It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

U.S. upstream M&A is slowing sharply, falling from $192 billion in 2023 to $65 billion in 2025.

Canada is seeing the opposite trend, with $37.8 billion in 2025 deals consolidating oil sands control among a handful of major players.

M&A action was driven by cost-cutting, operational synergies, pipeline constraints, and investor pressure for efficiency.

Previously, we reported that the U.S. Shale Patch has witnessed a big slump in corporate buyouts in recent years as premium acreage depletes and volatile energy prices keep buyers on the sidelines. Following a record $192 billion in mergers and acquisitions announced in 2023 and $105 billion in 2024, U.S. upstream oil and gas M&A activity totaled just $65 billion in 2025, despite a late-year rebound with $23.5 billion in deals announced in the fourth quarter.

However, the situation could not be more stark in America’s neighbor to the north.

Canada's oil and gas sector is currently experiencing a massive, multi-year wave of consolidation, with 2025 seeing over $37.8 billion in deals executed or pending, marking the highest activity level since 2017. This trend is consolidating control into the hands of a few dominant players including Canadian Natural Resources Ltd. (NYSE:CNQ), Cenovus Energy Inc. (NYSE:CVE), Suncor Energy Inc.(NYSE:SU), and Imperial Oil Ltd.(NYSE:IMO) and even Texas-based ConocoPhillips (NYSE:COP)--who together account for roughly 85% of Alberta's oil sands production. Some high-profile tie-ups in the space include Whitecap Resources Inc.'s (OTCPK:WCPRF) CA$15-billion merger with Veren Inc.; Cenovus Energy’s merger with MEG Energy for ~CA$8.6 billion as well as Ovintiv Inc.'s (NYSE:OVV) CA$3.8-billion acquisitionof NuVista Energy Ltd.

With oil prices remaining lacklustre over the past two years, energy companies are increasingly seeking to cut costs by scaling up, improving operational efficiency and slashing overheads, rather than through organic growth. Meanwhile, investors are demanding better returns through dividends and buybacks, forcing companies to focus on profitability rather than production growth. Further, rising crude oil production from the Western Canadian Sedimentary Basin (WCSB) has led to increased pipeline congestion and renewed rationing on the Enbridge Mainline system. This has depressed prices for heavy Canadian crude despite the completion of the Trans Mountain Pipeline expansion, discouraging new and expensive long-term projects.

“M&A is a way that you can grow when you don't want to invest in drilling, when you're not going to get the kind of returns you're expecting,” Grant Zawalsky, vice-chair at Calgary law firm Burnet, Duckworth and Palmer LLP, told Radio Canada. “Until the fundamentals change, we'll likely see more of the same.”

However, while consolidation will likely persist in the current year, analysts anticipate a modest slowdown in deal momentum, in large part due to a growing scarcity of high-quality targets, “I don't know if we'll see the values that we saw in 2025, which were dominated by a number of large deals over in the billions,” Tom Pavic, president of Sayer Energy Advisors, told Radio Canada. “I think you'll still see quite a bit of activity, just at a smaller scale,” he added.

Experts have predicted that the "field synergy" model, whereby merging companies combine operations that are geographically close to each other, will remain a popular M&A strategy. Tie-ups in the Canadian OilPatch are increasingly focusing on asset consolidation and improving efficiency by combining adjacent or complementary assets to improve operational scale, such as merging Montney producers to maximize infrastructure usage rather than just drilling new wells. These deals include optimizing field logistics, sharing procurement contracts and reducing overhead, such as Cenovus Energy’s estimated $400M/year in projected synergies after merging with MEG Energy, largely driven by field efficiencies and G&A cuts.

Consolidation often leads to lower job-per-barrel ratios through automation and leaner head offices, allowing for increased production with fewer, more specialized staff. Further, companies are utilizing predictive geophysics and "subsurface digital twins" to simulate and optimize field operations before drilling.

Interestingly, mergers in Canada’s energy sector are increasingly focused on improving the Environmental, Social, and Governance (ESG) profile, with over 70% of recent deals involving the target having a higher ESG score than the buyer.

Unlike in the U.S., ESG criteria remain critically important in Canada's energy sector, acting as a core framework for risk management, investment attraction, and social license to operate. While there is a shift away from glossy marketing towards more data-driven reporting, the pressure to maintain high ESG standards--particularly regarding greenhouse gas (GHG) emissions, indigenous partnerships, and corporate governance--is increasing, rather than decreasing. That’s probably not surprising considering that the federal government of Canada is led by the centre-left Liberal Party of Canada, which has been in power since 2015 and secured a fourth consecutive term in April 2025.

In contrast, many U.S. energy companies are scaling back, altering, or outright hiding their ESG commitments, a trend driven by political pressure coupled with investor backlash against underperforming sustainable funds.

The re-election of Donald Trump has accelerated the anti-ESG movement, with efforts to roll back Biden-era climate policies, clean energy tax credits from the Inflation Reduction Act (IRA) and regulations favoring ESG investing. Consequently, many U.S. Big Oil companies are ditching their previously ambitious clean energy roadmaps and have abandoned earlier plans to cut oil output.

By Alex Kimani for Oilprice.com

EU sees US easing impact of metals tariffs in coming weeks

European Union officials believe the US will soon streamline its broad tariffs on products containing steel and aluminum, a topic that’s been an irritant in transatlantic relations and a key sticking point in trade negotiations.

A move by President Donald Trump’s administration to reduce the amount of goods subject to the 50% tariff rate applied to so-called derivative products that contain the metals may be weeks away, according to people familiar with the bloc’s thinking.

The EU has long been seeking relief from the broad metals tariff, which officials in the bloc argue runs afoul of the trade deal struck last year that put a 15% tariff ceiling on most European products. The US regularly revises the list of derivative products, increasing the amount of goods subject to the 50% rate — that list currently surpasses 400 items.

“I got reassurances from our US colleagues that they know that this is a big problem for us and that they’re looking into this matter,” Maros Sefcovic, the EU’s trade chief, told lawmakers Tuesday. “Hopefully we’ll have better news in that regard rather soon.”

A request for comment sent to the office of the US Trade Representative wasn’t immediately returned.

The planned changes wouldn’t impact tariffs on commodity-grade forms of the metals.

The expanding derivatives list also creates an arduous task for companies to identify the percentage of the materials in goods they export and chips away at the benefits of last year’s trade agreement.

The potential progress comes at a difficult moment in transatlantic relations. Ratification of the US-EU trade deal was thrown into doubt after the US Supreme Court struck down Trump’s use of an emergency-powers law to impose his so-called reciprocal tariffs around the world.

In response to the court decision, the US introduced a new 10% global levy on top of existing most-favored nation tariffs, which will increase duties on some EU exports above the level permitted in the US-EU trade accord.

The European Parliament suspended legislative work on approving the EU-US accord on Monday, requesting clarity on Trump’s new trade policy.

Still, both sides have indicated that they want to uphold the accord even as a transition to a new trade policy could take months, said the people, who spoke on the condition of anonymity.

Sefcovic has been in contact with his US counterparts multiple times in recent days, said the people, and he briefed the bloc’s ambassadors on the latest developments on Monday.

(By Alberto Nardelli)

Nippon Steel sells $3.9 billion of bonds for US Steel loan

Nippon Steel Corp. said it has raised 600 billion yen ($3.9 billion) from an upsized sale of convertible bonds — the biggest Japanese offering of its kind — to help repay loans taken out for its acquisition of United States Steel Corp.

Japan’s largest steelmaker sold debt mainly in Europe and Asia, it said in a filing with the nation’s finance ministry, but didn’t offer any in the US. Half of the bonds, which can be converted into stock, are set to mature in 2029 and the remainder in 2031, according to the filing.

Nippon Steel shares slumped as much as 6% on Wednesday. The company earlier sought to raise 550 billion yen from the zero-coupon bonds. They carry a conversion premium of 10% above Tuesday’s closing price for the 2029 tranche and 11% for the 2031 tranche.

Investors expressed enough interest to buy all bonds on offer, people familiar with the matter said, shortly after the company started taking investor orders.

Japanese companies have been increasingly turning toward convertible bonds to raise funds as the prospects of a surge in fiscal spending and central bank rate hikes increase the cost of traditional debt instruments. Convertible bonds have been on the upswing around the globe. Asian companies raised $9.3 billion last month, the best January since 2018.

Nippon Steel’s bridging loan of about 2 trillion yen — secured to fund the company’s acquisition of US Steel — is approaching maturity in June. The Japanese company finalized the takeover last year after 18 months of negotiations that became entangled in American politics, and has plans to build a major new steel plant in the US.

The outstanding balance on the bridging loan has been reduced to around 1.3 trillion yen, chief financial officer Takahiko Iwai said in an interview last week, with repayments made using funds raised through yen-denominated hybrid loans and other instruments. The company’s total interest-bearing debt doubled to 5.3 trillion yen in December 2025 from March the same year.

Nomura Holdings Inc., Goldman Sachs Group Inc. and Bank of America Corp. are arranging the deal, the terms show.

(By Shoko Oda, Ryotaro Nakamaru and Dave Sebastian)

Copper price jumps as China traders cheer prospect of lower US levies

Base metals gained as China’s markets reopened after the Lunar New Year break and traders cheered potentially lower US tariffs.

Copper rallied as much as 2.8% to reach $13,228 a ton in London and aluminum also inched higher. China faces less-punitive charges, a boost for the country’s metal-intensive exports, with the administration proposing a 15% levy after the Supreme Court ruled against President Donald Trump’s reciprocal duties.

“The US Supreme Court dismantled the most cost-effective tariff instrument, but not the new tariff regime overall,” Allianz SE analysts, including chief investment officer Ludovic Subran, wrote in a note. “Uncannily, the Global South and China now emerge as the biggest winners.”

The gains in metals were echoed by a positive tone in mainland equities, as the benchmark CSI 300 Index also advanced on Tuesday. Under the new trade framework — if it’s confirmed — Morgan Stanley estimated that the average US levy on goods from China will drop to 24% from 32%.

The US news is bullish for metals, said Jon Li, an analyst at Guangzhou Finance Holdings Futures Co. Demand from manufacturers will return, he added.

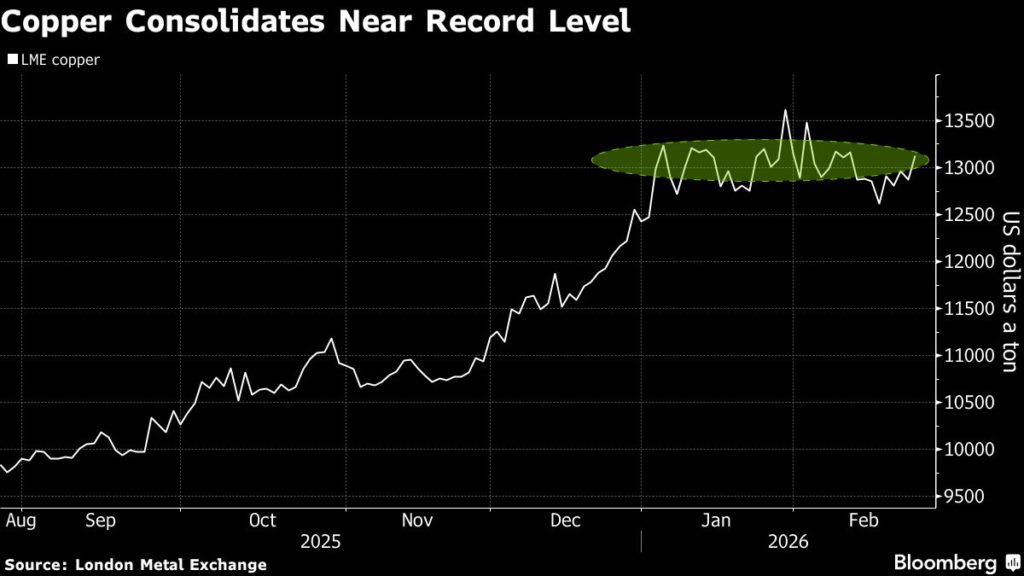

Copper has consolidated at a high level since hitting a record in January, with moves driven by frequent shifts in US policy, as well as mine snarls and forecasts for higher consumption from the energy transition. Higher prices have weighed on physical demand in China, causing exchange-tracked inventories to expand to the highest since 2024. Holdings of the red metal have been rising in the US, as well as in London Metal Exchange-tracked sheds.

Copper rose 2.3% to settle at $13,166.50 a ton on the LME. Aluminum was up 0.1%, as all base metals climbed.

Column: Copper drives BHP and Rio, but getting more is the trick

The latest corporate results from major miners BHP Group and Rio Tinto highlight copper’s starring role in driving profits, but they also underline how difficult it will be to get more exposure to the industrial metal.

BHP, the world’s largest listed miner, reported last week a stronger-than-expected half-year underlying attributable profit of $6.2 billion, up 22% from the same period a year earlier.

A similar dynamic was in evidence at Rio Tinto, with annual iron ore earnings dropping to around 60% of the miner’s total, down from 70% in the prior year, while those from copper doubled to about 30%.

The greater role of copper in the mining companies’ earnings is largely explained by price movements, with copper outperforming iron ore, which has struggled in line with softer Chinese steel production and rising supply.

London copper futures closed at $12,868.50 a metric ton on Monday, down slightly from the previous session and 11.4% below the all-time high of $14,527.50 hit on January 29.

However, copper has been in a sustained uptrend since April last year, and has risen 59% from a low of $8,105 a ton on April 25 to its close on Monday.

The rally has been driven by several factors including US stockpiling amid uncertainty over the tariff policy of President Donald Trump and supply disruptions at major mines.

But there is also a long-term fundamental driver for copper insofar as it is a vital component of the energy transition given its role in the electrification of power and transport systems.

Estimates vary as to how much more copper is going to be needed, but the more modest end of the scale is for a doubling of demand by 2050.

Finding long-term copper deposits is both challenging and costly, which explains why both BHP and Rio went looking to acquire existing mines.

Deals stymied

BHP proposed buying Anglo American in both 2024 and 2025, but eventually walked away from the projected $53 billion deal, largely because of differences in valuation of assets.

Anglo’s South American copper assets were what BHP wanted, and it was less interested in the iron ore, coal and diamonds also housed in the London-listed, former South African mining company.

Anglo instead found its own suitor in Canada’s Teck Resources in another $53 billion deal that will create the world’s fifth-largest copper producer when finalized.

Rio also tried to bulk up its copper production through a merger with Glencore, which would have created a $200 billion mining giant and the world’s largest copper producer.

Once again it was differences over valuations that scuppered the deal, with Glencore holding out for a greater share of the merged entity than Rio was prepared to offer.

With the benefit of hindsight and in view of the strong rally in copper, both Anglo and Glencore were probably correct in rejecting the overtures from BHP and Rio.

What the failure of these proposed mega-mergers shows is that any successful deal will require a much higher premium for the copper assets, one that reflects likely copper demand in 10 or 20 years, rather than what demand is currently.

It also makes it more likely that companies like BHP and Rio will be forced to either start gobbling up junior miners or start exploring and developing new mines, or a combination of both if they want to boost the share of copper in their portfolios.

And what of iron ore, the commodity that built both BHP and Rio into the companies they are today?

China’s steel output fell below 1 billion tons in 2025 for the first time since 2019, and it’s likely that it has now peaked and will slowly decline in coming years.

China buys about 75% of seaborne iron ore and it will remain the major market, but it is also going to get an increasing share from mines it controls in Guinea, where the Simandou project is ramping up over the coming years to an annual capacity of 120 million tons.

This has been reflected in prices, with Singapore Exchange iron ore contracts trading in a narrow range around $100 a ton for much of last year, but dipping below that level on February 13 and ending at $98.46 on Monday.

This is a double whammy for BHP and Rio, with lower prices meeting ebbing demand from China.

The question is whether the rising steel sectors in India and other Asian countries will be enough to compensate for what’s lost in China.

(The views expressed here are those of the author, Clyde Russell, a columnist for Reuters.)

(Editing by Muralikumar Anantharaman)

Disclosure: At the time of publication Clyde Russell owned shares in BHP Group and Rio Tinto as an investor in a fund.

Tungsten crunch can be fixed before prices spike further: BMO

Tungsten is a cornerstone of heavy industries, though it often receives little public attention. (Stock image by Kalyakan.)

Tungsten prices have surged fivefold over the past year as prolonged underinvestment and tightening Chinese supply push the market toward what analysts warn could become a severe global shortage.

In a note published on Monday, BMO Global Commodities Research analysts George Heppel and Helen Amos say the world has “sleepwalked” into a tungsten crunch, driven by persistent ore grade decline, environmental restrictions and a lack of new mining investment. With global inventories critically low and another deficit forecast for 2026, they expect tightness to persist.

Tungsten is a cornerstone of heavy industry, though it often receives little public attention. Tungsten carbide, prized for its extreme hardness and density, is essential in machine parts, drill bits and hard-facing materials. In many applications, it is close to irreplaceable, making the metal a key enabler of manufacturing, mining and defence.

China dominates the market, accounting for roughly 75% of global supply. Production has stagnated in recent years as ore grades decline, environmental controls tighten and Beijing has moved to restrict exports of dual-use tungsten.

As of early 2026, Chinese, exports have plummeted, with some, such as Ammonium Paratungstate (APT), falling to zero in late 2025. As a result, ammonium paratungstate prices broke out of their long-term average of about $300/t in 2025 and now trade around $1,775/t, according to Fastmarkets.

BMO expects 2026 to be a pivotal year. With stocks depleted and supply growth constrained, the market appears headed for another deficit. That dynamic, the analysts argue, is likely to keep prices elevated.

Five options

The bank outlines five potential mechanisms that could eventually rebalance the market, though none offers a quick fix.

A meaningful expansion of Chinese mine supply appears unlikely in the near term due to grade challenges and environmental limits, although projects such as Dahutang could add material volumes over time. Outside China, several projects are advancing, but new mines typically take years to permit, finance and build.

Artisanal mining, which accounts for about 6% of global supply, may respond to higher prices. BMO expects some short-term growth in this segment, but not enough to materially replenish depleted inventories.

Recycling presents another avenue. While there is limited scope to significantly increase recycling rates in western markets, China could expand secondary supply over time if it builds out collection and processing infrastructure. Even so, this would require investment and time.

Demand destruction is also possible, particularly at current price levels. However, substitution is challenging because of tungsten’s unique properties. The analysts identify limited areas where users might switch materials, but they do not expect widespread replacement.

High price cure

In the near term, BMO believes the market will balance through a mix of artisanal supply growth and some demand destruction. That adjustment, however, will not be enough to restore comfortable inventory levels. Over the longer term, the analysts argue that sustained higher prices will be required to incentivize new mine development.

“The cure for high prices is high prices,” they write, adding that meaningful investment in mined supply will likely occur only at price levels well above historical norms.

With reindustrialization and defence spending accelerating in the US and elsewhere, tungsten demand is set to grow. BMO expects the metal’s supply challenges to keep it firmly in the spotlight of critical minerals strategies in the years ahead.

Trump eyes Pentagon AI program for trade block’s minerals pricing

The Trump administration plans to use a Pentagon-created artificial intelligence program to help set reference prices for critical minerals as it works to build a global metals trading zone, three sources with direct knowledge of the effort told Reuters.

Vice President JD Vance earlier this month proposed that the US and more than 50 other countries impose “reference prices for critical minerals at each stage of production” that would be backed by “adjustable tariffs to uphold pricing integrity.”

Those reference prices will be set by the US Department of Defense’s Open Price Exploration for National Security (OPEN) AI metals program, according to the sources, who were not authorized to speak publicly.

The move sheds light on how the administration aims to shape market pricing, even as the AI technology has faced skepticism for whether it can retool how critical minerals are bought and sold.

The OPEN program was launched in 2023 by the Pentagon’s Defense Advanced Research Projects Agency (DARPA) with the goal of calculating what a metal should be priced at when labor, processing and other costs are factored in and when alleged Chinese market manipulation is factored out.

Trump officials are initially focusing OPEN’s AI pricing model on at least four critical minerals, including germanium, gallium, antimony and tungsten, before expanding to others, with S&P Global and Finnish data firm Rovjok supplying data and other technical assistance, according to the sources.

The White House, Department of Defense, S&P and Rovjok did not respond to requests for comment.

The minerals plan comes as the administration moves to rapidly deploy AI tools elsewhere, including via collaborations with OpenAI, Anthropic and Alphabet’s Google for the use of generative AI in battlefield settings.

Focus on thinly traded metals

China is the world’s largest miner or processor of many of the minerals considered critical by the US government. Beijing has used that advantage in recent years to produce minerals at a loss and dampen market prices, a backdrop that has forced Western rivals to close.

Chinese officials have long said that Beijing manages its exports of minerals in accordance with rules from the World Trade Organization.

The OPEN program, which is being transferred to the control of the non-profit Critical Minerals Forum (CMF) next year, has been focused from its inception on metals that are thinly traded or not traded at all.

The CMF said its focus has been on working with “government-funded partners to conduct stress-testing with AI models,” and on “identifying and supporting commercially viable mining and processing projects, rather than on government policy.”

The AI model is aimed at promoting metals supply deals between Western miners and manufacturers by giving both sides more pricing certainty.

It can be difficult for manufacturers that use germanium, antimony, gallium and other minerals to gauge whether Chinese prices reflect traditional supply-and-demand dynamics.

An antimony price set by the AI program and backed by the trade block could boost profits for companies developing US antimony projects, for example. Yet it could raise prices for automakers who use antimony in adhesives and other products.

It was not immediately clear if the AI-derived prices would oscillate or be fixed, nor if they would be set between the US and individual allies or applied across the trading block.

The timeline for implementation is also unclear as the Trump administration must first convince dozens of allies to join the block to guarantee effectiveness.

Canada’s Ministry of Energy and Natural Resources said in a statement to Reuters it was “working to comprehensively understand and analyze” the minerals trade block proposal.

‘An architecture of reliable investment’

The move comes as the Trump administration is stepping away from guaranteeing price floors for individual companies due to the lack of congressional funding, even as many miners have sought such support.

“The administration is still, in good faith, trying to respond to industry demand signals by creating an architecture of reliable investment, but it doesn’t have the one tool that everybody kind of wanted them to use,” said Eric Robinson, a special counsel with the Baker Botts law firm and former managing director of the Pentagon’s Office of Strategic Capital.

The plan to create a minerals reference price and support it with tariffs has sparked questions about whether the tariff would apply to all products containing critical minerals.

For example, the US has only a small cathode industry and thus has little need for lithium currently, but laptops containing lithium-ion batteries are routinely imported from Taiwan and elsewhere. Manufacturers have long voiced a preference for the cheapest source of minerals possible.

“You can try to set something approximating a price floor, but ultimately the trade barriers aren’t going to guarantee someone on the other side of that tariff wall an actual price floor because multiple producers are still going to compete on price,” said Nathaniel Horadam, a former US Department of Energy staffer who managed critical minerals lending programs during the Biden and Trump administrations.

The OPEN program comes amid private industry efforts to boost transparency. CME Group plans to launch the world’s first rare earths futures contract, Reuters reported earlier this month.

US miners say they are supportive of a reference price-and-tariff plan that could help them offset Chinese dumping, provided it helps them generate a profit.

“I have a good steer on what the price is to produce tungsten in the US,” said Oliver Friesen, CEO of Guardian Metal Resources, which is developing two Nevada mines for the metal used to harden steel. “I would want to make sure any reference price is above that.”

Trump has ordered the Department of Defense to rename itself the Department of War, a change that will require action by Congress.

(By Ernest Scheyder, David Ljunggren and Julia Payne; Editing by Veronica Brown and Nick Zieminski)

Chile’s right-wing pivot puts mining policy under the microscope

(Illustration by MINING.COM featuring stock and archived images.)

Chile is entering a new political phase as a right-wing government prepares to take office, putting mining policy under renewed scrutiny in the world’s largest copper-producing country.

In recent years, the local politics have also been shaped by rising concern over crime and migration, particularly a surge in Venezuelan migration and highly visible organized crime. While the causes are complex, perceptions linking irregular migration and insecurity became politically potent. President-elect José Antonio Kast, who takes office on March 11, campaigned on stricter border control and tougher law-and-order policies, making security a central issue in Chile’s electoral shift.

Kast has also signalled a change in approach for the mining industry. He merged the ministries of Mining and Economy into a single portfolio and appointed Daniel Mas, an agronomist with no mining background, to lead it. In a country where mining underpins economic growth, labour and export revenue, the move has unsettled parts of the industry.

Carlos Piñeiro, copper analyst at Benchmark Mineral Intelligence, said the fusion could improve coordination but risks diluting mining-specific expertise. “Mining has very particular challenges, especially the non-renewability of resources,” he said. “If this model is going to work, specialists need to be involved in decision-making.”

The Chilean Mining Chamber was more critical. “Mining, despite being our national emblem and the activity that contributes the most resources to the public purse, is treated as second-rate,” chamber president Manuel Viera told MINING.COM.

Viera said the Chamber would have preferred a minister dedicated exclusively to mining, noting that previous experiences placing mining under broader economic portfolios “have not been positive.” While he does not foresee governance risks due to the sector’s maturity, he said mining’s success depends on technically grounded public policy rather than political decisions.

Mas takes charge of a sector that is expected to attract an estimated $105 billion in investments between now and 2034, alongside proposed reforms to permitting and environmental assessment frameworks that companies say have slowed approvals and raised costs.

Eduardo Zamanillo and Marta Rivera, authors of the book Mining is Dead. Long Live Geopolitical Mining, said the merger of the ministries sent an important institutional signal at a time when major economies are placing critical minerals at the centre of industrial and security strategies.

Although Chinese ownership of Chilean copper mines is limited, Beijing maintains influence through trade, financing and equipment supply. At the same time, US trade policy and Inflation Reduction Act-linked investment aim to anchor Chile more firmly within allied supply chains.

From a geopolitical mining perspective, Zamanillo and Rivera argue the move could either integrate mining more deeply into industrial policy, trade and innovation, aligning Chile with US-led reindustrialization efforts, or dilute the sector if it becomes just another file within a broad portfolio.

In their view, Chile’s opportunity lies in treating copper and lithium not merely as extractive revenues, but as platforms for building full value chains tied to allied markets. Whether the merger strengthens or weakens Chile’s position will depend on political will, technical leadership and the clarity of its long-term strategy.

Mineral ambitions meet execution risk

Chile’s policy debate has been further shaped by the release of the country’s first critical minerals strategy in the final weeks of outgoing President Gabriel Boric’s administration. The strategy aims to position Chile as a supplier not only of copper and lithium, but also of 14 other minerals considered essential to the energy transition and resilient supply chains.

Beyond copper and lithium, the list includes molybdenum, cobalt, rare earth elements, antimony, gold, silver, iron ore and boron, to reduce Chile’s historic over-reliance on a single commodity.

Viera said diversification is not optional.

“Depending almost exclusively on copper exposes the country to market cycles and uncertainty,” he said, noting that copper accounts for around 11% to 12% of GDP and more than 20% when considering economic impacts and multiplication effects. While copper will remain the backbone of the economy through at least 2035, he said minerals such as lithium, gold, molybdenum, rhenium and rare earth elements must help reduce long-term risk.

Piñeiro said Chile’s mining base is already broader than often assumed, citing molybdenum, rhenium, lithium, iodine, nitrates and a recovery in gold output. He added that projects such as Salares del Norte could lift national gold production by about 25%.

The strategy groups minerals according to Chile’s current position in global markets, with copper, lithium, molybdenum and rhenium in the top tier, and cobalt, rare earths, selenium and tellurium among longer-term options.

According to Viera, Chile’s challenge is not geology but policy. “The resources exist,” he said. “What is missing is a promotional and development plan that encourages exploration, investment and production.”

Others remain cautious. Daniel Weinstein, partner at Morales & Besa and president of the Mining Ministry’s advisory council, said the strategy provides a framework but does not change investment conditions on its own.

“Cursed” permitting system

José Cabello, director of Mineralium Consulting Group, said the critical minerals plan lacks concrete near-term measures.

“Nothing in the document implies a definitive boost to Chile’s production of these minerals,” he told MINING.COM, pointing to the absence of clear decisions to advance early-stage projects.

Viera echoed those concerns, arguing that without incentives for exploration and faster permitting, Chile risks missing the current price cycle. He described the permitting system as “cursed,” noting that a single project can require more than 500 permits over several years before seeing the light of day.

Zamanillo and Rivera argue that diversification should not be understood only as adding more minerals to a list, but as defining Chile’s position along emerging Western critical mineral value chains.

Trade data show Chile still exports most of its copper as bulk concentrates, heavily tied to China, while a smaller share of refined copper flows to the US and other allied markets.

In their view, the strategic opportunity lies in gradually shifting toward more refined output, midstream processing and higher-value services, using copper and lithium as anchors to attract investment aligned with US and allied industrial policy. Rather than relying predominantly on concentrate exports, Chile could rebalance toward deeper integration with North American value chains.

Copper dominance, rising constraints

Chile remains the world’s largest copper producer by a wide margin, accounting for roughly a quarter of global mined output. But declining ore grades, ageing deposits and rising regulatory complexity are constraining growth.

That strain is showing in production, which fell on a year-on-year basis every month of 2025. Official Cochilco figures peg the decrease in copper production last year at 2%, when compared to 2024 figures.

“Deposits are becoming deeper and lower grade,” Piñeiro said, adding that this makes Chile less competitive than jurisdictions such as the Democratic Republic of Congo, where higher grades support lower costs.

Industry groups are hoping Kast’s government will adopt a more pro-growth stance that would benefit the mining industry, but they warn that meaningful production increases will take time.

They also expect increased government involvement in the northern mining regions, such as Antofagasta and Tarapaca. These areas have seen visible irregular migration flows, heightening security concerns in areas central to copper and lithium production. Business groups have called for stronger border control and protection of logistics corridors. While core mining jobs are specialized, tighter migration rules could affect local labour markets in supporting sectors, analysts say.

Against that backdrop of regional strain, industry leaders are also focused on output and long-term competitiveness. Viera said Chile is “obligated” to exceed six million tonnes of fine copper per year, but stressed that growth must come with greater added value through industrialization. “The future lies in industrializing copper and lithium with a global perspective,” he said.

While Kast’s team has floated boosting mining output by as much as 20% within a year or two, council executive chairman Joaquin Villarino has said Chile’s project pipeline would more realistically lift copper production to around seven million tonnes over the next decade, assuming permitting efficiency and sustained investment.

Mariano Machado, Americas analyst at risk intelligence firm Verisk Maplecroft, said the 20% target is a political signal, not a literal schedule. “It signals urgency, not an immediate step change,” he said, noting Chile’s constraints stem from mature assets and long lead-times.

Machado pointed to Cochilco’s own projections, which show output peaking mid-decade before drifting down toward around 4.4 million tonnes by 2034. “We expect the sector to discount the headlines and watch what Kast can change early, including faster permit decisions and fewer procedural pauses,” he said.

From Zamanillo and Rivera’s perspective, Chile’s fundamentals remain strong in a world where capital is mobile and increasingly shaped by geopolitical considerations. They note that large pools of public and private funding in the United States and allied countries are being directed toward critical mineral supply chains, including reserves, loans and equity instruments. For Chile to compete with both other jurisdictions and high-growth sectors, they argue, it must shorten and clarify permitting timelines.

Long-life copper and lithium projects need predictable rules and sovereign speed, they say, if Chile wants to capture a larger share of the capital now being mobilized under the new critical minerals architecture.

More broadly, the nation’s shift toward a tougher law-and-order agenda shapes perceptions of regulatory certainty and state authority. For foreign copper and lithium investors, that trajectory feeds directly into risk assessments, even if migration itself is not tied to production.

Lithium: cost advantage, policy uncertainty

Chile remains the world’s second-largest lithium producer but has lost market share to faster-growing rivals. A national lithium strategy unveiled in 2023 increased state involvement and reshaped project development pathways.

Piñeiro said Chile’s cost advantage remains significant, citing the Atacama Salt Flat as one of the lowest-cost lithium brine resources globally.

Viera argued the country’s loss of leadership in lithium is political rather than geological. He added that Mining Code restrictions reserving lithium for the state have discouraged private investment despite high-quality reserves.

Machado said investor confidence in lithium hinges less on signed agreements than on operating stability.

“A deal is the easy part — a stable licence to operate is harder,” he said, noting that investors still price in political and social constraints.

While the Supreme Court’s backing of the Codelco and SQM agreement removed a legal challenge, he noted that investors continue to price in political and social constraints.

“Chile’s advantage matters if it can offer a stable operating model that survives social scrutiny and electoral cycles,” he said.

According to Viera, Chile could regain its position as the world’s largest or second-largest lithium producer within the next decade if restrictions are repealed and a pro-investment framework is adopted. He cited projects such as Nova Andino Litio, a joint venture between Codelco and SQM, and Salares Altoandinos as positive steps, but said far greater potential exists across more than 40 salt flats nationwide.

There is also Codelco’s Maricunga lithium partnership with Rio Tinto (ASX: RIO), which is still awaiting antitrust approvals from regulators in Chile and China before the companies can move ahead and sign a shareholders’ agreement.

A credibility test

As Kast’s government prepares to take office, Chile’s mining sector stands at a crossroads. Demand for copper, lithium and other critical minerals continues to rise, but investors are focused on whether political realities, regulatory reform and their execution will align.

For the Chilean Mining Chamber, the central issue is credibility. Viera said Chile must boost exploration incentives, modernize its smelting capacity and position mining as a strategic driver of development, not a fiscal fallback.

He added that the new Minister of Economy and Mining could play a pivotal role. “For more than 15 years, Chile has not launched any new projects to increase copper production. The only initiatives have replaced depleted reserves,” Viera said. “The country needs a nationwide exploration policy… Without new discoveries, we will fall behind.”

For Machado, credibility rests on delivery capacity, not rhetoric. He said the clearest signal would be a delivery framework that promotes productivity and talent, positioning mining as a modern export platform. He pointed to the Critical Minerals Strategy’s call for redesigned curricula, new specializations and stronger integration between industry, academia and the public sector.

That focus aligns with Chile’s broader competitiveness diagnosis, which highlights a persistent mismatch between available skills and labour-market demand. Machado noted that the mining workforce is already structurally tight and increasingly contractor-heavy.

“A robust plan for developing human capital is not an add-on, but a necessity to mitigate capex risk,” he said.

In an increasingly geopolitical minerals market, Chile’s challenge is no longer just the size of its resource base, but whether it can reliably convert that advantage into sustained supply.

———

Brazilian state firm fights Equinox Gold asset sale to CMOC

Aerial view of the plant at Aurizona Gold Mine in Brazil (foreground) and Piaba Pit (background). (Image courtesy of Equinox Gold)

A Brazilian state-run company is taking legal action to try to block the sale of a precious metals asset by Equinox Gold Corp. to one of China’s biggest miners.

Companhia Baiana de Produção Mineral, or CBPM, is seeking an emergency injunction for the immediate repossession of a lease area in Bahia, a state in Brazil’s Northeast Region, according to a document seen by Bloomberg News. It argues that Canada-based Equinox was a leaseholder – not the owner – of the concession and therefore was not entitled to sell it.

Equinox agreed to sell its Brazilian operations to CMOC Group, one of China’s biggest mining companies, in a $1 billion deal completed last month. The transaction — announced in December — includes several mines and deposits, in different Brazilian states, under Equinox’s entities in the South American nation.\\

CBPM’s allegations relate to only one of these assets, known as the Bahia Complex. No other properties were listed in the document filed with the court. The company had previously signaled its opposition to the transaction in a statement.

Equinox Gold has not received notice of any lawsuit, Ryan King, the company’s executive vice president for capital markets, said in an emailed response to a request for comment. Equinox “is confident that the sale of its operations in Brazil was fully compliant with Brazilian law and all contractual obligations,” he said on Thursday.

“While Equinox Gold is prepared to defend its position in court if required, the company remains open to engaging in constructive discussions with the State to seek a mutually agreeable resolution,” King said.

CMOC Group, the Chinese company, did not immediately respond to requests for comment. Many Chinese businesses are closed this week for the Lunar New Year holiday.

CBPM alleged that the transaction was agreed without its express consent, which it said was a condition of the agreement governing the mining area. The company has asked the Bahia State Court of Justice to terminate the lease agreement, and is also seeking damages.

“The Canadian company sold a mining right that does not belong to it,” CBPM president Henrique Carballal said by telephone.