AU

Central banks’ gold buying momentum carries into 2026

Central banks remained firm buyers of gold in 2026, even as prices were skyrocketing to records in January, though the institutions’ appetite for bullion could face a stern test amid rising geopolitical tensions in the Middle East.

After surging to an all-time peak of nearly $5,600 an ounce earlier this year, gold has come under immense pressure in recent weeks as elevated energy prices from the ongoing Middle East war sparked fears of global inflation and reduced expectations of lower interest rates — a scenario that hurts the safe-haven metal.

At the same time, official-sector demand remains resilient in the first few months, according to the World Gold Council, which forecasts central banks to purchase roughly 850 tonnes of gold in 2026 — almost the same as last year.

Early 2026 trends

WGC data shows countries such as China and Kazakhstan remained active buyers in 2026, extending a multi-year trend of strong official demand, while countries like Indonesia and Malaysia have also turned into buyers after a long hiatus.

“A phenomenon we’ve been seeing in the last few months is new central banks, or central banks that have been inactive or absent from the gold market for a long time, entering the gold market,” Shaokai Fan, global head of world banks for the WGC, said on Tuesday.

“I think that might be a trend that will continue into 2026,” Fan added.

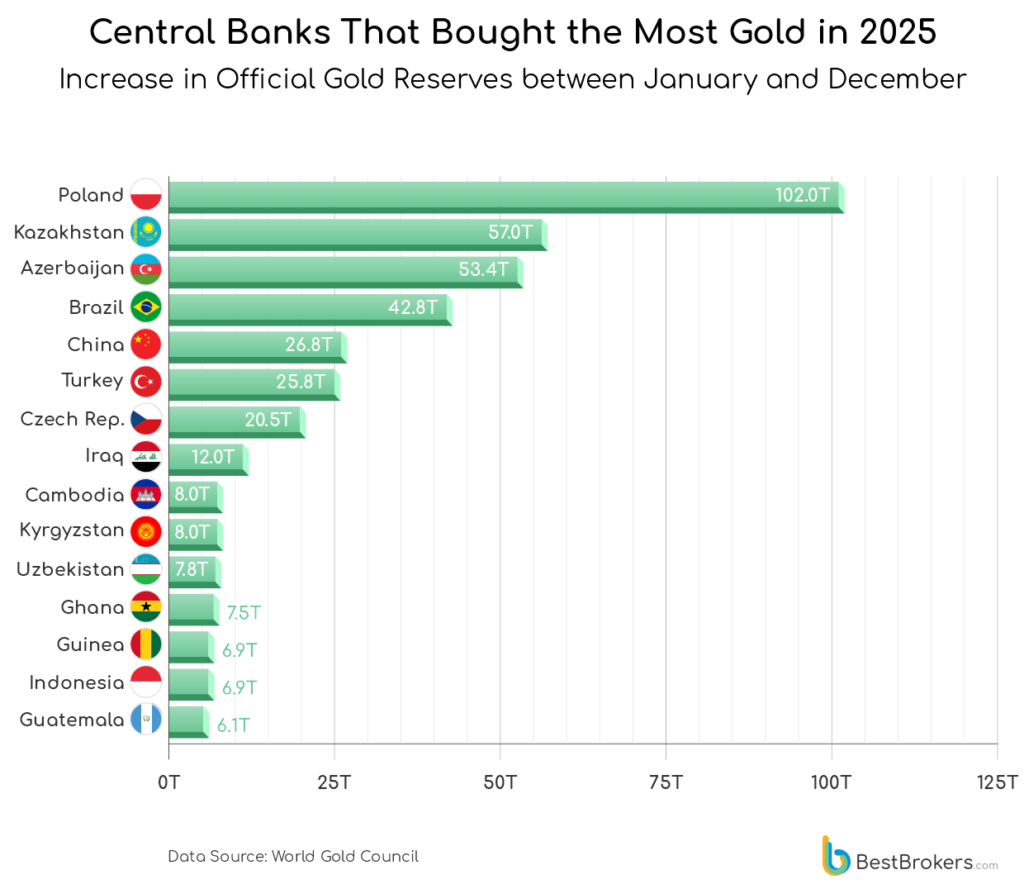

2025: another year of central bank buying

The buying momentum seen this year follows a sustained wave of purchases in 2025, when central banks again ranked among the largest sources of gold demand globally. Total official-sector buying reached about 863 tonnes for the year, according to WGC, slightly below the record levels of 2022–2023 but still historically strong.

Based on WGC data, analysts at investing research platform BestBrokers compiled the top buyers of gold in 2025:

Poland emerged as the standout buyer, adding more than 80 tonnes to its reserves, while Kazakhstan and Brazil also posted significant increases. China and Turkey continued to accumulate gold as well, albeit at a slower pace compared to prior years.

The buying spree comes amid a broader trend that has seen central banks collectively add large volumes of gold since 2020, helping drive prices higher and reinforcing bullion’s role as a strategic reserve asset.

Analysts point to a combination of factors behind the trend, including geopolitical uncertainty, concerns over currency debasement, and a desire among emerging economies to reduce reliance on the US dollar.

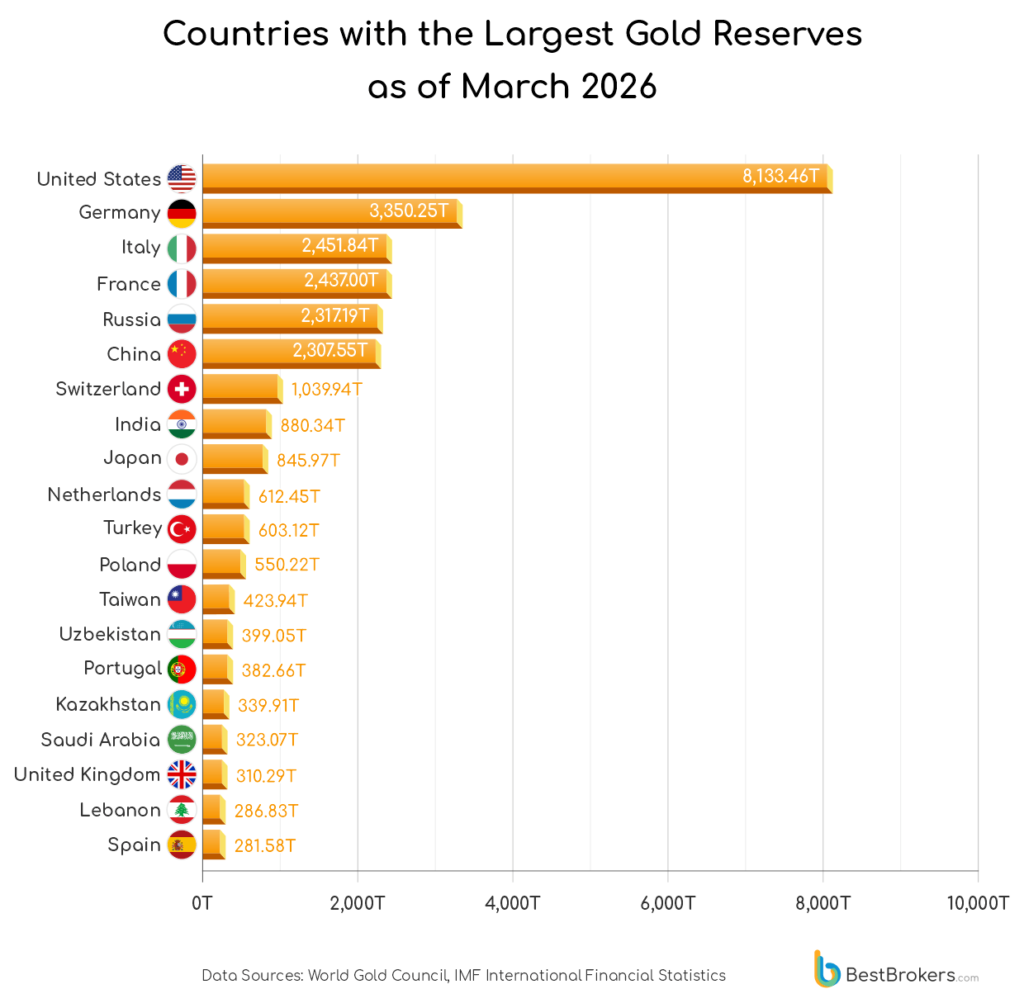

Who holds the most gold today

Despite the surge in buying from emerging markets, global gold reserves remain heavily concentrated among advanced economies.

The US continues to hold by far the largest stockpile, with more than 8,100 tonnes of gold, followed by Germany at roughly 3,350 tonnes. Italy and France rank next, each holding around 2,400–2,450 tonnes, while Russia and China have built reserves exceeding 2,300 tonnes apiece.

Other major holders include Switzerland, India and Japan, each with several hundred tonnes of gold in their central bank reserves.

Collectively, the US and European nations still account for a dominant share of global gold holdings, though emerging markets have been steadily increasing their positions over the past decade.

Short-term uncertainty

However, as some analysts have pointed out, the war in the Middle East may have forced some states to sell some of their gold to shore up foreign exchange reserves amid elevated oil prices — despite the underlying fundamentals of holding the metal remaining intact.

“Gold’s recent plunge marks a dramatic shift in investor sentiment, with the metal facing one of its sharpest weekly declines and edging toward bear-market territory,” Alan Goldberg, lead data analyst at BestBrokers, said.

“While some market participants view this as a temporary correction following record highs in early 2026, others warn that volatility could persist, testing central banks’ appetite for continued accumulation,” he added.

“It’s too early to see if the same phenomenon has occurred with this month’s rout,” WGC’s Fan said.

Additional central banks to buy gold on geopolitical risks, WGC says

Gold’s role as a hedge against de-dollarization and geopolitical risk is expected to spur central banks who have been absent from the market to buy the precious metal this year, a World Gold Council (WGC) executive said on Tuesday.

In recent months, central banks from Guatemala, Indonesia and Malaysia have all bought gold, either following a long hiatus or for the first time ever, Shaokai Fan, global head of world banks for the WGC said on Tuesday.

“A phenomenon we’ve been seeing in the last few months is new central banks, or central banks that have been inactive or absent from the gold market for a long time, entering the gold market,” he said.

“I think that might be a trend that will continue into 2026,” he said.

Some central banks are also buying gold from small-scale domestic producers to support the local industry and to stop those gold sales going to “bad actors”, Fan added without elaborating.

This month, gold prices have plunged by more than a $1,000 per troy ounce to last trade around $4,340, and historical trends suggest it’s partly due to margin call-related selling, Fan told Reuters on the sidelines of Minerals Week in Canberra.

The record peak for gold was just shy of $5,600 in late January.

During a gold selloff in October, central banks stocked up on the metal, but it’s too early to see if the same phenomenon has occurred with this month’s rout, Fan said.

Central bank demand for gold may decline because higher prices not only deter new buying but also increase the weight of existing gold holdings relative to total reserves, he added.

The WGC expects record gold prices to slow purchases by central banks to 850 metric tons this year from 863 tons in 2025, even though their buying remains elevated when compared to the pre-2022 level, the industry group said in January.

According to WGC figures, central bank buying accounted for some 17% of total demand last year.

(By Melanie Burton; Editing by Kevin Buckland)

South Africa’s gold producers stay in the shallows as prices surge

Record gold prices are pushing South Africa’s beleaguered mining industry to find new ways to recover the metal that sidestep the costly deep-shaft mining of old, industry executives said.

But with no boom in new mine development expected, they’re unlikely to add enough production any time soon to significantly lift the stubbornly low output of a country that for more than a century was the world’s biggest gold producer.

South Africa’s gold exploration has dropped nearly 90% from the 1990s, with spending on mineral exploration declining to just $43 million in 2025 from $900 million in 2006, according to Statistics South Africa.

Its gold production has plummeted to 90 metric tons annually from a 1970 peak of 1,000 tons on dwindling economically viable reserves, labour unrest, and the geologically taxing conditions in the world’s deepest mines.

Gold prices meanwhile have surged, climbing about 60% in 2025 to a series of all-time highs on trade tensions, central bank buying and expectations of US rate cuts. But rising prices are yet to entice South African miners to invest significantly in new output.

Producers favour shallower projects

As prices climb, diversified miner Sibanye Stillwater is prioritizing shallow, high-margin projects to boost its gold output. Its plans centre on Burnstone, a development project it says will be a low-cost, long-life operation.

It is also pursuing growth opportunities with its 50%-owned DRDGold, which recovers gold from waste dumps, CEO Richard Stewart said on a February 20 results call.

Harmony Gold, South Africa’s biggest gold producer, is looking to potentially recover 5.7 million ounces through waste retreatment, CEO Beyers Nel told analysts on March 11.

Underground mining expansion remains unlikely for Harmony.

“Given the lead time it takes to develop into an area, you will possibly only start mining there in about two to three years’ time,” finance director Boipelo Lekubo told Reuters. “Who knows what the gold price will be then?”

New mine in iconic basin

West Wits Mining launched South Africa’s first new underground mine in 15 years last October. The Qala Shallows mine taps into the Witwatersrand basin, reputed to have produced about half of all the gold ever mined in the world.

The mine is shallower than more established shafts and has access to existing infrastructure, cutting capital costs. It is also mechanized, reducing labour costs, and uses hydropower to extract ore, instead of the more expensive traditional compressed air.

“We actually got a very, very economical project, given the new gold prices,” West Wits Mining CEO Rudi Deysel told Reuters during a tour of the mine.

The company plans an initial annual output of 70,000 ounces and envisions scaling to 200,000 ounces in future phases.

But in the short term, not much change is expected in South African output. Next year the Minerals Council of South Africa expects gold production to remain at around 90 metric tons – not far from levels at which it has bumped along for the last five years.

(By Nelson Banya; Editing by Olivia Kumwenda-Mtambo and Jan Harvey)

Risk-off trade keeps gold price volatile as Iran war spooks investors

Acute volatility in gold prices is set to persist in the short term as investors cut risk, with the Iran war boosting inflation fears, curbing bets on interest rate cuts, and weighing on the outlook for global growth, analysts said.

However, in the long term its role as a store of wealth will reassert itself, they said.

With the Iran conflict entering its fourth week, spot gold is down 15% since hostilities began on February 28, and 22% below its January record high.

Gold is used as a hedge against inflation, but an increase in bets on rates staying higher for longer in the short- to medium-term due to the energy price jump is a headwind for bullion as an asset which pays no interest.

“Gold should do well in a stagflationary environment, it always has, but there may be more profit taking and liquidation first,” said John Reade, senior market strategist at the World Gold Council.

“2025’s trades are being unwound, and we are yet to see 2026 stagflationary trades.”

Liquidity needs outweigh safe-haven demand

Gold’s one-day jump at the start of the Iran war followed by a period of falls is consistent with previous episodes of extreme shocks, where liquidity needs outweigh safe-haven demand in the early stages, analysts at ANZ said.

When Russia invaded Ukraine in February 2022, gold prices rose initially but then fell back as the inflation shock fed through to rates.

Gold’s price rally from $1,650 per ounce in November 2022 to a record $5,595 in January 2026 was driven by demand from central banks and institutional investors, before a wave of speculative retail demand, particularly in Asia, became a feature of the market.

“The bigger picture remains intact: ballooning G7 budget deficits, sticky inflation and central bank foreign reserve diversification amid sustained deglobalization,” said SP Angel analyst John Meyer.

Gold-backed ETFs seen outflows

Gold touched a four-month low of $4,098 in early hours on Monday as stock markets in China – the world’s leading buyer of gold – tumbled by the most in a year.

Spot gold prices were last down 2.5% at $4,377 an ounce, having trimmed losses after US President Donald Trump said he would delay any strikes on Iran’s energy infrastructure.

On the global demand side, gold-backed exchange-traded funds have seen outflows of $7.9 billion, or 54.8 metric tons, mainly in the US, to 4,117.9 tons since the conflict in the Middle East started, according to the WGC data.

(By Polina Devitt; Editing by Jan Harvey)

No comments:

Post a Comment