Trump courts Brazil in rare earth supply push

US President Donald Trump and his Brazilian counterpart Luiz Inácio Lula da Silva are forging an unlikely partnership around rare earths as Washington races to loosen China’s grip on critical mineral supply chains.

Their improvised White House meeting last week underscored how geopolitical competition over strategic minerals is reshaping alliances, with Brazil emerging as one of the few countries capable of helping the US diversify supply away from China.

Lula told Trump that Brazil’s vast rare-earth reserves are open to investment from any country willing to process minerals domestically, while Trump sought to signal renewed US engagement in Latin America ahead of a key China trip. The April agreement by Oklahoma-based USA Rare Earth to acquire Serra Verde Group for $2.8 billion highlighted the scale of the opportunity.

“The Lula-Trump meeting was less a bilateral reset than a bid to keep a politicised relationship manageable,” Mariano Machado, principal Americas analyst at Verisk Maplecroft, said in a note. “Among the items discussed, critical minerals emerged as the one topic where both leaders can claim a win without resolving deeper political tension.”

Reality-check

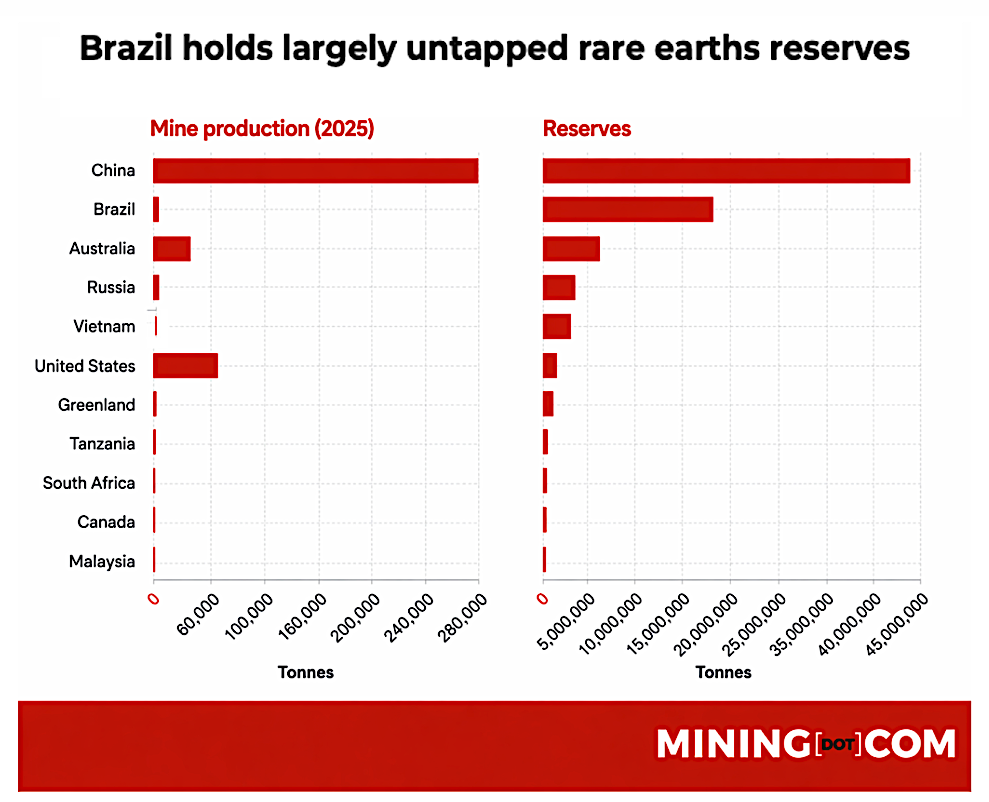

Yet Brazil’s long history with rare earths suggests the geopolitical enthusiasm may far exceed the industry’s near-term reality. Despite holding the world’s second-largest rare-earth reserves, the country has struggled for decades to turn geological potential into sustained production. Environmental licensing delays, bureaucratic hurdles, volatile commodity prices and periodic waves of resource nationalism have repeatedly stalled projects.

Mining companies can spend five to 10 years securing permits, while growing public opposition following deadly tailings dam disasters in Minas Gerais has hardened scrutiny of new developments.

The tensions expose a broader disconnect between global ambitions for critical minerals and local resistance to mining expansion. Rare earths are increasingly viewed as essential for semiconductors, AI infrastructure, electric vehicles and military technologies, but communities near prospective projects often see limited benefits and mounting environmental risks. Machado said the Serra Verde transaction illustrates both the opportunity and the constraints facing the two countries.

“The concrete test is Serra Verde in Goiás, Brazil’s only commercial-scale rare earths operation,” he said. “USA Rare Earth’s proposed $2.8 billion acquisition gives Washington a route into Brazilian production. But Lula’s message after meeting Trump was clear: Brazil has ‘no veto’ over US participation, yet also no intention to offer preferential access.”

Brazil’s Congress is advancing legislation that includes a $2 billion guarantee fund and $5 billion in tax credits to encourage domestic processing of critical minerals. Lula told Trump the country wants investment and technology transfer while ensuring more value-added processing remains domestic. Machado said that balancing act risks turning commercial development into a sovereignty debate that could slow approvals and delay investment.

“Critical minerals are not the simplest part of the bilateral agenda, even if they are the most practical,” he said. “Washington is going all-in on alternatives to China across rare earths, niobium, graphite, lithium, nickel and copper; while Brasília wants investment, technology transfer and domestic processing, without surrendering control over strategic resources.”

Second only to China

Brazil holds roughly 21 million tonnes of rare-earth reserves, second only to China and the Brazilian Mining Association projects $2.4 billion in rare-earth investment by 2030 as part of a broader $21.3 billion critical minerals pipeline.

But execution remains the central challenge. Licensing delays, land disputes, environmental scrutiny and limited processing capacity continue to cloud timelines for new developments.

“The risk for both sides is a development opportunity shifting into a de facto sovereignty debate, slowing approvals and dragging out business timelines,” Machado said. “This means Brazil can become a strategic rare earths supplier to the US — but not quickly nor on US terms alone.”

Race for critical minerals leaves EU struggling to keep up

For the European Union, the fate of a Cold War-era mine near Bratislava is becoming a litmus test for its ambition to break free from China’s chokehold over critical minerals.

Sitting in a wooded range of hills in Slovakia known as the Little Carpathians, the so-called Trojarova project is where Soviet engineers first discovered a rich seam of antimony in the 1980s. Its owners, Canada-based Military Metals Corp, are pitching the facility as a chance for Europe to secure access to an uncommon metal used in military equipment.

For crucial resources such as antimony, EU nations appear unable put up the money and act, leaving projects such as Trojarova open to being snapped up by rivals. So far, Military Metals hasn’t secured an offtake agreement from the bloc.

As US President Donald Trump prepares for summit talks in Beijing this week — and threatens to raise tariffs on Europe — the project serves to illustrate the dangers of getting left behind in a hotly contested race between superpowers.

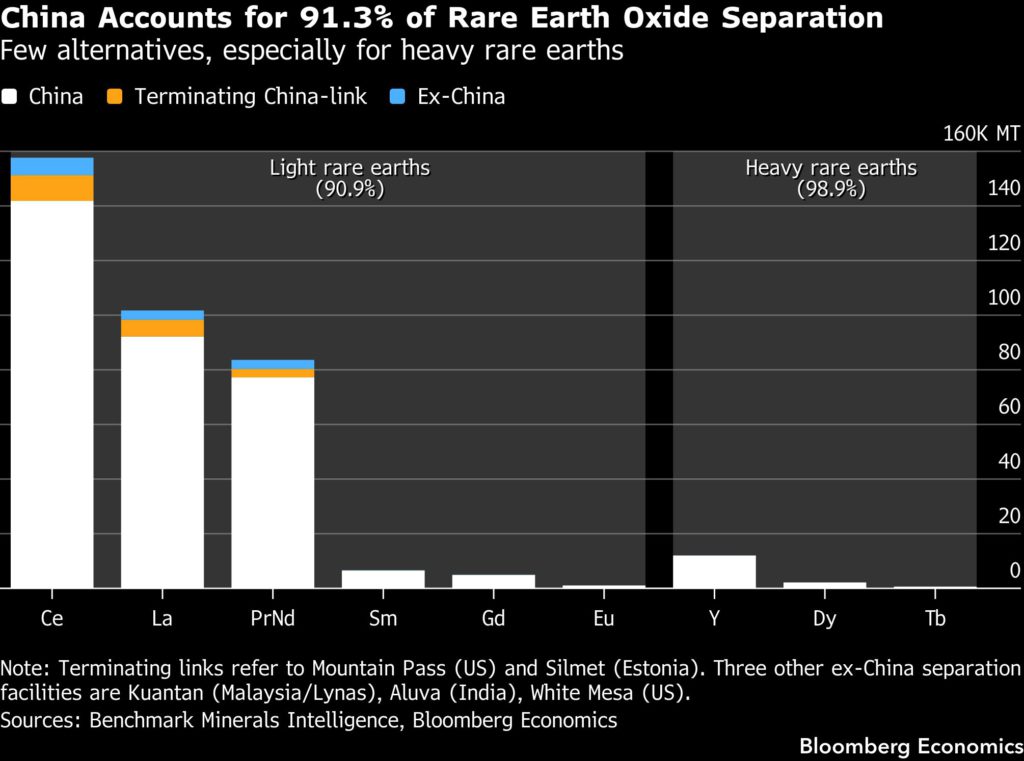

China imposed sweeping export controls on most critical minerals and rare earths last year. While the US has aggressively pursued partnerships with resource-rich nations and funded projects all over the world to catch up, Europe has lagged.

“Member states are still reluctant to pool resources for mining and processing projects beyond their borders, even as geoeconomic realities demand it,” said Sabrina Schulz, Germany director at the European Initiative for Energy Security. “Financing remains the central bottleneck.”

The bloc’s formal strategy was articulated in the European Critical Raw Materials Act of 2023, which set targets that included extracting at least 10% of annual consumption of key elements, and processing 40% of them. Those goals spurred action to identify vulnerabilities and to funnel investment to securing supplies of metals crucial for batteries such as lithium.

Global rivals have since pivoted toward resources with military uses such as antimony, gallium and germanium, but Europe has yet to follow suit. Brussels officials don’t have a mandate to pursue similar policies to the US, and lack money, people familiar with the internal deliberations said.

That leaves niche mining projects owned by thinly capitalized companies struggling to take off, not least because of the difficulty for them to raise finance in private markets.

With Europe, budgets are stretched, and many EU countries are unsure on how to engage. For example, in Germany there still isn’t consensus between the economy ministry, chancellery and foreign ministry of what exactly a de-risking strategy in critical minerals actually entails, the people said.

The result is an administrative impasse that leaves European officials worried about getting squeezed, with the feeling in Brussels and in capitals described as a fear of missing out.

Fretting about being left out of any deal Trump might cut with his Chinese counterpart Xi Jinping in their upcoming summit, the bloc last month reached an accord with the US to coordinate on policies to build secure critical minerals supply chains. For Military Metals, that’s a positive development that could result in joint US-EU investment and offtake partnerships for Trojarova.

Frank Hartmann, the official responsible for Asia at the German foreign ministry, told a March 24 event in Berlin that Europe is being too slow and operating on a “too limited scale.”

“What we have to do is long-term strategy, take money and funds into our hands to invest in these critical mineral funds for the next 10 years,” he said on a panel hosted by the German Council on Foreign Relations. “Otherwise, we never escape this dependency trap.”

The Trojarova project, acquired almost two years ago by Military Metals, epitomizes the challenge. The mineshaft there, protruding deep into the hillside, heads toward a murky gloom that seems endless, but a potentially bountiful opportunity might lurk within.

A shiny white metal that is often explored for alongside gold, antimony is largely found in China, Russia and Tajikistan. It’s essential for military applications such as munitions, night vision goggles and infrared sensors, which make up as much as 15% of demand. Other uses encompass fire retardants, and nuclear and renewable energy.

“Antimony is a textbook example of a small-volume mineral with outsized strategic impact,” said Schulz at the EIES. “Europe is almost entirely import-dependent, and supply is highly concentrated.”

She highlighted that China controls almost 80% of processing, pointing to another challenge. The Asian behemoth is pivotal not only as a source of such raw materials, but also as a refining hub. That’s one reason why Military Metals is pitching Trojarova’s riches to investors as a chance for Europe to catch up, with plans to produce ingots that can go direct to defense clients.

Alternatively, refining in Germany and Sweden could assist in smelting, meaning the facility could ultimately help establish an entire supply chain, from mining and processing, according to chief executive officer Scott Eldridge.

The mine, situated near the winemaking town of Pezinok in southwestern Slovakia, was first discovered and developed by the Soviets. When the Iron Curtain fell, the 1.7-km (1-mile) long excavation was abandoned, but it remained one of Europe’s most significant deposits of antimony.

Military Metals is too small a company to scale up the project on its own, and needs partners to invest and help develop an associated refining capacity. If reactivated, it could supply as much as a third of the continent’s annual demand, totaling about 6,000 tons, and be up and running in two or three years.

But the company — which has a market capitalization of less than $30 million — would need substantial funding.

Moreover, critical minerals are prone to wild price swings, and even in markets like lithium, several major projects have stalled as owners sought out government funding.

Whatever the merits of the company’s business case here, Europe’s money and resolve to secure such resources remain lacking. Germany’s own €1 billion ($1.2 billion) raw materials fund has only supported two projects so far and creates more hurdles for companies to qualify than it eliminates.

The EU Commission and member states have signed memorandums with producer countries — Spain agreed one with Brazil last month, for example — but US deals with the same countries are often bigger in funding terms and more ambitious on timelines for operationalizing the plans.

The Trump administration’s agreement with the EU reflects its push for so-called price floors, which guarantee minimum prices for producers that can’t be undercut by Beijing. European countries have been hesitant, but at some point might have little choice but to go along with the US-led initiative.

Meanwhile the region’s momentum to act has essentially taken a backseat to other more urgent crises. By contrast, despite the Trump administration’s recent focus on conflicts such as the Iran war, the president’s team of aides has been busy identifying mineral projects and bidding to secure them.

One American company has already approached Military Metals and asked to see the Trojarova project. Meanwhile just last month, the US government’s investment arm agreed on a $5 million deal to restart another dormant antimony mine in Northern Macedonia.

Thomas Hüser, the chairman of Military Metals, would like to prevent a similar outcome for Trojarova. The German native joined the company this year and was formerly a Glencore Plc manager.

“What we are still lacking is not ambition, but execution,” he said. “Europe’s raw materials strategy remains fragmented, slow, and often disconnected from industrial reality.”

(By Jenny Leonard and Jody Megson)

Japan’s Sojitz eyes Southeast Asia for new rare earths supply

Japanese trading house Sojitz Corp. is looking to Southeast Asia and other regions as new potential sources of rare earths outside Australia, as it aims to boost output and diversify its supply chain of the highly sought-after materials.

“Areas connected to southern China such as Laos, Cambodia and Vietnam will be potential regions that the company will look into,” chief financial officer Makoto Shibuya told Bloomberg News this week. The company will also consider India and other countries if suitable rare earths investment opportunities exist there, he added.

Rare earths are among the critical minerals used across high-tech manufacturing, including to build the powerful magnets used in electric vehicles, mobile phones and missile systems. China dominates the global supply chain for the materials, which has given it crucial leverage in trade and diplomatic negotiations, and countries including Japan are working to reduce their reliance on the Asian giant.

Sojitz, alongside Tokyo-backed energy agency Jogmec, has been in a joint venture with Australia-based Lynas Rare Earths Ltd. for more than a decade. They agreed in mid-March to start talks on mineral exploration and development of rare earth resources, including possible new mines “both in and outside Australia.” Sojitz has said its primary objective is to seek other sources besides Lynas’ major mining site at Mt. Weld in Western Australia.

As for its energy portfolio, Sojitz has no appetite either for a stake in the Alaska LNG project or to offtake volumes from the planned American venture as it’s simply too costly, Shibuya said. The proposed Alaska plant is backed by US President Donald Trump and often dismissed as fanciful by many in the industry.

Energy accounts for only around 10% of Sojitz’s total investments over the past decade and management has already been trimming that part of the business. Liquefied natural gas is one of its few remaining energy-related investments, but the company says it will only pursue projects that have been carefully scrutinized.

Japan’s government last year agreed with Washington to invest $550 billion in the United States, including possibly in the Alaska LNG project, in exchange for reducing tariffs on Japanese products to 15%.

(By Yusuke Maekawa and Koh Yoshida)

No comments:

Post a Comment