the asset considered a safe store of value as investors seek cover from uncertainties spurred by conflicts in the Middle East, between Russia and Ukraine, political developments in the US, Japan and France, all supplemented by bets for more US interest rate cuts.

“Gold is performing its important role as a bellwether or a barometer, which gauges when things just aren’t right,” said Ross Norman, an independent analyst.

Spot gold steadied at around $4,025 per ounce on Thursday, hitting pause after surging to an all-time high of $4,059.05 on Wednesday, as investors assessed an Israel-Hamas ceasefire deal.

“Having cleared the $4,000 hurdle, by rights gold should pause for breath. That said, it has not shown much restraint year to date,” Norman said.

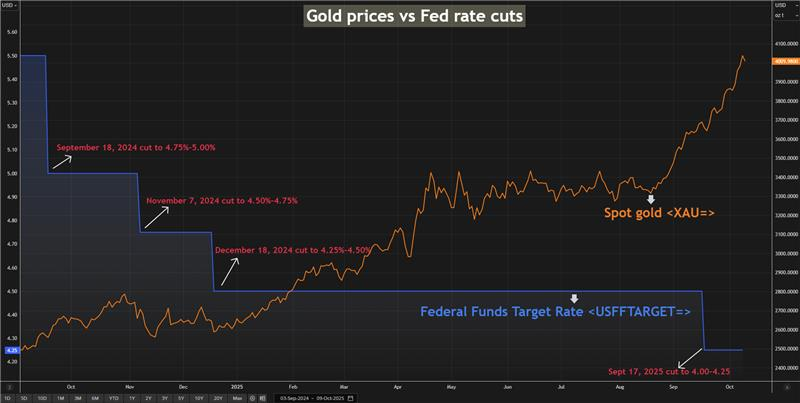

Bullion has logged multiple record highs this year, shattering analyst expectations, also underpinned by expectations of US interest rate cuts since that would translate into reduced opportunity cost of holding assets such as gold, which pays no interest or dividends, while also weakening the dollar.

Market participants see chances of two more rate cuts this year, with the CME FedWatch tool showing a 95% chance of a 25 basis-point cut during the Federal Reserve’s upcoming meeting on October 29.

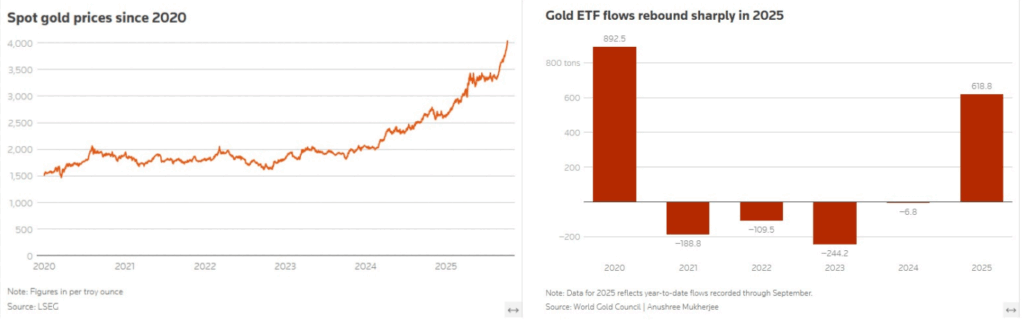

A continued rise in central bank purchases as a means to diversify assets, along with increased flow into gold-backed exchange-traded funds, has also boosted gold’s status.

Globally, inflows into gold ETFs have hit $64 billion year-to-date, according to World Gold Council data, flipping from outflows of about $23 billion over the last four years.

Gold-backed ETFs in the second-biggest bullion consumer India, meanwhile, registered their largest monthly inflow in September, taking assets under management to a record $10 billion.

And there is more room to go, market participants said.

“Investor appetite isn’t slowing down… this upward trajectory suggests more room for expansion, and less reason for it to drop,” said Fawad Razaqzada, market analyst at City Index and FOREX.com.

Silver, meanwhile, was trading at $51 per ounce, after hitting its all-time high of $51.22 earlier in the session. The metal has gained 72% this year, driven by the same factors driving gold and supported by underlying market tightness.

“Silver has also benefited as investors cast their sights across the precious metals complex amid the broader safe-haven play,” said Han Tan, chief market analyst at Nemo.money.

(By Anjana Anil, Kavya Balaraman and Anushree Mukherjee; Editing by Arpan Varghese and Marguerita Choy)