It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

Wednesday, May 27, 2026

Eramet partially restarts mineral sands production in Senegal after fire damages

Eramet Grande Côte extracts sand from the dunes located along the Atlantic coast. Credit: Eramet

French mining and metallurgic group Eramet on Wednesday said it had partially restarted production of heavy mineral concentrate at its plant in Senegal, as it seeks to mitigate a hit to its revenue from a fire that occurred in February.

The company said the affected plant now operates at around one-third of its nominal capacity. It aims to return to full production level by the first quarter of 2027, following reconstruction of damaged facilities.

Having paused its original mineral sands production target, Eramet now sees an output of between 300,000 and 400,000 metric tons of heavy mineral concentrate in 2026, versus 900,000 tons before the fire.

The company’s shares fell around 1.5% in early trading, pushing their year-to-date losses to 5.3%.

(By Mateusz Rabiega; Editing by Milla Nissi-Prussak)

P3 PUBLIC PENSIONS FUND PRIVATIZATION

AustralianSuper says possible Glencore listing on ASX would be positive

Pension fund AustralianSuper on Wednesday said if Glencore decides to list shares on the Australian Securities Exchange, it would be “positive” for both the bourse and the Swiss-based commodities trader and miner.

“If they were to list here we think it would be positive for Glencore and for the Australian stock exchange,” AustralianSuper portfolio manager Luke Smith said at the Australian Financial Review mining summit in Perth.\

The move would suit Glencore because “we believe the Australian share market is the best and most informed mining share market in the world,” Smith said, which would offer its shares a better chance to reflect the company’s worth. He added the fund had discussed the topic with Glencore and a listing on the ASX would offer more choice to investors such as itself.

Glencore and Rio Tinto earlier this year explored a possible merger that would have forged a $240 billion company, but Rio walked away saying it could not see sufficient cost advantages. There is speculation that Glencore is still interested in a tie-up.

Some mining CEOs like Glencore CEO Gary Nagle have argued that the industry needs to grow in size to become more relevant and influential – and to attract interest from a wider audience.

Smith said AustralianSuper was cautious about mining companies getting bigger because even if a large company emerged, “it’s still not going to be anywhere near the major tech companies.”

“We always approach cautiously, M&A, and if we can see it’s going to create value, we’ll be open-minded about it,” he said.

BlackRock portfolio manager Olivia Markham earlier said that she saw merit in “sensible” M&A as a way for miners to grow and attract generalist investors to fund large and complex projects.

“Australian Super has got a bit of a track record of sometimes saying yes and sometimes saying no, but it’s all about not looking just to this transaction and instant gratification of maybe a share price rise of 20% or 30%,” Smith said.

“We’re always looking for three to five years. What is the company’s … intrinsic worth in three to five years’ time? And is this appropriate price being paid today?”

(By Helen Clark; Editing by Christian Schmollinger and Thomas Derpinghaus)

BlackRock would back consolidation among large miners because it would open the sector to generalist investors at a scale that would make it easier to bring on large and complex projects needed for new supply, a portfolio manager said on Wednesday.

The mining industry has an issue around scale, especially compared to other sectors such as technology, said Olivia Markham, speaking at the Australian Financial Review (AFR) conference in Perth.

“When you speak to a US generalist investor, they want large, liquid equities to invest in. Bigger companies have better access to capital, they typically trade at a better multiple, and I think within the context of the mining sector, bigger companies have also got the teams and the people to go and build all these complex projects,” she said.

“We’ve had a wave of M&A, but I see merit in more,” she said.

Among major miners, Glencore and Rio Tinto explored a possible merger earlier this year that would have forged a $240 billion company and tied together Glencore’s marketing business and copper assets with Rio Tinto’s operational expertise.

Rio Tinto walked away saying it could not see sufficient cost advantages for the deal. However, there is speculation that Glencore CEO Gary Nagle is still interested in in the Anglo-Australian miner and may look to reopen talks if the Swiss miner’s share price continues to outpace Rio’s.

BlackRock holds stakes in both miners, as well as top global miner BHP.

Demand accelerating

Major investments in supply are needed as commodity demand speeds up, underpinned by trends including electrification, AI and defence spending, Markham said.

“Commodity demand is simply accelerating, and the commodity intensity of GDP growth continues to go up, and when you look at every exciting theme that’s going on in the market… it all leads back to mining,” she said.

“At the same time, you’ve got a supply side that is massively underinvested, so there’s just no immediate supply response…. we’re going to have to keep having commodity prices move up to incentivize more and more supply to come on line,” she said.

Markham also said that the closure of the Strait of Hormuz was driving a push towards energy independence that would support alternative energy sources. “We are going to be thinking much more about uranium,” she added.

BlackRock’s exposure to Australia has declined across the past five years as it has looked to invest in jurisdictions that have greater copper exposure and as Australia becomes less cost competitive with other countries since Covid, she added.

(By Helen Clark and Melanie Burton; Editing by Stephen Coates and Lincoln Feast)

Jung Jae Hyo, VP Hanwha Corporation (left); Mark Tory, President and CEO Defense Metals (centre); and Jeong Sung Kyun, VP Hanwha Ocean Co. Ltd. (right) (CNW Group/Defense Metals Corp.)

Defense Metals (TSXV: DEFN) has signed a memorandum of understanding (MOU) with Hanwha Ocean, a South Korea-based shipbuilding and marine engineering company, to explore the supply of rare earth elements.

Under the MOU, which is non-binding, the companies will evaluate a potential agreement where Defense Metals would sell rare earth materials from its Wicheeda project in British Columbia to Hanwha, supporting the company’s manufacturing and supply chain.

Hanwha is also considering an investment in Defense Metals, subject to due diligence and further negotiation.

“This MOU is an important step in advancing a made-in-Canada critical minerals supply chain supporting strategically important defence and maritime industries,” Defense Metals CEO Mark Tory said in a news release.

“Rare earth elements are increasingly recognized as foundational materials for next-generation defence technologies and advanced manufacturing,” he added.

A spokesperson for Hanwha said the company is looking to strengthen its ties to Canada’s critical minerals sector as the federal government moves to modernize its naval fleet.

The agreement comes as Hanwha competes for Canada’s multibillion‑dollar submarine program and follows other Canadian partnerships, including MOUs with the Automotive Parts Manufacturers’ Association and Algoma Steel.

Foreign ministers at this week’s meeting in New Delhi. Credit: Dr. S. Jaishankar | X

The Quad partner nations — United States, Japan, Australia and India — unveiled plans to invest $20 billion to further support the buildout of a reliable critical minerals supply chain in an effort to counter China’s dominance.

The Quad Critical Minerals Initiative announced on Tuesday sets out the framework for the nations to work together through economic policy tools and coordinated investment to accelerate the development of a secure supply chain of minerals powering advanced technology, defense systems, batteries and AI.

To support this initiative, the Quad partners intend to mobilize $20 billion in government and private-sector funding of the entire critical minerals supply chain, which includes mining, processing and recycling, the US Department of State said in a statement.

This, the Department said, would entail identifying projects with a so-called “Quad nexus” — those located in partner countries, operated by companies headquartered in Quad partner countries, or supplying Quad markets — that could fill gaps in the critical minerals supply chain.

The funding would involve various mechanism such as export credit agencies, development finance institutions, mobilization of private capital, or other public supporting tools, including guarantees, loans, equity participation, insurance, subsidies and offtake agreements.

Under the initiative, the Quad nations would share information on good practices and technical approaches to permitting, licensing and regulatory processes, cooperate on technology development and capacity building related to geological mapping and resource assessment, and consider coordinated measures to address non-market policies and unfair trade practices.

On the recycling front, the partners will also work together to improve the recovery and use of critical minerals from e-waste and other scrap materials.

The announcement came on the back of a meeting in New Delhi between the nations’ foreign ministers. In addition to the critical minerals initiative, the Quad partners also entered an Indo-Pacific energy security pact aimed at strengthening regional fuel and energy supply chains. Earlier that day, US and India also signed a framework agreement on critical minerals.

A warning to critical minerals buyers: avoid butter mountains, aluminum floods

Individual slings of La Carbonate, a secondary product produced at MP Materials. Photo by Michael Tessler, MP Materials

Western governments, currently ploughing tens of billions of dollars into critical minerals in an effort to break their reliance on China, could look to history to see how well-intentioned efforts to prop up commodity sectors can backfire.

As efforts to build stockpiles and combat China’s dominance gather pace, a dozen industry executives, investors and analysts interviewed by Reuters pointed to the risk of a repeat glut scenario.

“There needs to be some coordination between Western governments as they seek to incentivise new production,” said Brett Beatty, a partner at Resource Capital Funds, a mining-focused private equity firm that supplies the US government with niobium and tantalum via its holdings in Global Advanced Metals.

“The biggest risk is we all do our own thing,” Beatty added. “We all generate multiples of volumes the world needs and then you just crush everything, because you’ve got an oversupply.”

The US has allocated upwards of $20 billion to support its critical minerals sector across multiple programs and financing tools, including $10 billion for its stockpile, Project Vault. Australia has earmarked at least A$13 billion ($9.42 billion) to support critical minerals development across at least five programs including its own reserve.

Rare earths are a small piece of the $320 billion critical minerals market that the International Energy Agency expects to double by 2040. The rare earths sector that produces strong magnets used in defence technologies, advanced manufacturing and medical equipment was worth about $6.4 billion in 2024, according to IEA figures.

And yet the US, European Union, Australia and Japan have promised combined financial aid to rare earths projects globally that is already beyond that market value, Reuters calculations show.

Containing oversupply risks

In the 1980s and early 1990s, subsidies, cheap energy and price guarantees fuelled massive overproduction of European dairy – dubbed “butter mountains” – Russian aluminum “floods” and Australian wool, which flooded global markets, sent prices into a tailspin and spread pain far beyond national borders.

The wave of Western investment is already set to tip some rare earths, a group of 17 metallic elements, into surplus in the coming years, according to David Merriman of Project Blue, a consultancy. He added, however, that he did not expect large surpluses to develop because governments could temper support.

“Government-led stockpiles can stop purchasing, which can have a market-balancing impact and there is only limited capacity supported by price floors or guaranteed purchasing by governments at present,” he said.

For now, stockpiles do not present any risk of swamping markets, said Amanda Lacaze, the CEO of Lynas Rare Earths, the world’s top rare earths producer outside China, on May 6.

“I’m pretty alert to how much rare earths are sitting in stockpiles around the world right now and it’s not very much,” she said.

Australian Minister for Resources Madeleine King told Reuters earlier this year that the country’s support for its stockpile was “very different from the wool situation.”

“This is about a targeted, project-based investment to make something work, for creating secure supply chains for Australian manufacturing, but also for our neighbours and like-minded partners,” she said.

Some global coordination is afoot. The Group of Seven countries are in talks to create a permanent secretariat to make sure plans to increase critical mineral supplies survive beyond their rotating presidencies, five sources familiar with the discussions said earlier this month.

The DRC and Indonesia

Government intervention has yielded notable success for some, including the Democratic Republic of Congo (DRC), which has stockpiled cobalt and set export quotas to boost its mining revenue.

In the near term, the policy lifted global prices, helping to fill government coffers, but prolonged restrictions risk accelerating the shift to substitutes as buyers seek more reliable supplies, said Geraud-Christian Neema, the Africa editor at the China Global South Project, a non-profit focused on Beijing’s role in emerging economies.

Authorities now face a difficult balance: easing quotas could trigger export surges from players like China’s CMOC and erase gains, while keeping them tight risks a long-term erosion in demand, he said.

The DRC followed a path forged by Indonesia, which in 2020 banned nickel ore exports to encourage in-country processing and increase revenue from its resources.

Within three years, production trebled and it entrenched its position as the world’s dominant producer. But it has since cracked down on mining quotas to stem overproduction and falling prices – and last week, it unveiled a plan to centralize control of commodity exports.

One way to lower the risk of oversupply would be to add processing capacity at existing operations so that target metals are produced as byproducts, rather than following price signals, said Huw McKay, a visiting fellow at The Australian National University who previously served as BHP’s chief economist.

That model is underway in Western Australia with Alcoa and Japan’s Sojitz, which includes backing from the Japanese, Australian and US governments. They are adding a plant to extract gallium at Alcoa’s alumina operations near Perth. Trafigura has moved to extract antimony from its Nyrstar lead smelter in South Australia.

Given the capex of large miners, McKay said Western government investments were “more like seed funding.”

($1 = 1.3795 Australian dollars)

(By Melanie Burton, Maxwell Adombila and Fransiska Nangoy; Editing by Veronica Brown, Praveen Menon and Thomas Derpinghaus)

MP Materials accuses USA Rare Earth of magnet tech theft

An aerial view of MP Materials’ Mountain Pass rare earths mine photographed in 2022. Credit: MP Materials.

MP Materials (NYSE: MP) has filed a lawsuit against USA Rare Earth (NASDAQ: USAR) alleging that its rare earth mining rival stole its proprietary magnet technology through an ex-employee, Bloomberg reported.

According to the lawsuit filed in a Texas court last Friday and seen by Bloomberg, MP said one of its former employees had shared “grain boundary diffusion” formulations with USAR, which later disclosed the information to a third-party technology company.

“USA Rare Earth has exhibited a pattern of recruiting employees from other companies and then using those employees to misappropriate trade secrets to accelerate USA Rare Earth’s own development,” MP alleged in the suit.

The Las Vegas, Nevada-based miner also claimed USAR had failed on multiple operational milestones and questioned the validity of the mineral resources being touted at the latter’s flagship Round Top deposit in Texas.

In an emailed response to MINING.COM, USAR said MP Materials’ complaint “has misrepresented our company, our culture, and our people,” adding that the company will defend against those accusations and respond “appropriately”.

Shares of USA Rare Earth fell over 3% during the early hours of trading, sending its market capitalization below $6 billion. MP Materials also fell 3%, trading at a market capitalization of $11.6 billion.

Key US rare earth players

MP — the only producer of rare earths in the US — has developed its own technology to turn the extracted minerals from its Mountain Pass mine in California into permanent magnets used in electric vehicles, defense systems and advanced electronics.

USAR is also looking to follow the same path by developing its Texas deposit, which it calls “the largest heavy rare earth deposit” in the US, and has already commissioned a magnet manufacturing facility in Stillwater, Oklahoma. It also has ambitions to expand abroad through building another plant in France and recently announced a $2.8 billion acquisition of Serra Verde Group, which owns Brazil’s only rare earth mine.

Both companies are seen as key players in the US government’s plans to establish a domestic rare earth supply chain to reduce its dependence on economic rival China. To facilitate this strategy, the Trump administration has made large financial commitments to both, including a $400 million equity investment in MP in July, followed up by a $1.6 billion agreement with USAR this year.

MP’s lawsuit places USAR under further scrutiny, as the latter’s deal with the White House had already received pushback from lawmakers, while the Serra Verde deal remains under review. USAR, however, has said it is not concerned by questions surrounding the government’s investment.

“At USA Rare Earth, we are focused on the real challenge: China’s dominance of the rare earth supply chain. The American people, our allies and investors are counting on us–all of us in this industry–to deliver a secure Western, rare earth value chain to protect our national and economic security,” USAR said in its statement to MINING.COM.

Ionic Rare Earths, AML ink MoU for US permanent magnet supply

Ionic Rare Earths (ASX: IXR) has signed binding sales agreements with Florida-based Advanced Magnet Lab to supply magnet rare earth oxides, specifically neodymium/praseodymium oxide and dysprosium oxide, under AML’s recently awarded US Defense Logistics Agency (DLA) contract for domestically produced high-grade sintered NdFeB permanent magnets for defence applications.

Both companies have signed a non-binding Memorandum of Understanding (MOU) for the collaboration on both the supply of magnet REOs and recycling of swarf and pre-consumer waste.

The news is a step forward in IonicRE’s strategy to establish secure, sovereign, and sustainable rare earth supply chains across the US and Europe, while expanding the company’s global refining and magnet recycling footprint, it said.

The partnership has the potential to support increasing requirements from the U.S. Department of War (DoW) linked to the ramp up of domestically manufactured military drone motors and other critical defence equipment requiring secure, traceable, and domestically sourced rare earth permanent magnets, amid increasing geopolitical instability, the companies said.

Under the program, IonicRE will provide critical rare earth oxide feedstock to support AML’s PM-Wire manufacturing platform, designed to enable scalable, traceable, and high performance permanent magnet production in the United States.

AML’s DLA-supported initiative includes alloy optimisation, advanced manufacturing development, and integrated supply chain collaboration across Western-aligned partners.

“IonicRE’s patented, made-in-Belfast magnet recycling technology offers an innovative solution for the supply of magnet REOs, and working with several Western magnet manufacturers, and now AML, we are building an integrated, ex-China rare earth supply chain across the Western world and beyond,” IonicRE CEO Tim Harrison said in a news release.

AML president Wade Senti added that the partnership will help ‘close the loop’ on supply for critical inputs to the US industrial base.

Defence-driven demand powers surge in US listings by mining firms

The Pentagon, headquarters of the US Department of Defense. Credit: Wikipedia under public domain licence

There has been a surge in mining companies seeking US listings this year, but even more striking is the change in language as firms explicitly target defence-related demand for critical minerals.

At least 18 companies, mostly Canadian and Australian but also some US startups, have completed or are pursuing dual US listings this year, versus just three in 2025, according to exchange filings and company disclosures reviewed by Reuters.

They span in value from about $25 million to $7.5 billion and mark a shift in how critical mineral producers seek access to capital markets as listings explicitly pitch for defence end-use applications.

Defence focus

This year’s transactions have brought producers of antimony, rare earths, tungsten and uranium to the NYSE and Nasdaq – all minerals designated strategic by the Pentagon and used in fighter jets, missiles and radar systems.

The firms are positioning themselves as suppliers of munitions, armour-piercing materials and of inputs for US weapons systems, their public filings show, departing from traditional mining IPO language focused on supply-demand fundamentals and long-term price cycles.

“Our goal is to cover direct defence demand for tungsten,” Guardian Metal Resources , CEO Oliver Friesen told Reuters, estimating US military annual demand at 2,000 to 3,000 metric tons.

Guardian aims to help the US rebuild its domestic tungsten supply chain, citing uses in armour-piercing ammunition. It has received $6.2 million from the Pentagon and has applied for additional funding from the US military that would be worth at least $100 million, Reuters reported in March.

United States Antimony secured a $245 million Defense Logistics Agency contract to supply antimony for the defence stockpile, where the metal is used in munitions and other military applications.

Rare earth developers are also emphasising defence uses. REalloy Inc said its project contains dysprosium and terbium used in magnets for advanced weapons systems, while Rare Earth Americas, backed by Australia’s Gina Rinehart, partly focused its IPO on “defence applications”.

Most companies have raised modest sums so far. Guardian secured $68.3 million, Rare Earth Americas $63.3 million, and Atlas Critical Minerals about $11 million, according to filings.

But several have secured government funding through Pentagon-linked programs, suggesting the listings are as much about unlocking strategic financing and investor access as upfront capital raising, analysts and lawyers said.

Company

US Listing

Previous / Concurrent

Date

Atlas Critical Minerals

Nasdaq: ATCX

OTCQB (Jupiter Gold)

Jan. 13

Blue Moon Metals

Nasdaq: BMM

TSXV, Frankfurt, OTCQX

Jan. 26

Santacruz Silver

Nasdaq

TSX-V

Jan. 21

Mayfair Gold

NYSE American/ NYSE

TSX-V → TSX

Jan. 27

Aris Mining

NYSE: ARMN

TSX

Feb. 19

Versamet Royalties

Nasdaq

TSXV / private precursor

Mar. 6

Highlander Silver

NYSE American: HSLV

CSE / TSXV

Mar. 11

U.S. Antimony Corp

NYSE (uplist)

NYSE American

Mar. 11

Guardian Metal Resources

NYSE American

LSE

Mar. 20

OceanaGold

NYSE: OGC

TSX, ASX

Apr. 7

The Metals Royalty

Nasdaq: TMCR

TSX-V

Apr. 8

Nicola Mining

Nasdaq ADSs: NICM

TSX-V

Apr. 13

Compiled by Clara Denina

Equity stakes, project funding

Some Canadian-listed miners, including Lithium Americas and Trilogy Metals, are tapping US defence-linked financing through equity stakes and project funding as part of Washington’s push to secure key minerals.

That push follows a series of crises that left the United States and other Western nations racing to rebuild domestic mineral supply chains and reduce their dependence on China’s dominant production and processing.

China imposed export controls on antimony in August 2024, tightening global supply of a mineral used in military equipment and raising concerns about US defence supply chains.

By December 2025, the US military had begun testing small-scale refineries for critical minerals, shifting from funding projects to building processing capacity itself.

A 2025 Chinese export ban on tungsten has limited feedstock for US refineries built in the 1950s for filament light bulbs, which have production capacity of about 18,000 tons but are operating significantly below that, Guardian’s Friesen said.

In November 2025, China issued a one-year suspension of its export ban on antimony, gallium, germanium, and super-hard materials to the US, but kept restrictions on military users, easing commercial supply but leaving the Pentagon reliant on domestic sources.

In addition to China’s export curbs, Washington has faced restrictions on cobalt exports from the Democratic Republic of Congo and other risks.

Company

US Plan

Resolution Minerals

Nasdaq

Am. Rare Earths

Nasdaq H2’26

Sunshine Silver

NYSE (SSMR)

McEwen Copper

IPO Q4’26

Jindalee / USE

Nasdaq SPAC H2’26

Barrick / NA Barrick

NYSE/TSX vehicle

Compiled by Clara Denina

Capital follows policy

Private capital has also responded. JPMorgan, for example, said in October it could invest up to $10 billion in sectors tied to national economic security, including critical minerals.

In February, US President Donald Trump launched “Project Vault”, a $12 billion strategic minerals stockpile initiative backed largely by the US Export-Import Bank.

Investors say US government equity offers more than capital, giving companies access to defence-linked contracts, subsidies and policy backing, and helping protect them from price cyclicality.

Still, caution remains.

“There’s absolutely a lot of money going into defence-driven exploration, but a lot of it is also very speculative right now,” said Rick Werner, co-chair of the capital markets and securities practice at law firm Haynes Boone.

“As long as you can gain access to the mines and the resources, I don’t see why they can’t break China’s chokehold over it,” Werner said, “but it’ll take time and money.”

($1 = 1.3754 Canadian dollars)

(By Clara Denina and Ernest Scheyder; Editing by Veronica Brown and Jason Neely)

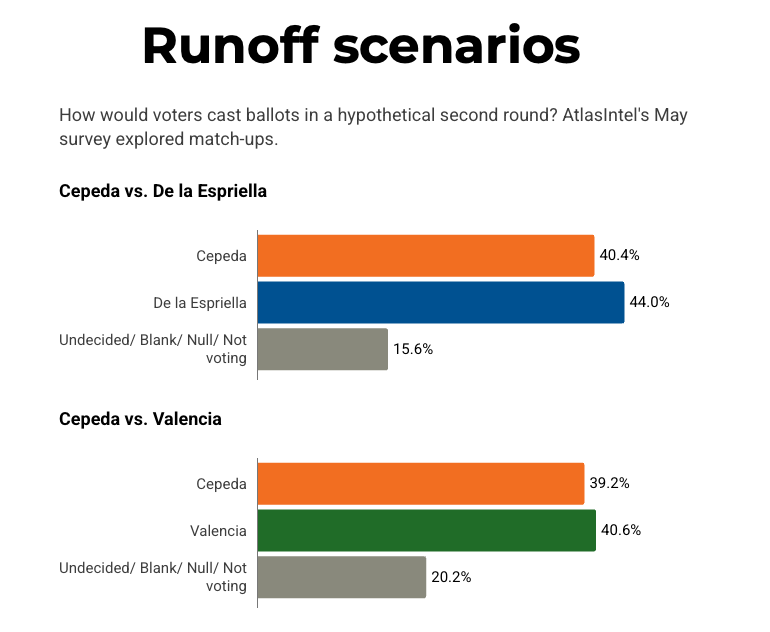

Colombia election outcome could reshape copper investment

Colombia’s presidential election this weekend could determine whether one of Latin America’s most underexplored copper frontiers attracts billions in mining investment or sinks deeper into regulatory uncertainty and security turmoil.

The May 31 vote has become a referendum on President Gustavo Petro’s leftist agenda after four years of environmental reforms, tax increases and worsening security conditions that rattled investors across Colombia’s mining and energy sectors.

Senator Iván Cepeda, the candidate aligned with Petro’s Historic Pact coalition, is campaigning to continue the government’s “Total Peace” strategy and energy transition policies, while conservative rivals Paloma Valencia and Abelardo de la Espriella promise deregulation, tougher security measures and stronger support for private investment.

Investors also fear Cepeda, the son of a slain communist leader, could deepen state intervention in the economy, loosen fiscal discipline and weaken the independence of Colombia’s inflation-targeting central bank system.

Cepeda has attempted to reassure markets by presenting himself as less confrontational than Petro and more open to negotiation with the hydrocarbons sector. Allies say he supports a slower energy transition that avoids forcing Colombia to depend on imported fuel, though investors remain uneasy about his support for greater state involvement in the economy and criticism of the central bank’s monetary tightening policies.

Recent polling suggests Cepeda holds a narrow lead ahead of Sunday’s vote, though few observers expect any candidate to win outright and avoid a June runoff. Valencia and de la Espriella have framed the election as a battle to restore investor confidence, revive Colombia’s pro-business tradition and reverse what they describe as institutional and economic decline under Petro’s administration.

Copper push

Mining executives and analysts say the outcome could shape the future of Colombia’s copper ambitions at a time when countries worldwide are racing to secure critical minerals needed for electrification and renewable energy infrastructure.

Colombia has launched tenders for 14 strategic copper regions and updated its list of priority minerals, but investors remain wary after reforms expanded environmental restrictions, increased taxes and created uncertainty over permitting and concession rules.

“From an investor standpoint, the key is not only who wins, but whether the next president can build a governing coalition that delivers regulatory stability,” Juan Ignacio Guzman, head of mineral consulting firm GEM, said. “Copper is a multi-decade investment that is extremely sensitive to timeline uncertainty.”

The broader industry has struggled under mounting pressure. Mining contracted more than 6% last year as higher taxes, declining exploration and insecurity in mineral-rich regions weighed on activity. Coal exports dropped 20% in 2025, gold exports fell 18% and investor confidence weakened after the government proposed a new mining law that would create a state-owned mining company, EcoMinerales, and restrict large-scale mining in environmentally sensitive areas.

Some investment decisions in mining and energy remain frozen until after the election, according to business leaders, while S&P Global Ratings last month downgraded Colombia to BB- the country’s lowest-ever credit rating, after Petro suspended fiscal rules limiting government debt growth.

Analysts say investors are increasingly focused on whether a new government would restore regulatory predictability and fiscal discipline.

“From the market perspective, the two main concerns associated with Cepeda are lack of commitment with fiscal consolidation and central bank independence,” Alejandro Arreaza, an economist at Barclays, said in a note.

Petro’s appointees to Colombia’s central bank have increasingly questioned the country’s 3% inflation target and opposed aggressive rate increases, raising fears among bondholders and investors about political pressure on monetary policy.

Gold + violence

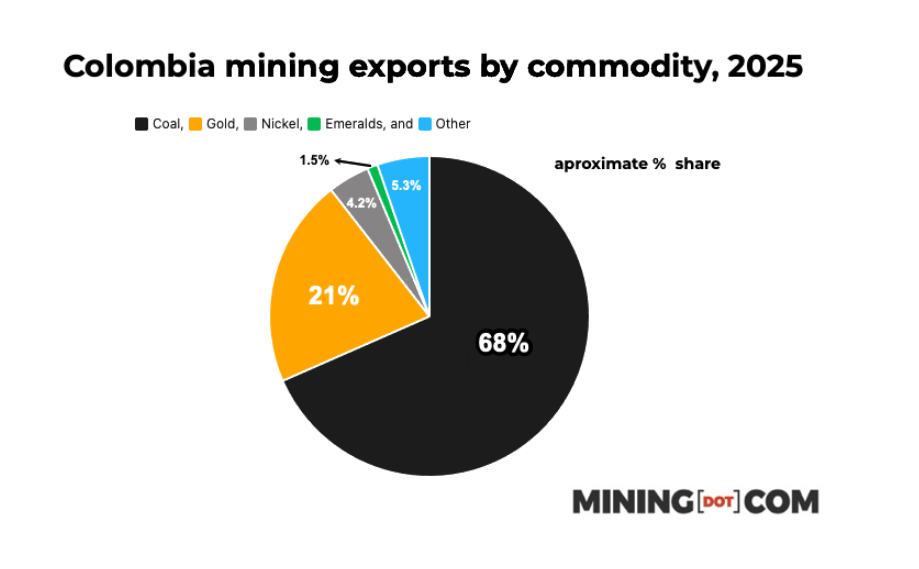

The stakes extend far beyond politics. Colombia holds significant deposits of coal, gold, nickel and prospective copper resources along the Andean metallogenic belt, yet the country remains a marginal copper producer compared with Chile and Peru. AngloGold Ashanti’s (JSE: ANG)(NYSE: AU)(ASX: AGG) Quebradona project, Cordoba Minerals’ (TSX-V: CDB) Alacrán development and Libero Copper’s (TSX-V: CGNT) Mocoa project form part of a growing pipeline that could eventually transform Colombia into a meaningful supplier of critical minerals.

Companies including Glencore (LON: GLEN), Rio Tinto (ASX, LON: RIO) and AngloGold Ashanti have long viewed Colombia as a high-potential jurisdiction, though projects often face years of delays tied to permitting disputes, environmental opposition and regional insecurity.

Security has also emerged as a defining issue in both the election and the mining sector. Violence linked to illegal gold extraction and organized crime has spread across rural Colombia, particularly in regions where dissident guerrilla factions and narcotics traffickers control mining supply chains. Analysts say Petro’s “Total Peace” negotiations have failed to contain armed groups, allowing illegal mining networks to expand.

Coal remains Colombia’s top mining export. (Sources: USGS, Asociación Colombiana de Minería, ColombiaOne.)

“The failure of President Gustavo Petro’s ‘Total Peace’ policy means that violence will continue to be a concern for the mining sector under any future administration,” Robert Munks, head of Americas at Verisk Maplecroft, said. “Illegal mining now accounts for roughly three-quarters of Colombia’s gold exports.”

Illegal mining has become one of the country’s most lucrative criminal businesses as soaring bullion prices fuel what analysts describe as a “narco-mining” economy.

Across parts of the Amazon basin and Colombia’s Pacific regions, armed groups use illegal gold operations to finance weapons purchases, territorial expansion and recruitment, according to analysts and security researchers. Former FARC dissidents and criminal organizations have increasingly shifted into mining as a stable source of cash flow, particularly in remote regions where state control remains weak.

The illicit trade is also reshaping Colombia’s relationship with global markets. The country exported about $4.1 billion in gold in 2024, with roughly $1.5 billion shipped to the US, according to UN trade data. Researchers warn that illegal production is becoming deeply embedded in international supply chains as criminal groups blend illicit gold with legal exports.

Investor gamble

For mining investors, the election may ultimately hinge less on ideology than predictability. The financial community and mining executives say billions in potential spending on copper, gold and energy projects remain sidelined until Colombia’s political direction becomes clearer.

Companies are closely watching whether the next government streamlines permitting, eases licensing bottlenecks and restores confidence in fiscal stability after years of policy volatility under Petro’s administration.

If the next administration can stabilize regulations, strengthen security and create clearer permitting timelines, analysts say Colombia could emerge as a strategic supplier of copper and other critical minerals as global demand accelerates. Failure to do so risks leaving one of the region’s richest untapped mining jurisdictions trapped in political and regulatory paralysis.