It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

The global copper market enjoyed one of its best years in 2025. The threat of US tariffs on the industrial metal and its elevated status as a critical mineral, together with major supply disruptions globally, all played a part to help to lift prices 40% last year.

That run extended into 2026, as expectations of surging AI-driven demand and persistent supply constraints drove prices to a record of $14,500 a tonne in January. This week, copper is nearing another record.

The prospect of higher mining costs due to rising energy prices and a shortage of sulfuric acid, which is used in a fifth of the global copper production, is considered the next big catalyst for copper prices, a Sprott analyst recently said.

Goldman Sachs is also optimistic of copper surging higher again, due to the supply-side disruptions. The International Copper Study Group recently outright abandoned its previous surplus projections, now forecasting a 150,000-tonne deficit for 2026.

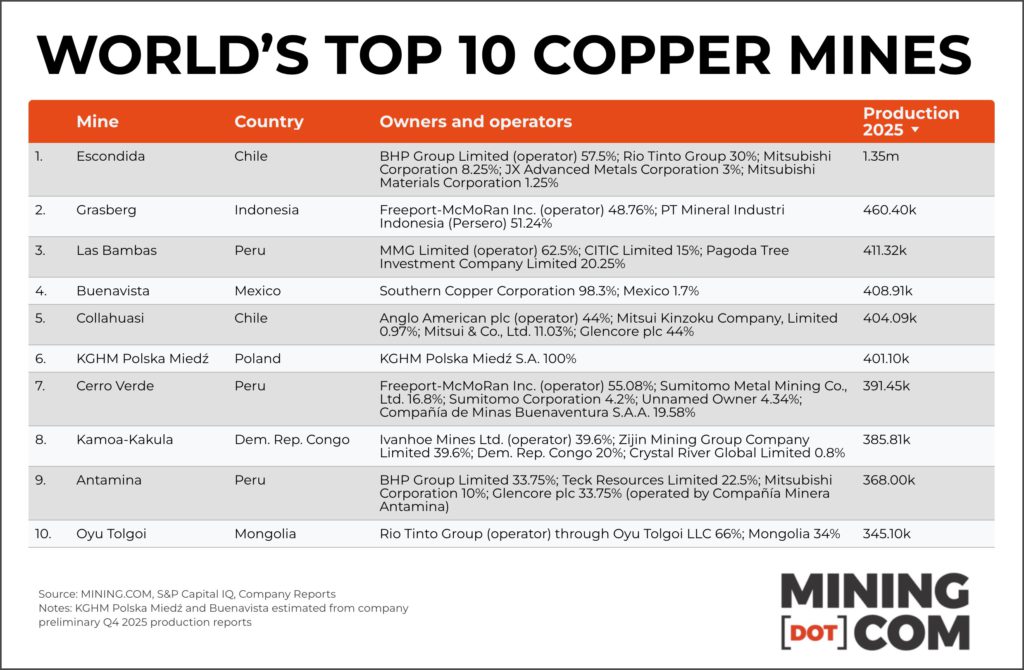

The top 10 mines, many of which have been in production for decades (some even trace roots back to the late 1800s) are responsible for more than a fifth of total global mined production – producing 4.9 million tonnes in 2025.

And surprisingly, after only recently being surpassed by BHP as the world’s number one copper producer on an attributable basis, Chile’s state owned Codelco does not have any of its operations qualify for the top 10.

As last year amply showed disruption at these giant operations (like the Grasberg and Kamoa-Kakula accidents that saw 100s of thousands of tonnes taken off the market,) can have a big impact on copper prices.

1. Escondida

Escondida in Chile, a joint venture between BHP, Rio Tinto, Mitsubishi, and JX Advanced Metals holds the top spot, producing 1,347.6 kts of copper metal in 2025. Escondida has long ranked the world’s biggest copper mine, but BHP’s operational review for the nine months to March 31 pointed to record material mined and concentrator throughput.

Las Bambas mine in Peru, owned jointly by China’s MMG, CITIC and Pagoda Tree Investment Company, churned out 411.3 kts in 2025. The mine was plagued by protests in 2024, but protesters agreed to lift a road blockade on a key Peruvian transport route, and operations resumed in April 2025.

4. Buenavista

Southern Copper’s Buenavista mine in Mexico moves up in this year’s ranking to fourth place with 409.4 kts produced. Copper has been mined at the historic site, 22 miles south of the US border, since 1899.

5. Collahuasi

Chile’s Collahuasi mine, a joint venture between Glencore, Anglo American and Mitsui produced produced 404.1 kts. In April this year, contractors finished building a system that will carry water from the coastal town of Punta Patache to the Ujina deposit, more than 4,400 meters above sea level, as part of a $1 billion infrastructure improvement project.

Cerro Verde in Peru, a joint venture between Freeport-McMohRan, Sumitomo and Buenaventura takes seventh place, producing 391.5 kts. The Peruvian government first mined Cerro Verde’s oxide ores and built one of the world’s first SX/EW facilities in 1972.

8. Kamoa-Kakula

The Kamoa-Kakula complex in the Democratic Republic of Congo, owned jointly by Ivanhoe Mines, Zijin Mining, Crystal River and the DRC government drops from third place last year to seventh — it produced 385.8 kts. Ivanhoe halted operations for three weeks in 2025 after seismic activity severely flooded the underground mine. In April, Ivanhoe slashed near-term production guidance, citing a shift toward underground development, rehabilitation and access work that will constrain ore delivery over the next 18 to 24 months.

9. Antamina

Antamina in Peru, co-owned by BHP, Glencore, Teck and Mitsubishi, moves up to ninth from 10th place, producing 368 kts. Last year, Antamina’s operators forecasted an almost 20% boost in cooper output.

10. Oyu Tolgoi

Oyu Tolgoi, a joint venture between Rio Tinto and the Mongolian government, churned out 345.1 kts. The government, which holds a 34% stake through state-owned Erdenes Mongol LLC., this year demanded earlier profit payments and a larger share of revenue, reopening negotiations over the $18-billion project’s commercial terms.

Honorable mentions: Morenci in Arizona, USA (313,100 tonnes), Quellaveco in Peru (309,900 tonnes), Los Pelambres in Chile (295,400 tonnes)

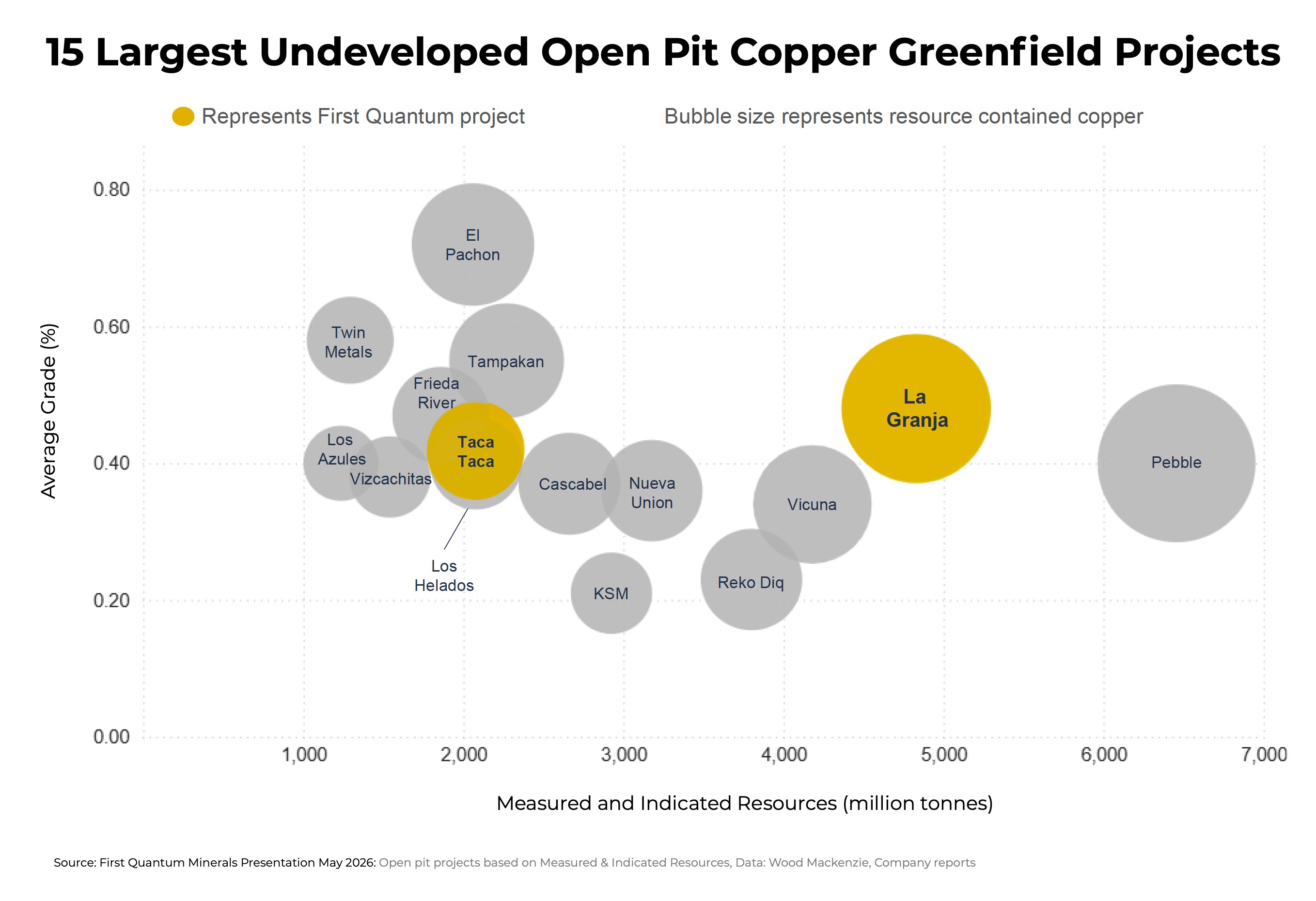

CHART: First Quantum’s Peru project joins ranks of copper giants

First Quantum has completed 370,000 metres of drilling at La Granja. Image: First Quantum Minerals.

First Quantum Minerals (TSX: FM) has filed a new NI 43-101 technical report for its La Granja project in the Cajamarca region of northern Peru it holds with Rio Tinto, outlining one of the copper sector’s largest undeveloped deposits.

First Quantum, said according to La Granja’s (meaning “the farm”) updated mineral resource, the orebody contains 4.8 billion tonnes of measured and indicated resources grading 0.48% copper, equal to 23.0 million tonnes of contained copper.

A further 5.2 billion tonnes grading 0.40% copper sits in the inferred category, containing another 20.7 million tonnes of copper, setting La Granja up as a tier-1, multigenerational asset, in the words of the company.

That places La Granja second among undeveloped copper projects in terms of measured and indicated resources behind only Northern Dynasty’s Pebble in Alaska and when including operating assets, also behind Kamoa-Kakula, the Ivanhoe Mines complex in the Democratic Republic of Congo.

First Quantum acquired the majority stake for only $105 million and has since spent $70 million out of a committed $546 million to advance the project.

Engineering challenges

In an interview conducted last year, First Quantum CEO Tristan Pascall said while the La Granja deal “wasn’t up there in the deals in terms of dollars, in terms of copper in the ground is one of the largest deals done in the last 10, 20 years.”

“Rio Tinto saw in First Quantum a partner that could want a challenging project, because it’s challenging from an engineering perspective, and particularly around deleterious elements like arsenic,” Pascall said. “We had a development hypothesis that we went to Rio with, and really that revolved around dealing with the orebody in a different manner.”

First Quantum says the drillhole database for La Granja now consists of a whopping 832 diamond holes totalling a whopping 370,000 metres, with more planned. The deposit remains open at depth with further exploration targets, according to the company.

Last month, ahead of the latest mineral resource estimate, Pascal told a group of reporters during a tour of its Zambian mines the company has spent the last three years of drilling validating this hypothesis:

“Our view was that it [the arsenic] wasn’t disseminated, that it was discreet and we could package it. That means you have assayable concentrate through a conventional flow sheet, and you don’t need any exotics in order to deal with arsenic.”

La Granja in Peru. Image: First Quantum Minerals

Water and tailings

La Granja’s pit optimization was based on a copper-only cut-off using a $4.00 a pound copper price (versus today’s price of $6.65 per pound, or $14,450 a tonne). Silver, gold and molybdenum should provide by-product upside, which may well lure streaming companies.

Other challenges at La Granja (and most sites in the South American copper belt) include water and tailings management. Unlike many copper projects in the Andean belt, La Granja sits at a moderate elevation between 2,000m and 2,800m above sea level.

First Quantum plans to carry out comminution near the pit, then move material by pipeline through a 7 km access tunnel to a flatter, arid Pacific coastal plain about 100 km from the mine where processing and tailings management would be located.

First Quantum said primary water supply would come from desalinated seawater, with site contact water captured and reused in processing to reduce impacts on local environmental flows.

Next up for La Granja is permitting, and progressing baseline environmental and social studies and continuing community engagement – a process that would take several years under Peru’s strict Environmental and Social Impact Assessment (ESIA) regulations.

A prior Peruvian government estimate put La Granja’s required investment at more than $2.4 billion. First Quantum is also advancing its Haquira project in the Apurímac region of southern Peru.

Annual output over the first 10 years at Taca Taca, which has qualified under Argentina’s fast-tracking program, is pegged at 291,000 tonnes of copper and 133,000 oz. of gold at cash costs of 97¢ per pound. Production over the mine’s life is projected at 209,000 tonnes of copper and 96,000 oz. gold at cash costs of $1.26 per pound.

Appian deepens Namibia push with $400M copper mine buy

Appian Capital Advisory has acquired Omico Copper in a deal giving the mining-focused private equity firm a 95% stake in Namibia’s Omitiomire copper project as it expands its exposure to a metal expected to face surging demand growth.

The mining-focused private equity firm plans to spend more than $400 million to develop Omitiomire into a mine producing about 30,000 tonnes of copper annually over a 15-year mine life, with first production targeted within three years.

The project, about 140 km northeast of Windhoek in Namibia’s Otjozondjupa Region, is considered one of the country’s most advanced undeveloped copper assets. Appian did not disclose the acquisition price for the asset, which was sold by Guernsey-based private equity fund Greenstone Resources LP and Australian mining company International Base Metals Ltd.

“Omico Copper is a technically robust development opportunity that aligns with Appian’s investment philosophy,” CEO Michael Scherb said in a statement. “The project complements our portfolio, offering near-term production alongside long-term growth potential.”

Scherb told Bloomberg News the firm could announce two more copper acquisitions before year-end involving projects at similar stages of development in South America, North Africa and southeastern Europe.

Mining investors are increasingly targeting copper assets amid expectations supply will struggle to meet rising demand from electric vehicles, renewable energy systems, power grids and AI infrastructure. S&P Global forecasts copper demand will climb 50% to more than 42 million tonnes by 2040 from 28 million tonnes last year.

The metal, crucial to electrification, is once again trading near a record high above $14,000 a tonne as a squeeze on Middle Eastern sulfur supplies threatens some operations, compounding disruptions at major mines elsewhere around the world.

Building a copper pipeline

Appian’s latest acquisition also builds on a broader strategy to expand its mining portfolio across Africa and Latin America. In October 2025, the firm established a $1 billion partnership with the International Finance Corp., the World Bank’s private-sector arm, to support mining investments in the regions.

The fund has already backed the development of an underground operation at the Santa Rita nickel mine in Brazil and the expansion of Asante Gold Corp.’s mines in Ghana, Scherb said. Namibia remains one of several “tier-one jurisdictions” where Appian is actively seeking investments alongside Morocco, Ivory Coast, Botswana and Zambia

The firm’s current portfolio includes operations producing about 480,000 ounces of gold annually, along with 55,000 tonnes of zinc and 19,000 tonnes of nickel.

First Quantum has completed 370,000 metres of drilling at La Granja. Image: First Quantum Minerals.

First Quantum has completed 370,000 metres of drilling at La Granja. Image: First Quantum Minerals.

No comments:

Post a Comment