It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Wednesday, November 05, 2025

How Energy Providers Can Capitalize on Data Center Growth

By Rystad Energy - Nov 04, 2025, 3:00 PM CSTThe rapid growth of artificial intelligence and digital infrastructure has made data centers the leading cause of new electricity demand in North America, creating a race for grid operators and policymakers to keep pace.The energy industry can address three key challenges for data centers: capacity bottlenecks by deploying flexible power solutions, grid stability by providing "stability as a service," and cost pressures by offering integrated on-site solutions.Energy companies that deliver quick, innovative, and cost-effective solutions will benefit most from this evolving power landscape, with carbon capture, storage, and renewable integration being crucial for sustainable growth.

The surge in artificial intelligence and digital infrastructure has turned data centers into the fastest-growing source of new electricity demand in North America. Grid operators and policymakers are racing to keep up, and for energy providers, this wave of demand could open new frontiers of opportunity.

Challenge 1: Capacity bottlenecks

Data center developers are demanding power within tight timelines, while interconnection queues for new generation and transmission projects can stretch for years. Some operators are now building private substations or developing on-site generation to accelerate delivery. For energy providers, the need for speed is creating opportunities to deploy flexible and rapidly scalable power solutions such as gas turbines, reciprocating engines and energy storage.

Challenge 2: Grid stability

Data centers are highly sensitive to even small voltage fluctuations, and recent incidents have already triggered large load losses. Regulators are tightening reliability rules, while the industry is investing in ride-through technology and on-site grid equipment. This opens a new opportunity for "stability as a service", where energy players supply not only power but reliability.

Challenge 3: Cost pressures

As utilities expand networks to meet surging demand, the cost of new infrastructure is putting pressure on electricity prices for all customer classes. Policymakers are exploring new cost-recovery models to protect consumers, but large power users are already taking action by moving behind-the-meter to control costs and improve price certainty. For energy providers, this shift creates demand for integrated, on-site solutions that balance reliability, cost and sustainability.

Data center growth is reshaping North America’s power landscape faster than grid and policy systems can adapt. Energy companies that deliver quick, innovative and cost-effective solutions will benefit most. Over time, carbon capture, storage and renewable integration will be key to sustaining this growth in a decarbonizing world.

Economists and politicians often assume continuous growth, ignoring the possibility of decline, which can lead to unrealistic promises and economic instability.

The period of low oil prices between World War II and 1973 fostered an unsustainable economic model, leading to debt bubbles when energy supplies became more constrained.

Historical secular cycles and the concept of "Stagflation" suggest that when populations exceed carrying capacity, wage disparity and debt increase, potentially leading to societal collapse.

Economists, actuaries, and others tend to make forecasts as if whatever current situation exists will continue indefinitely or will perhaps improve a bit. No one wants to consider the possibility that things will somehow change for the worse. Politicians want to get re-elected. University presidents want their students to believe that their degrees will be truly useful in the future. Absolutely no one wants to hear unfavorable predictions.

The issue I see is that many promises were made during the period between the end of World War II and 1973, when oil prices were very low, and most people assumed that oil supply could grow endlessly. No one stopped to think that this was a temporary situation that likely could not be repeated. If things didn’t work out as planned, debt bubbles could bring down the economy. This was a heading I used in my talk at the recent Minnesota Degrowth Summit:

Figure 1. Text: Our economy has been built as if a growing supply of $20 oil (EROI of 50 – 100) would continue! Simply add more debt if this isn’t true.

In this post, I will provide a few highlights from my recent talk. I also provide a link to a PDF of my Degrowth Summit talk and a link to a Vimeo recording of the summit, which includes a transcript. To access the transcript and an outline of the timings of the various talks, scroll down on the front page of the recording. Joseph Tainter spoke first; there was a recorded section showing clips by other speakers that only online viewers saw, and I spoke last (starting at about 1:55 on the video).

– – – – – – – – – – – – – – – – – –

Between 1920 and 1970, US oil supply grew rapidly. The early oil was easy to extract and close to customers wanting to purchase it. There had been warnings from physicists (including, most notably, M. King Hubbert) that this could not go on indefinitely, but most people assumed that any obstacles were far in the future.

Figure 2

Of course, there were other countries producing oil besides the US at that time, so it was possible to purchase imported oil. The US still had some oil it could produce, but it tended to require more complex operations. For example, some of the oil was in Alaska. Bringing this oil to market required working in a cold climate, laying a long pipeline, and using ships to transport the oil to locations with refineries.

Low oil prices were very beneficial to the economy, for as long as they lasted.

Figure 3

We don’t appreciate how important low-cost food is to our personal finances. If food purchases amounts to, say, 50% of available income, necessities such as clothing and housing would take nearly all our income. There would be little left over for optional items. On the other hand, if purchases of food require only 5% to 10% of available pay, there would much more likely be money left over for discretionary purchases, such as buying a vehicle or paying for school tuition for a child.

Oil and other energy products are like food for the economy. During the period when oil prices were very low, there was sufficient margin for purchasing all kinds of “extras,” such as the items listed in Figure 4 below.

Figure 4

In the low-priced oil era, small businesses were sufficient for many types of operations. There was little need for a deep organizational hierarchy, or for advanced energy-saving versions of manufactured devices. Most goods used in the US were made in the US.

Figure 5

Once the economy started to need more complexity, things began to change.

Figure 6

The economy needs a strong middle class to maintain the buying power needed to purchase goods such as vehicles, motorcycles, and new homes, to keep the price of oil up. If the middle class starts to disappear, or if young people start earning less than their parents did at the same age (adjusted for inflation), then it becomes difficult to keep the prices of oil and other energy products up. Prices must be both high enough for producers and low enough for consumers.

Figure 7

Recessions took place when oil prices rose. Governments found that they needed to bail out their economies with more debt when oil prices rose. Since 2008, the ratio of US debt to GDP has skyrocketed. Quite a bit of the added debt has been to pay for programs for poor people and the elderly.

Figure 8. Chart by the Federal Reserve Bank of St. Louis, showing the ratio of US public debt to GDP. The ratios would have been even higher if internal debt, such as debt owed to pay for Social Security benefits, were included.

The current level of debt of the US government is widely viewed as being too high. One analysis suggests that if the ratio of government debt to GDP exceeds 90%, economic growth is inhibited. The US debt to GDP ratio is now 120% on the basis shown, which is well above the 90% threshold. One concern is that interest payments on debt already exceed the amount the US spends on defense each year. Taxes need to rise, simply to pay the interest on the debt.

Growing debt, particularly during the Stagflation Stage, is one of the issues mentioned by researchers into so-called secular cycles, which are long-term cycles that take centuries to complete. In the book Secular Cycles by Peter Turchin and Sergey Nefedov, a group of people somehow obtain possession of an area of land (often by cutting down trees or winning a war) that allows the population of the group to temporarily surge. When the population reaches the carrying capacity of the area, population growth greatly slows in a period referred to as Stagflation. Wage and wealth disparity become more of a problem, as does debt.

Eventually, according to Turchin and Nefedof’s study examining eight societies, populations tended to collapse over long periods, ranging from 20 to 50 years. Such cycles are closely related to the periods of growth and collapse analyzed in Prof. Joseph Tainter’s book, “The Collapse of Complex Societies.”

Figure 9. This chart is my chart, using information from the book Secular Cycles. The extent of the decline of the in population during the Crisis Period is quite variable.

The time ahead looks worrying, if my analysis is correct.

Figure 10Figure 11Figure 12

A few comments for my regular readers:

My presentation included 51 slides. Look at the PDF to see the full presentation.

Even though I didn’t mention it, having a rapidly growing energy supply at a very high EROI would not be sufficient to forestall collapse indefinitely. Other issues would emerge. Population would rise higher, and pollution would be more of a problem. Eventually, the system would still reach a limit and tend to collapse.

I only included EROI because I thought a few people would already be aware of the concept. I didn’t define it or talk about it.

My analysis seems to suggest that extenders of fossil fuels, such as wind, solar, and nuclear, need to have very high EROIs. But even with high EROIs, they are unlikely to be helpful for very long because the system would still tend to reach its limits.

The new government's Climate Competitiveness Strategy, outlined in Budget 2025, will prioritize effective carbon markets, enhanced methane regulations, and technologies such as carbon capture and storage as the primary means to reduce oil and gas emissions.Canada’s federal government is signaling it plans to scrap the previous cabinet’s controversial emissions cap plan, which had put former PM Justin Trudeau on a collision course with the provincial government of oil-producing Alberta.

The former government of Justin Trudeau last year proposed regulations to set a cap on greenhouse gas pollution within the oil and gas sector and have companies reduce emissions by 35% compared to 2019 levels.

Alberta and its oil and gas industry have argued that the emissions cap is basically a cap on oil and gas production as companies are required to either invest a lot of money to make production cleaner, or simply cut production to comply with the emissions cap.

“This cap is not actually about emissions. This is about the federal government wanting to cut oil and gas production and control our energy sector, even if it costs thousands of jobs and hurts Canadians from coast to coast,” Rebecca Schulz, Alberta’s Minister of Environment and Protected Areas, said last year.

Now Mark Carney’s new federal government has introduced an update on the Oil and Gas Emissions Cap in the just-unveiled budget 2025 plan, saying that it would prioritize the creation of effective carbon markets.

The new government’s Climate Competitiveness Strategy in Budget 2025 acknowledges the need to reduce emissions from the oil and gas sector to ensure Canada has access to markets that prioritize sustainability.

Carney’s climate strategy is “based on driving investment, not on prohibitions, and on results, not objectives,” the plan says.

“Effective carbon markets, enhanced oil and gas methane regulations, and the deployment at scale of technologies such as carbon capture and storage would create the circumstances whereby the oil and gas emissions cap would no longer be required as it would have marginal value in reducing emissions,” according to the budget plan.

Norway has temporarily suspended the ethical investment rules for its $2.1-trillion oil fund, the Government Pension Fund Global (GPFG), to prevent the forced sale of significant stakes in big tech companies such to Microsoft, Alphabet, and Amazon.

The Finance Ministry states the suspension is an emergency measure necessary to protect the stability of the fund’s portfolio and maintain the fiscal framework, which relies on the fund's returns to support roughly one-quarter of Norway’s annual budget.

The move follows an earlier plan to boost spending from the oil fund in 2026 due to declining offshore production, and the combined policy shifts suggest an attempt to stabilize returns amid criticism from economists and lawmakers about prioritizing short-term performance over ethical principles.

Norway has suspended the ethical investment rules governing its $2.1-trillion oil fund just weeks after signaling higher 2026 withdrawals, drawing a direct line between petroleum revenues and fiscal control. The Government Pension Fund Global (GPFG) move, as detailed by the Irish Times, is being described as an emergency measure to prevent forced equity sales that could shake global markets.

Parliament has approved a temporary freeze on the fund’s Ethics Council, suspending new exclusion recommendations on human-rights and environmental grounds, according to Reuters. The Finance Ministry warned that maintaining the current rules risked triggering the sale of multi-billion-dollar positions in Microsoft, Alphabet, and Amazon, which collectively represent around 15% of the GPFG’s total equity exposure.

Finance Minister Jens Stoltenberg said the suspension was necessary to protect portfolio stability and the fiscal framework that depends on it. The fund contributes roughly one-quarter of Norway’s annual budget through returns generated from oil and gas revenues managed by Equinor and the State’s Direct Financial Interest scheme, as noted by the Financial Times.

The move builds on an October plan to boost spending from the oil fund in 2026, unveiled in response to slowing offshore production and softer gas export receipts. At that time, the government said it expected to lift withdrawals above the long-standing fiscal rule of 3% of fund value, citing energy-transition projects and social spending pressures.

That announcement drew criticism from economists who warned that expanding reliance on fund income risked undermining its long-term buffer role.

Combined, the two policy shifts suggest the Fund’s attempt to stabilize returns at a time of declining offshore revenues, weaker North Sea investment, and volatile gas prices that are tightening the screw.

Lawmakers from the Labour and Green parties have questioned whether the government is prioritizing short-term portfolio performance over the fund’s founding principles of ethical accountability and intergenerational equity.

Norway’s Finance Ministry said the suspension would remain in place until a review of the Ethics Council’s framework concludes, likely in late 2026.

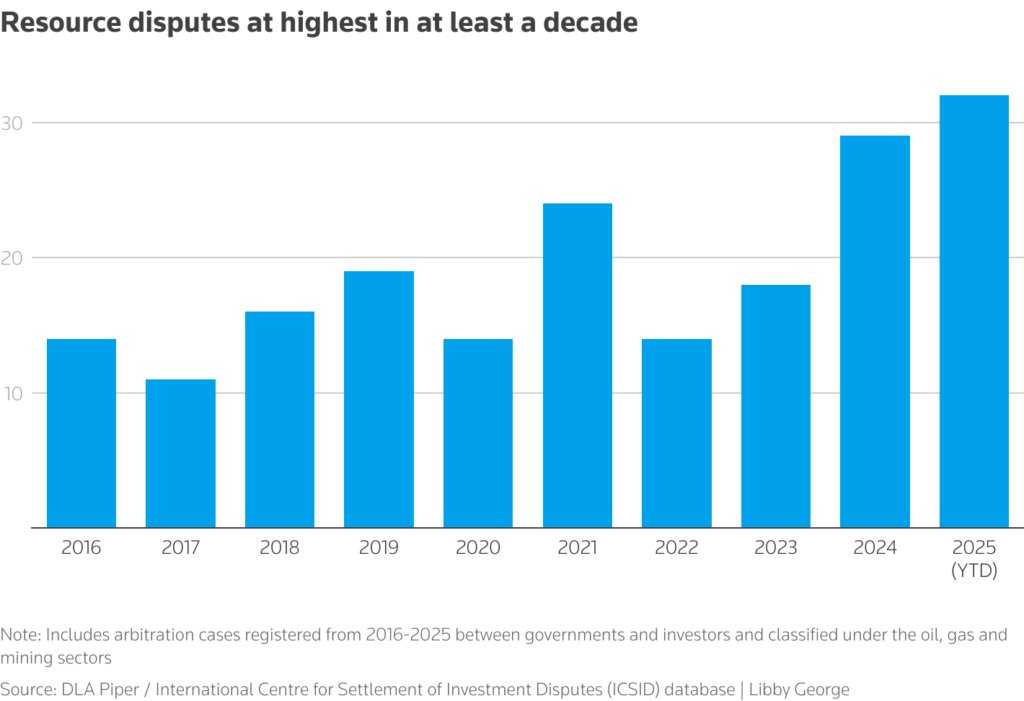

Disagreements between governments and investors over resources are at a 10-year high, law firm DLA Piper said, driven by resource nationalism and growing competition between the US and China for critical minerals.

This reflects the scramble for minerals that will power everything from chips for the AI boom, to electric vehicles, to the valuable oil and gas revenues critical to state coffers, particularly in emerging economies.

The 32 disputes lodged so far in 2025 with the World Bank arbitration body, over everything from oil and gas to gold, uranium and lithium, had already exceeded last year’s total, DLA Piper said.

“As their value has become more apparent, states have felt the need to exert greater control over any deposits of critical minerals within their borders,” said Gabriela Alvarez-Avila, a DLA Piper partner and co-leader of international arbitration.

Of the cases, 17 related to oil and gas assets, DLA Piper’s analysis of the International Centre for Settlement of Investment Disputes (ICSID) database showed.

The largest number of disputes, 11 in total, have been in Latin America, while Colombia, with four of those cases, is the single largest.

Colombian President Gustavo Petro last year designated several mining areas as temporary natural reserves, banned fracking and threatened to block coal exports to Israel, creating tension with some investors.

DLA Piper did not break down the specific disputes.

Africa, which has large reserves of critical minerals, has 10 disputes, which involved Niger, Tanzania, the Democratic Republic of Congo, Mali, Morocco and Senegal.

The DRC is home to a range of critical minerals including cobalt, copper, lithium and manganese – a target for many countries and investors.

The United States in particular has said it is open to exploring critical minerals partnerships in the DRC after a Congolese senator contacted US officials to pitch a minerals-for-security deal.

Australia-based AVZ Minerals said in July a new deal between Kinshasa and US-backed KoBold Metals to develop part of a lithium project breached an international arbitration order.

Most of the remainder of the disputes identified by DLA Piper’s research were in Europe and Central Asia.

(By Libby George; Editing by Amanda Cooper and Alexander Smith)

Investors call for creation of International Minerals Agency

A group of investors in mining called on Monday for the creation of an independent agency for the sector modelled after the International Energy Agency.

The group of investors, which together manage or advise on $18 trillion of assets, said the new International Minerals Agency would be able to monitor global mineral supply and demand as well as illegal flows, a statement said.

The agency would also provide data about which companies are progressing toward global performance standards on sustainability, it added.

The group of investors – the Global Investor Commission on Mining 2030 – includes PIMCO, ING, L&G, Allianz Investment Management, Church of England Pension Fund and Royal London Asset Management.

It released a report in Sao Paulo, aiming to provide a 10-year blueprint for a responsible mining sector, ahead of United Nations climate negotiations, having met with President Luiz Inacio Lula da Silva of Brazil.

“The Commission’s vision offers a roadmap for investors to unlock value by promoting sustainability and improving public perception,” said Peter Kindt, global head transition accelerator at ING.

“Achieving this will require multi-stakeholder collaboration and new initiatives like an International Minerals Agency.”