Australia’s Fuels Dependence Turns Into a Crisis

- Australia’s long-standing model of exporting crude and importing refined fuels is breaking down amidst supply disruptions.

- Around 80–90% of its fuel demand (around 850,000 b/d) is import-dependent, leaving the system highly exposed to Asian export restrictions.

- With product stocks at ~30 days and domestic refining barely covering 20% of demand, import disruptions are rapidly translating into a real availability crisis.

Australia has long been synonymous with resource abundance — a country rich in minerals, energy, and hydrocarbons, including its own crude oil production. Yet today, it finds itself in the paradoxical position of scrambling for fuel, as disruptions to imports expose just how dependent the nation has become on refined products from abroad.

Australia continues to produce oil domestically, with crude output around 320,000 b/d, yet its downstream dependency is overwhelming. In 2025, the country imported roughly 850,000 b/d of refined products against total demand of about 1.1 million b/d, leaving 80–90% of consumption reliant on external suppliers. Even before the current disruption, strategic fuel stocks stood at just 37 days — barely one-third of IEA requirements.

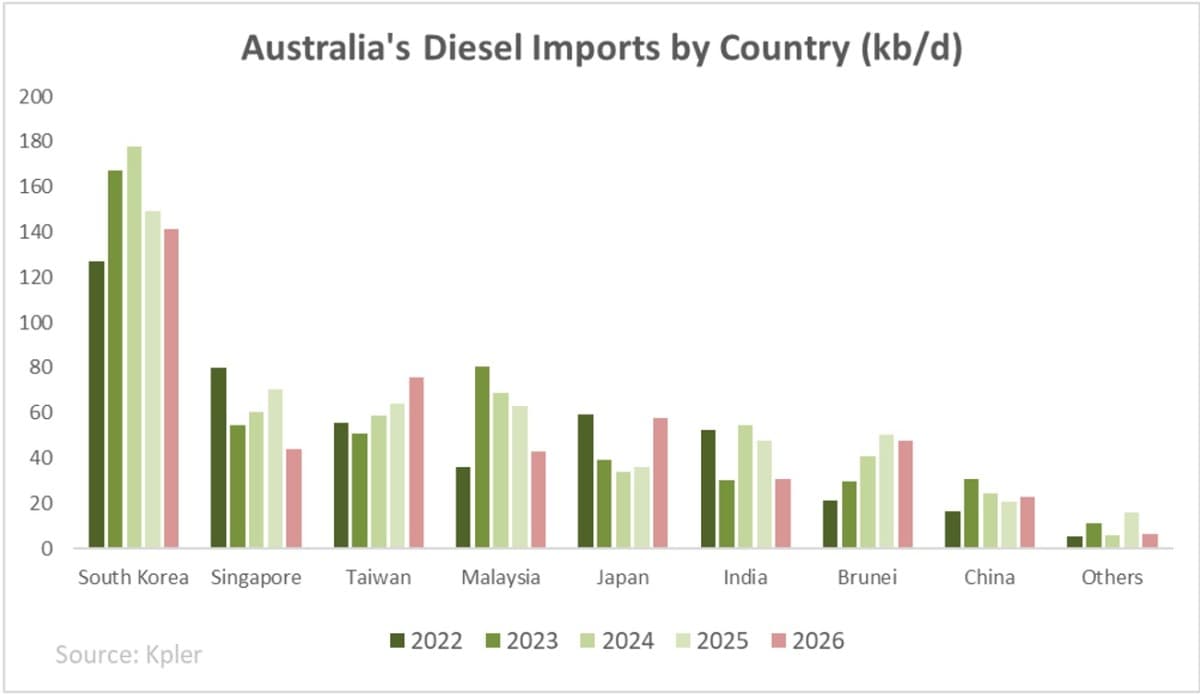

The trigger for today’s unraveling crisis has been a combination of disrupted shipping through the Strait of Hormuz and export restrictions imposed by key Asian suppliers. China, Thailand, and South Korea – all major exporters to Australia – have introduced full or partial curbs on refined product exports. South Korea alone accounts for roughly a quarter of Australia’s imports, supplying around 220,000 b/d – about half of which is diesel (around 120,000 b/d), the most critical fuel in Australia’s demand structure and the segment with the deepest supply deficit.

Jet fuel has largely been sourced from China, with February 2026 cargoes reaching around 190,000 b/d. Gasoline flows are mostly sourced from Singapore and South Korea, which together accounted for roughly two-thirds of Australia’s average 210,000 b/d gasoline imports in 2025.

The impact has been immediate. On March 22, Australia’s Energy Minister confirmed that six tankers carrying refined products from Malaysia, Singapore, and South Korea had either been cancelled or deferred. Officials have repeatedly stressed that cargoes are still arriving nonetheless. In reality, however, theincoming volumes on water largely reflect shipments that departed before the disruption took hold – with the true extent of the shortage yet to demonstrate itself in the upcoming days.

For the first time in decades, Australia has turned to the US as an emergency supplier. Around 240,000 tons of refined fuels have been secured – including roughly 120,000 tons of diesel, 70,000–80,000 tons of gasoline, and about 35,000 tons of jet fuel. The shipments consist of at least six vessels: three multi-product cargoes from ExxonMobil, two diesel shipments from BP, and one gasoline cargo from Vitol. Collectively, this marks the largest monthly inflow of US fuel to Australia since the 1990s.

The logistics alone underline the severity of the disruption. Transit times from the US Gulf Coast to Australia stretch to 55–60 days, with freight costs around $20/bbl, compared with typical Asia-Pacific routes that stood at $5–6/bbl before the crisis. The price dynamics of regional products briefly blurred that disadvantage: on March 18, delivered gasoline and diesel from Singapore and Houston converged at roughly $161/bbl. As of March 25, Singapore cargoes look more attractive again — around $153/bbl versus $164/bbl from Houston. But pricing is no longer the decisive factor. The issue has shifted to physical availability. With unsold cargoes in Asia increasingly rare, the US – despite longer routes and more expensive freight – might become the only reliable way out of this imports’ deadlock for Canberra.

Australia’s domestic refining system offers little relief. The country operates just two refineries – Lytton (110,000 b/d) and Geelong (120,000 b/d) – with combined capacity of 230,000 b/d, covering only around 20% of national demand. Both facilities are structurally constrained. They depend entirely on imported crude, as Australia’s domestic output (largely ultra-light, condensate-rich streams with API gravity above 55–60) is unsuitable for their configuration. The refineries themselves are aging assets, built in the 1950s and 1960s, designed for a different crude blend and market environment. Their output profile also mismatches domestic demand. Australian refineries are gasoline-heavy, producing around 100,000 b/d of gasoline and 80,000 b/d of diesel, while consumption is skewed toward diesel – the segment now under the greatest stress.

The refining sector’s decline reflects years of structural pressure. Between 2012 and 2022, five refineries ceased operations, driven into the ground by weak margins, high operating costs, and competition from highly complex mega-refineries across Asia. To keep the remaining capacity alive, the government has extended financial support to both remaining plants. The Fuel Security Services Payment (FSSP) scheme (originally due to expire in 2027) has been extended to 2030, effectively subsidizing domestic refining. Maintenance schedules, including planned work at Lytton, have been deferred as authorities push facilities to sustain maximum throughput.

In parallel, the government has activated emergency response measures. On March 13, it released 4.8 million barrels of gasoline and diesel from strategic reserves. Yet the country’s limited stockpile – structurally below IEA thresholds – constrains how long such interventions can be sustained. As of March 17, Australia held just 30 days of diesel and jet fuel, and 38 days of gasoline (as opposed to the IEA requirement of 90 days stock levels). All categories remain even below the national Minimum Stockholding Obligations — diesel by 18%, jet fuel by 28%, and gasoline by 78%.

Authorities have moved to relax fuel specifications in an effort to widen supply options. Gasoline sulphur limits have been temporarily eased from 10 ppm to 50 ppm, while diesel flashpoint requirements have been reduced from 61.5°C to 60.5°C for a six-month period. These adjustments allow a broader range of imported fuels to enter the market and enable the two domestic refiners to sell previously non-compliant products locally.

A potential resolution to Australia’s import struggles may lie with two key suppliers. First, South Korea. Korean authorities have introduced limits on refined product exports, capping them at 2025 monthly average levels. While this restricts any growth in supply, it does not fully exclude Australia from accessing Korean volumes - provided it remains competitive on pricing and bids up. Second, India. Prior to the EU’s January 2026 restrictions on imports of products refined from Russian crude, India exported approximately 160,000 b/d of diesel to Europe. With US sanctions on Russian barrels now lifted and Indian refiners increasing their purchases of Russian crude, these previously Europe-bound volumes are being redirected. In this context, Australia could emerge as a natural alternative destination for such flows.

Refineries may be running at full capacity, but their limited scale – and production skewed toward gasoline rather than the more critical diesel – leaves a gap they cannot close. Imports are still arriving, but largely from cargoes that sailed before the disruption and the imposition of export restrictions across Asia. With fuel stocks already well below the IEA’s 90-day benchmark, the outlook is increasingly strained. If anything, the crisis has already delivered its key lesson: for a country as remote as Australia, domestic refining is no longer just a matter of economic efficiency – it is a question of national security.

By Natalia Katona for Oilprice.com

No comments:

Post a Comment