The Very Real Possibility Of Peak Oil Supply

By Alex Kimani - Dec 26, 2020

Three months ago, British oil giant BP Plc. (NYSE:BP) sent shockwaves through the oil and gas sector after it declared that Peak Oil demand was already behind us. In the company’s 2020 Energy Outlook, chief executive Bernard Looney pledged that BP would increase its renewables spending twentyfold to $5 billion a year by 2030 and ‘‘... not enter any new countries for oil and gas exploration.’’ That announcement came as a bit of a shocker given how aggressive BP has been in exploring new oil and gas frontiers.

The investing universe appears to concur with BP’s sentiments, with the oil and gas sector consistently emerging as the worst performer over the past decade. The sector suffered yet another blow after the largest investor-owned oil company in the world, ExxonMobil (NYSE:XOM), was kicked out of the Dow Jones Industrial Average in August, leaving Chevron (NYSE:CVX) as the sector’s sole representative in the index.

Meanwhile, oil prices appear stuck in the mid-40s with little prospects of climbing to the mid-50s that most shale producers need to drill profitably.

Delving deeper into the global oil and gas outlook suggests that it’s peak oil supply, not peak oil demand, that’s likely to start dominating headlines as the quarters roll on.

Source: Bloomberg

Peak Oil Demand

When many analysts talk about Peak Oil, they are usually referring to that point in time when global oil demand will enter a phase of terminal and irreversible decline.

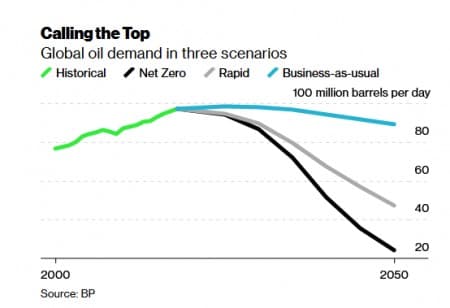

According to BP, this point has already come and gone, with oil demand slated to fall by at least 10% in the current decade and by as much as 50% over the next two. BP notes that historically, energy demand has risen steadily in tandem with global economic growth with few interruptions; however, the COVID-19 crisis and increased climate action might have permanently altered that playbook.

BP has modeled 3 possible scenarios for the future of global fuel and electricity demand: Business as Usual, Rapid Transition, and Net-Zero. Here’s the kicker: BP says that even under the most optimistic scenario where energy policy keeps evolving at pretty much the pace it is today (Business as Usual) oil demand will still suffer declines—only at a later date and a slower pace compared to the other two scenarios.

The oil bulls, however, can take comfort in the fact that under the Business-as-Usual scenario, BP sees oil demand remaining at 2018 levels of 97-98 million barrels per day till 2030 before falling to 94 million barrels per day in 2040 and eventually to 89 million barrels per day three decades from now. That’s a loss in demand of less than 1% per year through 2050.

However, things could look very different under the other two scenarios that entail aggressive government policies aimed at reaching net-zero status by 2050 as well as carbon prices and other interventions aimed at limiting global warming.

Under the Rapid Transition scenario (moderately aggressive), BP sees oil demand falling 10% by 2030 and nearly 15% under Net Zero (most aggressive).

In other words, the decline in oil demand is bound to be catastrophic for the industry over the next decade under any other scenario other than Business-as-Usual.

Luckily, this is the scenario that’s likely to dominate over the next decade.

David Blackmon, a Texas-based independent energy analyst/consultant, has told Forbes that many analysts are skeptical about BP’s grim outlook. Indeed, Blackmon says a “Business as Usual” scenario appears the most likely path for the time being, given the time the global economy might take to recover from Covid-19 as well as the trillions of dollars that would be required to implement the other two cases.

Further, it’s important to note that BP made those projections before Covid-19 vaccines had entered the fray. With several viable vaccine candidates now on the scene, there’s a good chance that the global economy might recover at a faster-than-expected clip and thus help oil demand to recover more rapidly than earlier estimates.

Peak Oil Supply

Though rarely discussed seriously, Peak Oil Supply remains a distinct possibility over the next couple of years.

In the past, supply-side “peak oil” theory mostly turned out to be wrong mainly because its proponents invariably underestimated the enormity of yet-to-be-discovered resources. In more recent years, demand-side “peak oil” theory has always managed to overestimate the ability of renewable energy sources and electric vehicles to displace fossil fuels.

Then, of course, few could have foretold the explosive growth of U.S. shale that added 13 million barrels per day to global supply from 1-2 million b/d in the space of just a decade.

It’s ironic that the shale crisis is likely to be responsible for triggering Peak Oil Supply.

In an excellent op/ed, vice chairman of IHS Markit Dan Yergin observes that it’s almost inevitable that shale output will go in reverse and decline thanks to drastic cutbacks in investment and only later recover at a slow pace. Shale oil wells decline at an exceptionally fast clip and therefore require constant drilling to replenish the lost supply. Although the U.S. rig count appears to be stabilizing thanks to oil prices rebounding from low-30s to mid-40s, the latest tally of 320 remains far below the year-ago figure of 802.

Although OPEC+ nations currently have about 8 million barrels of oil per day of spare capacity, the current price levels do not support much drilling at all, and the extra oil might only be enough to cover the shortfall by U.S. shale.

By Alex Kimani for Oilprice.com

The investing universe appears to concur with BP’s sentiments, with the oil and gas sector consistently emerging as the worst performer over the past decade. The sector suffered yet another blow after the largest investor-owned oil company in the world, ExxonMobil (NYSE:XOM), was kicked out of the Dow Jones Industrial Average in August, leaving Chevron (NYSE:CVX) as the sector’s sole representative in the index.

Meanwhile, oil prices appear stuck in the mid-40s with little prospects of climbing to the mid-50s that most shale producers need to drill profitably.

Delving deeper into the global oil and gas outlook suggests that it’s peak oil supply, not peak oil demand, that’s likely to start dominating headlines as the quarters roll on.

Source: Bloomberg

Peak Oil Demand

When many analysts talk about Peak Oil, they are usually referring to that point in time when global oil demand will enter a phase of terminal and irreversible decline.

According to BP, this point has already come and gone, with oil demand slated to fall by at least 10% in the current decade and by as much as 50% over the next two. BP notes that historically, energy demand has risen steadily in tandem with global economic growth with few interruptions; however, the COVID-19 crisis and increased climate action might have permanently altered that playbook.

BP has modeled 3 possible scenarios for the future of global fuel and electricity demand: Business as Usual, Rapid Transition, and Net-Zero. Here’s the kicker: BP says that even under the most optimistic scenario where energy policy keeps evolving at pretty much the pace it is today (Business as Usual) oil demand will still suffer declines—only at a later date and a slower pace compared to the other two scenarios.

The oil bulls, however, can take comfort in the fact that under the Business-as-Usual scenario, BP sees oil demand remaining at 2018 levels of 97-98 million barrels per day till 2030 before falling to 94 million barrels per day in 2040 and eventually to 89 million barrels per day three decades from now. That’s a loss in demand of less than 1% per year through 2050.

However, things could look very different under the other two scenarios that entail aggressive government policies aimed at reaching net-zero status by 2050 as well as carbon prices and other interventions aimed at limiting global warming.

Under the Rapid Transition scenario (moderately aggressive), BP sees oil demand falling 10% by 2030 and nearly 15% under Net Zero (most aggressive).

In other words, the decline in oil demand is bound to be catastrophic for the industry over the next decade under any other scenario other than Business-as-Usual.

Luckily, this is the scenario that’s likely to dominate over the next decade.

David Blackmon, a Texas-based independent energy analyst/consultant, has told Forbes that many analysts are skeptical about BP’s grim outlook. Indeed, Blackmon says a “Business as Usual” scenario appears the most likely path for the time being, given the time the global economy might take to recover from Covid-19 as well as the trillions of dollars that would be required to implement the other two cases.

Further, it’s important to note that BP made those projections before Covid-19 vaccines had entered the fray. With several viable vaccine candidates now on the scene, there’s a good chance that the global economy might recover at a faster-than-expected clip and thus help oil demand to recover more rapidly than earlier estimates.

Peak Oil Supply

Though rarely discussed seriously, Peak Oil Supply remains a distinct possibility over the next couple of years.

In the past, supply-side “peak oil” theory mostly turned out to be wrong mainly because its proponents invariably underestimated the enormity of yet-to-be-discovered resources. In more recent years, demand-side “peak oil” theory has always managed to overestimate the ability of renewable energy sources and electric vehicles to displace fossil fuels.

Then, of course, few could have foretold the explosive growth of U.S. shale that added 13 million barrels per day to global supply from 1-2 million b/d in the space of just a decade.

It’s ironic that the shale crisis is likely to be responsible for triggering Peak Oil Supply.

In an excellent op/ed, vice chairman of IHS Markit Dan Yergin observes that it’s almost inevitable that shale output will go in reverse and decline thanks to drastic cutbacks in investment and only later recover at a slow pace. Shale oil wells decline at an exceptionally fast clip and therefore require constant drilling to replenish the lost supply. Although the U.S. rig count appears to be stabilizing thanks to oil prices rebounding from low-30s to mid-40s, the latest tally of 320 remains far below the year-ago figure of 802.

Although OPEC+ nations currently have about 8 million barrels of oil per day of spare capacity, the current price levels do not support much drilling at all, and the extra oil might only be enough to cover the shortfall by U.S. shale.

By Alex Kimani for Oilprice.com

Alex Kimani is a veteran finance writer, investor, engineer and researcher for Safehaven.com

No comments:

Post a Comment