US aluminum buyers hunt for alternatives as Iran war upends global supply

Aluminum buyers in the US are rushing to secure alternative supplies from Asia as the war on Iran disrupts a major foreign source — a development that threatens to hike the cost of the metal used in auto parts, appliances and beverage cans.

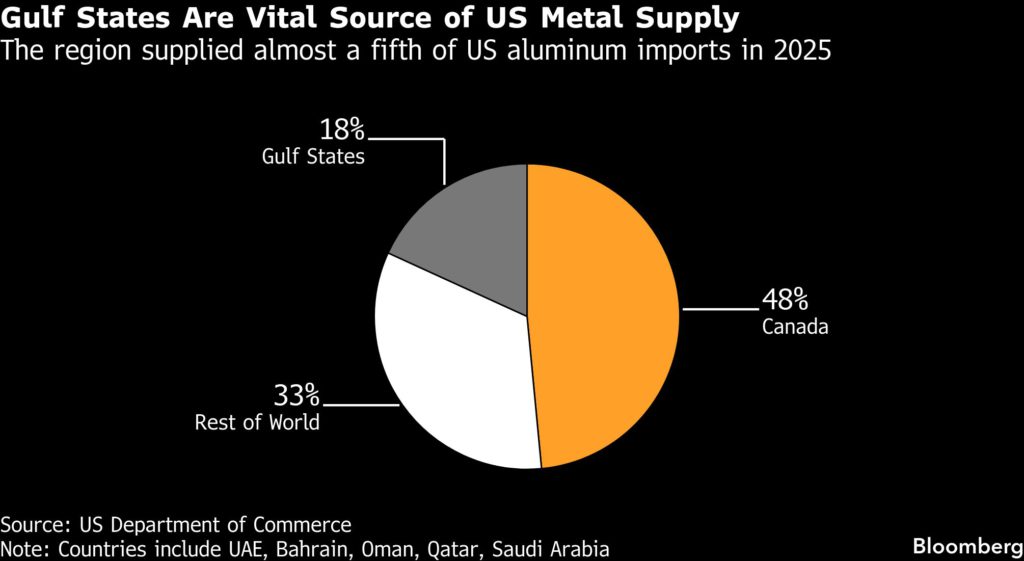

An effective halt on shipments through the Strait of Hormuz has already prompted two top producers in the region, Qatar and Bahrain, to suspend deliveries to customers. The US relies heavily on imports, with the Middle East supplying nearly a fifth of its aluminum last year, according to government data.

Andy Massey of Bonnell Aluminum said the company, which molds aluminum into shapes that can be used in products including cars and construction materials, is looking to source the metal from markets such as India and Australia. The Georgia-based manufacturer may even tap the domestic market for near-term deliveries if there’s metal that isn’t tied up in annual contracts.

“We’re all scrambling to figure out what’s happening on the ground” in the Middle East, said Massey, Bonnell’s vice president of metals, procurement and transportation. “I need to find alternative supplies over the next two days — fast — and make sure we don’t overpay.”

The Middle East supply turmoil comes at a particularly fragile moment for American aluminum consumers. They’ve already been squeezed by President Donald Trump’s import tariffs on the metal, which have driven up domestic prices and constrained flows from Canada, the largest foreign supplier to the US. Even brief interruptions to the supply of aluminum, prized by manufacturers for its abundance and low cost, can cause chaos for factories that tend to buy it on a just-in-time basis.

RM-Metals, a New Jersey-based supplier of specialty metal products, is facing a quandary similar to Bonnell’s. It’s seeking alternative sources as some of its shipments remain stuck in Dubai, according to vice president Sam Desai.

“Korea is a great option right now,” said Desai, adding that his firm is also looking at supplies from northern Europe. “It’s becoming very hard because the cost of aluminum itself has gone up” since the Iran war started.

Prices of the lightweight metal traded on the London Metal Exchange soared to the highest since 2022 this week. The so-called US Midwest premium — the amount added to global benchmarks to deliver aluminum to that region — climbed to a fresh record of $1.075 a pound. Before the Iran crisis, American manufacturers were already paying among the highest aluminum prices worldwide due to Trump’s 50% tariffs.

While aluminum from India is the most likely seaborne replacement for American consumers, shipping it across the Pacific takes about 60 days, according to Jean Simard, chief executive officer of Aluminum Association of Canada. Other alternatives include Brazil, Indonesia, Iceland and Norway, said Timna Tanners, an analyst at Wells Fargo Securities.

Meanwhile, shipments from Canada — the most obvious alternative for US buyers — have continued to decline under Trump’s tariffs. Producers there have increasingly favored Europe, where net returns have been more attractive than selling into the US market. At the same time, expectations that the levies could be eased or repealed in coming months have made US buyers wary of locking in large volumes, for fear of overpaying if the tariffs are later rolled back.

It could be “a timely moment to review” the US tariffs on Canadian aluminum, Simard said. Those levies, which fall under a law that allows duties on certain sectors to protect national security, weren’t affected by the recent Supreme Court decision that struck down other Trump tariffs.

About 6 million tons of primary aluminum — metal that has not yet been recycled — is now stranded in the Middle East, according to Simard. There is about 30 days’ supply of alumina, the raw material used to make aluminum, left for most smelters in the region, he said.

As the Iran crisis persists, aluminum producers in the Gulf region may have to curtail production as the near-shutdown of the Strait of Hormuz means they may soon run out of alumina. Those output cuts would have a sustained impact on global supply.

The regional conflict is likely to worsen a global aluminum deficit this year, according to Bank of America.

“Given the Middle East accounts for around 9% of global production and supply is at risk, we have raised our shortfall forecast to 1.5 million tons from 1 million tons,” analysts at the bank led by Michael Widmer said in a note Thursday.

Some suppliers are already going offline. Qatalum, jointly owned by Qatar’s state-owned aluminum producer and Norway’s Norsk Hydro ASA, said on Tuesday that it started a controlled shutdown of output because of a natural gas shortage, adding that a full restart could take six to 12 months.

“This could just be the tip of the iceberg. There could be more smelters affected, in which case this magnifies the impact,” said Tanners. “Aluminum smelters need to run full out — if not, they’re just going to shut. This isn’t a quick fix.”

(By Yvonne Yue Li, Jacob Lorinc and Mathieu Dion)

Column: Risks to Western aluminum supply rise as Iran war escalates

It is not just oil and gas that flow through the Strait of Hormuz, the Gulf’s key shipping choke point now threatened by the war with Iran.

The region is also a significant producer of aluminum, accounting for over 8% of global output last year, according to the International Aluminium Institute (IAI).

Over 5 million metric tons of metal are shipped through the Hormuz Strait each year by smelters in Bahrain, Qatar, Saudi Arabia and the United Arab Emirates. Huge amounts of bauxite and alumina travel the other way to feed the smelters.

None of these plants has yet been directly targeted in the escalating hostilities. But Qatar Aluminium, jointly owned by Norway’s Norsk Hydro and QatarEnergy, already faces possible closure because power supplies have been hit by the halt to the country’s liquefied natural gas production.

The longer the Strait of Hormuz is blocked, the greater the threat to Western manufacturers.

Key Western supplier

The Middle East has emerged as a major aluminum production hub over the last two decades, leveraging the region’s huge gas reserves to power the energy-intensive smelting process.

Gulf Cooperation Council (GCC) output has grown from 2.7 million tons in 2010 to 6.2 million last year, making it now the second largest regional supplier outside of China.

Actually, make that the largest.

The IAI’s production figures for Europe, the largest regional non-Chinese production hub on paper, include some 4 million tons of annual Russian metal.

Russian aluminum can’t be imported to the US due to Ukraine sanctions and the European Union is phasing out imports this year for the same reason.

Taken together, that makes GCC producers a core component of Western supply of a metal used across a wide spectrum of industries from automotive and construction to packaging.

Multiple channels

The potential impact on Western buyers runs down multiple channels.

Gulf smelters don’t just export primary aluminum. They are also major producers of bespoke alloys and feed local clusters of semi-manufactured product plants.

Bahrain, which hosts a 1.5-million-ton capacity smelter, exported over 1 million tons of alloy, 500,000 tons of products and 160,000 tons of virgin metal last year, according to the World Bureau of Metal Statistics, which uses official customs data.

Exports flowed to 70 different countries, including significant quantities to Europe and the US.

The diversity of product and destination means that any protracted halt to either regional production or export flows would hit multiple countries and multiple parts of the processing chain.

Vulnerable market

The aluminum market is as vulnerable as it’s been for many years to such supply disruption.

China, the world’s largest producer, has seen growth in both output and exports slow as its smelter sector runs up against Beijing’s capacity cap of 45 million tons.

Western buyers, particularly those in Europe, have been squeezed by the phase-out of Russian imports, the closure of the Mozal smelter in Mozambique, and the production hit to Century Aluminum’s Grundartangi smelter in Iceland.

London Metal Exchange (LME) inventory, including metal in off-warrant storage, fell by 331,000 tons last year and is down another 84,000 tons since the start of January.

LME aluminum prices had already been rising before the Iran crisis hit with full force.

Tuesday’s news that Qatar Aluminium may be facing a suspension of operations has lifted three-month metal to $3,315 per ton, within striking distance of January’s near four-year high of $3,356 per ton.

Power threat

While Western aluminum buyers are facing an immediate supply shock, there is likely to be a second one in the form of higher energy prices.

One reason why GCC production has become so important to the Western market is the closure of other smelters due to high power prices. The Mozal plant in Mozambique, a major supplier to the European market, is a case in point.

Europe itself has lost several plants in the wake of the power price surge that followed Russia’s invasion of Ukraine four years ago.

Another energy shock is the last thing Western aluminum producers need.

And the last thing Western buyers need is a loss of supply from producers sitting on the wrong side of the Strait of Hormuz.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by Marguerita Choy)