It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Sunday, November 09, 2025

Can North America Unite Against China’s Energy Dominance?

The Atlantic Council urges deeper U.S.-Mexico-Canada cooperation to counter China’s dominance in global energy value chains.

Mexico’s “Plan Mexico” outlines major ambitions in manufacturing, minerals, and energy that align with regional nearshoring goals.

Strengthened North American integration could transform energy abundance into a geopolitical advantage while securing regional supply chains.

The United States-Mexico-Canada Agreement (USMCA) is up for review in 2026, and the resulting policy outcome could have transformational importance for global energy markets and value chains. Even though it would seem that the United States, Mexico, and Canada are in an era of increasing political tension and division, the common strategic priorities of the North American bloc far overshadow the divergences and competing interests. Strengthening energy trade and mutual support to ramp up energy production and localized energy and manufacturing supply chains would be a win-win-win for all three parties, but will require a particularly heavy lift on the part of Mexico.

“Within this trilateral relationship,” reports the Atlantic Council, “Mexico’s role in particular could lean into its domestic priorities to expand energy infrastructure, strengthen its electric vehicle and semiconductor sectors, and develop its mineral wealth.”

The Atlantic Council, a longstanding bipartisan think tank dedicated to issues of international coordination and security, recently released a 14-page policy brief arguing for enhanced cooperation between North American nations in order to be able to compete with China in global energy value chains. As Mexico, Canada, and the United States have prioritized protectionist policies and fractured nationalism over the last decade, China has increasingly consolidated global supply chains and currently exerts a great deal of control over international energy markets, especially in emerging economies. The Atlantic Council argues that counteracting this precarious consolidation will require a course correction and a return to convergence, coordination, and cooperation on the part of North American nations, who will stand stronger together than divided in a rapidly changing global market.

While the governments of the U.S., Mexico, and Canada have had loud and contentious tiffs against the backdrop of the Trump administrations (see: 51st state, wall) the three economies remain highly dependent on each other, and politically entangled in inextricable and bilateral ways. Smoothing over trade tensions in light of those dependencies is therefore strongly in the nations’ favor.

Although China is unmatched in terms of energy spending and its rapid expansion of energy influence, supply chains, and investment into energy assets in emerging economies, the Atlantic Council argues that North America is well-positioned to challenge China’s runaway dominance if it can play to its historic strengths.

“North America’s energy abundance has positioned the region as the world’s dominant energy exporter,” states the October policy brief. “The United States leads global LNG exports, Canada supplies critical oil and gas resources, and Mexico’s emerging Pacific Coast LNG projects will provide direct access to Asian markets. This collective export capacity creates shared prosperity through export revenues while offering democratic allies alternatives to authoritarian energy suppliers, transforming energy integration from an economic opportunity into a geopolitical asset.”

This plan hinges on Mexico’s ambitious energy planning – including the Plan Mexico policy – as laid out by its new president Claudia Sheinbaum. Mexico is critical to the nearshoring ambitions of the United States and Canada, who seek to shorten and strengthen localized supply chains in the interest of energy security, independence, and sovereignty, not to mention increased control within global markets. Mexico also has enormous and largely untapped potential for green energy production.

“Through Plan Mexico, the current administration has outlined an ambitious economic transformation strategy that prioritizes manufacturing growth, critical mineral development, and energy security—priorities that align with US and Canadian interests in building more resilient regional supply chains,” writes the Atlantic Council.

Increased North American energy cooperation is also critical to keeping Mexico’s alliances pointed north rather than East. China has been rapidly expanding its presence in energy sectors across Latin America, and Mexico would be a highly strategic trade partner for Beijing. Isolating and alienating Mexico from North American cooperation would push the country toward Beijing, with likely disastrous consequences for policy and economic goals for the entire continent.

The U.K. now generates more electricity from wind than from fossil fuels, marking a historic milestone in its green transition.

A UCL study found that wind power reduced consumer energy bills by $137 billion between 2010 and 2023.

With wind capacity projected to exceed 67 GW by 2030, Britain’s investment in renewables is reshaping both its energy mix and pricing structure.

The United Kingdom has rapidly developed its wind energy sector over the last two decades to become one of the biggest wind power producers worldwide. As the government aims to accelerate the green transition through greater investment in renewable energies and upgrading the national grid, the U.K.’s wind sector is expected to continue growing substantially in the coming decades. Meanwhile, recent studies suggest that the deployment of more wind power has helped significantly reduce consumer energy bills.

There is approximately 15.7 GW of operational onshore wind power in the U.K., with an increase of 739 MW in 2024 through the development of projects such as the Viking (443MW), Kype Muir Extension (67.2MW), and Broken Cross (43.2MW) windfarms. In 2024, 77 onshore wind projects submitted for planning permission, a slight reduction from the 83 submissions in 2023, but far higher than the 44 submissions in 2022.

The U.K. is expected to achieve 26 GW of onshore wind by 2030, which is 3.1 GW below the target established in the U.K. Government’s Clean Power 2030 Action Plan (CP30), according to a forecasting model by EnergyPulse. The wind industry also employs around 55,000 people, a figure that is set to double to around 110,000 by the end of the decade.

The U.K. has an operational offshore wind capacity of around 14.7 GW. Construction is currently underway on six projects with a total capacity of 6.3 GW, and three of these projects have a generating capacity of 2.5 GW, with development expected to be completed in 2025. Two more (2.5GW) operators will commence offshore construction this year. There were 14 planning applications for offshore wind projects submitted in 2024, with a total capacity of 15.4 GW, making for a total offshore wind capacity pipeline of 22.85 GW. The U.K.’s offshore wind capacity is expected to reach 41.5 GW by the end of 2030, including 1.2 GW of floating wind capacity.

Wind energy was the U.K.’s largest source of electricity generation in the final quarter of 2023 and the first quarter of 2024, making it the longest stretch of time on record where renewable energy contributed more power generation than that of fossil fuels. In Q1 of 2024, wind energy generation totalled 25.3 terawatt hours (TWh), compared to 23.6 TWh from all fossil fuel sources. Wind power contributed an average of 39.4 percent of total electricity production in this period. This marked a major turning point for the U.K., which has long relied on fossil fuels for power.

In addition to helping the U.K. to achieve a green transition, it seems that wind power is also saving consumers billions, according to a recent study. An analysis from University College London (UCL) found that between 2010 and 2023, wind-generated energy decreased electricity bills by $18.7 billion and reduced the cost of natural gas by $175 billion. When green subsidies of $56.8 billion paid by consumers are factored in, it results in a total reduction of $137 billion in U.K. consumer energy bills over 13 years.

The rapid development of renewable energy capacity across Europe has spurred a decrease in the demand for gas, thereby driving down gas prices. This has meant that electricity companies have not needed to construct expensive new gas-fired power stations to meet the rising demand, thereby saving consumers money. The report assessed the period from 2010 to 2023, meaning that the rising gas prices resulting from the Russian invasion of Ukraine and ongoing war were not taken into account.

“Far from being a financial burden, this study demonstrates how wind generation has consistently delivered substantial financial benefits to the UK. To put it into context, this net benefit of £104 billion ($137 billion) is larger than the additional £90 billion ($118 billion) the U.K. has spent on gas since 2021 as a result of rising prices related to the war in Ukraine,” explained the lead author of the report, Colm O’Shea. “This study demonstrates why we should reframe our understanding of green investment from costly environmental subsidy to a high-return national investment.”

The operators of gas-fired power stations are relied upon for setting the price of electricity in the U.K. However, the shift in the country’s energy mix and the savings discussed in the report could encourage a new approach to energy pricing. Mark Maslin, a professor of Earth system science at UCL, stressed the need to “decouple gas and electricity prices” to reflect the international energy market. “That would mean gas prices would reflect the global markets, while the electricity price would reflect the savings from wind and solar,” explained Maslin.

The heavy investment in the U.K.’s wind sector over the last 25 years seems to have paid off, as it is supporting the government’s green transition aims as well as reducing the cost of consumer energy bills. The country’s wind energy capacity is set to continue growing rapidly over the coming decade and could ultimately change the way energy prices are set as the U.K. welcomes a more diverse energy mix.

By Felicity Bradstock for Oilprice.com

Slovakia’s Auto Empire Is Facing Its Biggest Test Yet

Slovakia’s car industry, the largest per capita in the world, is struggling under new U.S. tariffs and rising Chinese competition.

Domestic taxes and Prime Minister Fico’s controversial stance toward Russia have eroded investor confidence and EU relations.

Industry leaders urge the government to stabilize policy and support investment to sustain Slovakia’s transformation toward EV production.

One of Europe’s automotive manufacturing powerhouses, Slovakia, has been hit hard by tariffs and increased competition, which are threatening its role in the global auto market. Since the creation of the Bratislava Automobile Works (BAZ) in the 1970s, Slovakia has gradually developed its reputation as a major automotive manufacturer. It now produces the highest number of cars per capita each year, with an annual output of over one million vehicles.

Slovakia became known as “Europe’s Detroit,” attracting automakers such as Volkswagen, Stellantis, Kia, and Jaguar Land Rover. Its automotive industry contributes around 11 percent of the country’s GDP, as well as half of its industrial output. It also accounts for roughly 10 percent of national employment.

In recent years, it has broken into the electric vehicle (EV) manufacturing market, with plans from Sweden’s Volvo Cars to establish an EV facility in the central European country in 2026. This will be Slovakia’s fifth production plant. China’s Gotion High Tech and Slovakian partner InoBat also plan to launch an EV battery plant in Slovakia, which could attract more EV makers to the market.

However, growing challenges in recent years now threaten Slovakia’s reputation as Europe’s automaking powerhouse. These include the introduction of U.S. tariffs under President Donald Trump and increased competition from China’s growing vehicle manufacturing sector. In addition, rising national taxes and a geopolitical shift away from the EU have hindered the country’s automotive sector.

At present, Slovakia’s exports to the United States account for around 4 percent of the country’s total exports, with vehicles contributing around 80 percent of that export volume. This has made Slovakia highly reliant on U.S. trade and means it has been hit hard by the introduction of high tariffs on foreign goods.

The EU succeeded in establishing a framework trade deal with the U.S. in July, which reduced the tariffs on most EU products from the anticipated 30 percent to a lower 15 percent rate, and decreased tariffs on the bloc’s auto sector from 27.5 percent. Zuzana Pelakova, from the Slovakia-based thinktank Globsec, said, “In the current situation, the U.S.-EU trade alliance has stabilised, and tariffs have been lowered to 15 percent, which is certainly better than the initial proposal but is still challenging.”

However, when new 15 percent tariffs are viewed alongside the broader set of challenges faced by Slovakia’s automaking industry, it becomes clear just how hard the sector will have to fight to maintain its position as a global leader. Increased domestic levies, following the introduction of a transaction tax under Prime Minister Robert Fico’s government, aimed at curbing the budget deficit and funding social programmes, are undermining profits in the country’s automotive sector.

Fico has come under fire from the EU for his longstanding relationship with Russia’s President Putin in the wake of the Russian invasion of Ukraine and ongoing war. In a July statement, Fico said, “I refuse the politics of the ‘iron fence’ that exists between the EU and the Russian Federation, and I would like to offer a hand of cooperation over this fence… When it comes to energy, I openly say that I view any plans of the European Commission to stop any import of gas, oil or nuclear fuel from Russia as insanity.”

The Slovakian government’s stance on Russia has led several European countries to view Slovakia as a less reliable partner, one that is unwilling to support the sanctions on Russian energy that are meant to put pressure on Moscow to end its conflict with Ukraine.

As around 90 percent of Slovakia’s foreign direct investment comes from EU countries, rising geopolitical tensions could threaten its economic stability. A survey from earlier in the year showed that among foreign chambers of commerce, 36 percent of European companies with assets in Slovakia did not plan to invest in the country again. This is reflected in Volkswagen’s decision to launch operations in Portugal instead of Slovakia for its new electric ID.1 model, while Stellantis NV opted to establish an EV facility in Spain.

Despite the challenges, many believe that Slovakia’s longstanding automaking industry will weather the storm, as it has done in the past. However, the country’s auto association, ZAPSR, believes that to make headway, the industry must engage with the government to improve policy and economic support for the sector.

“To maintain the transformation of production to electromobility, it is necessary that the state creates framework conditions for investors, with clear and stable foreign policy orientation, keeping in mind that in the last 15 years, 93 per cent of investment arrived from the EU countries, UK and USA,” ZAPSR said in a statement earlier this year. Meanwhile, ZAPSR’s president, Alexander Matusek, stressed, “These concerns about Slovakia’s place in the world are relevant. Besides the economic factors, investors also look at what the state does – we shouldn’t underestimate this.”

By Felicity Bradstock for Oilprice.com

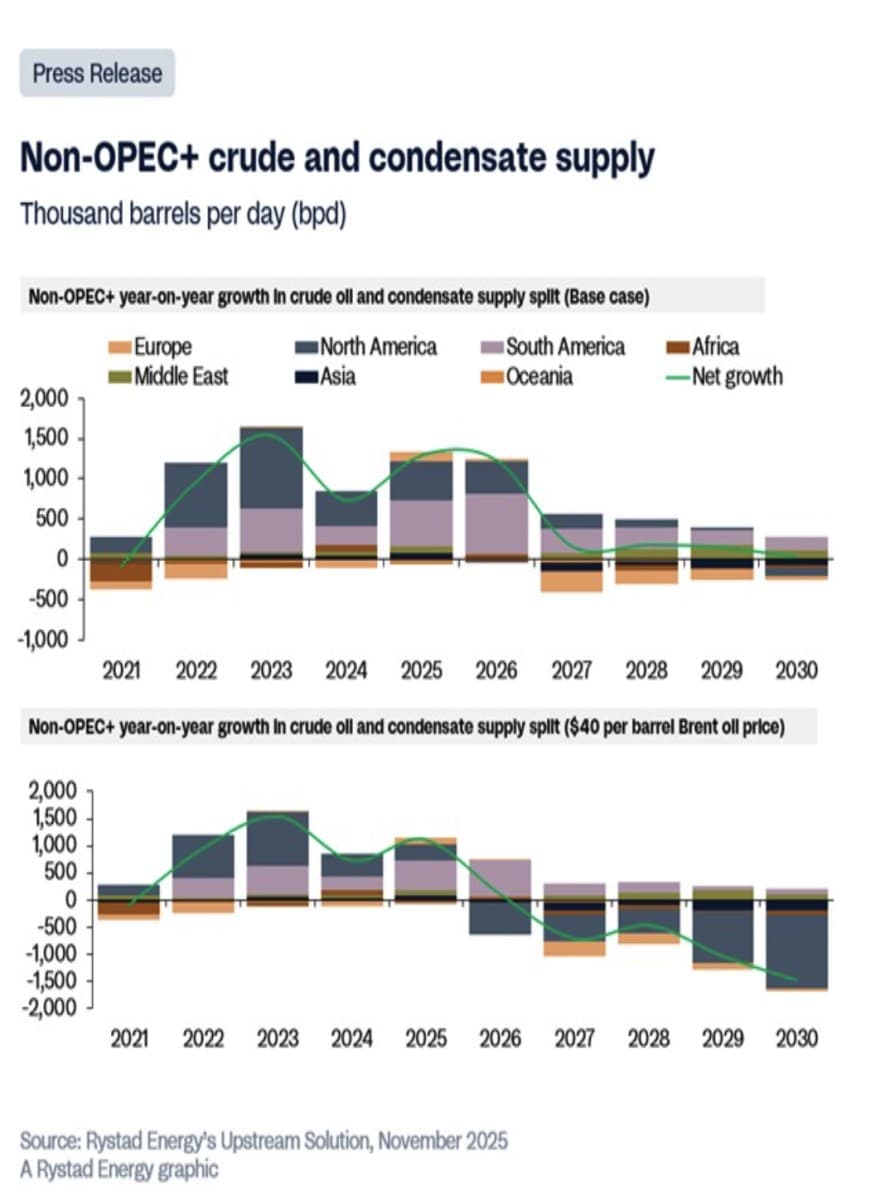

Brazil, Guyana, and Argentina Lead Next Wave of Non-OPEC Oil Production

Rystad Energy forecasts that South America, led by Brazil, Guyana, and Argentina's Vaca Muerta, will be the primary source of cost-competitive non-OPEC+ oil, accounting for nearly 60% of new conventional oil capacity through 2030.

Brazil's ultra-deepwater pre-salt fields and Guyana's rapid production growth from the Stabroek Block are key drivers, with Guyana expected to produce nearly 1.3 million barrels daily by 2027.

While Argentina's Vaca Muerta shale oil production has surged, natural gas is now stealing the spotlight, positioning Argentina to become a pivotal player in global liquefied natural gas export strategy.

Oil from offshore Brazil, Guyana, Suriname, and Argentina’s Vaca Muerta shale play will be key sources of cost-competitive non-OPEC oil supply through 2030, Rystad Energy has predicted. Rystad has predicted that global liquids demand will peak in the 2030s at around 107 million barrels per day (bpd), maintain a plateau above 100 million bpd through the 2040s before declining to around 75 million bpd by 2050. According to the Norwegian energy consultancy, non-OPEC+ supply will be key to balancing the global market, with cheap oil from South America helping to offset slower U.S. shale growth. Non-OPEC+ producers are expected to account for around 5.9 million bpd, or nearly 60%, of new conventional oil currently under development through 2030 (total new capacity). South America will be the main source of this supply growth at 560,000 bpd of crude and condensate, with North America supplying ~480,000 bpd.

Radhika Bansal, VP of Upstream Research at Rystad Energy, said today’s producing wells are on track to deliver less than half of their current output by 2030, a trend that reinforces the need for sustained investment in both new and mature fields. She noted that undeveloped and discovered assets will continue to play a key role in meeting global supply needs through the mid-2030s. While the market could briefly tip into oversupply, Bansal cautioned that “above-surface risks could trigger delays in project timelines.” She added that South America’s deepwater track record positions it well to provide competitive barrels globally, with continued investment needed as the supply gap is expected to widen after the mid-2030s.

Source: Rystad Energy

Brazil is a leading source of production growth, especially from its prolific offshore ultra-deepwater pre-salt oil fields, which boast low break-even costs. Major investments are being made, with several new Floating Production Storage and Offloading (FPSO) units scheduled to come online in the current year. Brazil's offshore oil production is a major driver of its economy, with production primarily from pre-salt fields like Lula and Búzios, operated mostly by the state-owned company Petrobras (NYSE:PBR). The country has set new production records and continues to increase its output through the development of new platforms and exploration in deepwater fields, though it faces regulatory and infrastructural challenges. The Lula Field is one of Brazil’s most significant offshore projects with estimated reserves of 8.3 billion barrels of oil equivalent(boe); Búzios Fieldachieved a record 800,000 barrels of oil per day in February 2025, with more platforms being added to increase capacity.

Guyana's oil production has increased rapidly, surpassing 770,000 barrels per day as of October 2025, primarily from the ExxonMobil (NYSE:XOM)-led consortium's projects in theStabroek Block. This surge was due to the start-up of the Yellowtail development, the fourth floating production vessel (FPSO). Guyana is expected to hit 900,000 bpd once the fourth facility is fully operational, with a long-term goal to eventually produce over one million barrels per day once projects like Uaru and Whiptail come online in 2026 and 2027. Indeed, Exxon says Guyana could be producing nearly 1.3m barrels daily by 2027, making it one of the most prolific per capita producers in the world.

Meanwhile, Vaca Muerta shale oil production has surged 26% Y/Y to over 447,000 barrels per day, and now accounts for the majority of Argentina's total oil output, according to estimates by Rystad Energy. Vaca Muerta is one of the world's largest unconventional oil reserves, estimated at 16.2 billion barrels of recoverable oil. Production has been boosted by significant investment, leading to lower lifting costs in main production areas and increased productivity.Positive investor sentiment and a focus on infrastructure development are crucial for future growth, as seen with companies reversing decisions to exit and companies like Norway's Equinor (NYSE:EQNR) returning to the play. Equinor and Shell Plc. (NYSE:SHEL) acquired a 49% stake in the Bandurria Sur block from Schlumberger (NYSE:SLB) in 2020, with the acquisition following its initial entry into the region in 2017 and a subsequent agreement with YPF to develop theBajo del Toro block.

However, the iconic basin is showing signs of slowing down, particularly in drilling activity due to saturated takeaway capacity. Interestingly, natural gas is now stealing the Vaca Muerta's spotlight, with dry gas production clocking in at 2.1 billion cubic feet per day (Bcfd) in the first quarter of 2025, up 16% Y/Y. According to Rystad, Argentina is now “…pursuing a bold, multi-phase national LNG export strategy, meaning Argentina could soon become a pivotal player in global gas supply, significantly reshaping markets and energy geopolitics.”

Rystad Energy forecasts global liquids demand to peak at 107 million bpd in the early 2030s, remaining above 100 million bpd through the 2040s.

South America is expected to add over 750,000 bpd by 2026, led by Brazil and Guyana’s offshore projects supported by FPSOs.

The region’s upstream investments are projected to total nearly $200 billion by 2030, with emerging exploration in Trinidad and Peru offering new frontier potential.

Oil production from offshore Brazil, Guyana and Suriname, as well as Argentina’s Vaca Muerta shale is well-positioned to supply cost-competitive barrels until 2030. Global oil demand is expected to remain robust throughout the 2030s, putting pressure on currently producing assets to keep pace. Rystad Energy’s research forecasts global liquids demand to peak in the early 2030s at around 107 million barrels per day (bpd), remaining above 100 million bpd through the 2040s before gradually declining to about 75 million bpd by 2050. Non-OPEC+ supply will be key to balancing the market, with South America playing a central role by delivering cost-competitive barrels even at low prices, offsetting slower US shale growth.

Today’s wells are projected to deliver less than half of their current output by 2030, underscoring the need for continued investment in both new and existing fields. While additional volumes can be brought online, undeveloped and discovered fields will remain important sources of supply through the mid-2030s. Although the market may experience a brief period of oversupply, above-surface risks could trigger delays in project timelines. South America is well-positioned to offer competitive barrels to a global market due to its success with deepwater projects. Looking ahead, continued investment and a stronger focus on deepwater expansion as the supply gap might widen after the mid-2030s.

Radhika Bansal, vice president, Upstream research, Rystad Energy

Nearly 60% of conventional under-development and discovered volumes, close to 5.9 million bpd, is expected from non-OPEC+ producers through 2030. South America will lead supply growth this year, adding over 560,000 bpd of crude and condensate, followed by North America with around 480,000 bpd. By 2026, South America’s additions should exceed 750,000 bpd, keeping the region among the few regions with additions over 500,000 bpd, alongside the Middle East (outside OPEC+), driving non-OPEC+ growth.

Offshore oilfields which have come online since 2020, and those set to start up by 2030, will account for over 65% of South America’s conventional production. This growth is supported by the increasing use of floating production, storage and offloading (FPSO) vessels, led primarily by developments in Brazil and Guyana. In Guyana, ExxonMobil has advanced multiple discoveries, with four FPSOs already in production, demonstrating effective project execution. However, the pace of new discoveries has slowed, with approximately 420 million barrels of liquids discovered over the past year, the lowest level since 2017, highlighting the ongoing need for exploration. Rystad Energy’s base case projections sees oil demand expected to outpace current supply by the mid-2030s, amplifying the need for renewed exploration and enhanced recovery; an area where South America is well positioned to play a key role.

The region’s future will also heavily depend on sanctioning activity. South America will maintain a strong final investment decision (FID) momentum through 2030, leading to a cumulative conventional greenfield capital expenditure (capex) for oilfields between 2020 and 2030 of $197 billion, largely concentrated in offshore deepwater projects. While Brazil and Guyana account for most of these investments, Suriname’s $10.5 billion GranMorgu field (formerly Sapakara South and Krabdagu), is slated to come online by 2028.

Total upstream investment in South American oilfields reached over $46 billion last year, the highest level since 2015. This year, investments are expected to grow by 10% before tapering slightly in the following years, stayuing close to $50 billion throughout the next decade. Greenfield investments will be led by Brazil and Guyana’s yet-to-produce assets. Already producing fields in Argentina, Brazil and Colombia will drive brownfield spending.

South America’s upstream sector occupies a pivotal role in the global energy landscape, having contributed substantially to conventional production and new discoveries over the past decade. The region has been a consistent driver of net oil exports and is set to remain crucial in the years ahead, with Argentina, Guyana, Suriname and Venezuela leading the charge. Brazil, Colombia and Ecuador are also expected to sustain meaningful export contributions at least through the mid-2030s. With adequate investment in exploration, there remains considerable upside potential, as new discoveries could unlock future volumes and enhance recoverable resources from existing fields.

Two countries that may receive less attention but show potential are Trinidad and Tobago and Peru. ExxonMobil has made a strategic re-entry into Trinidad and Tobago, one of the Caribbean’s least-explored ultra-deepwater frontiers, through a new production-sharing contract (PSC). Using a similar exploration approach that identified over 13 billion barrels of recoverable resources in Guyana’s Stabroek Block, ExxonMobil aims to replicate this model. If new discoveries are made, the company could invest more than $20 billion, signaling continued interest in frontier deepwater exploration.

In Peru, offshore northern basins are emerging as a promising exploration area. A consortium of Chevron, Anadarko (Occidental Petroleum), and Westlawn has recently partnered to explore three offshore blocks, Z-61, Z-62, and Z-63, in the Mar de Grau, off northern La Libertad. Successful exploration could add significant new reserves, where a commercial discovery could yield between 100,000 and 150,000 barrels per day in peak production.

Europe's liquefied natural gas imports have risen substantially, more than compensating for a year-on-year decline in Asian imports, shifting the global LNG demand center from Asia to Europe

The increase in European demand has made LNG more expensive, effectively pricing out more price-sensitive Asian importers and causing a decline in their purchases.

Major LNG suppliers like Exxon and Qatar are threatening to stop doing business with the EU over the new Corporate Sustainability Due Diligence Directive, which would require tracking supply chain emissions and human rights records.

Asia has been the driver of global demand for liquefied natural gas for years now, with its fast-growing economies guzzling energy at elevated rates. This year, however, has seen this change. Asian demand for LNG is weakening—but Europe’s is on a substantial rise, more than offsetting Asia’s weakness, despite plans to reduce consumption of all hydrocarbons.

LNG imports to Asia last month stood at 22.84 million tons, Kpler data, cited by Reuters’ Clyde Russell, showed. This was a slight increase from September but palpably lower than October 2024, when imports hit 24.39 million tons. Over the first ten months of the year, Asia’s imports of liquefied gas were down by over 14 million tons on the year to 225.8 million tons. Russell suggests China was one driver of this trend, booking year-on-year LNG import declines every month since November 2024.

Yet while Asian energy importers curbed their purchases of liquefied gas, European buyers stepped up their orders. The Kpler data shows that over the first ten months of the year, Europe imported 101.38 million tons of the fuel. This was 16.75 million tons more than what Europe imported a year earlier—even as the EU leadership boasted about permanently reducing the bloc’s consumption of natural gas, not just from Russia but in general.

It was this increase in European LNG purchases that likely affected demand for the superchilled fuel in Asia. Despite growing at a faster clip than Europe overall, Asian economies are more price-sensitive in energy imports. A surge in demand for LNG from Europe regularly prices out poorer Asian importers, although an argument could be made that Europe is finding it increasingly hard to pay its own energy import bills as it stretches itself thin to fund an energy transition away from oil and gas, and an accelerated buildout of military capabilities that requires cheap energy to be successful.

Europe, in other words, has emerged as a hotspot for LNG demand, drawing the attention of producers. However, this attention is not homogeneous. U.S. Energy Secretary Chris Wright, for instance, has repeatedly called on Europe to stop importing Russian energy altogether and boost its purchases of U.S. LNG. Indeed, the European Commission’s president Ursula von der Leyen signed a trade deal with President Trump, committing to a massive increase in such purchases. Yet one of the largest LNG exporters in the world, Exxon, has warned it may have to stop doing business with the EU unless it axes new legislation that aims to force international companies to track their emissions and human rights record across their supply chains.

Exxon, moreover, is not the only one threatening to quit Europe if it goes ahead with the Corporate Sustainability Due Diligence Directive. Qatar, the world’s number-two in LNG exports, is also going to stop selling gas to Europe if it tries to force QatarEnergy to track and reduce its emissions, and monitor human rights protection, or risk getting fined 5% of its annual global revenues.

Meanwhile, as the EU buys ever more LNG—including from Russia—one energy-focused energy transition advocacy outlet warned the bloc should not saddle itself with long-term LNG purchase commitments, because demand for gas in Europe was about to shed a quarter over the next 25 years.

“European countries risk over-relying on one supplier if they commit to long-term US LNG contracts. The US supplied more than half (57%) of Europe’s LNG imports in H1 2025, as deliveries from the country reached a new high,” the Institute for Energy Economics and Financial Analysis reported earlier this month, noting that Germany and Greece had topped the single-supplier list, sourcing a respective 94% and 84% of their LNG from the United States over the first half of the year.

Yet the IEEFA believes this acceleration in LNG purchases this year is a temporary glitch while demand dynamics point to a weakening in the future. The reason: more wind and solar. This has been the go-to argument of the pro-transition lobby, even though evidence suggests the record buildout of wind and solar generation has done little to change the energy consumption makeup of the European energy system outside certain seasonal output peaks. Germany, for instance, was recently revealed to have booked the highest rate of power generation from natural gas power plants due to weak winds for most of the year.

While the IEEFA and other transition outlets predict gas demand destruction in Europe, they also predict a glut of LNG due to excess capacity. Yet cheaper LNG is likely to only push demand higher across more importing countries as the commodity becomes more affordable for everyone. With the weather unlikely to become more predictable in the future, chances are that reliance on natural gas will continue strong in both Europe and Asia, regardless of transition ambitions.

.jpg)