It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Saturday, December 27, 2025

NUKE NEWZ

WAIT, WHAT?!

US, Russia Allegedly Discuss Nuclear Plant Crypto Mining

Russian media claimed on Friday that the Trump administration held talks with Russia over joint management of Ukraine’s Zaporizhzhia Nuclear Power Plant, including the potential to use its power for crypto mining, Russian newspaper Kommersant has revealed. The discussions, which have not been independently confirmed, were allegedly held without Ukraine’s participation, and likewise proposed resuming electricity supply to Ukraine.

The Zaporizhzhia Nuclear Power Plant is currently not supplying electricity to Ukraine, with its six reactors in cold shutdown since 2022 when Russia invaded Ukraine. However, ZNNP still requires constant external power from Ukraine's grid to cool the reactors and spent fuel, a connection that is frequently lost due to the ongoing conflict.

The plant is under Russian control, and its operations are focused solely on nuclear safety and cooling, relying on emergency generators when the main power lines are cut, which happens often. With a total installed capacity of 5.7 gigawatts (5,700 megawatts), ZNNP is the largest nuclear power plant in Europe. Located in Enerhodar, ZNNP supplied ~20% of Ukraine's electricity.

Ukraine continues to attack Russia’s energy infrastructure with peace talks still ongoing. Ukraine hit a major Russian oil refinery with British Storm Shadow missiles on Thursday.

According to the Ukrainian General Staff, Ukraine hit the Novoshakhtinsk oil refinery in Rostov, one of southern Russia's biggest suppliers of oil products. Located 1,400km (870 miles) from the Ukrainian border, the giant refinery is responsible for supplying jet fuel and diesel to Russian troops fighting in Ukraine.

Last month, a Ukrainian drone strike on an oil-loading facility near Novorossiysk completely stopped exports, affecting 2% of global supply. Ukraine's deep-strike drone campaign targeting Russia's oil and gas production facilities has impacted half of Russia’s major oil and gas facilities and cost its bigger adversary ~10% of its refining capacity, according to industry experts.

"Ten percent, it's not an astonishing number," says Tatiana Mitrova of Columbia University. "But it is still something that starts to be felt with the Russian domestic fuel crisis, with reduced oil refined products exports, and general tension inside the Russian oil sector."

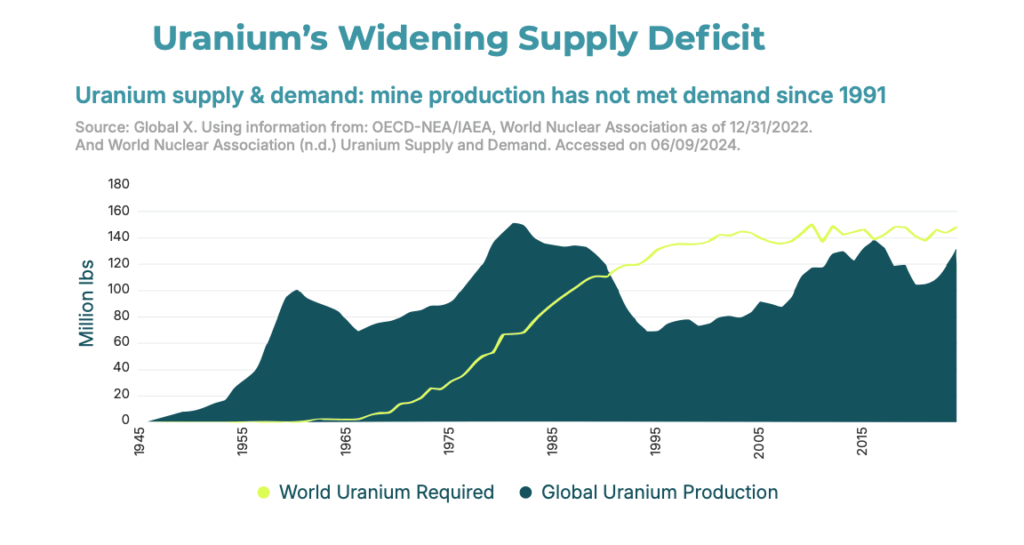

Artificial intelligence is emerging as a major new driver of global electricity demand, reinforcing the investment case for nuclear power and tightening the outlook for uranium markets heading into 2026.

A global investor survey commissioned by Uranium.io shows that the rapid expansion of AI systems and hyperscale data centres is already reshaping long-term expectations for nuclear generation and uranium procurement. Based on responses from more than 600 investors, the study finds that electricity demand linked to AI is increasingly viewed as structural rather than cyclical, at a time when uranium supply is already constrained.

More than 63% of respondents believe AI-related consumption will become a material factor in nuclear planning over the next decade, arguing that traditional demand models underestimate the power needs of large-scale computing. As a result, nuclear energy is gaining renewed attention as a reliable, carbon-free baseload option capable of supporting surging digital infrastructure.

Limited supply relief

That demand signal is colliding with a market facing persistent supply challenges. A majority of surveyed investors expect mined uranium to meet less than 75% of future reactor requirements, citing years of underinvestment, long permitting timelines and declining secondary supplies. Against that backdrop, more than 85% anticipate higher prices into 2026, with many pointing to a $100–$120/lb range and some referencing upside scenarios as high as $135/lb if supply fails to respond.

Sprott Asset Management echoes that view in its latest uranium outlook, describing a market defined by “two speeds”: short-term volatility masking increasingly bullish long-term fundamentals. The firm expects a supply deficit to widen over the coming decade as global mine production continues to lag reactor demand, while utility contracting remains below replacement levels. In Sprott’s assessment, higher prices will be required to incentivize restarts and greenfield developments needed to close the gap.

Despite a choppy 2025, Sprott sees conditions aligning for a catch-up trade in 2026. Long-term uranium prices have begun to move higher, with utilities showing greater willingness to accept elevated contract levels, even as spot prices remain relatively contained. The firm argues that utilities can defer procurement only so long before replacement needs force them back into the market.

Incentives on the rise

Policy momentum is adding another layer of support. Investors surveyed by Uranium.io highlighted planned and proposed nuclear capacity additions across North America, Europe, the Middle East and Asia as key demand signals. Incentives in the US and Canada, Europe’s inclusion of nuclear within sustainable finance frameworks, and state-backed expansion programmes in countries such as China, South Korea and the UAE are reinforcing the role of nuclear in future energy systems.

Taken together, the rise of AI-driven power demand, tightening uranium supply and improving policy support are shifting how investors frame the commodity. Rather than a fuel tied narrowly to reactor build cycles, uranium is increasingly viewed through the lens of energy security and critical infrastructure. For many market participants, that combination points to a structurally stronger uranium market beyond 2026.

Texas Energy Firm Wants to Turn Naval Reactors Into Powerplants

Decommissioned reactors from subs and carriers could power datacenters, according to Bloomberg

U.S. Navy subs have high power-to-weight ratios and long endurance thanks to nuclear propulsion (USN file image)

An American energy company has come up with a novel way to generate nuclear power for civilian uses without the high cost and long timeline of building a new nuclear plant. Texas-based HGP Intelligent Energy LLC wants to reuse a pair of retired naval reactors to generate power for a data center, according to Bloomberg, augmenting the grid with a local and long-lasting source of electricity.

According to HGP, a pair of submarine or aircraft carrier reactors could provide about 500 megawatts of power, which could be used to satisfy the ever-increasing demands of warehouse-sized computing centers. One complete plant would cost about $2 billion, a tiny fraction of the expense of building a new civilian nuclear powerplant.

Newbuild nuclear stations take years to permit and construct because of the perceived risks and the complexity of the task involved, and they require a large and hard-to-find workforce of talented welders and pipefitters. By contrast, HGP thinks that a naval reactor-based powerplant could be up and running by 2029, just four years away.

In operation, the equipment would be intimately familiar to veterans of the U.S. Navy's nuclear propulsion program, the men and women known as "Navy nukes," so the plant operator could hire qualified technicians from day one. Similarly, the supply chain for spare parts has been established for decades.

There is one challenge for scaling: security. American naval reactors run on weapons-grade, high-enriched uranium. If extracted from reactor fuel rods, the 93% uranium-235 fuel could be used to make nuclear weapons, and it is considered a proliferation risk. The reactor technology itself is among the defense establishment's most closely-guarded secrets.

The first plant project, according to a proposal filed with the Energy Department and seen by Bloomberg, would be built at Oak Ridge, Tennessee. The small city is home of Oak Ridge National Lab, the secure facility that helped develop the Navy's first nuclear propulsion reactors and train its first nuclear-qualified officers. ORNL has housed some of the nation's most important nuclear research since World War II, and it is a leading employer of ex-Navy nuclear personnel.

HGP has experience as a grid-scale project developer, having installed 20 sites with battery backup power storage and thermal-power generating capacity for grid resilience. It was among the first battery-backup developers in Texas, and now has nearly two dozen assets in development.

Texas Launches $350 Million Nuclear Energy Initiative

Texas Governor Greg Abbott has congratulated the Texas Legislature for passing House Bill 14, saying it will help revolutionize Texas’ energy sector and cement the state’s role in leading a nuclear power renaissance in the United States.

“Texas is the energy capital of the world, and this legislation will position Texas at the forefront of America’s nuclear renaissance,” said Governor Abbott. “By creating the Texas Advanced Nuclear Energy Office and investing $350 million–the largest national commitment--we will jumpstart next-generation nuclear development and deployment. This initiative will also strengthen Texas’ nuclear manufacturing capacity, rebuild a domestic fuel cycle supply chain, and train the future nuclear workforce. I look forward to signing it into law.”

The U.S. nuclear power sector is seeing renewed momentum as electricity demand rises, particularly from data centers, alongside policy support for carbon-free generation and growing interest in long-duration, firm power. Large technology companies are increasingly positioning themselves around nuclear energy through long-term power contracts, development partnerships, and early-stage investments, marking a shift from decades of limited new nuclear deployment.

Microsoft has signed a 20-year power purchase agreement with Constellation Energy tied to the company’s nuclear generation fleet, as Constellation evaluates the future of assets including the Three Mile Island site in Pennsylvania. Separately, Microsoft is backing nuclear fusion development through its partnership with Helion Energy. Alphabet has partnered with nuclear startup Kairos Power to support the development of small modular reactor technology, with the aim of sourcing power from future reactors expected to come online in the 2030s. Google has also invested in fusion developer TAE Technologies and early-stage fission company Elemental Power.

Meta Platforms has also signed a 20-year agreement with Constellation Energy for electricity from an existing nuclear reactor in Illinois and has issued a request for proposals seeking 1–4 gigawatts of new nuclear capacity in the United States. Meanwhile, TerraPower, founded and backed by Microsoft co-founder Bill Gates, is developing a sodium-cooled fast reactor, with a demonstration project underway in Wyoming. Oklo, backed by OpenAI chief executive Sam Altman, is developing small-scale nuclear reactors aimed at supplying power to data centers, with the company targeting initial deployment later this decade, subject to regulatory approval.

North Korean dictator Kim Jong Un has unveiled the completed hull of what his government claims to be its first nuclear-powered submarine.

To date, North Korea's submarine fleet has consisted of Soviet-era conventionally powered attack subs, which have comparatively limited capability in a modern context. North Korea also commissioned a conventionally-powered ballistic missile sub, the Yongung, in the 2010s and used it to test-fire a sub-launched ballistic missile in 2016. A second ballistic missile sub crafted out of a modified 1960s-era Romeo-class attack sub was spotted in 2019.

The new nuclear-powered, nuclear-armed ballistic missile sub has been under construction for some time, and its completed hull was first unveiled on Christmas Day. It is likely near to being fully outfitted, ex-submariner and analyst Moon Keun-Sik of Hanyang University told AP. Ballistic missile launch trials may still be some years off, given the challenges of bringing a first-in-class sub into operation and training a naval reactor crew.

North Korea is capable of producing its own nuclear fuel, nuclear weapons and ballistic missiles. Its access to naval reactor technology is less certain, as is the functionality of the vessel that Kim revealed on December 25. If it is a functional vessel, speculation has circulated about whether Russia could have supplied technical assistance for the North Korean reactor program - or even a complete reactor.

Some form of a military-to-military trade between Russia and the North is likely: Kim supplied 10,000 North Korean infantry troops to assist Russian military operations against Ukraine in 2024, and the force sustained heavy losses before being ultimately withdrawn. The North has also provided Russia with hundreds of thousands of rounds of howitzer ammunition, sustaining Russian artillery units for the war.

In unveiling the new sub, Kim also criticized South Korea's plans to build the same type of equipment. In a statement carried by state media, he called the newly-announced joint U.S.-South Korean nuclear attack sub development program an "aggressive act that seriously infringes on national safety and maritime sovereignty that must be countered," and said that North Korea would "further accelerate" its nuclear-navy program in response.

Experts Question Russia's Ability and Desire to Attack NATO

Senior European officials, including NATO chief Mark Rutte and top German and Polish generals, have issued frequent and serious warnings in 2025 about the possibility of a direct conflict with Russia.

Skeptics argue that Russia's inability to subdue Ukraine and the lack of concrete evidence for an immediate attack suggest these warnings may be used to push NATO members to meet defense spending commitments or gain political leverage.

The long-term risk of a military provocation is considered likely, especially if the war in Ukraine freezes, though the timeline for a full-scale attack on a NATO member like Estonia is debated, ranging from the near future to 5-10 years away.

The polite applause faded and NATO chief Mark Rutte arranged his papers neatly on the rostrum. It took him 62 seconds to get to the point.

“The dark forces of oppression are on the march again,” he said. “We are Russia’s next target.”

Rutte’s speech in Berlin on December 11 was just the latest in an unprecedented series of warnings of direct conflict with Russia made in 2025 by senior European officials and intelligence agencies.

In February, Danish intelligence said “Russia sees itself in conflict with the West and is preparing for a war against NATO;” in June, Germany’s top general said an attack may come within four years; in November, his words were echoed by his Polish counterpart -- two days after German Defense Minister Boris Pistorius said “some military historians even believe we have already had our last summer of peace.”

This list of warnings is far from exhaustive. Rutte has been most frequent.

In January, he urged NATO members to hike defense spending or get Russian language classes, while in June he said an attack could be coordinated with a Chinese assault on Taiwan.

His December 11 speech was his loudest alarm bell yet, speaking of “the scale of war our grandparents or great-grandparents endured” with “mass mobilization, millions displaced.”

What's Behind The Warnings?

The frequent comments have made headlines -- and raised question marks, especially with the United States showing waning interest in maintaining the levels of security support it has given Europe in the past.

“This is something that I’ve been pondering especially as there is no evidence at all that Russia can or wants to attack NATO,” John Foreman, a former British military attache in Moscow and Kyiv, told RFE/RL.

“I think a number of politicians and military types are using the specter of the Russian threat for more prosaic reasons: Rutte to encourage NATO nations to meet their spending commitments. The Poles to get more NATO on their territory,” he added.

Other skeptics have pointed out that after nearly four years of war Russia has been unable to subdue Ukraine -- even if it has been edging forward this year at enormous cost in casualties and equipment.

Teemu Tammikko, from the Finnish Institute of International Affairs, also said that Russia did not appear “willing and able to attack NATO for the moment.”

But he told RFE/RL’s Russian Service that President Vladimir Putin’s grip on power was “dependent on an external threat,” meaning “in the longer term, some kind of direct military provocation is likely, especially if the war in Ukraine freezes.”

Some argue this is already happening, such as with Russian drone and air incursions into NATO airspace. But the warnings issued this year hint at much darker scenarios.

Attack On Estonia

A paper issued by the European Council on Foreign Relations (ECFR) on December 18 focuses on fears of a direct attack on Estonia to test the willingness of the United States and other NATO allies to fight.

“In Europe, this anxiety sits atop a deeper fear: that the American government, distracted by domestic politics and tempted by retrenchment, might soon reduce its presence or attach conditions to its role in Europe’s defense,” it says.

Describing Estonia as “small, flat, and exposed,” the report says a 2016 wargame predicted Russian forces could seize the capital within 60 hours of an invasion.

But it also says that Russia would need 5-10 years after the end of the war in Ukraine “to refit and rearm for such an attack” -- a much longer timeframe than those posited by Rutte, Pistorius, and others.

It’s notable that US officials have not repeated European warnings.

The recently released National Security Strategy argues that “European allies enjoy a significant hard power advantage over Russia by almost every measure, save nuclear weapons.”

But it also acknowledges the need for US diplomatic engagement “to mitigate the risk of conflict between Russia and European states.”

'Warmongers'

Kremlin officials have denounced European leaders as “warmongers” and denied any desire to attack. They were making similar comments about Ukraine on the eve of their full-scale invasion in February 2022, though this does not automatically mean there are plans for further aggression.

“Russia is not pursuing the military goals attributed to our country,” Deputy Foreign Minister Sergei Ryabkov said on December 22. “As the President of Russia has already said, we are even prepared to guarantee this legally as part of a settlement” of the war in Ukraine, he added.

But any such commitment would be unlikely to be taken seriously by many in the West. Russia also signed and then broke promises to respect Ukraine’s borders in the 1994 Budapest Memorandum.

Ultimately, it may all depend on one man.

“As we know, Russia is not a democracy. Such a decision would essentially just be a result of Vladimir Putin deciding that he wanted to attack a European country which is a NATO member state, or another European country, so we just have no way of knowing,” Elizabeth Braw, of the RUSI defense and security think tank, told RFE/RL’s Russian Service.

“That's why you see military leaders all over Europe saying we have to be prepared for something to happen tomorrow. It may happen five years, 10 years from now or never, but you can't bank on it.”

By RFE/RL

Vessels Damaged as Russia Intensifies Attacks on Ukraine’s Ports

A ship and a barge were damaged during the latest attack on Odesa (Oleksiy Kuleba on Telegram)

Russia appears to be intensifying its assault on the Black Sea ports of Ukraine. The relentless barrage continued for a second night at the Port of Odesa with reports of damage to multiple vessels and port infrastructure.

Ukraine says the attack consisted of 99 drones and one ballistic missile. They reported shooting down or jamming 73 of the drones, but 26 struck 16 locations in Ukraine.

It was the second consecutive night of strikes in Odesa, causing damage to administrative buildings, grain elevators, other equipment, and warehouses. A cargo ship registered in Palau and a barge owned by Slovakian interests were both reported damaged in the port. The barge named Majestic, the Slovakian officials said, had been damaged in a previous attack and was no longer seaworthy. No Slovakians were aboard the vessel, they reported.

Ukraine said there were no injuries from the latest attack. The previous night, one person was killed, and two others were injured.

(Oleksii Kuleba photo)

The officials asserted that Russia has escalated the attacks on the region after vowing to cut off Ukraine from the Black Sea after the attacks on the oil tankers. The Ukrainians assert that Russia is deliberately destroying energy and civilian infrastructure, leaving people without power, water, and heating amidst the cold winter temperatures. They assert that Russia has increased its focus on destroying logistics through the seaport attacks, aiming at the Ukrainian economy and food security.

Beyond Odesa, there were reports of strikes in the Izmail district that also damaged port infrastructure.

A drone strike on the terminal at Mykolaiv region damaged a vessel registered in Liberia.

Ukrainian officials said efforts were underway to restore the damage to the power system. Port workers are reported to be surveying the extent of the damage.

National Oil Companies Quietly Set The Pace For The Next Decade

National oil companies are increasingly setting the pace in global energy investment, outspending majors, locking up long-life assets, and taking control of future supply.

Listed oil companies face tighter capital discipline and shareholder constraints.

North America has become the de-risking hub for foreign NOCs, especially in U.S. gas, LNG, and petrochemicals, offering stable cash flows and regulatory certainty

The prevailing structural theme right now is that national oil companies (NOCs), in some cases and across some segments, are moving faster than the majors, outspending them, beating them in locking up supply chains, and building cash cows faster for the future. You can see it directly in upstream spending trends highlighted by the IEA Oil 2025 report, and the money is shifting this way because the NOCs have political backing, lower lifting costs, and much clearer mandates than the big listed companies.

Wood Mackenzie has warned that tighter capital conditions are forcing oil and gas companies to become more selective in business development. Neivan Boroujerdi has said this will require a more nimble and creative approach as budgets tighten. In practice, that environment favors national oil companies with the balance sheets and mandates to secure gas, chemicals, and integrated assets early, rather than defer decisions. This is no longer hypothetical. Capital is already moving in that direction.

Similarly, OPEC’s latest medium-term outlook assumes that most incremental supply growth will come from countries with state-backed producers and low-cost reserves, suggesting we will be relying on NOCs for more long-cycle investment through the decade. Rystad Energy’s recent upstream and LNG analysis shows that the majority of newly sanctioned long-life projects are either led by NOCs or depend on them as anchor partners, while IOC capital remains concentrated in shorter-cycle or brownfield work. The IEA has also been explicit that future supply security hinges on investment decisions by national producers willing to commit capital beyond typical shareholder-return horizons.

Combined, these views indicate that capacity growth and control over future supply are increasingly being set by national companies rather than listed majors.

Asia: Adding Gas, Chemicals and Transition Materials Asia’s NOCs are not easing off hydrocarbons, but they’re tightening their grip on those parts of the supply chain that will matter most over the next decade: gas, chemicals, metals and trading. PetroChina is a case in point: It has been pulling more capital toward downstream and gas while upgrading refineries for higher-margin products, as reported by Caixin.

The LNG side of things tells a similar story. PetroChina has been layering long-term supply deals into the 2030s, according to China Daily, and then diversifying away from spot exposure with new procurement corridors.

And while Western outlets fixate on earnings, Asian media have been quicker to catch the shift into transition materials. The South China Morning Post (SCMP) notes that PetroChina wants exposure to the upstream of electrification just as much as it wants downstream oil and gas. It’s not really a transition as much as it is a hedge. They’re going for whatever powers Asian industry next.

China’s Sinopec is doing something similar, but the strategy is chemicals-heavy. As fuel demand flattens, Sinopec is putting more capital into petrochemicals, hydrogen, and CCUS. It’s also doubling down on long-term LNG to feed industrial boilers and heavy manufacturing that fall under its new policy mandates. The bigger refining margins in 2025 gave them the power to do this, according to SCMP.

CNOOC, as an outlier, is staying the course, focusing on upstream and LNG, but looking to scale both. Offshore output is rising again with new South China Sea projects being added on, and the company is buying into LNG projects up the chain rather than staying a pure buyer. The goal is straightforward: control more of the gas it needs for its power and industrial clients rather than relying on the spot market.

Petronas is expanding its LNG position and lining up more supply from projects in the Atlantic and Indian basins. At home, it is spending on gas, CCS, hydrogen and midstream work that supports the domestic power system.

India’s ONGC is adding to its overseas portfolio and increasing its access to gas. The Economic Times reports that ONGC Videsh has raised its spending outside India, and state buyers are now coordinating long term LNG procurement.

Across the region, NOCs are concentrating on the areas that support their revenue base: gas supply, refining output, chemicals and firm access to transport routes. They are securing these positions now while the opportunity is still visible.

Middle East / Gulf: Expanding Capacity and Integration

Gulf NOCs are expanding low-cost supply and increasing their integration across refining, petrochemicals and LNG.

Middle Eastern NOCs continue to take a larger share of global upstream spending, according to the IEA’s 2025 investment report. Global upstream totals are largely flat, but the region’s state producers are still increasing outlays. Most of this capital is going into long-life capacity and integrated projects rather than short-cycle additions, consistent with their role as the lowest-cost suppliers in the system.

ADNOC’s investment arm XRG has outlined the largest expansion plan in the region. It is targeting 20 to 25 million tonnes a year of gas and LNG capacity by 2035 and is adding assets in North American gas to support that target. Reuters reporting also shows ADNOC is moving its existing U.S. holdings into XRG and positioning the unit to lead further international gas and LNG deals, including in North America.

What we know for certain: ADNOC wants a larger operational and financial position in North American gas.

QatarEnergy is expanding LNG output through the North Field program and using longer-term contracts to secure demand in Europe and Asia. Based on public statements from the energy minister, Qatar expects tighter LNG balances later in the decade.

Finally, Saudi Aramco, the NOC that gets the most headline attention, is tying together upstream, downstream, gas and “new energies” into one roaring machine. Recent agreements in the United States on LNG, technology and services show Aramco placing capital directly inside key consuming markets.

The overriding Gulf strategy? Outspend everyone, integrate everything, and get as close to the customer as possible.

Latin America: Holding Output and Preserving Cash

Latin America’s state producers are trying to hold production steady while managing tight budgets and a very mixed bag of political situations.

Petrobras has more room than the others. The Brazilian NOC’s 2026 to 2030 plan shows lower headline capital spending, but the company still intends to grow pre-salt output and keep most of its money in projects that are already under way. Company filings confirm about $109 billion in planned investment, with roughly $91 billion already committed. The plan is to keep the pre-salt program moving along, avoid expensive frontier work, and only allocate to gas, chemicals and lower carbon projects once the core fields are covered.

Ecopetrol, of Colombia, is trying to build a broader base. Its public strategy documents outline a larger role for transmission, solar and wind along with the oil and gas business. The ISA unit already delivers steady money, and the company wants that share to rise. The changes are meant to give Ecopetrol more stable earnings while it manages slower growth in upstream oil.

Mexico’s Pemex, Venezuela’s PDVSA and Argentina’s YPF face constraints that limit their options. Debt, field decline and political pressure shape most of their decisions. Pemex remains the most indebted energy company in the world despite government support and debt operations, with falling output still a concern. PDVSA’s exports and operations remain heavily shaped by U.S. sanctions, payment problems and the structure of swap deals with foreign partners. YPF is under pressure from higher costs, rising debt and adverse court rulings, and has reported recent quarterly losses. Across all three, the priority is to keep existing production from falling faster and to maintain enough progress on power or lower carbon projects, where applicable, to preserve financing and political backing.

Africa: Building Control While Managing Risk

Africa has real upside. The hard part is getting projects funded and delivered on schedule.

A Bloomberg investigation showed how large discoveries across the continent have brought in less local economic benefit than expected, which has led several governments to push their national companies to take more control.

Nigeria’s NNPC is the one pushing volume. Guardian Nigeria reported NNPC Exploration and Production reaching about 355,000 barrels a day, the highest level in more than 30 years. And now the NNPC has a new chief, with a new mandate: lift output and get the domestic refining system working.

Mozambique,Senegal, Ghana and Uganda are banking on gas. Their LNG and integrated gas projects are the only near term path to new export income at scale. The payoff depends on construction staying on schedule and on governments holding meaningful equity rather than sliding back into arrangements where most of the value lies with outside operators.

Across the region, governments want their national companies to move from passive royalty collectors to active operators, but there is plenty of execution risk here.

North America: The Market NOCs Use to De-Risk

North America is not building a national oil company, but it is building something else: a federal-backed critical-minerals base. The Trump administration has been taking equity positions in rare earth and battery-metal supply chains, buying into private and public companies to secure domestic production. On the hydrocarbon side, the region has become the place where foreign NOCs go to balance their portfolios.

ADNOC’s use of XRG, as mentioned above, makes the intent clear. Gulf producers want a bigger position in U.S. gas, LNG and petrochemicals, and they are using XRG to buy the exposure. Equity in LNG trains, chemical complexes on the Gulf Coast and related midstream is now being treated as core to their ten-year plan.

On the Asian side, PetroChina is moving into transition materials. It wants to operate across the industrial supply chain, not just in crude and products.

Wood Mackenzie’s public outlooks point to a busy upstream M&A cycle, with several state-owned producers listed among the likely active buyers. Their U.S. gas and LNG notes also underline that North America remains one of the most stable regions for long-life assets, with deep capital pools and clear operating rules. That combination makes the U.S. a practical place for foreign NOCs to take positions, even if Wood Mackenzie does not explicitly describe this as a dedicated NOC strategy.

North America is the hedge, then. It is the one market where NOCs can diversify risk and attach themselves to cash flow that holds up in volatile cycles.

The map for the next decade is fairly easy to follow. Asia’s national companies are keeping oil and gas at the center while adding metals, LNG and trading positions. The Gulf producers are putting money into long-life supply and deeper integration. Latin America is leaning on pre-salt output and transmission assets to keep their budgets steady. Africa is trying to capture more value by taking a larger operating role in its own projects. North America is where foreign NOCs place capital to stabilize returns and broaden their portfolios.

Enriched uranium billet. (Stock image by RHJ)

Enriched uranium billet. (Stock image by RHJ)