It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Sunday, January 18, 2026

Retail investors steer record amount cash into silver, creating crowded trade

Individual investors have been snapping up silver at such a pace it has turned into the most crowded commodity trade in the market, according to a report published on Thursday by Vanda Research.

Vanda calculated that in the last 30 days alone, individual investors have snapped up $921.8 million of exchange-traded funds underpinned by silver such as the iShares Silver Trust. The iShares ETF recorded $69.2 million in retail inflows on Wednesday, marking the largest day of retail buying second only to 2021, when retail investors last drove prices skyward.

The ETF is up 31.3% so far this year and has soared 210.9% in the last 12 months. Silver has set a series of new highs. On Thursday, silver prices traded at $91.90 an ounce late in the afternoon, up from $72.62 on the first trading year, but below the record of more than $93 intraday Wednesday and Thursday, according to data from LSEG.

Meanwhile, the MSCI ACWI Select Silver Miners Investable Index, which tracks stock prices of mining companies with shares particularly exposed to changes in the price of the metal, has soared some 225% in the last 12 months.

That 2021 bull market in silver came as part of a broader retail speculative boom in meme stocks like GameStop and AMC Entertainment. But this time, Vanda says, there are more concrete reasons underpinning the rally.

“This isn’t just a meme-stock spike; we are witnessing a structural accumulation that has now surpassed the heights of the 2021 ‘Silver Spike’,” Vanda noted. That means it is time to treat silver as “a core macro trading asset” and not just a speculative bet, it added, pointing to the fact that retail investors are big players in the ProShares UltraShort Silver ETF, an inverse leveraged fund that returns double any decline in the daily price of silver.

Others remain more wary.

“We waited 45 years for silver to break above $50 an ounce and now we’ve seen it zoom past $80 in less than three months,” said Kathy Kriskey, head of alternatives ETF strategy at Invesco.

(By Suzanne McGee; Editing by David Gregorio)

Silver’s torrid rally has Americans in frenzy to buy, sell coins

The last time silver was this hot, Reddit posters piled in to drive prices even higher, creating a frenzy that overwhelmed dealers. The metal’s current rally has set off a similar dynamic.

Over the past year, the price of the white metal has tripled, with a nearly 30% jump just this month as investors turn to hard assets amid ongoing geopolitical risks, supply tightness and renewed uncertainty surrounding the independence of the Federal Reserve. Spot silver pulled back from a record high on Thursday as investors booked profits from the rapid price advance and as the US refrained from imposing import tariffs on critical minerals.

“The relentless of the momentum with silver is really unusual. That has really catalyzed on the retail side a tremendous new influx of retail purchasers and sellers,” said Stefan Gleason, chief executive officer of Money Metals Exchange, one of the top US bullion dealers. “We’re seeing record levels on both selling and buying.”

Gleason said his firm recorded its largest sales month in December in its 16-year history, when silver gained nearly 27%. Many longtime holders of silver and gold bars and coins have come out to cash in on the price gains while newcomers are enticed for the same reason, he said.

The bullion dealer charges retail buyers of one-ounce American Eagle silver coins $12 over spot prices, the highest since 2023. And sellers pay $5-$8 to the online exchange to take the metal, the largest ever in dollar terms.

In 2021, silver was caught up in the Reddit day traders short-squeeze mania that saw prices surge 14% to top $30 an ounce in just three sessions. The moves also roiled the physical market with dealers unable to process orders of bars and coins for several days due to unprecedented demand.

The demand since Christmas is similar to 2021, Gleason said, “where it was just a massive amount of unexpected volume.” In addition to Money Metals, dealers including Apmex, SD Bullion and JM Bullion are telling customers to expect delays in processing and shipping times.

Money Metals has hired 40 people since Christmas and needs to hire 30 more, said Gleason. It’s “just overwhelming but exciting.”

Spot silver fell 2.9% to $90.48 an ounce as of 10:27 a.m. in New York.

(By Yvonne Yue Li)

FE

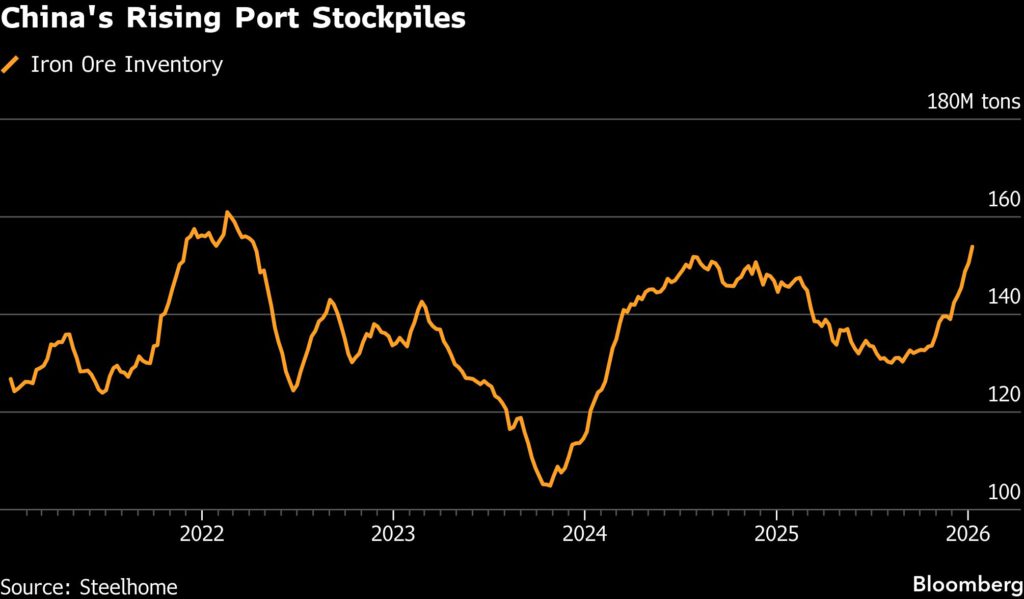

Iron ore’s strength hard to reconcile with soft Chinese demand

Iron ore’s robust start to the year continues to highlight what many observers deem to be a persistent mismatch between market pricing and conditions on the ground.

Benchmark Singapore futures topped $109 a ton this week, a level last reached 15 months ago when the Chinese government was busy with measures to stimulate the economy. The country is the world’s biggest buyer of iron ore, the main feedstock for steelmaking.

But the market’s resilience is proving hard to reconcile with fundamentals. While China’s iron ore imports hit a record last year, its steel output in 2025 is on course for a seven-year low. Port stockpiles have ballooned to near four-year highs, underscoring persistent pressures on demand as the nation’s property downturn drags on and policymakers emphasize reforms to reduce overcapacity.

“The strong start for iron ore futures in early 2026 looks increasingly disconnected from underlying fundamentals,” said Ewa Manthey, a commodities strategist at ING Groep NV in London. The rally is being driven by improved risk appetite among hedge funds and expectations of policy support, rather than a sustained tightening in the physical market, she said.

“That divergence leaves prices more vulnerable if macro sentiment or positioning were to turn,” Manthey said.

Short-term pricing is likely benefiting from the expectation that Beijing will front-load fiscal spending early in 2026, when its latest five-year plan begins. “A stronger boost from infrastructure investment and related activities should help to support commodities demand,” HSBC Holdings Plc said in a note.

Simandou’s shadow

But the view further out is less constructive. Chinese steel demand has settled into long-term decline, even as more iron ore becomes available, chiefly from the Simandou mega-project that recently came online in Guinea. A Bloomberg survey of analysts forecasts a steady drop in spot prices, from a median of $100 a ton in first-quarter 2026 to $90 in second-quarter 2027.

“Looking into 2026, the iron ore market is expected to remain oversupplied, raising questions over how excess volumes will be digested,” BRS Shipbrokers said in a note.

Simandou is casting a long shadow over prices. The first commercial shipment is set to land in China this month, and the $23 billion mine will eventually account for about 5% of global production.

“The decline will occur gradually, rather than a sharp one, as most of the supply surplus — Simandou — will require time to ramp up production and benefit from economies of scale,” said Jack Teah, an analyst at Shanghai Metals Market.

A resolution to BHP Group Ltd.’s pricing dispute with China’s state-run iron ore buyer would also unlock more supply and pressure prices.

“Once those talks make progress, a huge amount of previously restricted ores will definitely impact market price,” he said. “But no one can really predict when that will happen.”

Oyu Tolgoi open pit has been producing since 2012. (Image courtesy of Turquoise Hill.)

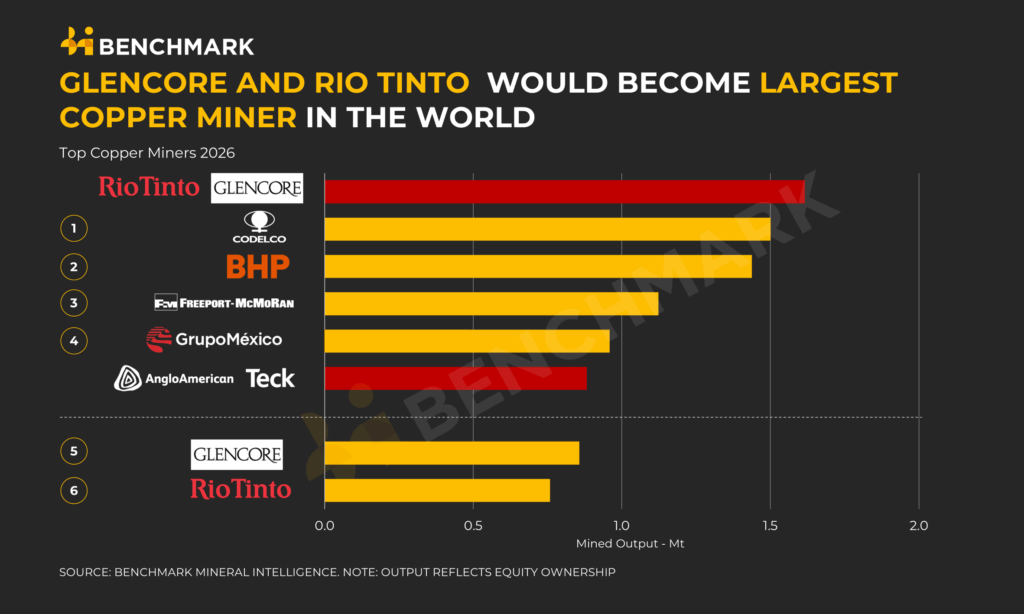

The proposed tie-up between Rio Tinto and Glencore could require asset sales to secure regulatory approval from top commodity buyer China, which has longstanding concerns about resource security and market concentration.

The two mining giants revealed last week that for the second time in two years they were in early merger talks – potentially creating the world’s largest mining company with a market value of more than $200 billion.

But analysts and lawyers said the scale of their sales to China means any deal will need approval from Beijing, as have past mining mega-deals such as Glencore’s $35 billion purchase of Xstrata in 2013.

China’s antitrust regulator is likely to be concerned about a combined entity’s concentration in copper production and marketing as well as iron ore marketing, several analysts and lawyers told Reuters. Beijing may also see an opportunity to force asset sales to friendly entities, they added.

Even before the Glencore talks were made public, Rio Tinto had already been exploring an asset-for-equity swap aimed at trimming the 11% holding of its biggest shareholder, state-run Aluminium Corporation of China, known as Chinalco. Rio Tinto’s Simandou iron ore mine in Guinea and Oyu Tolgoi copper mine in Mongolia were among the assets of interest to Chinalco, sources said then.

To get the Glencore deal over the line, assets in Africa are especially likely sales candidates as Latin America has become less accepting of Chinese investment, according to Glyn Lawcock, an analyst at Barrenjoey in Sydney.

“China will see this as an opportunity to squeeze out assets,” he said.

China’s commerce ministry, its market regulator and Chinalco did not respond to questions about the deal. Glencore and Rio Tinto declined to comment.

Glencore precedent

Glencore has been here before. In 2013, Chinese regulators forced the Swiss-based company to sell its stake in the Las Bambas copper mine in Peru, one of the world’s largest, to Chinese investors for nearly $6 billion in exchange for blessing its takeover of Xstrata.

“The Las Bambas deal is still looked at as a very successful solution and it’s going to be a potential playbook that regulators can draw on,” a China-based partner at an international law firm said on condition of anonymity.

Glencore also agreed to sell Chinese customers minimum quantities of copper concentrate at certain prices for just over seven years as Beijing was concerned the merged group would have too much power over the copper market.

Glencore is one of Australia’s largest coal exporters, operating 13 mines in New South Wales and Queensland. (Image courtesy of Glencore.)

Rio Tinto (RIO) and Glencore (GLEN) are said to be examining whether a coal-heavy business could be spun off into an ASX-listed vehicle as part of early-stage talks on a potential merger that would create the world’s largest mining company.

The companies confirmed last week they are discussing a possible combination of some or all of their businesses, sparking speculation about how assets that sit awkwardly together would be handled, particularly coal and Glencore’s lucrative trading arm.

“All we know is that they are trying to hammer out important details, like the price, the premium, who would run the new company, exactly what structure it would have,” Clara Ferreira Marques, Bloomberg’s Asia-Pacific head of commodities, said on the The Australia Podcast on Thursday.

“They’re hiring banking teams to help them do that, and they really have to come up with some sort of proposal by the fifth of February to meet the UK takeover panel rules.”

One option under consideration is carving out coal assets, potentially into a separately listed Australian vehicle, echoing BHP’s (ASX, LON: BHP) South32 demerger a decade ago.

Glencore’s coal operations across NSW, Queensland, central Africa and Latin America would account for about 8% of a combined group’s $45.6 billion in EBITDA and could be worth tens of billions of dollars. Glencore’s trading arm, which would represent about 9% of earnings, remains another sensitive piece of the puzzle.

Analysts have also floated alternatives, including Glencore spinning off coal ahead of any transaction or Rio bidding only for Glencore’s copper assets, following Glencore’s decision last year to abandon a self-driven coal separation.

Why now

The renewed talks come as pressures that were present a year ago have intensified, particularly around copper, scale and market positioning.

“What has changed since the last time they held talks is that some of the issues that were already there a year ago have become a lot more stark,” Ferreira Marques said. “You look at the copper price, we’re now over $13,000 a tonne. That makes the case for adding copper to your portfolio not only compelling, but urgent.”

She added that Rio’s recent share price performance has improved the financial logic of a deal, while the sector’s shrinking relative size has become harder to ignore.

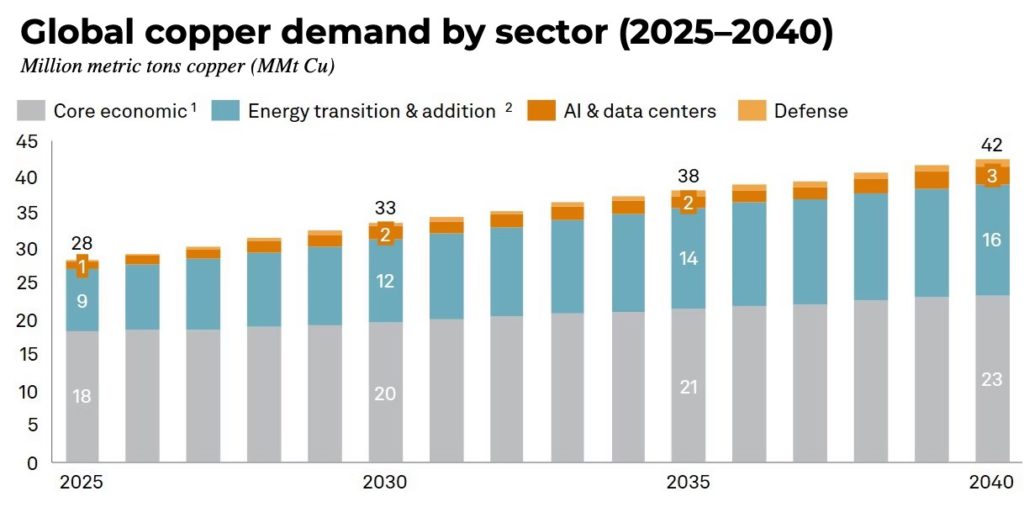

Demand for the metal is anticipated to rise by as much as 50% by 2040, according to S&P Global Energy & Market Intelligence, leading to a projected production deficit of up to 10 million tonnes annually by that time.

A Rio Tinto-Glencore tie-up would position the new company as the leading copper producer globally, accounting for approximately 7% of the world’s output.

“You look at Rio Tinto at about $141 billion, and then you look at Nvidia at $4.5 trillion,” she said. “The problem of scale is very important. It’s not just about being the biggest, it’s about being able to attract generalist investors, talent and opportunities.”

1. Includes copper demand from construction, cooling, appliances, fossil power generation, machinery and internal combustion engine (ICE) vehicles. 2. Includes copper demand from clean energy technologies, transmission and distribution and EVs. (Courtesy of S&P’s Copper in the Age of AI.)

Leadership changes have also helped reset the dynamic. Rio now has a new chief executive in Simon Trott and a more deal-minded chair in Dominic Barton, while Glencore is led by Gary Nagle, who has called the tie-up the “most obvious” deal in mining.

Previous talks in late 2024 stalled over valuation, culture and control, but people familiar with the discussions say both sides now appear more open to compromise.

Hurdles ahead

Price remains the primary obstacle, followed closely by cultural fit, coal exposure and regulatory risk. Rio exited thermal coal in 2018, and some investors remain constrained by mandates that bar coal holdings, even as the political climate in the US has softened and coal profitability has endured longer than expected.

Antitrust scrutiny would be significant, particularly given China’s role as a major stakeholder in Rio, and the operational risks tied to Glencore’s copper assets in jurisdictions such as the Democratic Republic of Congo.

“At this point, it’s unlikely,” Ferreira Marques said. “BHP is not a company that jumps on things at the last minute. The signalling is very much that they wouldn’t step in.”

She cautioned, however, that early-stage deals can still unravel. “When companies talk about an M&A deal, they basically tell the world that they need to do something,” she said, adding that BHP’s earlier bid for Anglo American (LON: AAL) helped reopen the door to mega-deals across the sector.

Whether the talks culminate in a full merger that gives rise to a GlenTinto, a RioCore or something else entirely, a partial asset deal or yet another false start, the discussions underscore how urgently the world’s biggest miners are hunting for growth in an increasingly copper-constrained world.

Copper assets are in even higher demand today given the metal’s role in the green transition and artificial intelligence. Rio Tinto and Glencore are shifting their focus to the metal, as are rival miners including Australia’s BHP.

Chinese regulators will also be examining a planned $53 billion copper-focused merger between Anglo American and Teck Resources, Teck CEO Jonathan Price said in September.

Political challenges

Copper’s rising importance is politicizing the metal. The White House has alluded to China’s dominance over the supply chain as a direct threat to national security, and it remains to be seen how it would react to major mineral asset sales to Chinese interests.

A combined Rio Tinto-Glencore would market about 17% of global copper supply, according to Lawcock, although analysts at Barclays say the share of mine production is only 7.5% and unlikely to trigger major antitrust concerns.

Nonetheless politics has doomed deals before.

US chipmaker Qualcomm walked away from a $44 billion deal to buy NXP Semiconductors in 2018 after failing to get approval from Chinese regulators in what was seen as a response to the trade war then underway between Washington and Beijing. The inability to get Chinese regulators on board similarly sank Nvidia’s proposed takeover of Arm Ltd.

In previous resource deals, however, Beijing has given approval as part of a bargain. A year before the sale of Las Bambas, Beijing required major changes to a tie-up between Japan’s Marubeni and US grain merchant Gavilon, citing food security concerns.

“Clearly this would be a long, complicated deal from a regulatory approval perspective,” Mark Kelly, CEO of advisory firm MKI Global Partners, wrote in a note, “and the presence of Chinalco on Rio’s shareholder register always complicates this picture further.”

(By Lewis Jackson, Amy Lv, Melanie Burton, Anousha Sakoui and Clara Denina; Editing by Veronica Brown, Tony Munroe and Jamie Freed)

AU

Mali gold output plunges 23% as Barrick halt, tougher rules reshape sector

A view of open-pit operations at Fekola. Credit: B2Gold.

Mali’s industrial gold output fell 22.9% in 2025, hurt by the lengthy suspension of Barrick Mining’s operations due to a dispute over tougher mining rules, provisional figures from the West African country’s mines ministry showed.

Mali, one of Africa’s largest gold producers, has been pushing reforms intended to capture more value from the sector, enshrined in a mining code introduced in 2023.

A sweeping audit led to the recovery of 761 billion CFA francs ($1.2 billion) in arrears from mining companies, the government said in December.

But the tougher rules rattled some miners and sparked a two-year standoff with Barrick, and the Canadian company’s massive Loulo-Gounkoto complex was put under provisional administration before a deal was struck late last year.

The standoff weighed on sector sentiment and disrupted output across the industry, offsetting gains from new entrants and expanded small‑scale industrial mines, according to the data seen by Reuters late on Thursday.

Industrial production fell to 42.2 metric tons from an updated 54.8 tons in 2024, the data showed. Mali’s industrial gold output peaked at 66.48 tons in 2023.

The Loulo‑Gounkoto complex, Mali’s biggest producer, reopened in July under a state‑appointed administrator, but persistent logistical issues capped output at just 5.5 tons in 2025, down from 22.5 tons a year earlier, the data showed.

B2Gold overtook Barrick to become Mali’s largest gold producer in 2025, delivering 17.5 tons, according to the data.

Allied Gold, boosted by its large new mine Korali-Sud alongside its Sadiola mine, ranked second with 9.58 tons, followed by Barrick with 5.5 tons.

Artisanal gold output remained unchanged at six tons in 2025. Combined with industrial output, total national production was 48.2 tons in 2025 – 22.7% below the government’s original 54-ton forecast.

(By Tiemoko Diallo; Editing by Maxwell Akalaare Adombila, Robbie Corey-Boulet and Emelia Sithole-Matarise)

Trump sets process to secure critical minerals after trade probe

US President Donald Trump (Image courtesy of White House.)

President Donald Trump moved to set up a new process to secure access to imports of critical minerals, capping a months-long review to determine whether foreign shipments threaten US national security.

“What it does is it sets up a mechanism, a process by which the United States will seek to secure its international supply chain of critical minerals and critical mineral derived products,” White House Staff Secretary Will Scharf said at a signing ceremony Wednesday at the White House.

Neither Trump nor Scharf clarified if the mechanism would increase tariffs on rare earth elements, and the pair did not immediately provide additional details on how the effort would work. The White House is expected to provide additional detail later Wednesday.

Trump has been under pressure to respond after China, the world’s largest processor of many critical minerals, constrained access to rare earths crucial to advanced technologies during a trade spat last year.

Industry watchers for months have awaited the decision on the critical minerals investigation, which the Commerce Department launched last April under Section 232 of the Trade Expansion Act. That authority is seen as a way the administration could rebuild its tariff regime if the Supreme Court strikes down Trump’s global levies.

But additional duties could destabilize the trade truce Trump and Chinese President Xi Jinping agreed to last fall, under which the sides agreed to lower import-tax rates and ease export controls.

It may also have implications for uranium, which has growing appeal as the US looks to build out nuclear power as quickly as possible to keep up with the massive power needs for artificial intelligence.

A major hurdle the administration will need to address, if tariffs are imposed, is the lack of domestic production the US has for most of these raw materials.

Traditionally, trade lawyers have argued that tariffs are needed to protect an existing domestic industry that can prosper with appropriate controls that prevent foreign nations from oversupplying the US market to take down American companies.

Given China processes more than 80% of the world’s rare earths, and Kazakhstan accounts for the majority of the world’s uranium, it isn’t clear how US companies will benefit as paltry domestic production forces them to rely on foreign supplies.

(By Joe Deaux)

Mkango launches rare earth plant in Britain using recycled materials

The facility at Tyseley Energy Park has enabled the first commercial rare earth magnet production in the UK in 25 years. Credit: Tyseley Energy Park

Canadian rare earths group Mkango Resources on Thursday opened Britain’s first commercial plant in 25 years to produce permanent magnets from recycled materials, as the West seeks to loosen China’s “stranglehold” over critical minerals.

Western countries have pledged to reduce reliance on China, which dominates mining and processing of rare earths, used in electric vehicle motors, wind turbines and consumer electronics. But new production outside China has been slow to scale up, leaving supply tight and making recycling one of the few options available to expand access to these materials in the short term.

The plant, in Birmingham in central England, is operated by Mkango’s subsidiary HyProMag. It uses a hydrogen-based process developed at the University of Birmingham to strip magnets from end-of-life products and turn them into new rare earth material with far lower emissions than conventional mining and refining.

Britain and its G7 partners aim to reduce China’s dominance through new domestic capacity, Industry Minister Chris McDonald told Reuters. China accounts for about 70% of rare earth mining and 90% of refining.

“Fundamentally, that’s the stranglehold on the supply chain that we’re aiming to break,” he said.

The new plant adds to Britain’s strategy to increase critical minerals supply, aiming to meet 10% of domestic demand from local mining and 20% from recycling by 2035, backed by up to 50 million pounds ($66.86 million) in funding.

Britain previously had magnet-making capacity but this ceased about 25 years ago as production moved overseas.

The plant has the capacity to produce 100-300 metric tons of magnets a year, depending on the number of work shifts, using the new technology that has a low-carbon footprint, the company said.

McDonald said that the facility was already drawing strong interest from automakers, and the technology was starting to be rolled out in the United States and Germany. HyProMag has previously said it was developing similar plants in these two countries.

($1 = 0.7478 pounds)

(By Sam Tabahriti and Eric Onstad; Editing by Jane Merriman)

Italian Prime Minister Giorgia Meloni (left) and Japanese Prime Minister Sanae Takaichi (right). Credit: Prime Minister’s Office of Japan

Japanese Prime Minister Sanae Takaichi and Italian Prime Minister Giorgia Meloni agreed to work together on critical mineral supply and elevate their relationship to a new level.

“We agreed that cooperating to strengthen the resilience of our critical mineral supply chains is of utmost urgency,” Takaichi told reporters in Tokyo after their meeting on Friday.

The push for closer ties comes as Japan seeks to strengthen its supply chain resilience, with a diplomatic standoff raising uncertainties over China’s rare earths supply to Japan.

Takaichi added that the two countries would launch a dialogue on space issues, and that ties between them would be raised to a new level of “special strategic partnership”.

Meloni said through a translator that there is alignment between Japan and Italy in seeking a peace achieved through a free and open order. A joint statement with more details is set to be released later in the day.

State-run China Daily reported earlier this month that Beijing is considering tighter export license reviews for certain medium and heavy rare earth–related items bound for Japan. Such a move would be a blow to Japan’s economy given the reliance of its huge autos industry on such minerals.

Deeper ties between Japan and Italy may reflect the personal affinity between the two leaders.

Takaichi and Meloni are both the first female premiers of their respective nations. They went viral last year for an enthusiastic embrace captured in videos from the sidelines of the Group of Twenty summit held in South Africa.

They again emphasized their closeness on Friday, with Takaichi wishing Meloni a happy birthday as she opened her speech. The two were set to huddle with female cabinet ministers later in the day.

(By Sakura Murakami)

Saudi Public Investment Fund plans to spin off mining firm Manara

Saudi Arabia’s Public Investment Fund plans to spin off its mining investment firm Manara Minerals, the kingdom’s mining minister said, as it seeks to revive its pursuit of investments abroad.

Saudi Arabia, in common with other Middle Eastern economies, is working to secure critical minerals such as copper and lithium, essential for electric vehicles and renewable energy, as part of its efforts to reduce dependence on oil.

Manara, a joint venture between the Saudi Arabian Mining Company, also known as Maaden, and the $925 billion PIF, was established in 2023 to invest in critical minerals abroad.

But, although it has bid for assets across Africa and Asia, it has so far completed only one deal: a $2.5 billion 10% stake in Vale Base Metals, which was spun off from Brazilian iron ore giant Vale in 2024.

Industry and Mineral Resources Minister Bandar Al-Khorayef said spinning off Manara from the PIF would sharpen its focus.

“This will change the culture of the company from being only an investment vehicle to having more technical capability,” Al-Khorayef told Reuters in an interview on the sidelines of the Future Investment Forum event.

“PIF is a large investor, but they don’t have mining expertise.”

He did not give any timing on a spin-off, but said discussions over new shareholders in Manara were ongoing, adding that they could be Saudi or foreign investors.

In Saudi Arabia, the pursuit of international investments and the development of mining are part of Crown Prince Mohammed bin Salman’s broader plan to diversify the economy away from oil.

Riyadh estimates its untapped mineral resources, including phosphate, gold, bauxite and rare earth elements, at about $2.5 trillion.

Maaden is also exploring for rare earths and developing technology to extract lithium from seawater.

(By Clara Denina; Editing by Veronica Brown and Barbara Lewis)

Column: Europe falling behind in critical minerals race

Sweden’s LKAB has identified significant deposits of rare earth elements in the Kiruna area. Credit: LKAB

The European Union has taken action to strengthen critical mineral supply chains that support the energy transition but the US is moving faster and offering greater support, leaving Europe vulnerable to China’s dominant position.

China already dominates the global supply of solar power components and Europe has minimal production and processing capacity for key materials used in battery storage like lithium, nickel, cobalt, manganese, high-purity graphite, as well as rare earths and permanent magnets for wind turbines and electric motors, Ruben Davis, senior policy officer at Cleantech for Europe, told Reuters Events.

For clean power developers, over-reliance on dominant suppliers of critical minerals increases the risk of project delays due to licensing issues, export controls or other sudden supply disruptions.

In 2024, 95% of EU rare earth imports came from just three countries: China, Malaysia and Russia, according to Eurostat. China hosts 32% of global lithium production and Chinese companies control another 18% based in other countries, including Zijn’s Tres Quebradas scheme in Argentina and Gangfeng Lithium’s Sonara project in Mexico, according to Wood Mackenzie.

Importantly, China dominates critical minerals processing, holding 81% of global capacity, Wood Mackenzie said.

Critical minerals production – share of top three countries

In a bid to speed up investment, the EU adopted the ResourceEU action plan in December 2025 which aims to expand the primary extraction and refining of critical minerals on EU territory, promote recycling and reduce dependence on dominant suppliers.

Funded by 3 billion euros ($3.5 billion) from the EU’s 2024 Critical Raw Materials Act (CRMA), the action plan includes measures to speed up project permitting and ban scrap exports and sets a target of extracting 10% of EU critical minerals needs on home territory and hosting 40% of processing capacity on EU soil by 2030, while setting a minimum recycling threshold of 15%.

The CRMA comes from existing financing sources and “falls short of a fully funded industrial strategy,” Arthur Leichthammer, geoeconomics policy fellow at the Jacques Delors Centre, told Reuters Events.

European policymakers have understood the importance of diversification but current efforts are too slow and policymakers have not focused enough on promoting processing, Luc Pez, chief commercial officer at Viridian Lithium, said.

“Investment momentum has weakened globally because of low prices,” Pez noted.

According to Davis, the EU’s regulations “have not yet fundamentally shifted the bankability or business case of most projects.”

Huge challenge

Europe and the US have a long way to go to reduce their reliance on dominant critical mineral suppliers. For copper, lithium, nickel, cobalt, graphite and rare earth elements, the average market share of the top three producers increased from about 82% in 2020 to 86% in 2024, according to the IEA in May 2025, with almost all supply growth coming from the single top supplier: Indonesia for nickel, and China for all other minerals.

In one example, the EU sources 93% of its permanent magnets for wind turbines from China, according to the Centre for Strategic and International Studies.

Critical minerals projects that have stalled in Europe include the Chvaletice manganese project in the Czech Republic, which hit long delays in permitting and grid access despite Strategic Project designation by the European Commission. The fast-track permitting provisions in the CRMA have not yet been incorporated into Czech law.

Venture, growth investments in critical minerals innovation

In November, the UK updated its national critical mineral strategy to reduce permitting hurdles, accelerate diversification of supplies and support more recycling of waste.

“Our Critical Minerals strategy will see us collaborate with the EU as we look to build more secure and resilient supply chains”, a spokesperson for the UK’s Department for Business and Trade, told Reuters Events.

The UK strategy provides just 50 million pounds ($67.4 million) in funding and lacks “credible instruments to shift investment decisions in new projects or mandatory diversification,” Leichthammer warned.

Europe has historically looked to market forces to solve supply issues but “we’re now reassessing that,” Cillian O’Donoghue, policy director at European Electricity Association Eureletric, told Reuters Events.

The EU should create a single market for the recycling of PV and battery storage systems to help diversify critical raw material supply, a spokesperson for industry group SolarPower Europe said.

This market would help build a circular economy and allow recycling businesses to scale up, the spokesperson said.

Europe trails US

Projects underway in Europe include Swedish group LKAB’s $800 million demonstration plant for processing phosphorous and rare earth elements. The facility is scheduled to become operational in 2026 and will be scaled up with additional processing facilities to achieve “full operation during the 2030s,” the company said in a statement.

But the US is moving faster to diversify its critical mineral supply, pursuing a more “security-driven and deal-based” strategy, Davis noted.

The Trump administration has enacted policies to ramp up the supply of critical minerals in the US and from allied countries, while engaging in a high-stakes trade and tariff battle with China.

Measures in President Joe Biden’s 2022 Inflation Reduction Act and President Trump’s 2025 One Big Beautiful Bill provides private companies with tax credits, loans, price floors, grants and offtake guarantees.

This range of incentives will help to “build mine-to-magnet or mine-to-battery chains at speed,” Davis said.

The US has also used the Defense Production Act to provide supplier guarantees that help make projects commercially viable.

In contrast, many European strategic minerals projects are shelved by private companies before the final investment decision stage, Davis said.

“Europe’s challenge is that, compared with the US or China, public tools to de-risk projects are still relatively small,” he said.

(Opinions expressed are those of the author, Neil Ford, an energy reporter for Reuters Events.)

(Image by Generation Grundeinkommen)

(Image by Generation Grundeinkommen)