It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Monday, January 12, 2026

NI

Nickel price extends drop amid lack of detail on Indonesia output cuts

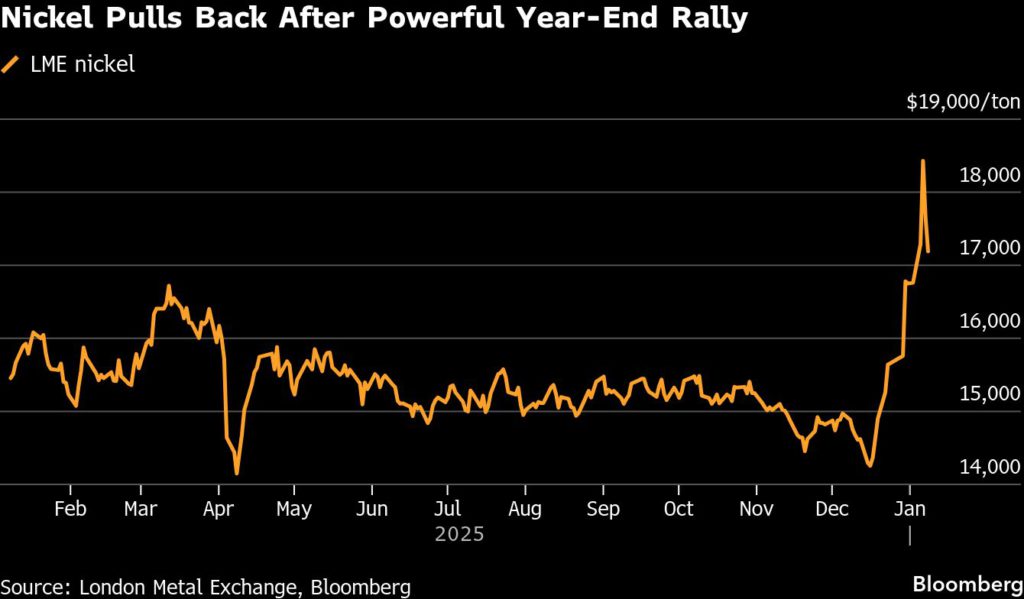

Nickel fell further from a 19-month high after Indonesia didn’t provide details on its pledge for output cuts, which had earlier fueled a sharp rally.

Three-month futures declined as much as 5.9% on the London Metal Exchange. Prices had surged as high as $18,800 a ton on Wednesday — the highest since June 2024 — as investors bet on risks to output in top supplier Indonesia, but the metal ended the day 3.4% lower.

Indonesia has flagged plans to reduce production this year to improve the balance between supply and demand. The Energy and Mineral Resources Ministry didn’t provide any details on this year’s nickel mining quota at a Thursday press briefing, with Minister Bahlil Lahadalia saying the figures are still being finalized.

Nickel — used in batteries and stainless steel — has surged about 20% since mid-December, joining a rally in copper and aluminum. The metals have been buoyed by a wave of buying from Chinese traders, as well as heightened geopolitical concerns.

The sustainability of nickel prices “remains uncertain, unless quota reductions are implemented in a meaningful and consistent manner,” Benyamin Mikael, an analyst with UOB-Kay Hian Holdings Ltd., said in a note. The impact of the planned quota cuts is likely to be limited in the near term as “most committed investments are largely exempt for the next one to two years.”

Nickel settled 4.1% lower at $17,155 a ton on the LME as of 5:52 p.m. London time. Most other metals also settled lower, with copper falling 1.4% to close at $12,720.50 a ton.

Pressure for Indonesian quota U-turn is a risk for nickel price rally

Nickel pig iron plant in Indonesia. (Image from Nickel Mines Ltd.)

Indonesia’s plan to cut nickel mining quotas to boost revenues has succeeded in pushing nickel to close to 19-month highs but analysts say pressure for a policy reversal is likely to mean the rally will be short-lived.

Accounting for around 70% of global nickel production, which was estimated at around 3.8 million metric tons last year, Indonesia is the world’s biggest nickel producer.

Following its announcement of mining curbs in December, prices of nickel have steadily gained more than 30%. They hit $18,800 a ton this week, the highest since June 2024. It was last trading near $18,000.

How long the rally will last, however, depends largely on how long the government can keep lower quotas in place. A similar effort a year ago had a limited effect: in January 2025, the government said it would issue quotas for around 200 million wet metric tons for 2025, but ended up approving permits for nearly 300 million tons.

Industry pressure

“There will be a lot of pressure on them to relent. There are a lot of projects coming onstream this year,” said Macquarie analyst Jim Lennon.

“Cutting quotas would be like saying to Chinese companies which have built these plants, they can’t operate them. That would put the kibosh on any future investment.”

Nickel industry sources say many of the new projects will be ready to produce in the second half of the year and that Indonesia could limit the quotas – known locally as RKABs – only for the first half of the year.

When production increases, miners could reapply for higher quotas and the government could grant more licences, they said.

“The owners of these nickel operations are pretty close to the government, they always have been. They will lobby and the government will backflip like it did last year,” said Panmure Liberum analyst Tom Price.

Nickel, which is needed for electric vehicle batteries and steel production, accounted for about 12% of Indonesia’s exports last year. Directly and indirectly the industry employs thousands of people and Chinese companies are still investing millions of dollars to increase capacity.

Amply supplied

Regardless of Indonesian quotas, traders expect prices to retreat as funds finish short-covering as there is no shortage of nickel in the market.

Stocks in London Metal Exchange-approved warehouses have risen more than 300% to 275,634 tons since the start of 2025.

Meanwhile, off-warrant stocks, or nickel that could be delivered to the LME, at 112,028 tons is nearly double the level at the end of October last year.

(By Pratima Desai; Editing by Barbara Lewis)

IPO of India’s top coking coal miner oversubscribed on first day

The IPO of India’s largest coking coal miner was oversubscribed on the first day of bidding on Friday, as investors lined up for the first main board listing of 2026 and the maiden public sale from a firm in the key sector.

Bharat Coking Coal’s $118.7 million IPO drew bids for 1.72 billion shares, nearly five times the shares on offer, as of 1:20 p.m. IST. The firm’s parent state-owned Coal India is offloading a 10% stake in the IPO.

India was the world’s second-largest primary equity issuance market in 2025, with firms raising $21.8 billion through 367 deals in 2025, data compiled by LSEG showed.

“The pace of oversubscription in BCCL’s IPO sets the tone for the rest of the year,” said Mahesh Ojha, vice president of research and business development at Kantilal Chhaganlal Securities.

“India’s coking coal demand remains structurally strong, driven by sustained growth in steel production, infrastructure development, and industrial expansion,” Ojha said in a note.

Coking coal is a critical raw material for blast furnace-based steelmaking. India, the world’s second-largest crude steel producer, is seeking to curb import dependence amid rising demand.

At the IPO, retail investors bid for 864.9 million shares, more than six times the portion allocated to them.

The offering comes as the Indian government is pursuing divestment plans in state-owned firms, with public sector banks and energy firms at the forefront.

Bharat Coking’s revenue fell 3% to 138.03 billion rupees in fiscal year 2025, while its net profit declined 20% to 12.4 billion rupees.

The firm had total reserves of about 1,495.4 million tonnes as of March 31, 2025.

The shares are expected to make their trading debut on January 16.

($1 = 90.2650 Indian rupees)

(By Urvi Dugar and Hritam Mukherjee; Editing by Sonia Cheema and Mrigank Dhaniwala)

Highland Valley copper mine in British Columbia. Credit: Teck Resources

The proposed merger of London-listed miner Anglo American and Canada’s Teck Resources is heading for antitrust clearance in Europe after EU regulators signalled the absence of competition concerns, according to a European Commission filing.

The EU competition enforcer is reviewing the deal, the second-largest ever in the mining sector, under a simplified procedure after the companies sought approval on Tuesday.

Such a step means the EU watchdog does not see a merger giving rise to significant competition problems, leading it to conduct only a routine check.

The Commission will issue its decision on the deal to form the world’s fifth-largest copper company by February 10. Canada has already cleared the deal.

The Commission is also assessing the deal under its Foreign Subsidies Regulation which takes aim at unfair foreign aid for companies, with the goal of reining in competition from non-EU companies subsidized by their governments.

The BHP office building in Houston, Texas. Stock image.

Rio Tinto’s talks to buy Glencore and create a new global industry leader could spur consolidation efforts across the copper-hungry mining sector and heap pressure on BHP, currently the world’s biggest miner, to respond.

If the bid succeeds, and depending on any final value, it could rank among the biggest 10 M&A deals yet and it reflects an appetite for scale that bankers have said could drive mega-deals in 2026.

“This is yet another example that the mining space is consolidating and the big firms are being forced to do corporate action to create value,” Mark Kelly, CEO at advisory firm MKI Global, said.

Half a dozen analysts, investors and bankers told Reuters that BHP, which has a market capitalization of $161 billion, is the most likely spoiler of Rio’s bid talks with Glencore, which could create a company worth almost $207 billion.

If BHP keeps out of the current talks, it may consider another deal to retain its leadership.

One banking source, who spoke on condition of anonymity, said that was the most likely outcome, given the company views Glencore’s portfolio is too diverse and would benefit from asset sales. Regulatory authorities would almost certainly require some disposals to ease competition concerns.

BHP declined to comment.

“The most likely interloper to this deal is BHP,” said Richard Hatch, analyst at Berenberg. “Essentially, with the deal driven by copper, we think that BHP could look to acquire Glencore with a rival bid, keep copper, and likely divest the balance.”

Talks between Rio and Glencore are at a preliminary stage and Rio has until February 5 to make a formal offer, a deadline that could be extended.

The two sides have held talks in the past that have led nowhere and again they may fail to reach agreement.

George Cheveley, natural resources portfolio manager of Ninety One, which is a shareholder of Glencore, said BHP may feel the need to intervene, but also that it may find it “difficult emotionally” given its repeated failure to buy Anglo American.

To try to reinforce its dwindling dominance in copper, BHP tried to acquire Anglo American in a months-long pursuit in 2024. It briefly revived the effort in November last year.

Adding to the pressure on BHP, sources say the company is preparing to appoint a new CEO, most likely an internal candidate who will be expected to deliver change.

BHP declined to comment on its CEO succession.

Size matters and so does copper

Apart from the quest for scale to increase margins and contain costs, copper is a major reason for tie-ups in the mining sector.

The mass adoption of artificial intelligence and the transition across the world to cleaner energy have driven demand for copper as the most cost-effective metal to conduct electricity.

The advantage of mergers is that they can provide access to producing assets, avoiding the lengthy, costly and uncertain process of hunting for new reserves.

“The real read across from both this and the Anglo-Teck deal is in copper – we know that copper is attractive and that’s what buyers want access to,” said Kelly. If it does not bid successfully for Glencore, there are other possible targets to consider.

“Vale and Freeport are both going to be in focus – but it’s unlikely they’re for sale,” Kelly added.

Equally, BHP may decide it is better to do nothing, some analysts say.

“BHP has a cleaner growth profile in copper than a merged Rio/Glencore so I don’t think they need to do anything,” said Kaan Peker, an analyst at RBC.

“That said, if the transaction is successful, you might get some pressure with shareholders saying: ‘How come Rio pulled this off and you couldn’t with Anglo?’.”

(By Anousha Sakoui, Clara Denina, Melanie Burton and Charlie Conchie; Editing by Veronica Brown and Barbara Lewis)

Rio Tinto and Glencore hold buyout talks to create $207 billion mega-miner

Glencore currently operates 26 mines in 21 thermal and coking coal mining complexes across Australia, Colombia and South Africa. (Image courtesy of Glencore.)

Glencore and Rio Tinto said late on Thursday they were in early buyout talks that could potentially create the world’s largest mining company with a combined market value of nearly $207 billion.

Global miners are racing to bulk up in metals like copper, set to benefit from the global energy transition, and that has sparked a wave of project expansions and takeover attempts.

London-listed Anglo American and Canada’s Teck Resources are nearing the finish line on a merger to create a $53 billion copper-focused heavyweight.

The discussions between Rio Tinto and Glencore about combining some or all of their businesses are the second round of talks in just over a year between the two companies, after Glencore approached Rio Tinto in late 2024 but a deal did not proceed.

The two companies said one option would include an all-share buyout of Glencore by Rio Tinto. There was no certainty that the terms of any deal or offer would be agreed upon, the miners said after the Financial Times first reported the revived talks.

US-listed shares of Glencore were up 6% after the talks were confirmed. But Rio Tinto’s Australian-listed shares fell as much as 6.4%, the biggest intraday fall since July 2022, against a broader positive market.

“There is a risk (Rio) could overpay. It comes down to price, but if they have to pay a big premium there is a risk that a transaction could destroy some value for shareholders, said Tim Hillier, an analyst at fund manager Allan Gray, which is a Rio Tinto investor.

“Rio has a strong pipeline of internal high-growth projects. It’s not clear why they need to look externally for things to do,” he added.

Under UK takeover rules, Rio Tinto has until February 5 to make a formal offer for Glencore or say it will not proceed.

Rio Tinto, the world’s biggest iron ore miner, has a market capitalization of about $142 billion. Glencore, one of the world’s largest base metal producers, is valued at $65 billion as of its last close.

The transaction would be the world’s largest-ever mining deal if completed, according to LSEG data, and the market value of the combined company would top Australia’s BHP Group at $161 billion. BHP shares were up 0.6% in early Australian trade on Friday.

Cultural questions

Rio Tinto and Glencore restarted deal talks at the end of 2025, according to a source with knowledge of the matter.

Rio Tinto has undergone significant changes since the 2024 approach by Glencore. New Rio Tinto CEO Simon Trott was selected after the company’s chairman expressed a preference for a leader more open to large-scale deals than his predecessor, Jakob Stausholm, who was in charge when the miner turned down Glencore’s approach in late 2024.

Under Trott, who took over in August, Rio Tinto is focused on becoming leaner with fewer non-core assets.

Andy Forster, senior investment officer at Rio Tinto shareholder Argo Investments, said the deal made sense if the terms were right for both companies.

“The biggest question mark would be the culture of the two companies as Glencore clearly has trading background, is very opportunistic and results-focused, some of those aspects of their culture could actually be good for Rio,” he said. “I hope Rio stays disciplined but it makes sense to look at deals where value can be extracted by both parties.”

Rio Tinto and Glencore are both shifting their focus towards copper, a commodity expected to be in high demand as the world adopts greener forms of energy and the take-up of power-hungry artificial intelligence gains ground.

Before the deal talks were announced, Rio Tinto’s London-listed shares had risen 35% since Trott took over in August, while Glencore’s shares were up 41% over the same period in line with price increases for the materials they produce, particularly copper.

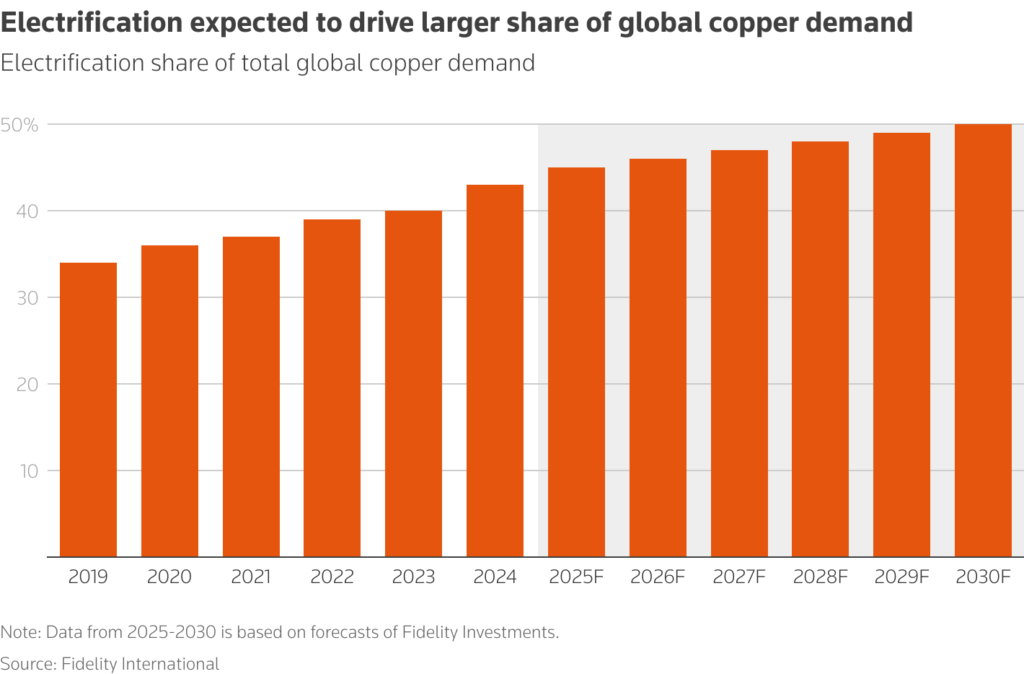

Growth in the artificial intelligence and defence sectors will boost global copper demand 50% by 2040, but supplies are expected to fall short by more than 10 million metric tons annually without more recycling and mining, consultancy S&P Global said on Thursday.

(By Clara Denina, Scott Murdoch and Shivani Tanna; Editing by Veronica Brown and Jamie Freed)

Rio-Glencore deal closer than ever with premium and CEO in focus

Glencore Plc boss Gary Nagle has called it the most obvious deal in mining. His predecessor and mentor Ivan Glasenberg has been trying to pull it off for nearly two decades. And yet the merger of Glencore with Rio Tinto Group has proven elusive – until now.

People familiar with the matter say that the current round of talks to create the world’s largest miner, which the two companies confirmed on Thursday night, are the most serious they have ever been, while emphasizing they are still at an early stage. At the heart of the shift is a concern within Rio that its iron ore-heavy portfolio could be left behind as copper M&A frenzy sweeps the sector, as well as a configuration of personalities on both sides who are better able to come to an agreement, the people said.

When the deal was last seriously discussed in late 2024, the talks foundered over Rio’s unwillingness to pay a big premium, as well as differences in the cultures fostered by Rio’s then-CEO and the Glencore leadership. At the time, Glencore pushed for Nagle to run the combined company.

Now Rio has a new boss and both sides appear more willing to compromise. Rio may ultimately consider paying a takeover premium, some of the people said, while other people suggested that the Glencore side is open to being pragmatic on the subject of management — recognizing that a larger firm paying a takeover premium would most likely seek to install its leadership in the new company.

What’s more, a shift in investors’ attitudes toward coal mining means that Rio could buy Glencore outright with less fear of a backlash. Bloomberg earlier reported that Rio was open to retaining Glencore’s vast coal business.

Still, talks are at a very early stage and the people cautioned that the two sides are still some way from reaching a deal. Even if they can, any combination would be highly complex and require the approval of numerous regulators at a time of heightened government scrutiny of natural resources.

“It does feel like these two sides want a deal,” said George Cheveley, a portfolio manager at asset manager Ninety One, who owns Glencore shares. “Glencore have a lot of brownfield and greenfield copper projects and Rio don’t, but Rio have the expertise to build them and run them.”

Representatives for Rio and Glencore both declined to comment.

In the 2024 talks, Glencore had asked for a merger ratio that would leave its shareholders with about 40% of the combined company, according to several of the people. If the same level remained a benchmark for Glencore’s negotiations, that would represent a premium of just over 25% relative to the two companies’ undisturbed share prices.

Two people familiar with Rio thinking said it may be willing to consider paying a takeover premium, although other people cautioned it was too early in the process to assess.

The idea of a combination of the two companies has been discussed several times over more than a decade. It was first floated before the global financial crisis of 2008, and then revived in 2014 – when Rio quickly rejected an informal approach from Glencore – before conversations resumed in earnest in 2024.

While those talks ended without a deal, the idea of combining the two companies never went away. Bloomberg reported last September that Glencore had continued to work behind the scenes with its bankers on the contours of a potential deal.

This time, it was Rio that re-initiated the most recent conversations, according to some of the people.

The miner had undergone a key change since the failed 2024 discussions: it had a new chief executive. Jakob Stausholm, a sober Dane with no background in the cut-and-thrust world of mining, had been asked by the board to step down, with his replacement announced as long-time Rio executive Simon Trott in July.

Equity markets have also moved in the larger miner’s favor as it mulls a possible all-share transaction, with Rio shares up about 26% between Bloomberg’s report on the 2024 talks and the close of trading on Thursday, compared with a 12% gain for Glencore. Rio closed down 3% in London on Friday, while Glencore jumped 9.6%.

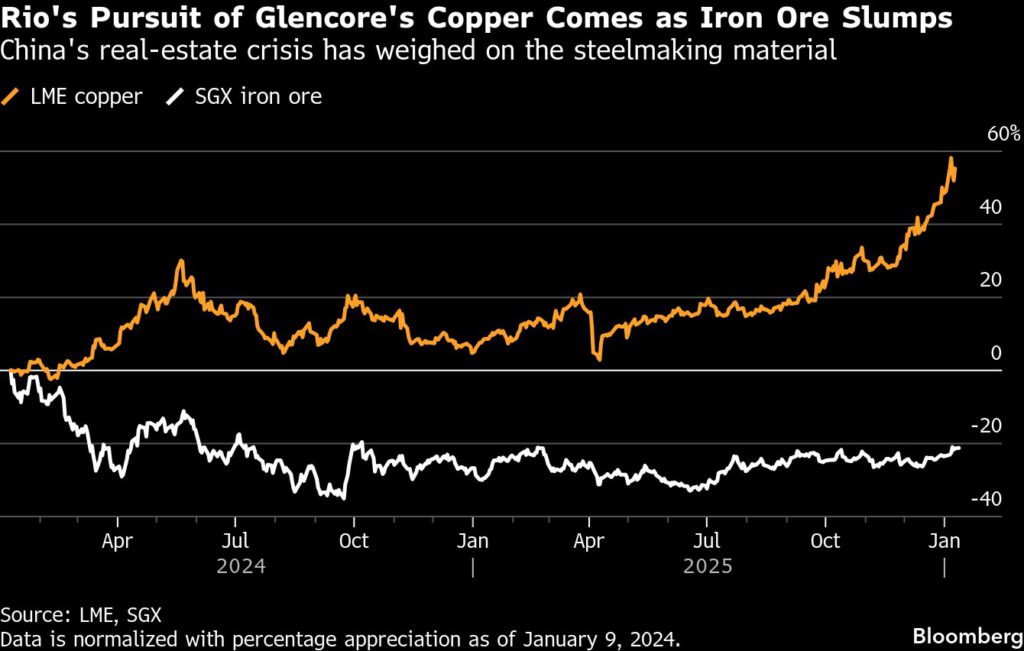

For Rio, the fundamental case for buying Glencore boils down to copper. While the miner is a significant player in markets from aluminum and copper to lithium, iron ore still accounted for more than half of its earnings in its most recent financial report.

The medium-term outlook for iron ore is downbeat, with China’s cooling property market sapping demand while Rio’s huge new project in Guinea is poised to flood the market with supply. Copper, meanwhile, has long been the most coveted metal for mining executives who see a bright future for the metal as the trend to electrification supercharges demand.

Rio has a relative dearth of copper development prospects as its vast Oyu Tolgoi mine in Mongolia reaches capacity. Glencore, on the other hand, spent an investor day last month highlighting its array of copper development options in Argentina, Peru and the Democratic Republic of Congo.

The company’s executives recognized that its own relative reliance on iron ore, together with Glencore’s growth plans if it is able to achieve them, meant that waiting would likely only make the deal more expensive, according to some of the people.

There remain many complexities to navigate, even if the two companies are able to agree terms. Glencore’s coal business is still problematic for some large Rio shareholders because of sustainability concerns. And other parts of its business – from its trading unit, which in 2022 admitted to widespread historical corruption, to its assets in countries like Congo and Kazakhstan – could prove unattractive to some.

The transaction structure is also likely to be complicated by Rio’s dual UK and Australian listings, while a successful deal would be scrutinized by antitrust regulators everywhere from China to Canada.

Still, speaking to Bloomberg on Friday, large shareholders of both companies were tentatively supportive of a potential deal.

“We’re not pushing for a deal, but we’re open to any and all options that create and highlight value for Glencore shareholders,” said Justin Hance, a partner at Chicago-based Harris Associates LP, which is Glencore’s 11th-largest shareholder, according to Bloomberg data. “The attractiveness of any deal would depend not only on the shareholder ratio, but also on the structure, terms, and finer details of the transaction.”

(By Thomas Biesheuvel, Dinesh Nair, Jack Farchy and Leonard Kehnscherper)

AU

Gold overtakes US bonds as largest foreign reserve asset

Gold has surpassed US Treasuries as the world’s largest reserve asset globally for the first time in 30 years amid rising prices and aggressive buying by central banks.

According to new data from the World Gold Council, the value of gold held by foreign central banks is now approaching the $4 trillion mark, more than their approximate $3.9 trillion holding in US Treasuries. The last time that foreign institutions held more gold than US bonds was 1996.

The shift coincides with rising gold prices, which recently crossed over the $4,500-an-ounce milestone during an end-of-year rally. The precious metal ended 2025 with a gain of nearly 70%, as geopolitical tensions and concerns over fiscal sustainability boosted its safe-haven appeal.

On Wednesday, gold prices briefly touched $4,500 an ounce again before paring gains to near the $4,500 level. In the first week of 2026, the yellow metal rose by 3.6%, extending last year’s scorching rally.

De-dollarization movement

Central banks, undeterred by high gold prices, have been accumulating bullion, with the WGC forecasting another 1,000 tonnes in net purchases for 2025. To analysts, this marked a structural shift in global reserve holdings, as foreign governments pivot away from dollar-denominated assets and into gold.

This shift — what they call de-dollarization — stems from the United States’ overall standing as the world’s leading economic, political and military power, said JP Morgan in a note last year. “Increased polarization in the US could jeopardize its governance, which underpins its role as a global safe haven,” it wrote.

Meanwhile, gold — traditionally seen as a much safer alternative to fiat currencies with no counterparty risk — has risen up the ranks. Over the last four years, foreign central banks have been buying the metal at a fast pace to safeguard themselves from any US geopolitical fallout.

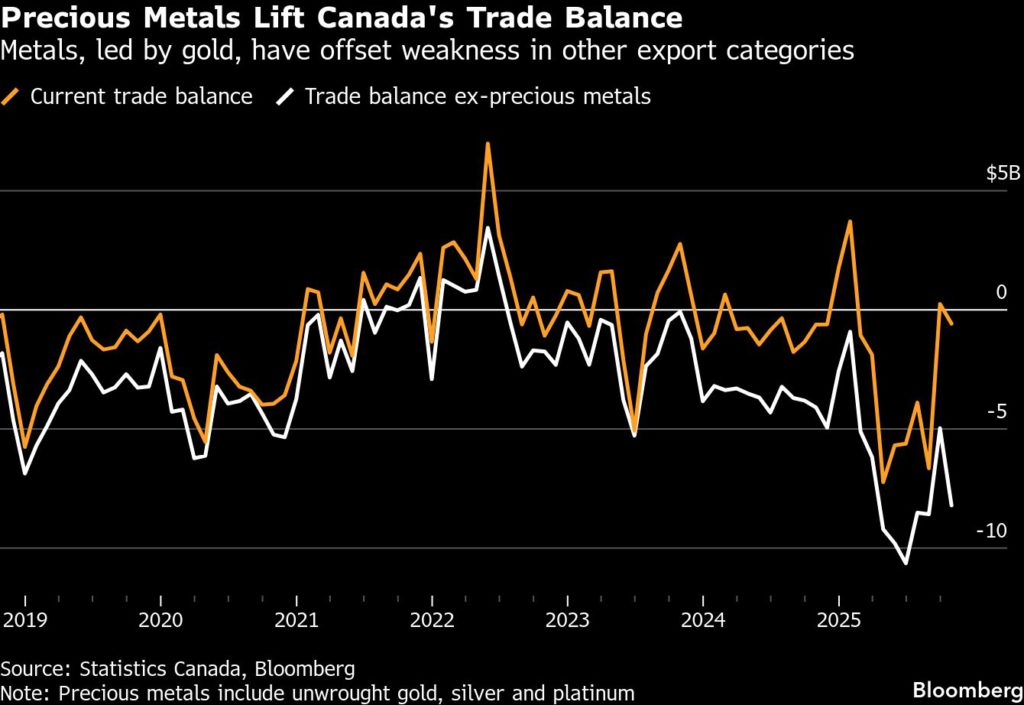

Gold exports mask weakness in Canada’s broader trade picture

Canada posted a C$583 million ($421 million) trade deficit in October, but surging precious metal exports — mostly gold — are doing a lot of heavy lifting. Strip those out, and Canada would have a C$8.2 billion shortfall.

The gap underscores how the country’s trade fortunes have become more dependent on global demand for bullion.

Gold prices have jumped as investors flock to safe‑haven assets due to rising geopolitical uncertainty. The rally is boosting the value of Canada’s precious metal exports, with shipment volumes growing too — just more slowly than prices. That’s helping steady Canada’s export performance even as US tariffs squeeze Canadian industries and weigh on global growth.

Strong gold shipments to the UK pushed Canada’s overall exports to non‑US countries to new heights in October. The share of Canada’s exports bound for the US fell to a record low, outside of the pandemic period.

“As of October, precious metals (unwrought + alloys) made up roughly 13% of Canadian exports,” Bank of Montreal economist Shelly Kaushik said in a note.

“For the first time on record (or 1997), that’s more than exports of oil or autos. Those two traditional heavyweights have, of course, been under pressure from lower prices and higher trade tensions, respectively. While Canada’s trade flows will continue to face headwinds amid geopolitical uncertainty, gold will remain a stalwart as long as prices hold up.”

(By Mario Baker Ramirez)

GNOMES OF ZURICH

Gold price surge boosts Swiss National Bank’s profit

The Swiss National Bank made a profit of around 26 billion Swiss francs ($33 billion) in 2025, the central bank said on Friday, thanks to a sharp increase in gold prices as investors headed for safe-haven assets last year.

The provisional figure was down from the record 80.7-billion-franc profit in 2024, but still ranked among the top five in the SNB’s 119-year history.

The 2025 result was driven by a 36.3-billion-franc valuation gain on its gold holdings, as investors piled into the precious metal to shield against global economic turmoil triggered by US President Donald Trump’s tariffs.

The SNB’s gold profit was its biggest ever, helped by a 64% rise in the metal’s price last year, lifting the value of its 1,040 metric tons of reserves.

Foreign currency losses

The central bank’s profits were capped by a 9-billion-franc loss on foreign currency positions as the franc’s strength erased valuation gains on equities and dividends.

The SNB, which holds 37% of its 764 billion francs in foreign currency investments in US dollar assets, was hit by the dollar’s 13% slide against the franc in 2025, analysts said.

“The flight to safety had a mixed effect for the SNB in 2025,” said UBS economist Alessandro Bee.

“On one hand it was helped by a big increase in the price of gold, but on the other hand the Swiss franc – another safe haven – gained in value which turned the gains on foreign equity markets into losses when converted back into francs.”

Bee estimated that foreign exchange moves ultimately cost the SNB around 55 billion francs last year.

The bank also booked a 900-million-franc loss on its Swiss franc positions, mainly due to interest payments to commercial banks with sight deposits.

The overall profit was in line with UBS’ forecast of 23.5 billion to 28.5 billion francs.

($1 = 0.7996 Swiss francs)

(By John Revill; Editing by Miranda Murray and Mark Potter)

Philippine central bank gold holdings jump 70% in 2025 to record

The value of the Philippine central bank’s gold holdings surged almost 70% last year to a record high as the metal jumped.

Gold holdings rose to an all-time high of $18.6 billion at end-2025, according to central bank data released late Wednesday. They accounted for about 17% of its foreign-exchange reserves – a ratio officials had said exceed the ideal.

The rise in the central bank’s gold holdings reflects the surge in the metal, which jumped more than 60% last year. Bangko Sentral ng Pilipinas does not report the volume of its gold holdings.

Ideally, the precious metal should be anywhere between 8%-12% of the total reserves, Monetary Board member Benjamin Diokno said in October.

China’s central bank buys gold for 14th consecutive month

China’s central bank continued gold purchases for a 14th straight month, with gold holdings amounting to 74.15 million fine troy ounces at the end of December, from 74.12 million in the previous month.

The value of China’s gold reserves increased to $319.45 billion at the end of last month, from $310.65 billion a month earlier, data from the People’s Bank of China showed on Wednesday.

(By Qiaoyi Li and Ryan Woo; Editing by Bernadette Baum)

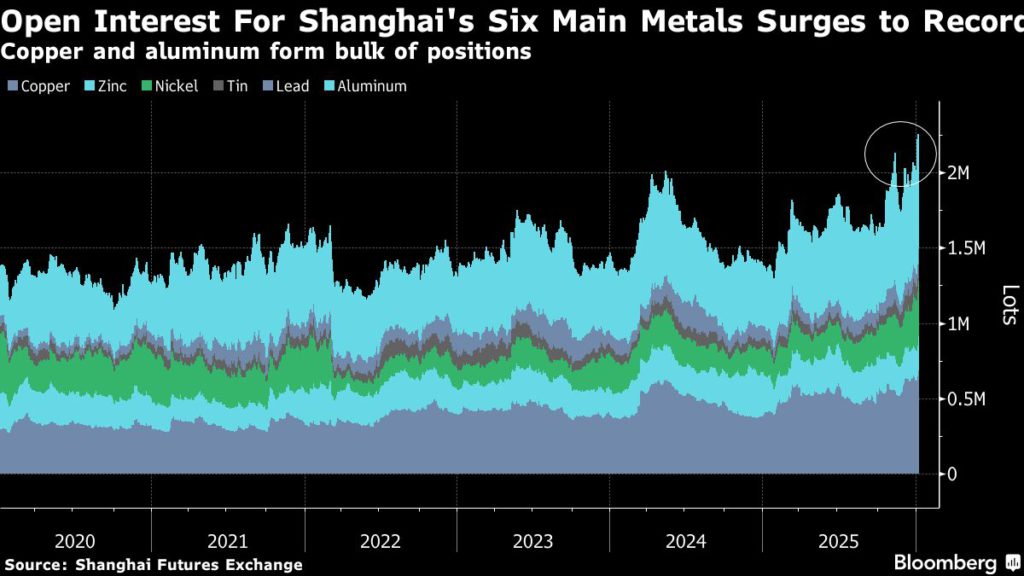

China’s metals in grip of frenzy as investors bet on rally

China’s metal markets are in the grip of a speculative frenzy, with trading values in Shanghai surging more than 260% from a year earlier, as traders and deep-pocketed funds pile into commodities like copper, nickel and lithium.

Open interest has surged to a record across the six base metals traded in Shanghai, pointing to robust sentiment as investors bet on global supply tightness, resilient industrial demand and a more supportive interest-rate backdrop in China and the US. Heightened geopolitical risks have added to the rush into raw materials.

The total turnover of the Shanghai Futures Exchange’s six base metals contracts, plus gold and silver futures, reached 37.1 trillion yuan in December – equivalent to more than $5 trillion. By trading volume, Dec. 29 was the single busiest day for copper in more than a decade.

As well as general supply tightness, metals are finding support from monetary easing by central banks. Lower interest rates typically encourage investors to buy non-yielding assets like metals. A weaker dollar is also a tailwind, with investors piling into the so-called debasement trade.

“We’ve seen significant macro allocation flows into commodities,” said Jia Zheng, head of trading at Shanghai Soochow Jiuying Investment Management Co., adding that some equity funds are betting commodity futures will rise alongside stocks this year.

Nickel – used in stainless steel and batteries – advanced nearly 6% on the Shanghai Futures Exchange on Wednesday. The most-active aluminum contract closed at its highest since 2021, while copper has shot beyond a milestone 100,000 yuan a ton, defying some bearish signs in the local market including rising inventories.

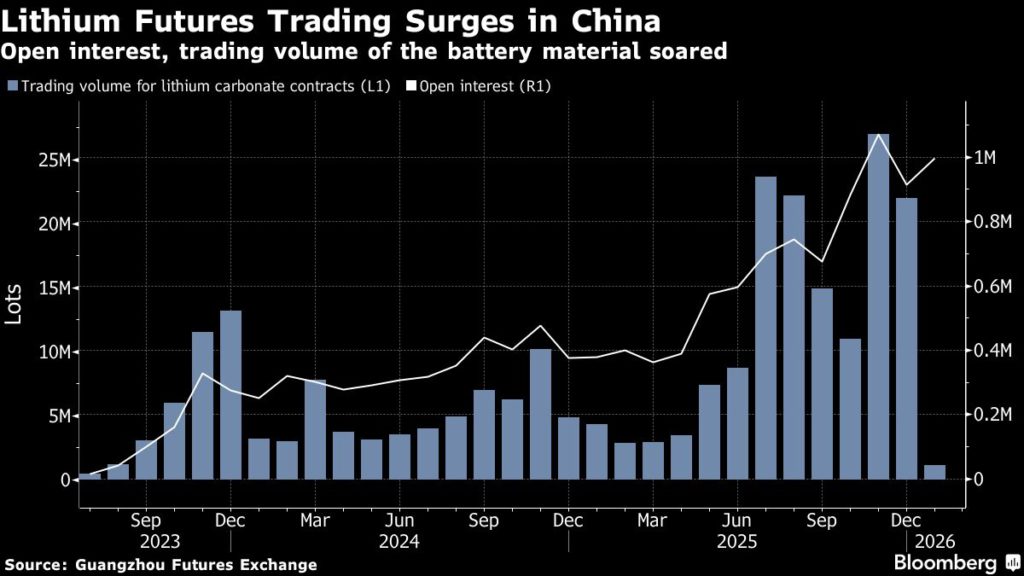

Turnover on the Guangzhou Futures Exchange — including lithium, palladium, platinum and silicon futures — was around 5.6 trillion yuan in December. This was more than six times higher than the same month in 2024, although some of the Guangzhou contracts are relatively new.

But questions remain as to whether the scorching rallies have run too far, too fast. As the bull run accelerated in the second half of last year, some of the new capital invested was speculative, said Chi Kai, chief investment officer at Shanghai Cosine Capital Management Partnership.

“This market will test trading skills,” he said. “Easy profits won’t come simply by holding positions – and the risks are increasing.”

Volatility is becoming an increasing risk, especially in Guangzhou, where a platinum contract launched at the end of November has already traded either limit-up or limit-down on eight occasions.

From mid-December, the Guangzhou bourse also capped new positions and raised fees for lithium carbonate after the contract rallied 35% in the space of around seven weeks. Though open interest has retreated since then, it remains at a historically elevated level. The most-active lithium futures contract rose 4.5% on Wednesday.

The Shanghai Futures Exchange will also raise the trading margin and daily price limit for some silver futures from Friday, according to a statement from the exchange. The bourse urged investors in a separate statement to invest rationally, citing recent developments that have caused volatility in metal prices.

With base metals starting the year strongly — copper hit a record on the London Metal Exchange earlier this week and the LMEX Index that tracks the six main metals surged to the highest level since 2022 — Chinese investors are likely to stick around. This is reinforced by the presence of macro funds, which tend to hold their positions longer, Shanghai Soochow’s Jia said.

“Looking ahead to the next six months, under the broad backdrop of monetary easing in China and the US, macro capital is unlikely to exit,” she said.

Stock image.

Stock image.

Nickel pig iron plant in Indonesia. (Image from Nickel Mines Ltd.)

Nickel pig iron plant in Indonesia. (Image from Nickel Mines Ltd.)