The geopolitical shocks of the Gulf war are dominating headlines and investor sentiment, but these shocks rarely act as the primary engine of global economic downturns, according to a note by Ben May, director of global macro research at Oxford Economics.

“Heightened geopolitical risk doesn’t inevitably translate into economic volatility or cyclical downturns,” says May. “But historical experience shows that heightened geopolitical risk doesn’t inevitably translate into economic volatility or cyclical downturns.”

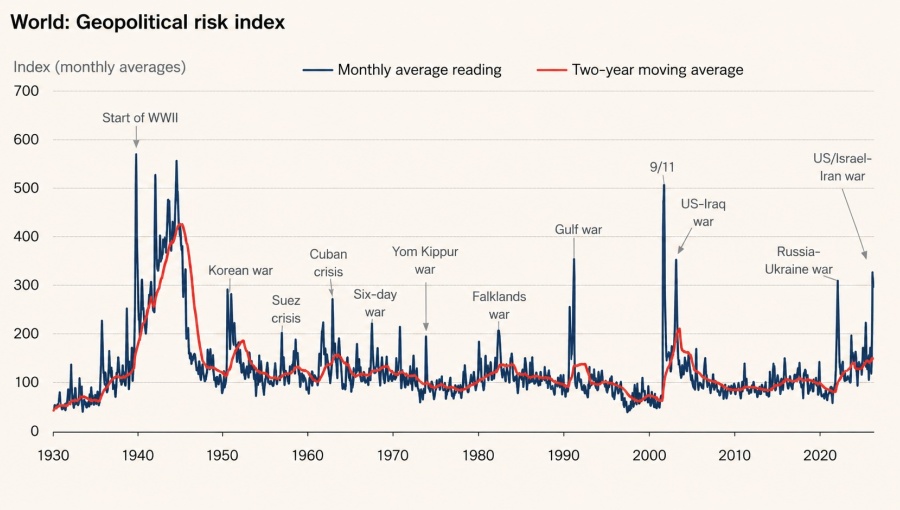

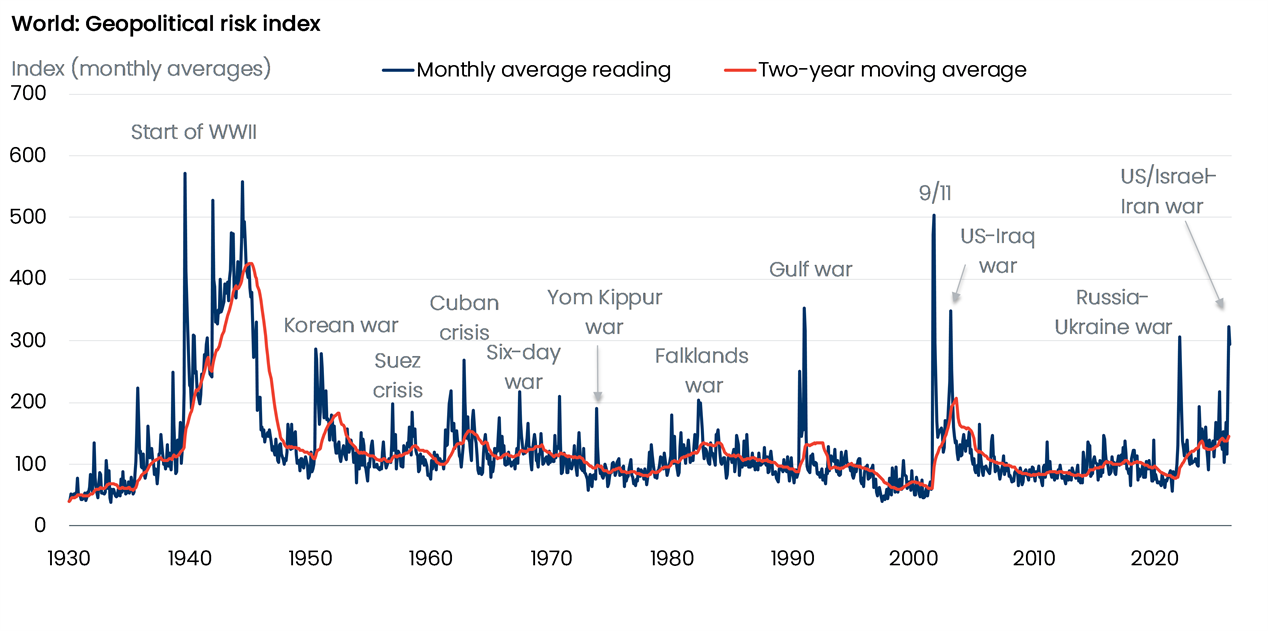

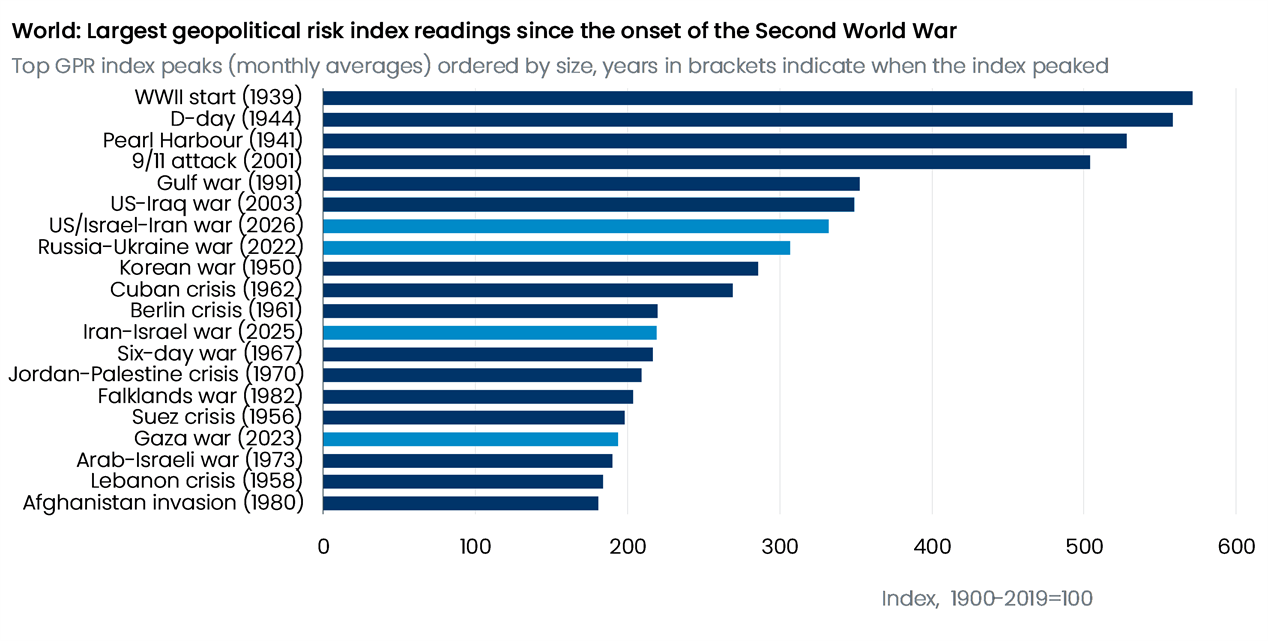

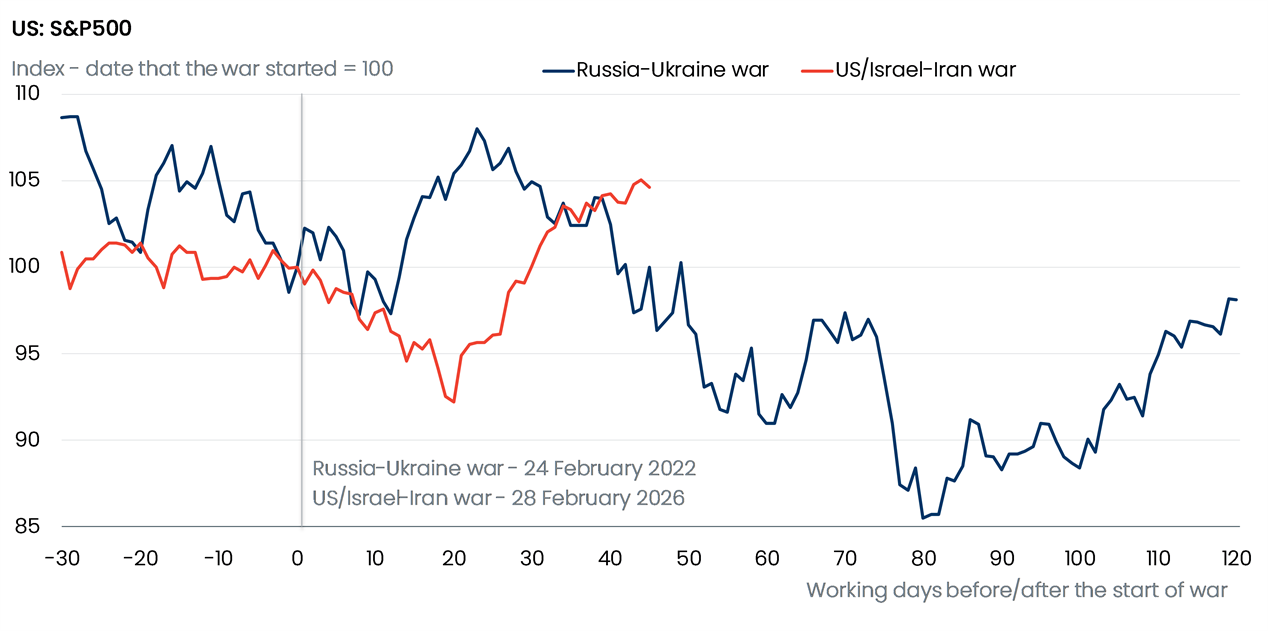

The recent surge in the Geopolitical Risk (GPR) index has reinforced the perception that the global economy has entered a more dangerous phase. Yet, as May notes, “the upward shift since Russia’s invasion of Ukraine looks similar to the step jump after the September 11 attacks — and that period was followed by an upswing in global growth.” In other words, while geopolitical tensions have intensified since the start of Operation Epic Fury on February 28 and clearly this is “the worst energy disruption in history” according to the International Energy Agency (IEA), the crisis has not yet moved into uncharted territory.

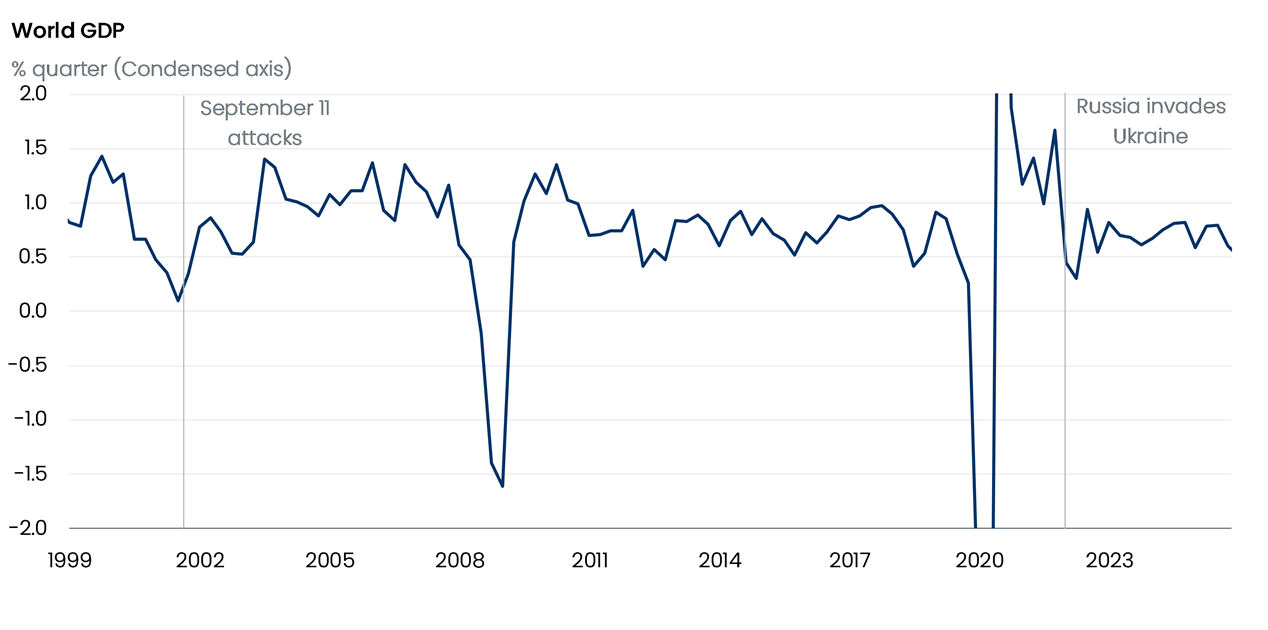

The distinction matters. Since 2022, the GPR index has recorded frequent spikes, bookended by the Russia-Ukraine war and the more recent US-Israel confrontation with Iran. But, as May points out, “global GDP growth has been remarkably stable despite these shocks.” The implication is clear: geopolitics alone is insufficient to derail the global economy.

The recent downgrade to global growth expectations reflects this more nuanced reality. Oxford Economics has cut its 2026 global GDP growth forecast by 0.6 percentage points and now expects the level of world GDP to be 0.8% lower than projected earlier in the year. But May is careful to stress that “while the war contributed to this, it wasn’t the only surprise.” Instead, the post-pandemic reopening, supply chain disruptions, and the subsequent inflation shock played decisive roles in tightening financial conditions and dragging on growth.

The true transmission mechanism from geopolitics to the real economy lies elsewhere. “The commodity and financial channels are the crucial shock spreaders,” he says. A useful rule-of-thumb is “a sustained $10 increase in oil prices reduces annual global GDP growth by around 0.1 percentage points.”

During the early phase of the Ukraine war, oil briefly rose from around $90 to $110 per barrel, before falling back to roughly $80 by the end of 2022. The impact, while meaningful, was temporary and limited at the global level.

Europe, however, felt a sharper blow after gas prices skyrocketed in the 2022 energy crisis, illustrating that the economic fallout of geopolitical shocks is often unevenly distributed.

“The surge in natural gas prices caused by Russia turning off the taps was far more concentrated than the oil shock,” May notes, underlining the importance of regional dynamics that are more affected, but don’t necessarily spread and have a global impact.

Nevertheless, the current Gulf War presents a potentially more serious risk, largely because of its implications for global energy supplies. “The Middle East conflict has the capacity to trigger a more substantial economic hit than the Russia-Ukraine war due to the sharper rise in oil prices everywhere,” May says.

Yet even here, Oxford Economics believes its baseline forecasts already incorporate a reasonable allowance for disruption. The greater danger would come from a prolonged interruption to shipping through the Strait of Hormuz, rather than from a broader collapse in confidence.

And the delivery of oil out of the Persian Gulf is restricted, not stopped. About half of the oil that used to be exported via the Strait of Hormuz is still leaving, via Iran’s own unfettered exports, the the Kingdom of Saudi Arabia (KSA)’s westward pipelines that terminate at the port of Yanbu on the Red Sea, and Gulf of Oman oil terminals belonging to the UAE and Oman. At the same time the US has ramped up production and exports and new Venezuelan oil has come onto the market.

One of the more surprising findings is how broader economic uncertainty has remained. “Spikes in geopolitical risk don’t typically push economic uncertainty measures up sharply,” May observes. Forecast dispersion for US GDP and inflation has actually declined since 2022, suggesting that markets have not been gripped by systemic fear. Even historically significant events such as the Gulf War, 9/11, and the Iraq war generated only short-lived increases in uncertainty.

This resilience extends to financial markets. While equity prices initially dipped following geopolitical shocks, subsequent movements have been driven more by monetary policy than by conflict itself. “The tightening in financial conditions in 2022 was not predominantly down to the Russia-Ukraine war,” May argues, pointing instead to the role of rising interest rates and inflation expectations.

None of this is to say that geopolitics is irrelevant. The counterfactual — a world without recent conflicts — would almost certainly have delivered stronger growth. Oxford Economics estimates that global GDP growth in 2022 and 2023 fell short of expectations by around 0.7 percentage points, though only part of this can be attributed to geopolitical tensions.

More broadly, the persistence of elevated geopolitical risk may yet have longer-term consequences. “It will take time to assess whether spillover effects from heightened uncertainty will prove larger than expected,” May cautions. Investment decisions, in particular, tend to respond with a lag, meaning the full impact may not yet be visible.

As IntelliNews has reported, the peak pain from major crises tends to arrive with a long delay. The short-term pain to sectors like aviation and fertilisers are already very visible, but a food shock is on its way that will hit this autumn, and an inflation shock will follow that, spilling into 2027. Separately, the world is on course for a “super El Niño” this year that means all these problems will be exacerbated by what is likely to be the fourth hottest year of all-time and a fourth disaster season that could be as bad, or worse, than the preceding three seasons.

For now, however, the evidence points in a different direction. “Geopolitical shocks may unsettle markets, but they rarely act as the primary driver of global downturns,” May concludes. Instead, it is the secondary effects — higher energy prices, tighter financial conditions, and structural economic adjustments — that ultimately shape the trajectory of growth.

No comments:

Post a Comment