Canada turns from U.S. to Europe as Iran war propels aluminum higher

Aluminum Market Facing ‘Serious and Prolonged Supply Outage’

- The Iran war and Strait of Hormuz disruption have triggered a historic aluminum supply crisis, damaging major Gulf smelters and cutting Western production by 2.4 million tonnes in just two months.

- Aluminum prices and physical premiums have surged globally as inventories collapse, with traders warning of the biggest base metals supply shock since 2000 and a potential multi-million-ton market deficit.

- Key industries, including power grids, EVs, solar, construction, aerospace, and packaging face rising costs and shortages, while the U.S. market is especially strained by high tariffs and falling Canadian imports.

The war in Iran and the accompanying shipping bottleneck are triggering a historic crisis in the aluminum market, with potentially devastating knock-on effects across sectors that depend on the base metal.

Aluminum is the third most used metal in the world, behind only iron and steel.

Aluminum is prized for its high strength-to-weight ratio, corrosion resistance, and excellent conductivity — properties that make it essential for everything from beverage cans and cooking foil to aerospace components and power grids.

Key sectors utilizing aluminum include packaging, transportation, defense, construction, electronics, solar power, and electricity transmission. Aluminum is also used in everyday consumer goods such as cookware, patio furniture, bicycle frames, and sporting goods.

For the past 20 years, the aluminum market has been in structural oversupply with high inventories. But everything changed with the war in Iran and the effective closure of the Strait of Hormuz.

Discussing how the conflict is affecting non-ferrous base metals markets, Argus Media reported in April that The most immediate and visible effect has been in aluminium because the Middle East is a major export hub, accounting for around 9pc of global supply.

Gulf Cooperation Council countries produce around 6 million tonnes per year of primary aluminum, with the majority exported through the Strait of Hormuz to Europe, Asia and North America.

Two Gulf aluminum smelters were damaged in missile strikes: Emirates Global Aluminium’s (EGA)’s Al Taweelah plant in the UAE, and Aluminium Bahrain, the largest production plant outside of China.

Al Taweelah will take a year to repair, while at least one other producer — Qatalum — has reduced capacity, Reuters’ metals columnist Andy Home wrote last week, adding that the continued closure of the Strait of Hormuz is causing major logistical problems for those still operating.

Gulf production has plummeted to its lowest level in over a decade in April, according to the International Aluminium Institute (IAI).

The attacks saw aluminum prices soar to their highest levels since the start of the Ukraine war in February 2022. As of this writing, UK aluminum futures were trading at $3,678.60 per tonne, the highest in over four years. Since the war began, UK prices are up 16%.

Despite falling short of 2022 record highs, Home argues that “red lights are flashing on the market dashboard” due to the sharp tightening in London Metal Exchange (LME) time-spreads, and the rise in physical premiums around the world.

LME time-spreads (also called calendar spreads) represent the price difference between different maturity or prompt dates for the same base metal. These spreads are essential for physical hedgers, financiers and traders looking to manage risk along the forward curve.

The LME's benchmark cash-to-three-months spread flipped into backwardation in early March and cash is currently trading at an $80 premium, the tightest the market has been since 2007. Back then it was a short-lived squeeze on short position holders. This time around the tightness is persistent and looks structural.

That's because LME stocks, which were already low, have been raided as traders look to fill the supply-chain gaps opening up due to the loss of Gulf production.

LME registered stocks have fallen by a third to 339,475 tons since the start of the year.

As for the rise in physical premiums, the Chicago Mercantile Exchange (CME) spot premium for Japan has more than doubled to $316 per ton over the LME price since the start of hostilities; and the European duty-paid premium has jumped by 58% and the duty-unpaid by 75% since the beginning of March.

The U.S. Midwest premium had only risen by 8%, but American buyers were already paying record prices to secure physical metal due to 50% import tariffs.

Another manifestation of the aluminum supply shock is in non-exchange segments of the market such as billet, a semi-finished, solid bar of metal used in transportation and construction.

According to price reporting agency Fastmarkets, in Rotterdam, the premium for aluminum extrusion billet has more than doubled to $1,100 over the LME base price.

The loss of production in the Gulf has been compounded by the closure due to high energy prices of the Mozal smelter in Mozambique.

The combined hit has been a 2.4-million-ton drop in Western production over the last two months, according to the IAI's latest figures. Things may get worse depending on whether those Gulf smelters still producing can source enough raw materials via routes that circumvent the Strait of Hormuz.

China's giant aluminium production base has stepped up production but is now running close to the government's capacity cap, leaving little room for further significant upside.

An earlier article by Zero Hedge had analysts at Mercuria, a Geneva-based commodities consulting firm, sounding the alarm on the global aluminum market:

The scale of the supply shock we’re seeing in the aluminum market is probably the largest single supply shock a base metals market has suffered in the post-2000 era,” Mercuria commodities analyst Nick Snowdon told Reuters on the sidelines of the Financial Times Commodities Global Summit in Lausanne, Switzerland.

Mercuria estimates the aluminum market could face at least a 2-million-ton deficit by the end of the year, potentially worse if the US-Iran conflict drags on.

JPMorgan analysts warned that the aluminum market is descending into a black hole, or a “metaphorical point of no return,” where the “global aluminum market will face a serious and prolonged supply outage,” even if vessel flows through the Hormuz chokepoint resume in the near term.

The war in Iran is creating severe supply shortages and driving up costs across the US aluminum sector; Middle Eastern nations supply roughly a fifth of American aluminum.

Latitude Media reports the supply chain disruption is likely to have complicated consequences for a variety of sectors but particularly energy, where aluminum is used extensively for overhead power transmission lines, solar panel frames, wind turbine structures, and both utility-scale and EV batteries.

The problem for US aluminum buyers stems from the steep 50% tariff the Trump administration imposed on aluminum articles and derivative products imported into the United States. The tariff was primarily directed at Canada, which represents the majority, or 60% of US aluminum imports.

But the tariff has driven up the regional premium, which is the surcharge paid on top of the LME benchmark price. A higher US price is required to incentivize foreign suppliers to continue shipping the metal into the country despite the additional cost, Latitude Media explained.

“The situation in the Middle East will add further upward pressure to the premiums, which are already very high and will get higher as people compete to get metal,” said Uday Patel, senior research manager for global aluminum markets at Wood Mackenzie, adding that anyone involved in the production of energy equipment, such as wiring cables, is likely to see an increase in costs. “The U.S. is absolutely in a bind at the moment.”

Meanwhile, Canadian aluminum imports have fallen as the country diversifies its markets beyond the United States. Before the tariffs they were consistently above 200,000 tonnes per month, but since April they have dropped to roughly 50,000 tonnes.

Without a steady supply from the Middle East, says Latitude Media, that gap is hard to fill. Two unsavory alternatives are China and Russia. The latter, while not subject to a total global prohibition, remains practically inaccessible to the US due to a persistent 200% tariff and the reluctance of international banks to provide credit for transactions with Russia.

Short-term, Latitude Media says these solutions are either unviable or difficult to implement, leaving aluminum buyers scrambling to get their hands on the metal and likely paying more for it.

“For the U.S. and for the electricity, distribution, and transmission sector, it’s going to be expensive,” Patel said.

By Andrew Topf for Oilprice.com

Column: Warning lights flash as aluminum reels from Gulf shock

(The opinions expressed here are those of Andy Home, a columnist for Reuters.)

The Iran war is shaping up to be one of the biggest supply shocks in the history of the aluminum market.

Gulf production of the metal, which is used across sectors as diverse as transport, packaging and solar panels, plummeted to its lowest level in over a decade in April, according to the International Aluminium Institute (IAI). Regional run-rates dropped by an annualized 2 million metric tons over March and April.

Two Gulf aluminum smelters have been damaged in missile strikes. Emirates Global Aluminium’s Al Taweelah plant will take a year to repair. At least one other producer – Qatalum – has reduced capacity.

The continued closure of the Strait of Hormuz is causing major logistical problems for those still operating.

The Gulf accounts for over a fifth of non-Chinese production and is a core supplier to buyers in Japan, South Korea, the European Union and the United States.

The scale of the supply hit is not obvious from the London Metal Exchange (LME) price , which at $3,650 per ton is up by just 14% since the start of hostilities and has yet to scale the 2022 heights that followed Russia’s invasion of Ukraine.

But red lights are flashing on the market dashboard.

LME tightens as stocks drain away

The first is the sharp tightening in LME time-spreads.

The LME’s benchmark cash-to-three-months spread flipped into backwardation in early March and cash is currently trading at an $80 premium, the tightest the market has been since 2007. Back then it was a short-lived squeeze on short position holders. This time around the tightness is persistent and looks structural.

That’s because LME stocks, which were already low, have been raided as traders look to fill the supply-chain gaps opening up due to the loss of Gulf production.

LME registered stocks have fallen by a third to 339,475 tons since the start of the year. The last couple of weeks have seen almost 68,000 tons cancelled in preparation for physical load-out.

The residual tonnage left on LME warrant is now largely Russian aluminum being stored at the South Korean port of Gwangyang. That’s no use to either US or European buyers due to sanctions imposed over the Ukraine war.

The recent daily drawdowns haven’t been transfers to off-warrant storage. These LME “shadow” stocks have also been draining away and are the lowest they’ve been since the exchange started reporting off-warrant stocks in 2020.

Physical premiums surge

The second warning sign is the rise in physical premiums around the world.

The CME spot premium for Japan has more than doubled to $316 per ton over the LME price since the start of hostilities. Japanese buyers have accepted a premium of $350 for their second-quarter deliveries, which is the highest surcharge in 11 years.

The European duty-paid premium has jumped by 58% and the duty-unpaid by 75% since the start of March.

The US Midwest premium has risen by a relatively modest 8% but American buyers were already paying record numbers to secure physical metal thanks to the impact of 50% import tariffs.

These are the most visible manifestations of the Gulf supply shock. Less visible is what is going on in non-exchange-traded segments of the market such as billet, a product used by construction and transport sectors.

In Rotterdam, the premium for aluminum extrusion billet has more than doubled to $1,100 over the LME base price, according to price reporting agency Fastmarkets.

Structural deficit

The relative calm of the LME outright price belies a severe tightening of availability along the processing chain.

While LME traders are pricing in the ebb and flow of headlines around the Iran war, physical buyers are paying up just to secure enough metal in a market that is heading towards a structural supply deficit.

The loss of production in the Gulf has been compounded by the closure due to high energy prices of the Mozal smelter in Mozambique.

The combined hit has been a 2.4-million-ton drop in Western production over the last two months, according to the IAI’s latest figures. Things may get worse depending on whether those Gulf smelters still producing can source enough raw materials via routes that circumvent the Strait of Hormuz.

China’s giant aluminum production base has stepped up production but is now running close to the government’s capacity cap, leaving little room for further significant upside.

While the country is showing signs of increasing exports in reaction to the Gulf supply hit, these shipments will mostly be in the form of semi-processed products such as strip, foil and bars rather than raw metal.

Inventories, both exchange and non-exchange, can provide some short-term buffer but the longer the Strait of Hormuz remains closed, the thinner that cushion becomes.

All of this is a generational shock for a market that has lived with structural oversupply and high inventories for the last 20 years.

The aluminum price isn’t yet reflecting the tectonic changes in the supply chain. Physical buyers, however, already know how much the landscape has changed.

(Editing by Marguerita Choy)

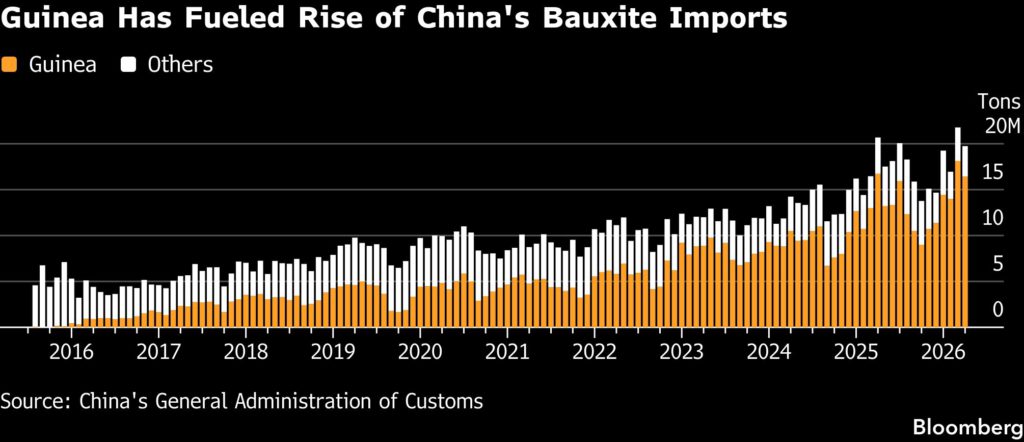

China aluminum market braces for launch of Guinea export curbs

China’s aluminum industry is preparing for significant disruption to its raw materials supplies after Guinea, the world’s biggest bauxite producer, said it’s finalizing plans to limit exports of the ore.

The West African nation will set out steps to control bauxite exports in June, Mines and Geology Minister Bouna Sylla said in an interview with Bloomberg News. Guinea’s shipments — which surged by more than a quarter in 2025 to 183 million tons — have played a pivotal role for China’s aluminum sector in feeding its refineries and keeping costs low.

The minister said the rapid growth of bauxite exports has triggered a slump in global prices that the government wants to address. “Supply mustn’t exceed demand,” Sylla said. “We want to regulate the quantity to raise prices back to reasonable levels.”

The plan adds to a wave of interventions by commodity-rich nations aimed at influencing prices and encouraging investment in domestic processing. Democratic Republic of Congo and Zimbabwe restricted exports of cobalt and lithium, respectively, which are mainly shipped to China. Indonesia is ramping up years of resource nationalism with sweeping plans for a state agency to oversee its exports.

Most of Guinea’s bauxite is shipped to China, where it’s first refined into alumina and then used in the Asian nation’s battalion of aluminum smelters. Last year, around three quarters of China’s 201 million tons of bauxite imports came from the country, and monthly volumes from Guinea reached a record above 18 million tons in March.

Alumina on China’s Shanghai Futures Exchange surged by as much as 4.3% after Guinea’s plan to 2,865 yuan ($422) a ton, swinging from a loss to a gain for this year. Traders in China said they were waiting for details of the measures, amid speculation that Guinea’s government could impose a cap of 150 million tons of bauxite annually.

“That would turn a surplus market into a significantly tight market, greatly boosting bauxite prices,” said Peng Dinggui, analyst with Zhongtai Futures Co. “That’s going to accelerate the exit of Chinese alumina capacity.”

Price slump

Bauxite delivered to China dropped to a four-year low below $60 a ton earlier this year, down from a record $120 in January 2025, according to data from Asian Metal Inc. Mining investors “have an interest in seeing prices rise,” Sylla added.

Guinea is pushing miners to build refineries capable of producing alumina, with three facilities already at the planning stage or under construction to add to the country’s single existing plant.

China’s State Power Investment Corp., Aluminum Corp. of China Ltd. and a consortium headed by Singapore-registered Winning International Group are developing those refineries, which will process some of the bauxite produced at their operations in the country.

The government wants a total of five new refineries, with the combined capacity to produce 7.2 million tons of alumina annually, according to Sylla. That volume would still only absorb less than 15% of the bauxite mined in Guinea last year.

Sylla said Guinea also intends to seek investors for an aluminum smelter. “For us, the transition from alumina to aluminum is inevitable,” he said.

(By Ougna Camara and William Clowes)