It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Friday, July 25, 2025

Congo is targeting cobalt price that boosts local processing

Processing facilities at Tenke Fungurume mine in 2016 before the CMOC acquisition. (Image courtesy of Lundin Mining.)

The Democratic Republic of Congo is seeking a cobalt price that encourages domestic processing, as the government considers its next steps to follow a ban on exports of the battery metal, according to the chairman of the state mining company.

Congo, which accounts for about three-quarters of global cobalt supply, suspended shipments for four months on Feb. 22, before extending the ban by three months in June. The decision came after prices slumped in recent years as output soared, particularly from two mines operated by China’s CMOC Group Ltd.

“No one can invest in a refinery in the country because the price was not sustainable,” Gecamines Chairman Guy-Robert Lukama said in a discussion this week with the Washington-based Center for Strategic and International Studies.

Congo’s mines export an intermediate product called cobalt hydroxide which is transformed into battery-grade material or metal elsewhere, mainly in China.

The initial ban was introduced shortly after benchmark prices dropped toward historic lows of less than $10 a pound. They have risen almost 60% since Congo closed its borders to cobalt shipments, while the price of hydroxide has more than doubled, according to Fastmarkets data.

Congo doesn’t want a return to peaks above $40 a pound — experienced in 2018 and 2022 — but “it was our duty as a country to stabilize the price,” Lukama said. A period of “totally insane” supply growth had led to more than 12 months of inventory being held outside the country, he said.

The trading unit of CMOC, which produced more than 40% of the world’s cobalt in 2024, last month declared force majeure on hydroxide deliveries, showing the increasing strain on flows. Miners are stockpiling cobalt while continuing to export copper – the two metals are mined together in Congo.

China’s imports of cobalt intermediates slumped over 60% in June from the prior month, according to customs data published over the weekend, marking the first significant month-on-month decline since Congo’s export ban was introduced in February.

The largest producers of cobalt after CMOC are commodities giant Glencore Plc and Kazakhstan-backed Eurasian Resources Group Sarl, which both own major assets in Congo. Gecamines is a minority shareholder in joint ventures with all three firms.

The continuing ban coincides with Congo and the US working toward a strategic partnership to bring more American investment into the African nation’s reserves of copper, cobalt, lithium and tantalum. President Donald Trump’s administration is trying to loosen China’s grip on key minerals and their supply chains.

Congo wishes to ensure that cobalt is “available for everyone” instead of the world being “dependent on one jurisdiction,” Lukama said.

The country’s leaders are weighing longer-term options, including possible export limits once the ban is lifted, to balance the market, support prices and promote local refining. A quota “could make sense,” according to Lukama. “We are very pragmatic on what we’re looking for.”

Analysts have warned that too-stringent controls and surging prices could hasten a shift by manufacturers of electric-vehicle batteries – the biggest single source of cobalt demand – toward technologies that don’t use the metal.

(By William Clowes)

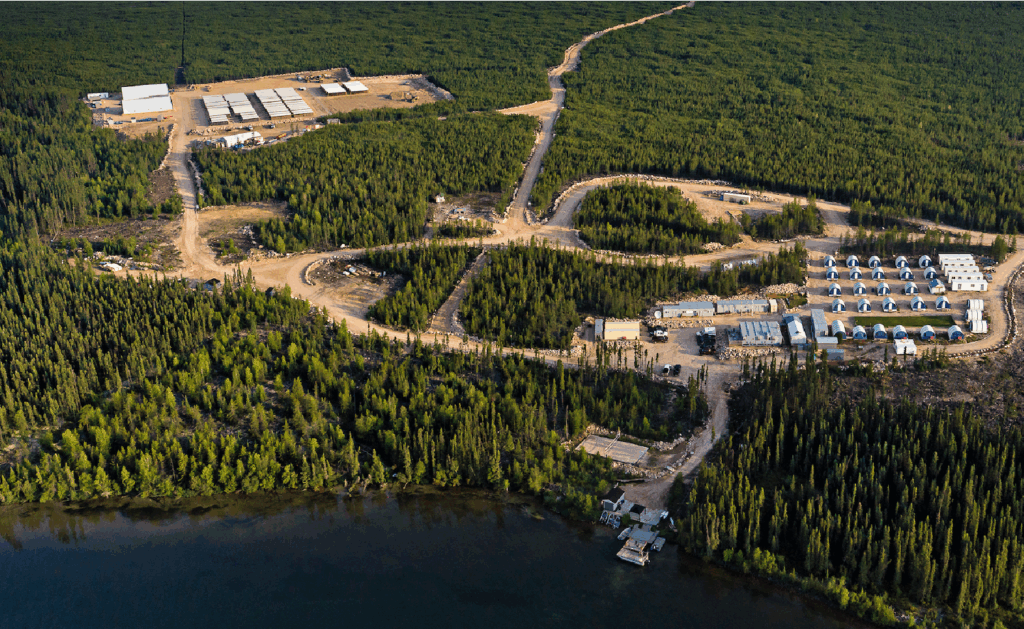

NexGen consolidates interest in Athabasca land package from Rio Tinto

Aerial view of NexGen Energy’s Rook 1 project in Saskatchewan, Canada. Image from NexGen Energy.

NexGen Energy (TSX, NYSE: NXE) (ASX: NXG) is now the 100% owner of its portfolio of exploration assets in the southwestern Athabasca Basin after consolidating a minority interest held by Rio Tinto on certain projects.

On Thursday, the Vancouver-headquartered uranium miner announced it has acquired Rio’s 10% production carried interest over 39 mineral claims in the region, including those hosting the PCE discovery, by exercising its right of first refusal on these assets.

Financial details of the transaction were not disclosed by the company.

As set out in the parties’ initial arrangement, Rio is entitled to a 10% undivided interest in future production from the mineral claims, carried through to the commencement of commercial production. This was put in place before NexGen acquired the land package in 2012.

The centrepiece of the claims package is PCE — or Patterson Corridor East — an uranium occurrence situated 3.5 km east of the world-class Arrow deposit that the NexGen team discovered in 2014.

Part of the larger, 100%-owned Rook I property, the Arrow deposit is host to one of the largest uranium resources in the world, containing 256.7 million lb. of U3O8 (uranium oxide) in the measured and indicated categories and another 80.7 million lb. in inferred.

Anchored by this resource, NexGen considers Rook I to be the largest development-stage uranium project in all of Canada. A feasibility study in 2021 estimated an after-tax net present value (at 8% discount) of C$3.47 billion with a 52.4% internal rate of return. The proposed mine, which is now in the engineering phase, could produce nearly 29 million lb. of U3O8 per year over the first half of its approximate 10.7-year life.

The PCE discovery, according to the company, could mirror that of Arrow due to their similarities in geology. Initial drilling results at PCE have indicated an expansive footprint with remarkable continuity of mineralization, it said.

In a press release, NexGen CEO Leigh Curyer said that the two deposits could help meet the “ever-growing need for a safe, secure supply of uranium,” citing that the market is currently in a deficit and the massive spending required to build AI data centres, which would be powered by nuclear energy.

“Given the world class extent, high grade and superior technical setting of mineralization discovered to date at our two projects, consolidating our portfolio at PCE and surrounding area to match our 100% ownership in our world-class Arrow deposit, is entirely in line with our strategic objective of becoming the future leader in uranium production worldwide,” he said.

Shares of NexGen Energy surged more than 5% on Thursday in New York, closing at a near six-month high of $7.43 with a market capitalization of $4.4 billion. By Friday, the stock had pulled back to around $7.10.

US rare earth stock cracks top 50 mining companies for the first time

Rare earth mining – a magnet for investors. Image: MP Materials

At the end of the second quarter the MINING.COM TOP 50* ranking of the world’s most valuable miners had a combined market capitalization of just under $1.50 trillion, up a respectable $213 billion so far in 2025.

The total stock market valuation of the world’s biggest mining companies remains nearly $250 billion below the all-time high reached three years ago, however. The Top 50 also once again underperformed the broader market despite new multi-year highs and record prices for a number of major metals over the last three months.

Rare event

Since the inception of the Top 50, China Northern Rare Earth has been the only producer of the 17 elements in the ranking despite the frenzy surrounding the sector as China tightens control and rare earth becomes a geopolitical hot potato.

At the end of Q1, these pages speculated that there are no obvious REE candidates that could join the Top 50 in short order. It took a groundbreaking deal with the Pentagon to prove investors wrong and reorder an industry that – despite its high profile – has few large caps.

MP Materials, which operates the Mountain Pass mine in California, is now up three-fold in value year to date, with the Las Vegas-based company debuting at position 40 at an $11 billion valuation. The counter did come close in March 2022, but the whole mining industry was riding high at the time and the ticket for entry meant it fell just outside the ranking.

While the MP Materials-DoD deal is certainly a game-changer in the US rare earth landscape, how much will filter through to the rest of the industry still suffering from depressed Chinese pricing for the magnet material is debatable.

Australia’s Lynas Rare Earths has come close in the past and is up more than 50% this year for a valuation of $6.1 billion, but given rare earth mining’s relatively small overall size – in the single billions of dollars – MP Materials and China Northern Rare Earth may have the field to themselves for the foreseeable future.

Lithium lift

Lithium’s representation in the ranking is set to increase again after Zangge Mining – controlled by Zijin Mining, which comfortably occupies the no 4 slot – announced the suspension of operations at its lithium mine in China’s west.

That breathed some life into lithium stocks which have been decimated since peaking in 2022 with six stocks in the ranking. Those days are long gone, but China’s Ganfeng Lithium did manage to squeak back in to join Chile’s SQM.

Albemarle only just missed the cut and now ranks as the 51st most valuable mining firm at a $9.1 billion valuation, but Australian producers like Minerals Resources and Pilbara Minerals have a long road ahead as does another former constituent, China’s Tianqi.

Whether other producers follow Zangge’s move, which was at the behest of the local government after all, is yet to be determined but the brutal economics of EV battery lithium means the game of chicken among producers outside China must be entering its final innings.

Despite the recent flicker, the value destruction caused by the slump in lithium prices has been eye-popping. Lithium stocks in the index peaked in the second quarter of 2022 with a combined value of nearly $120 billion – now the two remaining counters barely make it to $20 billion.

More precious

Unsurprisingly, precious metals counters dominate the best performer list and make up the majority of new entrants. After a long absence, Impala Platinum returns to the ranks at no 50 after jumping 16 places to join the only other PGM representative, Valterra (formerly Anglo Platinum), which itself has gained 9 places so far in 2025.

Gold, silver and PGM miners, and royalty companies now represent 31% of the value of the Top 50, up from 24% at the start of the year. The strength in precious metals has also seen Canada overtake Australia for the first time in terms of the value of miners headquartered there.

At 22% of the index, the 13 Canadian companies collectively are worth $320 billion compared to $293 billion for the now five Australian firms with the inclusion this year for the first time of Sydney-based gold stock Evolution Mining.

In their current form, Melbourne-based BHP and Rio Tinto have been the top two global mining stocks since the turn of the century, together worth $234 billion today.

Old guard

For the Q2 snapshot the lowest ranked entry must now be worth $9 billion from less than $7 billion at the end of last year, providing some support for the index as the old guard continues to underperform.

Mining’s traditional big 5 – BHP, Rio Tinto, Glencore, Vale and Anglo American – that trace their roots back many decades if not more than a century, were pounded down in 2024 losing a collective $120 billion over the course of the year. So far this year investors in the group have seen these counters recoup only 1% of those losses.

In the past these companies would, apart from wobbles as the Chinese supercycle became just a cycle, consistently occupied the top five slots in the ranking, supported by vast asset portfolios covering a range of commodities across many regions.

Now the big diversified stocks – the mining industry’s now erstwhile version of the Mag 7 – make up less than 24% of the total index, down from a height of 38% at the end of 2022.

Diversification and an extensive metal portfolio is not the ticket it used to be and for the second quarter another longtime occupant drops out for the first time.

Sweden’s Boliden, which operates Europe’s largest copper mine and can make the most of PGM credits at its other base metal operations, follows another European stalwart – Polish copper producer KGHM – out the door proving that despite the bellwether metal’s bright prospects, investors have become very picky.

KGHM dropped out at the end of 2024 and now languishes in the mid-60s after a lacklustre year not far behind South32, a base and minor metal specialist, which exited at the end of the Q1 after an unbroken entry since being spun out of BHP a decade ago.

NOTES:

Source: MINING.COM, stock exchange data, company reports. Share data from primary-listed exchange at close July 18, 2025 close of trading converted to US$ where applicable. Percentage change based on US$ market cap difference, not share price change in local currency.

As with any ranking, criteria for inclusion are contentious. We decided to exclude unlisted and state-owned enterprises at the outset due to a lack of information. That, of course, excludes giants like Chile’s Codelco, Uzbekistan’s Navoi Mining (the gold and uranium giant may list later this year), Eurochem, a major potash firm, and a number of entities in China and developing countries around the world. Another central criterion was the depth of involvement in the industry, and how far upstream is the bulk of its revenue, before an enterprise can rightfully be called a mining company.

For instance, should smelter companies or commodity traders that own minority stakes in mining assets be included, especially if these investments have no operational component or even warrant a seat on the board?This is a common structure in Asia and excluding these types of companies removed well-known names like Japan’s Marubeni and Mitsui, Korea Zinc and Chile’s Copec.

Levels of operational or strategic involvement and size of shareholding were other central considerations. Do streaming and royalty companies that receive metals from mining operations without shareholding qualify or are they just specialised financing vehicles? We included Franco Nevada, Royal Gold and Wheaton Precious Metals on the basis of their deep involvement in the industry.

Vertically integrated concerns like Alcoa and energy companies such as Shenhua Energy or Bayan Resources where power, ports and railways make up a large portion of revenues pose a problem. The revenue mix also tends to change alongside volatile coal prices. Same goes for battery makers like China’s CATL which is increasingly moving upstream, but where mining will continue to represent a small portion of its valuation.

Another consideration is diversified companies such as Anglo American with separately listed majority-owned subsidiaries. We’ve included Angloplat in the ranking but excluded Kumba Iron Ore in which Anglo has a 70% stake to avoid double counting. Similarly we excluded Hindustan Zinc which is listed separately but majority owned by Vedanta.

With other groups like Mexico’s Penoles where refining and chemicals make up a substantial part of the business where possible the Top 50 would include separately listed operating subsidiaries that are dedicated to mining. This is also why Southern Copper represents Grupo Mexico in the ranking.

Many steelmakers own and often operate iron ore and other metal mines, but in the interest of balance and diversity we excluded the steel industry, and with that many companies that have substantial mining assets including giants like ArcelorMittal, Magnitogorsk, Ternium, Baosteel and many others.

Head office refers to operational headquarters wherever applicable, for example BHP and Rio Tinto are shown as Melbourne, Australia, but Antofagasta is the exception that proves the rule. We consider the company’s HQ to be in London, where it has been listed since the late 1800s.

Please let us know of any errors, omissions, deletions or additions to the ranking or suggest a different methodology: email Frik Els at fels@mining.com with Top 50 in the subject line.

Trafigura’s buyback headache grows amid fresh wave of exits

A fresh wave of senior executive departures is heaping pressure on Trafigura Group’s commitment to buy back its employees’ shares, just as a profit boom shows signs of faltering.

Trafigura has deferred about 30% of the buybacks that were scheduled for this year, according to people familiar with the matter. Among current and former Trafigura traders, many of whom have the majority of their wealth tied up in the company, conversations have turned to whether the commodity trading giant will delay part of next year’s planned repurchases as well, the people said.

Share buybacks are the main way that Trafigura rewards the roughly 1,400 employees that own the company, and have been a conduit for vast riches in recent years. The deferrals mean its current generation of traders face a less certain future — at the same time as some of its rivals are going on aggressive hiring sprees.

The departure of a large number of longstanding top executives has piled pressure on the company because it commits to buy their shares back in installments when they leave. The departures are also coming after a period of extraordinarily high profits, which has inflated the value of the shares due to be bought back. Already in the six months to March, Trafigura spent more money on buybacks than it made in net profit.

Trafigura does have wide discretion about how much to spend on buybacks, and a person close to the company said that any decision about next year’s buyback would only be made after the end of Trafigura’s financial year in September. The person highlighted that the company’s group equity of $16.2 billion at the end of March was well above a self-imposed minimum of $15 billion, and represented nearly 20% of its total assets — also well above a ratio of 15% that the company considers to be comfortable.

Over the past two years, Trafigura’s three top executives all retired from their jobs, culminating in only the second CEO transition in the trading house’s history.

The departures have continued this year with a fresh wave of senior exits, including Hadi Hallouche, head of Trafigura’s downstream oil division, Julien Rolland, head of strategic projects, and Ignacio Moyano, the chief risk officer.

More are leaving from the middle ranks of the trading house: former crude trading head for Asia and Europe Daniel Yuen is joining Millenium Management, while head of Asia carbon trading Rushan Pandya is leaving to join Mercuria Energy Group Ltd., according to people familiar with the matter.

At the same time, the company’s profits are also under pressure. While Trafigura continues to report earnings far higher than any time before 2020, its profits have fallen from the highs of 2022-2023 when the market fallout from Russia’s full-scale invasion of Ukraine helped lift earnings across the industry. When Trafigura reported half year results in June, it warned of trading headwinds.

People familiar with the matter said that the company took a hit earlier this year in gas, where prices have tumbled since February. Meanwhile, its sprawling zinc smelting business Nyrstar remains under severe pressure from a tight market for raw materials.

The company is also still trying to rebuild its reputation after a series of scandals — ranging from alleged frauds against it in nickel and Mongolia that have cost it more than $1.5 billion, to a corruption conviction earlier this year in Switzerland.

The situation has made for a challenging first few months in the job for Richard Holtum, who took over as the third chief executive officer in Trafigura’s history in January. Bloomberg reported last year that he had told staff he wanted Trafigura to focus on making money, and since taking the job he has expounded a mantra of making the company “simpler,” “smarter,” and “sharper.”

Still, the large buyback bill hasn’t stopped Trafigura investing, with the company forming part of a consortium to buy an oil refinery in France, as well as striking large prepayment deals in copper and iron ore. The trading house also recently returned to the bond market, raising $500 million earlier this month.

“Trafigura’s key financial metrics are at historically high levels, and shareholder returns do not constrain its ability to invest and grow,” the company said in a response to questions. “In addition, the group maintains near-record liquidity, and its trading performance remains strong.”

(By Jack Farchy and Archie Hunter)

US targets mine waste to boost local critical minerals supply

The US government has launched a new effort to extract valuable critical minerals, including rare earths, lithium, cobalt, and uranium, from mine waste and abandoned sites, aiming to reduce dependence on foreign suppliers and strengthen domestic production.

Interior Secretary Doug Burgum has ordered a series of regulatory changes to streamline federal oversight and fast-track projects recovering minerals from coal refuse, tailings, and shuttered uranium mines.

The directive includes updated guidance to make these recovery projects eligible for federal funding and requires faster review timelines for new proposals. It also directs the US Geological Survey to map and inventory mine waste on federal lands to identify sites rich in critical minerals.

Research by the USGS and state geological agencies has already revealed promising sources, including tellurium in tailings at Utah’s Bingham Canyon copper mine and zinc and germanium in waste from the long-abandoned Tar Creek mines in Oklahoma.

“This initiative reflects our unwavering commitment to achieving mineral independence and ensuring that America leads the way in advanced technologies that power our future,” Burgum said in a release. His department controls large swathes of federal land some of it home to abandoned mines and the initiative could turn environmental liabilities into economic assets.

Acting Assistant Secretary of Lands and Minerals Adam Suess added that streamlining recovery efforts will help “unleash the full potential of America’s mineral resources to bolster national security and economic growth.”

The move builds on Trump’s broader strategy to revitalize the US mineral sector, which has lagged behind global leaders like China in both production and processing. In March, Trump invoked the Defense Production Act to ramp up domestic processing of several key minerals.

Teck approves $2.4B expansion of Highland Valley Copper

Teck Resources’ (TSX: TECK.A, TECK.B)(NYSE: TECK) board has approved a C$2.1–C$2.4 billion ($1.6 -$1.8 bn) project to extend the life of its Highland Valley Copper Mine (HVC) in British Columbia, securing operations at Canada’s largest copper mine into the mid-2040s.

Construction on the mine life extension (MLE) is set to begin in August. The Vancouver-based miner expects the expansion to support average annual production of 137,000 tonnes of copper through the remainder of the mine’s life.

“This extension is foundational to our strategy to double copper production by the end of the decade,” President and CEO Jonathan Price said in a statement.

“Given the strong demand for copper as an energy transition metal, the HVC MLE will generate a robust internal return rate (IRR) and secure access to this critical mineral for the next two decades,” Price said.

The board’s green light follows the province’s approval of the project’s environmental assessment certificate last month.

The project includes a major pushback of the Valley pit to access higher-grade ore, along with infrastructure upgrades: an expanded mine fleet, grinding circuit enhancements, increased tailings capacity, and improved power and water systems.

Teck says the project will create roughly 2,900 construction jobs and support 1,500 ongoing roles once operational. Price also emphasized the project’s role in strengthening Canada’s critical minerals sector and stimulating economic activity in the region.

The fresh capital estimate reflects current construction risks, inflation, potential impact of tariffs, and early procurement of mobile equipment. It includes built-in contingencies and opportunities for cost optimization as work progresses, Teck said.

The HVC expansion forms part of Teck’s broader $3.9 billion investment plan to boost copper output to 800,000 tonnes annually by 2030.

Revised copper guidance

The company made the announcement alongside its second-quarter results, which showed a sharp improvement from the same period last year. Profit before tax surged to C$125 million from just C$20 million, while net profit jumped to C$206 million, or $0.42 per share, compared to C$21 million, or $0.04 per share, in Q2 2024. Revenue rose to C$2.02 billion from C$1.80 billion a year earlier.

Adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) came in at C$722 million, beating BMO Capital Markets’ forecast of C$661 million. Copper output totalled 109,000 tonnes, exceeding BMO’s estimate but falling short of the broader analyst consensus.

Despite the strong quarterly performance, Teck lowered its 2025 copper production guidance to between 470,000 and 525,000 tonnes, down from a previous range of 490,000 to 565,000 tonnes. The revision stems mainly from lower-than-expected output at its Quebrada Blanca mine in Chile. BMO had forecast 479,000 tonnes, with the consensus at 502,000 tonnes.

The Vancouver-based miner ended the quarter with a net debt of C$211 million. It noted that elevated capital spending at Quebrada Blanca and Highland Valley weighed on cash flow.

Gem Diamonds to cut jobs, salaries amid industry crisis

Letšeng diamond mine in Lesotho. (Image courtesy of Gem Diamonds.)

Gem Diamonds (LON: GEMD) has become the latest casualty in a deepening crisis engulfing the global diamond industry, announcing sweeping cost-cutting measures as the market buckles under falling prices and the growing popularity of lab-grown alternatives.

The Africa-focused diamond producer reported a 43% drop in revenue to $44.7 million for the first half of its financial year. Carat sales fell 22% to 44,360, while the average price per carat plunged 26% to $1,008.

In response,Gem Diamonds said it would reduce operating costs by $1.4 million to $1.6 million per month and cut around 250 jobs, or 20% of its workforce, at its Letšeng mine in Lesotho. Executives have also taken voluntary salary reductions.

“Considering the prolonged weakness in global diamond prices, compounded by a weak dollar and ongoing US tariff uncertainties, Gem has implemented decisive measures to conserve cash and protect shareholder value,” the company said.

Despite meeting production targets, Gem Diamonds admitted it has not been shielded from sustained pressure on rough diamond prices and adverse currency movements. Investors reacted accordingly, with the company’s shares falling more than 20% in early trading on the London Stock Exchange. They partially rebound to 5.5 pence in late trading, valuing the company at £7.7 million ($10 million).

Gem Diamonds’ measures mirrors those of its peers. just last week, Burgundy Diamond Mines (ASX: BDM) halted open pit operations at its Ekati mine in Canada’s Northwest Territories, triggering mass layoffs.

All three operating diamond mines in the region — Ekati, Diavik and Gahcho Kué — are now facing eventual closure, with Diavik scheduled to close in 2026 and Gahcho Kué expected to cease operations by 2030. Ekati’s long-term future remains uncertain. Getting worse

Signs of a worsening crisis in the diamond sector were already clear in the first three months of 2025. De Beers, the world’s largest producer by value, saw a 44% drop in revenue in Q1 and is sitting on $2 billion in unsold inventory. It plans to cut over 1,000 jobs at its Debswana joint venture in Botswana.

Even Lucara (TSX: LUC), which operates in both Botswana and Canada, has flagged an “ongoing concern” risk despite hitting production records.

All eyes are now on De Beers. Once synonymous with manufactured scarcity and aggressive branding, the company is up for sale. Parent company Anglo American (LON: AAL) has cut its valuation by $4.5 billion in just over a year. No buyers have emerged, but Botswana is reportedly pushing to take a controlling stake. Botswana seeks control of De Beers

Botswana is pushing to take a controlling stake in De Beers as Anglo American (LON: AAL) prepares to divest from the diamond company.

The country’s mining minister Bogolo Kenewendo told the Financial Times on Wednesday that President Duma Boko “remains resolute” in his quest to increase Botswana’s stake in De Beers to ensure Botswana’s full control over this strategic national asset and the entire value chain including marketing.

The comments come ahead of an early August deadline for bids to be submitted to Anglo from potential buyers of the diamonds business.

Kenewendo said any sale of the company “without our support will be difficult to achieve”.

“Our partners at Anglo American have, regrettably, failed to manage the process transparently or in co-ordination with the government and with our support,” she added.

De Beers, the world’s leading diamond producer by value, has been on the chopping block since May 2024, when Anglo announced plans to either sell the unit or launch an initial public offering (IPO). This decision came as part of a corporate overhaul triggered by Anglo’s successful defence against a £39 billion ($49 billion) takeover bid by Australian rival BHP (ASX: BHP).

The miner sources about 70% of its diamonds from the country.

The country’s bold move comes despite a widening budget deficit, expected to hit 7.5% by 2026, and analysts’ skepticism over its ability to raise sufficient funds. Kenewendo, however, insisted that “financing is not an issue.”

Shares of Anglo American rose 0.3% to close at £23.47 apiece in London on Wednesday, valuing the company at £27.6 billion. Strategic asset, market slump

The developments pose a major challenge to Anglo’s “dual-track” strategy of either selling or publicly listing its 85% De Beers stake.

De Beers has struggled amid falling demand from China and growing competition from lab-grown stones. Anglo has twice cut De Beers’ valuation, most recently to $4.1 billion in February. The miner also reported a 44% revenue drop in the first quarter and is holding $2 billion in unsold diamonds.

Anglo said it remains in regular talks with Botswana and acknowledged the country’s role as a key partner.

Lab-grown gems put squeeze on diamond mining industry

Man-made diamonds are 100% carbon, with the same hardness and sparkle of the original.(Stock image: Motortion.)

De Beers, the world’s largest diamond miner by value, once convinced the world that true love needed a mined diamond. The precious stones weren’t just beautiful — they were a natural wonder, formed over billions of years deep within the Earth and extracted from far-off places by companies like De Beers itself.

That mystique guaranteed mine diamonds a century of dominance. Today, that power is fading fast as lab-grown diamonds, identical in structure, sparkle, and hardness, are redefining what a “real” diamond means.

These synthetic gems, created under high pressure and temperature in controlled environments, have gone from novelty to norm. They are widely available and increasingly affordable. And that’s rattling the foundations of a global industry. Alarm bells

The central Chinese province of Henan now produces over 70% of the world’s lab-grown diamonds for jewellery. Many end up on the ring fingers of newly engaged couples, especially in the United States.

In 2022, Walmart began selling lab-made stones. Two years later, they made up half its diamond assortment. Sales surged 175% in 2024 compared to the previous year, making the retail giant the second-largest fine jewellery seller in the country, just behind Signet.

The rapid growth has triggered alarm among some traditional players. Yoram Dvash, president of the World Federation of Diamond Bourses says synthetic diamonds now dominate new US engagement rings. He warned of an “unprecedented flood” of lab-made stones and called on the industry to unite in response.

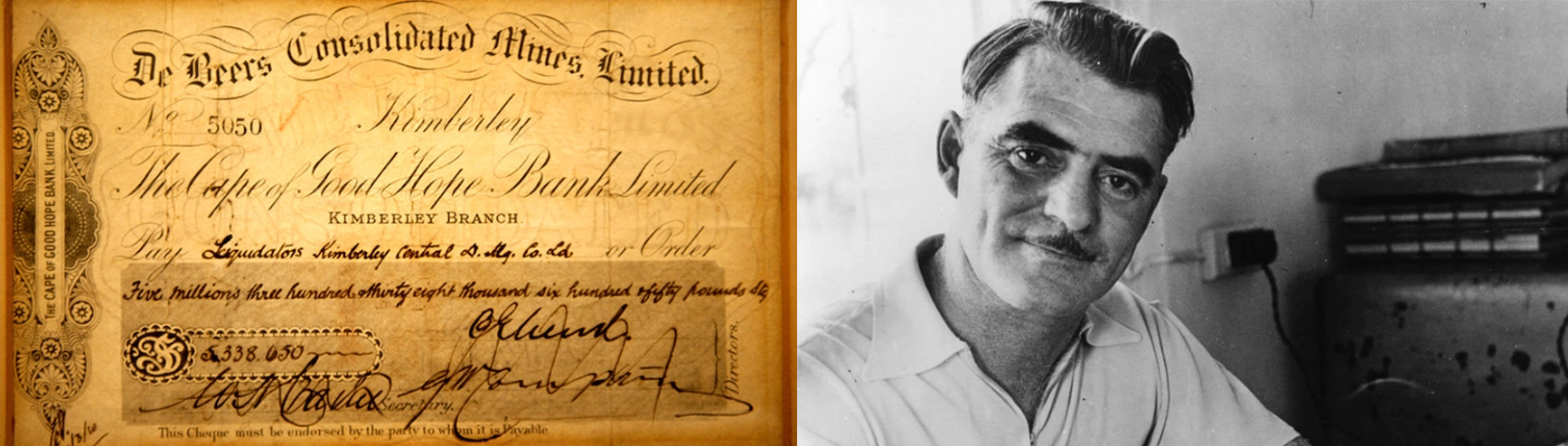

(Click on image to enlarge) LEFT: Competitors Cecil Rhodes and Barny Banato join forces, creating De Beers Consolidated Mines in 1888. | RIGHT: Canadian geologist Dr. John Williamson sets up the Williamson mine in Tanzania, famous for its pink diamonds. (Images courtesy of De Beers Group.)

Not everyone sees an existential threat. Independent analyst Paul Zimnisky attributes the recent downturn to post-covid demand corrections, a luxury slowdown in China, and the disruptive ascent of lab diamonds. He remains cautiously optimistic, noting that lab-grown stones now account for over 20% of global diamond jewellery sales, up from under 1% in 2016.

For engagement rings, the market share is even higher. A 2024 survey of nearly 17,000 US couples by The Knot found that more than half of engagement rings featured a lab-made diamond, up 40% from 2019.

Zimnisky believes the industry’s survival hinges on branding. “If the industry gets lethargic and loses its way on the marketing front, all bets are off,” he told MINING.COM earlier this year.

Marketing reset

The spotlight has shifted back to De Beers. Once the architect of diamond scarcity and prestige, it’s now for sale. Parent company Anglo American (LON: AAL) slashed its valuation by $4.5 billion in just over a year. While no buyer has stepped forward, Botswana is reportedly pushing to take a controlling stake.

De Beers’ troubles go beyond ownership uncertainty. To counter the effects of oversupply and waning demand, the company is mining fewer diamonds. Rough diamond production fell 26% in the first half of the year to 7.22 million carats. Anglo had already slashed its 2025 output forecast to as low as 20 million carats, down from an earlier target of up to 33 million.

In May, De Beers shut down its lab-grown diamond jewellery brand, Lightbox, in a clear move to recommit to natural stones. It’s betting that a focused narrative, one rooted in rarity and romance, can revive demand and stabilize mined diamond prices.

Making that case is harder than ever. Lab-grown diamonds are chemically identical to their natural counterparts. Even trained gemologists need specialized equipment to tell them apart. The core difference now lies not in composition, but in story.

Lab-grown diamonds may be more affordable and visually identical to natural ones, but they typically don’t hold their value. While mined diamonds can resell for 20% to 60% of their original retail price, lab-grown gems often fetch just 10% to 30%, sometimes even less.

In a recent interview with The Wall Street Journal, De Beers CEO Al Cook predicted that as lab-grown diamonds become more abundant, their value will continue to fall. He warned they risk being seen more like low-cost imitations such as cubic zirconia or moissanite, which have different chemical compositions and are easily recognized as fakes.

The Luanda Accord was signed in June to pool resources and boost global marketing efforts for natural diamonds. (Image courtesy of the Natural Diamond Council.)

For buyers who spent thousands on lab-created stones, Cook didn’t sugar-coat the outlook. “I weep for you,” he said.

To sway a younger, more value-conscious generation, the industry has turned to fresh campaigns. De Beers and Signet launched “Worth the Wait” in October 2024, targeting so-called Zillennials — those born between 1993 and 1998 — with messaging about milestones, meaning, and the uniqueness of natural diamonds.

In June, a coalition of producing countries and De Beers inked the Luanda Accord, pledging 1% of rough diamond revenues toward a marketing fund run by the Natural Diamond Council. The NDC has since rolled out a new short film series and an educational website aimed at helping retail staff better articulate the case for natural gems.

A previous campaign that branded lab-made stones as “dupes” and urged buyers to “swipe left” backfired and was taken down. Changing values

Even as traditionalists double down, the cultural ground is shifting. Young buyers care about origin and ethics. They want proof their purchase doesn’t fund conflict or exploit workers. Danish retailer Pandora switched entirely to lab-made diamonds in 2021, citing environmental and social concerns as well as lower prices.

Even experts need specialized equipment to tell the difference between quality lab-grown and mined diamonds. (Image courtesy of the Natural Diamond Council.)

Zimnisky notes that for economies “sensitive” to changes in the diamond market, such as Botswana, Canada, Namibia, Angola and Russia, the stakes are high. “This is a luxury product,” he said. “It needs to be merchandised as such. All stakeholders must contribute to shaping the message.”

The mystique of mined diamonds may be fading, but the desire for something meaningful remains. For the industry to stay relevant, it must shift from legacy to legitimacy, replacing old myths with modern values.

Six university students drown in China mine accident

Six university students drowned on Wednesday while on a field visit to a copper-molybdenum mine in northern China owned by Shanghai-listed Zhongjin Gold Corp, according to a stock exchange filing on Thursday.

The students from Northeastern University in Shenyang fell into a flotation cell – a piece of mining equipment that uses a liquid solution to extract copper from crushed ore – after protective grates collapsed.

A teacher was also hurt in the accident at the mine located in China’s Inner Mongolia region, according to the filing from Zhongjin Gold, a subsidiary of state-owned China National Gold Group Co.

The company said it activated an emergency plan and reported the incident to the relevant departments of the local government.

The operator of the mine, a subsidiary of Zhongjin Gold, halted production, the company said in another stock exchange filing later on Thursday.

Shares of Zhongjin Gold closed down 4.4% on Thursday.

Such field visits have been organized for years and the incident was unexpected, said a teacher from Northeastern University, according to a social media account belonging to Henan Radio and Television.

The university sent staff to the site to manage the incident, the teacher said.

(Reporting by Beijing newsroom; Editing by Raju Gopalakrishnan and Joe Bavier)

Three workers rescued after 60 hours trapped in British Columbia mine

Three workers who were trapped at Newmont’s (NYSE, ASX: NEM)(TSX: NGT) Red Chris mine in northwest British Columbia, Canada, have been safely rescued after more than 60 hours underground.

Newmont said that Kevin Coumbs, Darien Maduke and Jesse Chubaty — contractors for B.C.-based Hy-Tech Drilling — were in “good health and spirits” after being brought to the surface late Thursday night. The rescue followed two significant rockfalls that occurred early Tuesday morning, blocking their exit and later cutting off communication.

“This was a carefully planned and meticulously executed rescue plan,” the company said in a statement.

Newmont said that, before losing contact on Wednesday, the men had confirmed they were in one of the mine’s refuge chambers with steady access to food, water, and air. They were rescued at approximately 10:40 PM local time Thursday (1:40 AM ET Friday), following the complex operation.

Newmont halted all operations at Red Chris during the rescue efforts. The team used drones and a remote-controlled scoop, brought from the company’s Brucejack mine, also in B.C., to clear the massive debris—estimated at 20 to 30 metres long and up to eight metres high.

Newmont credited the successful outcome to “tireless collaboration, technical expertise, and above all, safety and care.”

B.C.’s Mining and Critical Minerals Minister Jagrup Brar said in a post on X he could not describe “the relief we all feel knowing that these three workers are going to be able to go home to their families.”

Red Chris, located about 80 km south of Dease Lake and 1,050 kilometres (652 miles) north of Vancouver, is a joint venture operated by Newmont (70%) and Imperial Metals (30%). The gold-copper mine has been in production since 2015.

A full investigation into the incident is underway.