It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Wednesday, January 14, 2026

Kal Tire’s Mining Group, Decoda team up to develop KalPRO HaulSight

Kal Tire’s Mining Tire Group and Australian mining technology firm Decoda have announced a strategic alliance that the companies say will bring mines real-time, autonomous haul road hazard detection to increase truck productivity, tire life and fuel efficiency.

Kal Tire and Decoda have collaborated to develop KalPRO HaulSight, which builds on the momentum of KalPRO TireSight autonomous tire inspections.

“HaulSight’s ability to detect road hazards as they arise means mines can prevent the tire damage that TireSight detects,” Kal Tire’s technology services director Christian Erdelyi said in a news release.

“We’re excited about how this collaboration with Decoda will further our achievements in the autonomous space to bring customers even greater improvements to tire life, productivity and fuel efficiency.”

With Decoda’s LiDAR and camera sensors mounted to the front and rear of haul trucks, and an ‘edge’ computer processing live footage, HaulSight gives fleet teams instant alerts about hazards such as spillage, road undulations and high G-force events that can cause truck and tire damage and slow down operations, the company said.

Modeling TireSight, HaulSight’s scanning technology integrates with Kal Tire’s TOMS (Tire & Operations Managing System) and allows condition monitoring experts to assess flagged issues and automate priority-based work orders.

“HaulSight gives mine sites unprecedented visibility across the entire haul circuit and turns that insight into action. By making critical data easy to visualize and act on, operations see measurable improvements, like faster circuits and reduced downtime, from day one,” George Spink, Decoda’s executive general manager, stated.

“Leveraging Kal Tire’s longstanding relationships means we have the chance to bring these benefits to more mines.”

HaulSight enables road crews to react quickly and create optimal road conditions that maximize cycle speed and fuel use. When long-term planning opportunities arise, HaulSight calculates the cost to lost tire life, productivity and fuel against the cost of a road improvement.

“The responsiveness of the system means mine sites benefit right away with trucks spending more time hauling, but HaulSight also offers long-range planning insights that enable confident decision-making around tire maintenance and road upgrade investments,” Erdelyi added.

To ensure HaulSight is just as effective in sub-zero conditions, testing began on Canadian mine sites 18 months ago with strong results, the companies said, adding that since no two mines are alike, and no two roads even within a site are alike, HaulSight’s real-time feedback option can guide truck operators into loading or dumping spots to avoid impacts with road hazards.

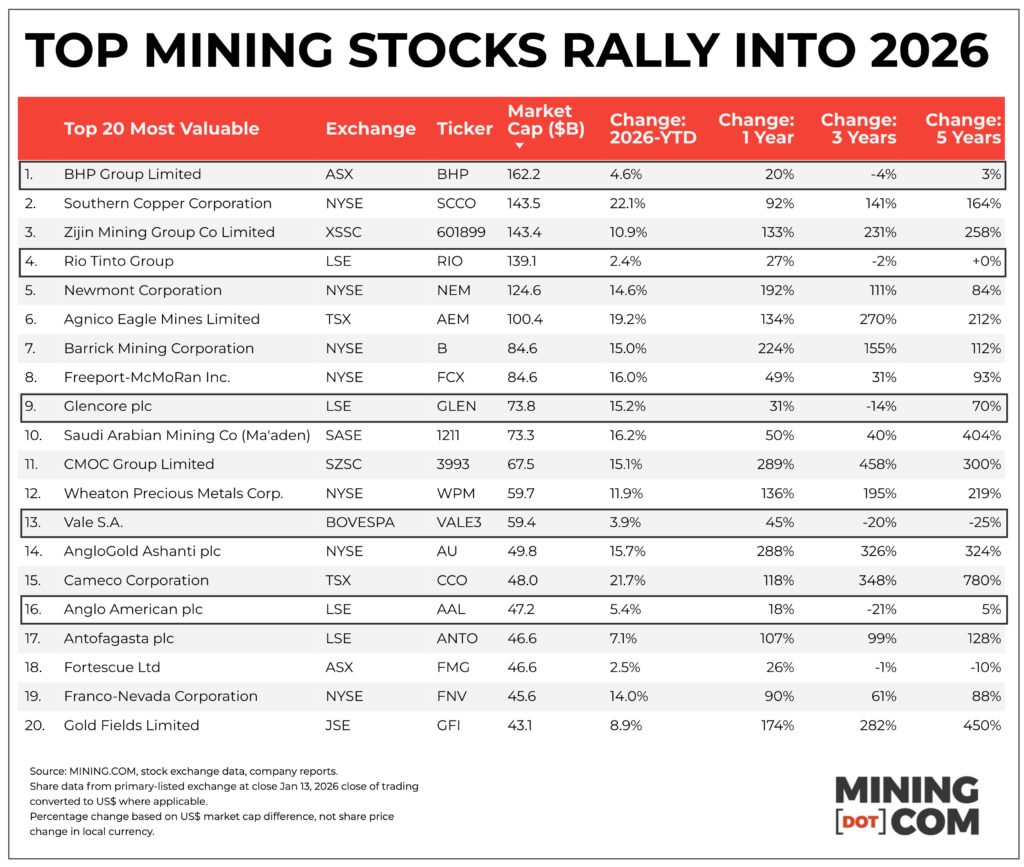

Rio Tinto kicked off number 2 perch, Agnico tops $100 billion for the first time

Global mining started 2026 the way it ended 2025 – with a huge rally.

Gold now looks to have $5,000 in sight, silver’s wild swings are getting wilder, and copper is hitting all time highs with regularity.

Mining stocks have duly responded, and after a blowout 2026, the Top 50 biggest mining stocks’ collective value now sits comfortably above the $2 trillion level reached at the end of last year.

You have to scour the corners of the mining world to find something that’s down and titanium and silicon are not exactly pillars of the industry.

While the metal and mineral price rally is broadbased and most mining stocks in the upper echelons already sport double digit percentage gains YTD, a few underperformers stand out. Stocks of the losers (or small gainers) appear to be driven by factors beyond buoyant metal prices.

Global mining is beefing up – and that’s before the mergers and acquisition currently being discussed.

Since inception, the MINING.COM TOP 50 was headed by two firms – BHP and Rio Tinto – the only miners with consistent market capitalizations above $100 billion (with a wobble here and there).

Now there are six firms with the distinction. The latest is Agnico Eagle, (TSX:AEM) which on Tuesday entered the ranks of the triple digit billion dollar miner. If only just.

The Toronto-based company joins Chinese champion Zijin Mining (SHA: 601899), Southern Copper (NYSE: SCCO), the mining arm of Grupo Mexico, and Denver’s Newmont Corporation (NYSE: NEM) which rode gold and copper prices all the way to the top towards the end of last year.

While the ascent of these counters is not surprising given gold’s glorious run and copper’s inexorable climb, the recent underperformance of BHP (ASX:BHP) and Rio Tinto (LSE:RIO), appears to have more to do with doubts over M&A.

While there is little separating them, it is striking that Rio Tinto is now in position number four, below Southern Copper and Zijin. Rio Tinto is up 2.2% on the LSE so far this year at $140.8 billion. Zijin has added 11% in Shanghai in USD terms while Southern Copper has surged by 22% in New York just eight trading days in.

In fact Rio Tinto and BHP (up 4.6% for $162 billion) are some of the only counters that have not seen double digit gains in 2026. Rio Tinto has received the sharp end of investor skepticism over a combination with Glencore.

Glencore in turn has gained 15.2% in value in London to $73.9 billion. The talks between Baar and Melbourne date back more than a year and investors have had ample time to digest its prospects.

The downsides of a deal for Rio Tinto, apart from what to do with coal, do not seem insurmountable while the upsides when it comes to copper are obvious. A merged entity would become the clear copper king with attributable production of roughly 1.6 million tonnes a year by 2028 – and when Glencore’s projects come on stream in the early 2030s it could hit 2m tonnes-plus (versus BHP and Codelco’s 1.3m tonnes).

Rio Tinto just this week appointed three investment banks to give advice so at least who needs who more may soon become apparent.

BHP’s lacklustre performance also appears to have an M&A angle, this time because the company has been relegated to the sidelines after more than one failed attempt over the years (including with Rio Tinto) while others partner up.

Today a RioCore would be worth not that much more than $200 billion (a number the likes of GOOG gains or gives up in an afternoon) and it’s easy to forget that BHP flirted with this level all the way back in April 2022 when it briefly displaced oil major Shell as the most valuable stock on the FTSE.

Trading in two other merger candidates has also been uninspiring. Anglo American (LSE:AAL) stock rose by 5.4% by Tuesday for a $46.7 billion valuation while Teck Resources (TSX:TECK.B) is 5.2% for the better at $24.3 billion in Toronto (well outside the top 20).

BHP’s odd last-minute intervention aside, AngloTeck is coming closer to reality with the EU poised to also clear the deal within weeks. At current prices a combined entity would only just make it into the top 10. That Anglogold Ashanti (NYSE:AU) is now worth more than its erstwhile parent must sting in the offices of 17 Charterhouse (slated for evacuation).

Apart from an operational level agreement with Glencore to explore in Canada’s Sudbury basin, absent from the conversation has been Vale (BOVESPA:VALE3).

Long the number three most valuable and for a day or two in 2022 also worth more $100 billion, the Brazilian miner continues to drift down the ranking. An IPO for the Rio de Janeiro-based company’s base metals unit would be in 2027 by the earliest.

Mining’s traditional big 5 diversified giants – BHP, Rio Tinto, Glencore, Vale and Anglo American – that trace their roots back many decades if not more than a century, not that long ago occupied the top five spots as a matter of course and constituted nearly a third of the overall value of the Top 50.

It is not just their recent performance that stands out, when looking at a three-year (or even five-year) chart it is hard not to conclude that the old guard has not kept up with the new world of mining.

Among spectacular gains for copper, gold and other commodity specialists with three/four or sometimes eight-fold gains in value since 2022, the geographically spread out, diversified mining model remains in the red.

And mergers and acquisitions and spinoffs and bolt-ons, it seems, do not provide solutions for this perennial disappointment.

Gold bars and coins. (Image by Zlaťáky.cz, Pexels.)

Gold vaulted above the historic $4,600 an ounce mark on Monday as a flare-up in geopolitical tensions and expectations of looser US monetary policy led bullion to hit its first record peak of 2026 after a string of all-time highs last year.

Here are some ways to invest in gold:

Spot market

Large buyers and institutional investors usually buy gold from big banks. Prices in the spot market are determined by real-time supply and demand dynamics.

London is the most influential hub for the spot gold market, with the London Bullion Market Association setting standards for gold trading and providing a framework for the over-the-counter market to facilitate trades among banks, dealers, and institutions.

China, India, the Middle East and the US are other major gold-trading centres.

Futures market

Investors can also get exposure to gold via futures exchanges, where people buy or sell a particular commodity at a fixed price on a particular date in the future.

COMEX, part of the New York Mercantile Exchange, is the largest gold futures market in terms of trading volumes.

The Shanghai Futures Exchange, China’s leading commodities exchange, also offers gold futures contracts. The Tokyo Commodity Exchange, popularly known as TOCOM, is another big player in the Asian gold market.

Exchange-traded products

Exchange-traded products or exchange-traded funds issue securities backed by physical metal, allowing people to gain exposure to gold prices without taking delivery of the metal itself.

Global gold ETFs witnessed the strongest year of inflows on record in 2025, led by North American funds, according to World Gold Council data. Annual inflows surged to $89 billion.

Bars and coins

Retail consumers can buy gold from metals traders selling bars and coins in shops or online. Gold bars and coins are both effective means of investing in physical gold.

What drives the market?

Investor interest and market sentiment

Rising interest from investment funds in recent years has been a major factor behind bullion’s price moves, with sentiment driven by market trends, news and global events fuelling speculative buying or selling of gold.

Foreign exchange rates

Gold is a popular hedge against currency market volatility. It has traditionally moved in the opposite direction to the US dollar, since weakness in the US currency makes dollar-priced gold cheaper for holders of other currencies and vice versa.

Monetary policy and geopolitical tensions

The precious metal is widely considered a safe haven during times of uncertainty.

US President Donald Trump’s trade tariffs have over the last year sparked a global trade war, rattling currency markets. Trump’s capture of Venezuelan leader Nicolas Maduro and aggressive statements on acquiring Greenland are adding to market volatility.

Global central banks’ policy decisions also influence gold’s trajectory. Lower interest rates reduce the opportunity cost of holding gold, since it pays no interest.

Central bank gold reserves

Central banks hold gold in their reserves, and demand from this sector has been robust in recent years because of macroeconomic and political uncertainty.

The World Gold Council said in its annual survey in June that more central banks plan to add to their gold reserves within a year despite high prices.

Net central bank purchases in November totalled 45 metric tons, World Gold Council data showed, pushing the figure for the first 11 months of 2025 to 297 tons as emerging market central banks continued their significant gold buying.

China kept adding gold to its reserves, with its holdings totalling 74.15 million troy ounces at the end of December from 74.12 million in the previous month as it extended its buying spree for the 14th month in a row.

(Compiled by Bangalore commodities and energy team; Editing by Peter Graff and Jan Harvey)

Caledonia plans to spend $132 million on Zimbabwe’s biggest gold mine this year

Caledonia Mining is weighing its options on how best to press the Bilboes gold mine in Zimbabwe back into service. Credit: Caledonia Mining

Caledonia Mining Corporation plans to spend $132 million this year to launch development of what, once operational, will be Zimbabwe’s largest gold mine, the company announced on Wednesday.

Miners are riding a wave of record bullion prices to expand output. Spot gold prices hit another record high of $4,639.48 an ounce early on Wednesday, fueled by escalating tensions in Iran, concern over the Federal Reserve’s autonomy and softer inflation readings that boosted rate cut bets.

Caledonia said in a production update that the planned spending, part of a $162.5 million total capital expenditure program for 2026, was subject to board approval and availability of funding.

Caledonia, which already operates the 80,000-ounce-per-year Blanket mine in Zimbabwe, plans to develop the Bilboes mine at a projected total capital cost of $584 million.

Production from the new mine is expected to begin in late 2028, with steady-state annual output of 200,000 ounces anticipated from 2029 for an initial period of 10 years.

The company has said it plans to fund the Bilboes project through a mix of non-recourse senior debt, contributions from existing operations as well as specialized financing methods such as streaming, where investors provide cash in return for future metal supply.

Caledonia’s expansion plans received a boost last month when Zimbabwe’s government reversed plans to double the gold royalty rate and change the tax treatment for capital expenditure.

(By Chris Takudzwa Muronzi; Editing by Nelson Banya and Joe Bavier)

Bharat Coking Coal draws $13 billion bids in India IPO

Bharat Coking Coal drew bids worth 1.17 trillion rupees ($12.97 billion) for its $118.7 million initial public offering on Tuesday, as prospects of strong demand for coking coal from steelmakers lifted appetite for the shares.

The company, which is India’s top coking coal miner, received bids for 50.93 billion shares, nearly 147 times the number of shares on offer, at the end of three days of bidding, as per exchange data.

The firm is a subsidiary of state-owned Coal India.

The strong response underscores continued investor interest in Indian primary market after two years of record fund-raising.

Bharat Coking Coal is the first mainboard IPO in India this year and consists entirely of a stake sale by its parent.

India ranked as the world’s second-largest primary market in 2025 after the United States, with 367 IPOs raising $21.8 billion, according to LSEG data.

Offerings from companies such as LG Electronics India and ecommerce platform Meesho drew strong demand during the year.

“Despite turbulence in the secondary market, this shows that primary market remains buoyant. The investor interest in Bharat Coking Coal is also driven by its strong parentage,” said Kranthi Bathini, director of equity strategy at WealthMills Securities.

“The Indian coking coal industry benefits from structural demand growth driven by government-led infrastructure development, capacity addition in steel manufacturing, and policy emphasis on import substitution,” said Ventura Securities.

Qualified institutional buyers bid for 24.61 billion shares of Bharat Coking Coal, about 311 times the number of shares on offer for them, leading the subscriptions.

Non-institutional investors and retail investors quota were subscribed 258 times and 49 times, respectively.

($1 = 90.1780 Indian rupees)

(By Vivek Kumar M; Editing by Nivedita Bhattacharjee)

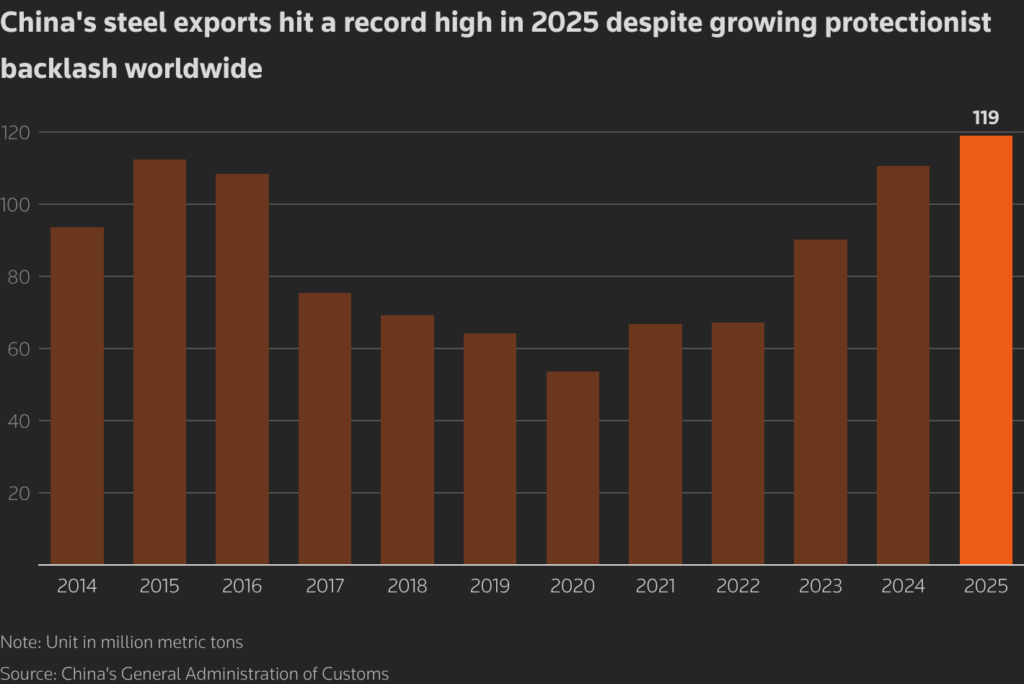

China’s steel exports, iron ore imports hit record highs

China’s steel exports hit a record monthly high in December, fueled by front-loading driven by Beijing’s announcement of an export licence requirement for shipments from 2026.

The world’s largest steel producer shipped 11.3 million metric tons of the metal used in construction and manufacturing last month, the highest for a single month, data from the country’s General Administration of Customs showed on Wednesday.

Beijing has plans to roll out a licence system from 2026 to regulate steel exports, as robust shipments have sparked a growing protectionist backlash worldwide.

Some exporters rushed to ramp up shipments before January on fears that the export licence requirement might impact shipments, analysts said.

Despite surprisingly high exports, China’s prolonged property market woes have remained a drag on steel consumption.

China’s steel demand is projected to slide by 1% this year after an annual fall of 5.4% in 2025, according to a forecast from a state-backed research agency.

Steel exports for the whole year rose by 7.5% from the year before to an all-time high of 119.02 million tons despite an increasing number of countries throwing up trade barriers on Chinese steel arguing that domestic manufacturing has been hurt.

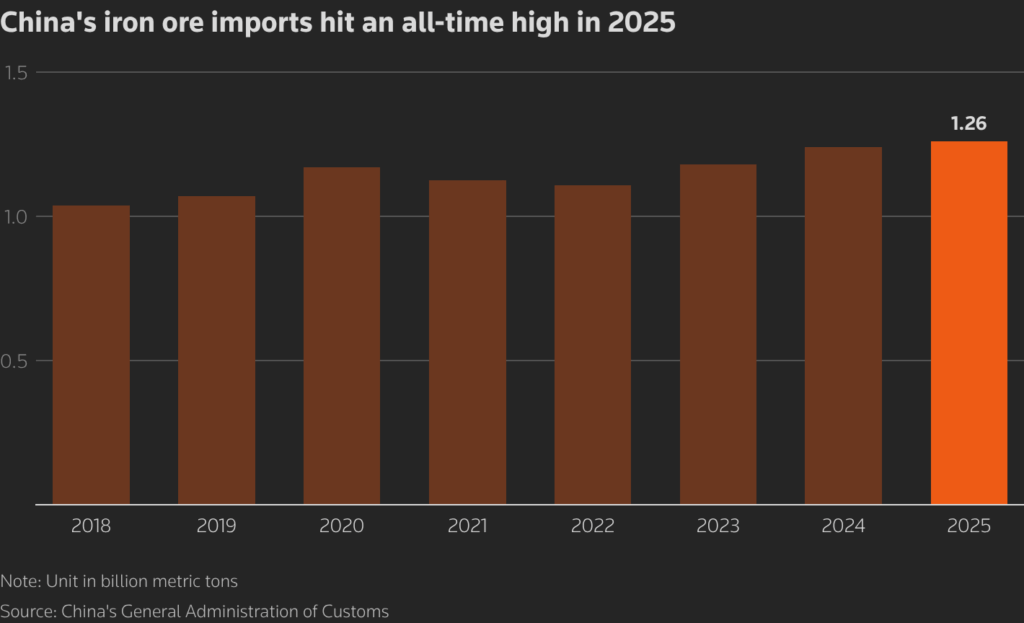

Iron ore imports at record

Iron ore imports in the world’s largest consumer hit a record high last year as low in-plant inventories and improved steel margins encouraged mills to book more cargoes.

Chinese steelmakers have kept low inventories at plants since late 2022 as a demand slump caused by the crisis-hit property market strained their cash flow.

Moreover, robust steel exports underpinned resilient demand for the key steelmaking ingredient, analysts said.

Imports in December rose 8.2% from the month before to 119.65 million tons, the highest for a month, bringing the total in 2025 to a record high of 1.26 billion tons with a rise of 1.8% from 2024.

Global iron ore supply is forecast to grow by 2.5% in 2026, and shipments to China are expected to increase by between 36 million and 38 million tons, piling pressure on prices this year, said Bai Xin, an analyst at consultancy Horizon Insights.

(By Amy Lv and Lewis Jackson; Editing by Jacqueline Wong and Tomasz Janowski)

Congo pitches new $29 billion iron ore and logistics project

The Democratic Republic of Congo, one of the world’s biggest producers of copper and cobalt, wants to add a $29 billion iron ore project to its mineral portfolio.

The country’s government has created a project called Mines de Fer de la Grande Orientale, or MIFOR, to develop a particularly rich seam of ore in the remote north of the country, Mines Minister Louis Watum told the council of ministers Friday, according to minutes published on the website of the office of the prime minister. The deposit has an estimated 20 billion tons of resources at an average grade of 60%, he said.

The first phase of the project would require the construction of heavy rail and transport on the Congo River to the deep-water port of Banana on the Atlantic Ocean and cost $28.9 billion, Watum said. Initial production capacity would be approximately 50 million tons per year, expandable to 300 million tons, Watum told the council.

“After more than 100 years of mining primarily focused on copper and cobalt, the MIFOR project marks a major strategic shift in the Democratic Republic of Congo’s extractive model,” Watum said, according to the minutes.

The project has already attracted institutional investors, he told the council, which agreed to create an inter-ministerial commission dedicated to the project.

(By Michael J. Kavanagh)

Radiant unloads BHP iron ore in China as trader tests curbs

A bulk carrier laden with BHP Group’s Jimblebar iron ore has discharged in China after weeks idling offshore, in a rare case of a trader pressing ahead with restricted cargoes despite an ongoing pricing dispute.

The Berge Mawson unloaded its cargo, owned by trading firm Radiant World, at the northern port of Caofeidian in the first week of January and has now left the country, Bloomberg ship tracking data show. The vessel saw lengthy delays after port storage constraints led to a backlog of ships waiting to offload cargoes.

The Jimblebar Fines blend is one of the BHP products subject to curbs imposed by China’s state-run iron ore trader. The nation is the world’s largest buyer of the steelmaking staple and BHP one of its biggest suppliers. As such, the fate of the cargo has become a focal point for traders wanting to gauge whether restricted material can ultimately be sold in the country, according to people familiar with the matter.

Radiant World is a private trading company that has grown rapidly in recent years to become one of the largest players in the market. The Berge Mawson had been anchored off the coast since early December before finally docking on Dec. 31.

It isn’t clear whether Radiant has found a buyer, or whether the ore is stacked up at the port and yet to clear customs. Prolonged delays to shipments threaten to tie up vessels and raise demurrage and storage costs.

BHP is locked in a dispute with China Mineral Resources Group Co., the state-run firm set up in 2022 to consolidate iron ore purchases and wrest pricing power away from foreign miners. Although CMRG told steelmakers in September to stop purchasing Jimblebar, there may be mills that aren’t linked to the state-owned firm willing to take the product. Others might seek special approval from CMRG.

Radiant World and BHP both declined to comment. CMRG didn’t respond to a request for comment. Another vessel loaded with BHP ore that’s being closely watched by traders, the Ever Shine, has been idling off the port of Qingdao since early December

CMRG is also in talks with BHP’s Australian peers, Rio Tinto Group and Fortescue Ltd., for long-term supply deals in 2026. Meanwhile, Chinese customs has been stepping up checks to screen for cargoes of BHP ore, said two of the people, who declined to be named discussing a sensitive matter.

China’s customs administration didn’t immediately respond to a fax seeking comment.

Taylor Swift’s vintage ring shines new light on diamond industry

Taylor Swift’s engagement ring, featuring a large, antique Old Mine Cut diamond. (Image courtesy of Taylor Swift | Instagram.)

Some in the battered diamond industry believe an unlikely figure, pop star Taylor Swift, may have done more to revive interest in natural diamonds than years of marketing campaigns.

Diamond industry analyst Edahn Golan says the so-called ‘Swift effect’ follows a familiar pattern. “Celebrity style has long played a role in driving attention toward particular jewelry designs and diamond trends, with high-profile examples including Jennifer Lopez and Kobe Bryant,” he notes.

Lab-grown diamonds now account for more than half of engagement rings sold in the US, according to The Knot wedding website, up sharply from 2019, as prices have collapsed amid oversupply from China and India. A one-carat lab-grown solitaire can retail for as little as $150 at Walmart, while the gap with natural stones can reach 90%.

They have significantly less resale value than natural diamonds, however, often dropping up to 40% of the original price due to their mass-producible nature, unlike rare natural stones.

The impact on miners has been severe. Botswana, the world’s leading exporter of natural diamonds, has been forced into production cuts and job losses as revenues fall. Debswana, its joint venture with De Beers, is estimated to have cut output by as much as 40% in 2025.

De Beers itself has stockpiled roughly $2 billion worth of unsold stones, cut prices by more than 10% in 2023 and announced plans to shed more than 1,000 jobs. Parent Anglo American (LON: AAL) has moved to sell the business as it pursues a merger with Canada’s Teck Resources (TSX: TECK.A, TECK.B; NYSE: TECK). Russia’s Alrosa saw profits plunge nearly 80% and suspended activity at key sites, which helped it end the year in a better shape than expected. Smaller miners entered administration or shut mines entirely.

Governments and producers are now scrambling to defend the sector’s relevance. Under the Luanda Accord, countries including Botswana and Angola agreed to spend 1% of annual diamond revenues on a global campaign to revive demand for natural stones.

Celebrityeffect

Against this bleak backdrop, Swift’s engagement ring has landed like a cultural shockwave. Designed by New York jeweller Kindred Lubeck, it features a large old-mine-cut natural diamond set in hand-engraved yellow gold. This contrasts sharply to the sleek, minimalist solitaire styles popularized in recent years. Industry experts estimate the stone weighs between seven and ten carats.

Independent sector analyst Paul Zimnisky told MINING.COM that celebrity engagement rings have always driven positive attention toward the diamond industry.

Old-mine cuts date back to the 18th and 19th centuries, when diamonds were shaped by hand under candlelight, producing chunky facets, open culets and warmer light than modern round brilliants.

“Not just Taylor Swift, but also Zendaya and Miley Cyrus, have garnered significant publicity over the last year with diamond rings fit for a fantasy,” Zimnisky said. “All three feature large stones, but all are unique in style: Swift’s antique-cut diamond, Zendaya’s east-west setting and Cyrus’s bezel.”

Once a niche obsession among collectors, the style exploded across social media after Swift’s engagement became public.

“What a diamond!” De Beers CEO Al Cook wrote on LinkedIn, calling it a reminder that every natural diamond is “a unique and ancient treasure from the Earth.”

Dealers say the attention has triggered renewed interest in antique and heritage stones, which offer something lab-grown diamonds cannot easily replicate: scarcity and story. At Sim Gems USA in New York’s diamond district, president Chirag Mehta said clients are increasingly looking for stones that feel different from mass-produced brilliance. “People know what a round brilliant is,” he told The New Yorker earlier this month. “After what happened, they’re looking for something else.”

A new narrative

For an industry built on marketing, that shift matters. “Diamonds are all about emotion, romance and selling a dream, and the industry thrives on PR like this,” Zimnisky noted.

Lab-grown diamonds excel at purity and price, undermining a century-old message that equated value with flawless, colourless stones. Now, natural-diamond producers are reframing rarity around character, age and provenance, even embracing once-shunned brown or “textured” stones.

Zimnisky said the renewed attention has coincided with a clear shift in buying preferences. There has been an uptick in larger natural diamond sizes in fancy-cut shapes such as long cushions, marquis and ovals, with 2–4-carat elongated fancy shapes emerging as the hottest category over the past year.

Cristiano Ronaldo proposed to Georgina Rodríguez in 2025 with an extravagant engagement ring featuring a 25-30+ carat oval-cut diamond centrepiece, flanked by smaller diamonds in a platinum setting. (Image courtesy of Georgina Rodríguez | Instagram.)

Antique diamonds also offer a perceived ethical middle ground for buyers wary of mining but unconvinced by lab-grown gems, though their supply remains limited and their histories complex.

Whether Swift can truly “save” the industry is doubtful, but her ring has given natural diamonds something they desperately need: cultural relevance. In a market where consumers can buy size and sparkle for a fraction of the cost, miners are betting that romance, individuality and celebrity influence still have the power to sell a story.

Congo readies to pitch mineral projects to US investors

Tenke Fungurume mine is one of the largest producers of copper and cobalt in the DRC. (Image courtesy of CMOC.)

The Democratic Republic of Congo is sending the United States a list of mineral projects open to American investment as Washington steps up efforts to counter China’s dominance in critical supply chains.

Congo’s mines minister, Louis Watum, said the list would be delivered this week and would form the basis of commercial talks, stressing the country is not offering assets on preferential terms. Watum spoke on Wednesday at the Future Minerals Forum in Riyadh, weeks after Washington and Kinshasa announced a minerals agreement without naming specific deposits.

The move follows a Dec. 4 accord that gives US companies privileged access to Congo’s vast reserves of copper, cobalt, lithium and tantalum, materials central to electric vehicles, defence systems and advanced electronics. Congo is the world’s second-largest copper producer and the leading supplier of cobalt, a key battery metal.

“We are sending this week to the US a list of strategic projects where the US can invest,” Congo Mines Minister Louis Watum told attendees, according to Bloomberg News. “It’s going to be, strictly speaking, a commercial discussion. It’s not going to be like we are giving it for free, not at all.”

Chinese companies, such as CMOC, currently dominate production of both metals in the Congo, where copper and cobalt are often mined together. US firms have historically stayed away, citing conflict, corruption and logistical challenges, while Chinese operators have expanded rapidly.

China’s hold

Kinshasa hopes a wave of American investment will dilute that dominance. In 2007, Congo granted Chinese miners tax breaks running until 2040 in exchange for promised investments of $9 billion, of which only about $6 billion materialized. At the time, Western governments showed little interest in curbing sales to Chinese buyers.

By the time US President Donald Trump returned to office in January 2025, Chinese firms controlled about 80% of Congo’s mining output, including Tenke Fungurume, once owned by a US company and now the world’s second-largest source of cobalt, run by CMOC.

The minerals pact forms part of a broader US-brokered peace agreement between Congo and neighbouring Rwanda, aimed at ending decades of violence in eastern Congo.

Under the so-called “Washington Accords”, the US will help oversee a regional peace process in return for Congo facilitating American investment.

Watum described the deal as a framework designed to deliver mutual benefits, even as fighting continues in parts of the country, echoing concerns seen in similar US resource agreements elsewhere.

Washington has identified 60 critical minerals essential to technologies ranging from weapons systems to wind turbines and semiconductors, many of which are predominantly supplied by China. President Trump has pushed to diversify supply, including through recent resource deals and proposals abroad, arguing that access to minerals is a strategic priority.

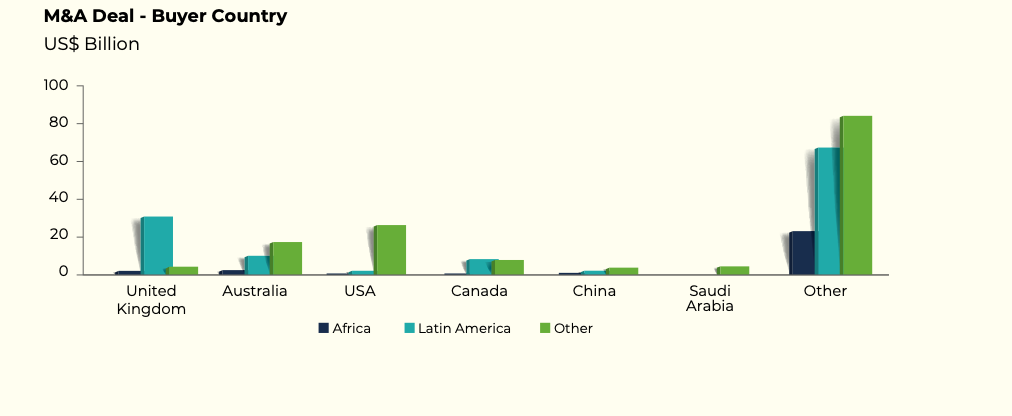

Global mining mergers and acquisitions hit about $30 billion in the first three quarters of 2025, with 74% of deal value flowing to Latin America as investors retreat from higher-risk jurisdictions, a report from McKinsey & Company and the Future Minerals Forum shows.

The figures are part of the Future Minerals Barometer Report 2025, which tracks supply-chain readiness across Africa, West Asia, Central Asia and Latin America.

Developed in partnership with McKinsey & Company and other sector experts S&P Global Market Intelligence, Global AI and GlobeScan, the barometer integrates stakeholder sentiment, data, market intelligence and project-level evidence into a single authoritative platform to guide global decision-making.

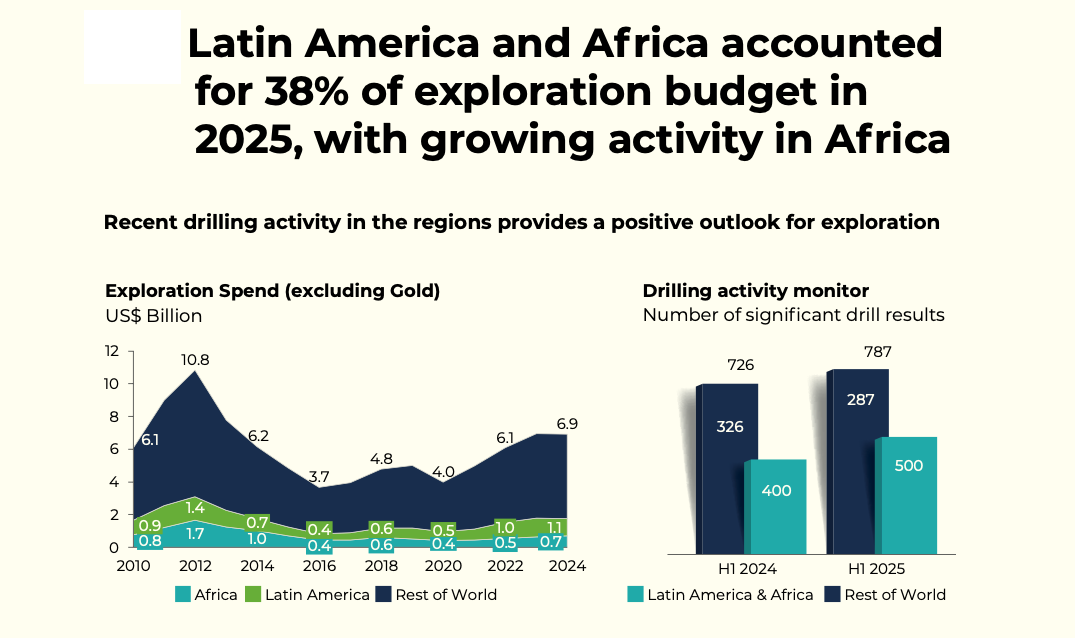

The report found there is a widening gap between mineral endowment and investment. More than 50% of global critical mineral reserves sit in the so-called Super Region — Africa, West Asia and central Asia — yet it attracts the lowest exploration spending worldwide, heightening long-term supply risks.

Deals value skyrockets

Since 2021, mining deal values in Latin America are up more than 200%, while Africa has seen an almost 80% decline as capital gravitates toward jurisdictions perceived as more stable.

The barometer builds on McKinsey’s Global Materials Perspective, released in October last year, which shows mining productivity has improved by just 1% a year since 2018, reinforcing why investors are increasingly focused on capital discipline and permitting certainty.

The report warns that global critical mineral supply chains are under growing strain just as demand accelerates, driven by the energy transition, digitalization and rising defence needs.

Demand for copper, lithium, nickel and rare earths is rising faster than new supply can be brought online, while long permitting timelines, infrastructure gaps, capital intensity and policy uncertainty continue to slow project development.

More than 45% of refined production for electric vehicle materials is concentrated in a single region, increasing exposure to geopolitical risk, trade disruptions and price volatility.

Anglo American (LON: AAL) CEO Duncan Wanblad said global copper demand is projected to rise 75% to 56 million tonnes a year by 2050, requiring about 60 new mines the size of Quellaveco in Peru to be developed over the next decade to offset declining output from aging assets.

Risk reset

Investment flows reflect a broader reset in risk perception. McKinsey partner Jeffrey Lorch said the barometer integrates market data and stakeholder sentiment to give companies a practical roadmap to navigate volatility. GlobeScan CEO Chris Coulter said the Super Region faces major challenges but also a significant opportunity if policy, financing and infrastructure gaps can be addressed.

The report estimates the world will need about $5 trillion in cumulative investment by 2035 to meet critical minerals demand, while exploration spending remains 40% to 50% below what is required. Compounding the shortfall is an average 16-year timeline from discovery to first production, meaning projects found today are unlikely to contribute meaningfully to 2030 or 2035 climate targets.

Industry leaders at the forum argued that faster development will depend on regulatory harmonization, new funding mechanisms and deeper collaboration between governments, miners and investors to unlock supply in Africa, Asia and Latin America.