Brazil, Guyana, and Argentina Lead Next Wave of Non-OPEC Oil Production

- Rystad Energy forecasts that South America, led by Brazil, Guyana, and Argentina's Vaca Muerta, will be the primary source of cost-competitive non-OPEC+ oil, accounting for nearly 60% of new conventional oil capacity through 2030.

- Brazil's ultra-deepwater pre-salt fields and Guyana's rapid production growth from the Stabroek Block are key drivers, with Guyana expected to produce nearly 1.3 million barrels daily by 2027.

- While Argentina's Vaca Muerta shale oil production has surged, natural gas is now stealing the spotlight, positioning Argentina to become a pivotal player in global liquefied natural gas export strategy.

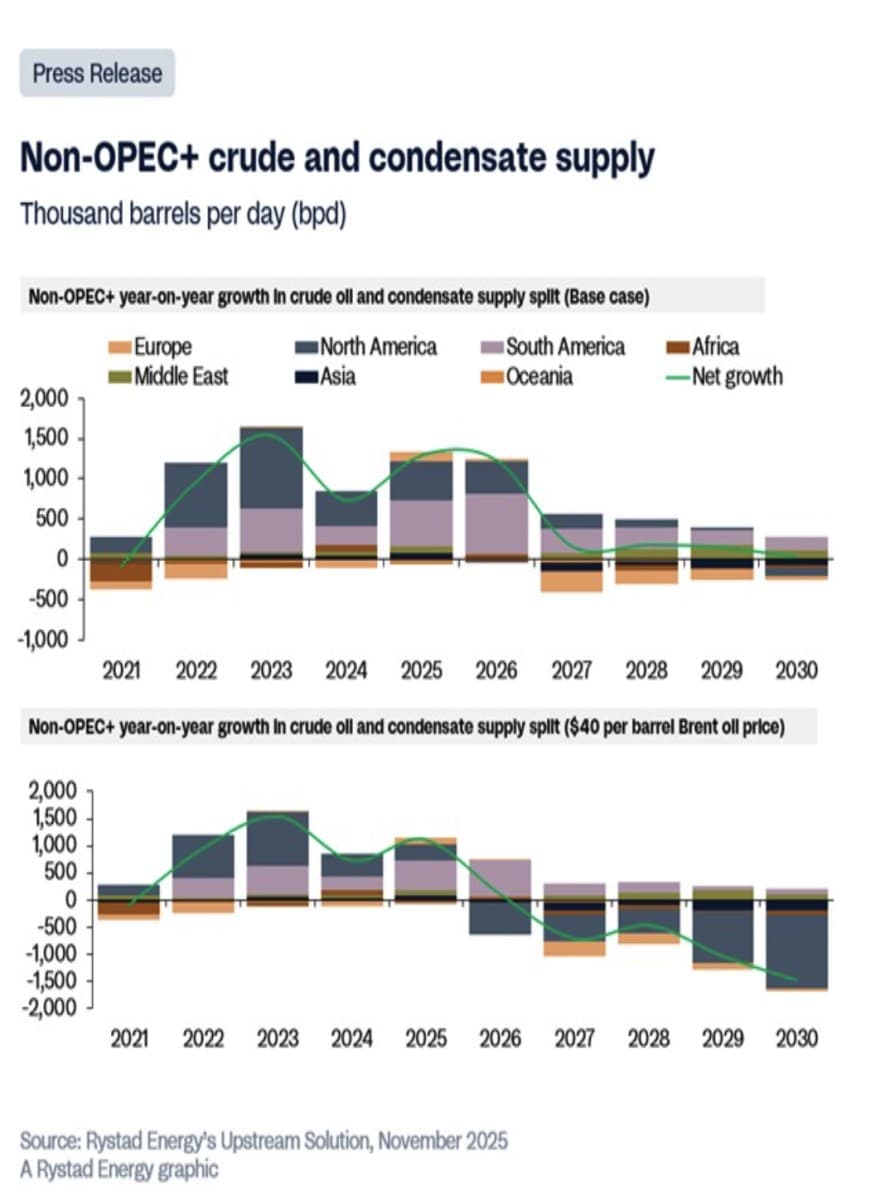

Oil from offshore Brazil, Guyana, Suriname, and Argentina’s Vaca Muerta shale play will be key sources of cost-competitive non-OPEC oil supply through 2030, Rystad Energy has predicted. Rystad has predicted that global liquids demand will peak in the 2030s at around 107 million barrels per day (bpd), maintain a plateau above 100 million bpd through the 2040s before declining to around 75 million bpd by 2050. According to the Norwegian energy consultancy, non-OPEC+ supply will be key to balancing the global market, with cheap oil from South America helping to offset slower U.S. shale growth. Non-OPEC+ producers are expected to account for around 5.9 million bpd, or nearly 60%, of new conventional oil currently under development through 2030 (total new capacity). South America will be the main source of this supply growth at 560,000 bpd of crude and condensate, with North America supplying ~480,000 bpd.

Radhika Bansal, VP of Upstream Research at Rystad Energy, said today’s producing wells are on track to deliver less than half of their current output by 2030, a trend that reinforces the need for sustained investment in both new and mature fields. She noted that undeveloped and discovered assets will continue to play a key role in meeting global supply needs through the mid-2030s. While the market could briefly tip into oversupply, Bansal cautioned that “above-surface risks could trigger delays in project timelines.” She added that South America’s deepwater track record positions it well to provide competitive barrels globally, with continued investment needed as the supply gap is expected to widen after the mid-2030s.

Source: Rystad Energy

Brazil is a leading source of production growth, especially from its prolific offshore ultra-deepwater pre-salt oil fields, which boast low break-even costs. Major investments are being made, with several new Floating Production Storage and Offloading (FPSO) units scheduled to come online in the current year. Brazil's offshore oil production is a major driver of its economy, with production primarily from pre-salt fields like Lula and Búzios, operated mostly by the state-owned company Petrobras (NYSE:PBR). The country has set new production records and continues to increase its output through the development of new platforms and exploration in deepwater fields, though it faces regulatory and infrastructural challenges. The Lula Field is one of Brazil’s most significant offshore projects with estimated reserves of 8.3 billion barrels of oil equivalent(boe); Búzios Field achieved a record 800,000 barrels of oil per day in February 2025, with more platforms being added to increase capacity.

Guyana's oil production has increased rapidly, surpassing 770,000 barrels per day as of October 2025, primarily from the ExxonMobil (NYSE:XOM)-led consortium's projects in the Stabroek Block. This surge was due to the start-up of the Yellowtail development, the fourth floating production vessel (FPSO). Guyana is expected to hit 900,000 bpd once the fourth facility is fully operational, with a long-term goal to eventually produce over one million barrels per day once projects like Uaru and Whiptail come online in 2026 and 2027. Indeed, Exxon says Guyana could be producing nearly 1.3m barrels daily by 2027, making it one of the most prolific per capita producers in the world.

Meanwhile, Vaca Muerta shale oil production has surged 26% Y/Y to over 447,000 barrels per day, and now accounts for the majority of Argentina's total oil output, according to estimates by Rystad Energy. Vaca Muerta is one of the world's largest unconventional oil reserves, estimated at 16.2 billion barrels of recoverable oil. Production has been boosted by significant investment, leading to lower lifting costs in main production areas and increased productivity.Positive investor sentiment and a focus on infrastructure development are crucial for future growth, as seen with companies reversing decisions to exit and companies like Norway's Equinor (NYSE:EQNR) returning to the play. Equinor and Shell Plc. (NYSE:SHEL) acquired a 49% stake in the Bandurria Sur block from Schlumberger (NYSE:SLB) in 2020, with the acquisition following its initial entry into the region in 2017 and a subsequent agreement with YPF to develop the Bajo del Toro block.

However, the iconic basin is showing signs of slowing down, particularly in drilling activity due to saturated takeaway capacity. Interestingly, natural gas is now stealing the Vaca Muerta's spotlight, with dry gas production clocking in at 2.1 billion cubic feet per day (Bcfd) in the first quarter of 2025, up 16% Y/Y. According to Rystad, Argentina is now “…pursuing a bold, multi-phase national LNG export strategy, meaning Argentina could soon become a pivotal player in global gas supply, significantly reshaping markets and energy geopolitics.”

By Alex Kimani for Oilprice.com

South America to Anchor Non-OPEC+ Oil Supply Through 2030

- Rystad Energy forecasts global liquids demand to peak at 107 million bpd in the early 2030s, remaining above 100 million bpd through the 2040s.

- South America is expected to add over 750,000 bpd by 2026, led by Brazil and Guyana’s offshore projects supported by FPSOs.

- The region’s upstream investments are projected to total nearly $200 billion by 2030, with emerging exploration in Trinidad and Peru offering new frontier potential.

Oil production from offshore Brazil, Guyana and Suriname, as well as Argentina’s Vaca Muerta shale is well-positioned to supply cost-competitive barrels until 2030. Global oil demand is expected to remain robust throughout the 2030s, putting pressure on currently producing assets to keep pace. Rystad Energy’s research forecasts global liquids demand to peak in the early 2030s at around 107 million barrels per day (bpd), remaining above 100 million bpd through the 2040s before gradually declining to about 75 million bpd by 2050. Non-OPEC+ supply will be key to balancing the market, with South America playing a central role by delivering cost-competitive barrels even at low prices, offsetting slower US shale growth.

Today’s wells are projected to deliver less than half of their current output by 2030, underscoring the need for continued investment in both new and existing fields. While additional volumes can be brought online, undeveloped and discovered fields will remain important sources of supply through the mid-2030s. Although the market may experience a brief period of oversupply, above-surface risks could trigger delays in project timelines. South America is well-positioned to offer competitive barrels to a global market due to its success with deepwater projects. Looking ahead, continued investment and a stronger focus on deepwater expansion as the supply gap might widen after the mid-2030s.

Radhika Bansal, vice president, Upstream research, Rystad Energy

Nearly 60% of conventional under-development and discovered volumes, close to 5.9 million bpd, is expected from non-OPEC+ producers through 2030. South America will lead supply growth this year, adding over 560,000 bpd of crude and condensate, followed by North America with around 480,000 bpd. By 2026, South America’s additions should exceed 750,000 bpd, keeping the region among the few regions with additions over 500,000 bpd, alongside the Middle East (outside OPEC+), driving non-OPEC+ growth.

Offshore oilfields which have come online since 2020, and those set to start up by 2030, will account for over 65% of South America’s conventional production. This growth is supported by the increasing use of floating production, storage and offloading (FPSO) vessels, led primarily by developments in Brazil and Guyana. In Guyana, ExxonMobil has advanced multiple discoveries, with four FPSOs already in production, demonstrating effective project execution. However, the pace of new discoveries has slowed, with approximately 420 million barrels of liquids discovered over the past year, the lowest level since 2017, highlighting the ongoing need for exploration. Rystad Energy’s base case projections sees oil demand expected to outpace current supply by the mid-2030s, amplifying the need for renewed exploration and enhanced recovery; an area where South America is well positioned to play a key role.

The region’s future will also heavily depend on sanctioning activity. South America will maintain a strong final investment decision (FID) momentum through 2030, leading to a cumulative conventional greenfield capital expenditure (capex) for oilfields between 2020 and 2030 of $197 billion, largely concentrated in offshore deepwater projects. While Brazil and Guyana account for most of these investments, Suriname’s $10.5 billion GranMorgu field (formerly Sapakara South and Krabdagu), is slated to come online by 2028.

Total upstream investment in South American oilfields reached over $46 billion last year, the highest level since 2015. This year, investments are expected to grow by 10% before tapering slightly in the following years, stayuing close to $50 billion throughout the next decade. Greenfield investments will be led by Brazil and Guyana’s yet-to-produce assets. Already producing fields in Argentina, Brazil and Colombia will drive brownfield spending.

South America’s upstream sector occupies a pivotal role in the global energy landscape, having contributed substantially to conventional production and new discoveries over the past decade. The region has been a consistent driver of net oil exports and is set to remain crucial in the years ahead, with Argentina, Guyana, Suriname and Venezuela leading the charge. Brazil, Colombia and Ecuador are also expected to sustain meaningful export contributions at least through the mid-2030s. With adequate investment in exploration, there remains considerable upside potential, as new discoveries could unlock future volumes and enhance recoverable resources from existing fields.

Two countries that may receive less attention but show potential are Trinidad and Tobago and Peru. ExxonMobil has made a strategic re-entry into Trinidad and Tobago, one of the Caribbean’s least-explored ultra-deepwater frontiers, through a new production-sharing contract (PSC). Using a similar exploration approach that identified over 13 billion barrels of recoverable resources in Guyana’s Stabroek Block, ExxonMobil aims to replicate this model. If new discoveries are made, the company could invest more than $20 billion, signaling continued interest in frontier deepwater exploration.

In Peru, offshore northern basins are emerging as a promising exploration area. A consortium of Chevron, Anadarko (Occidental Petroleum), and Westlawn has recently partnered to explore three offshore blocks, Z-61, Z-62, and Z-63, in the Mar de Grau, off northern La Libertad. Successful exploration could add significant new reserves, where a commercial discovery could yield between 100,000 and 150,000 barrels per day in peak production.

No comments:

Post a Comment