It’s possible that I shall make an ass of myself. But in that case one can always get out of it with a little dialectic. I have, of course, so worded my proposition as to be right either way (K.Marx, Letter to F.Engels on the Indian Mutiny)

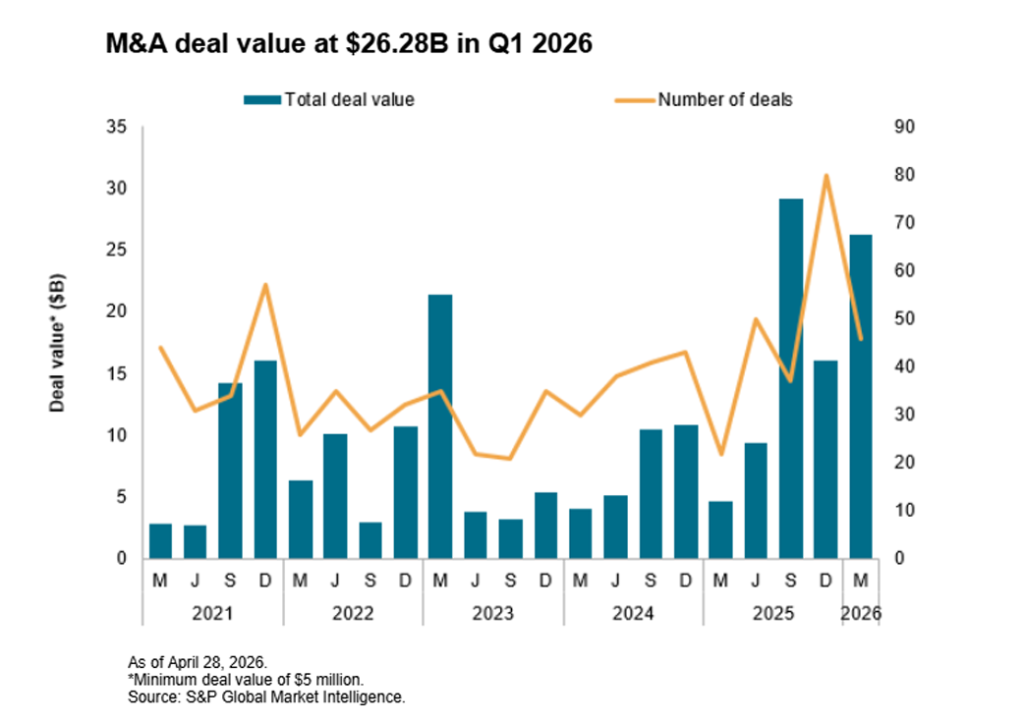

The mining industry saw mixed mergers and acquisitions (M&A) activity in the first quarter of 2026, with a surge in deal value but a sizeable decrease in the number of transactions, according to S&P Global.

In its latest M&A trends report, the firm highlighted a strong resurgence in deals involving companies in the metals and mining sector during the January-March period, with the combined value of transactions rising 63% over the previous quarter.

At $26.28 billion, the total value of deals represents the second highest ever for a quarter since it began tracking the data in late 2013, S&P said, pointing to the industry’s strategic focus on securing long-term supply.

It also noted that companies in the mining sector are now seeking immediate scale, which explains the surge in corporate-level deals as opposed to asset acquisitions. In total, there were 30 company acquisitions recorded by S&P during the quarter, nearly double the number of asset purchases (16).

However, the report came with a caveat, as Q1 2026 was the first quarter that the firm included steel deals in its coverage. As such, the $10 billion acquisition of BlueScope Steel — the largest of the quarter — likely overstated the increased value of M&A deals compared to past years.

This was also evident in the number of M&A deals, which at 46 was nearly half of the December quarter totals.

Focus on copper-gold remains

Aside from the steel deal, the second and third largest deals centered on gold and copper respectively, an indication of the strong appetite for the two hottest commodities, S&P said. Several large players, including South Africa’s Gold Fields and China’s Zhaojin Mining, have indicated they are open to deals.

As for individual asset buys, the combined value ($3.35 billion) was well above the quarterly average, buoyed by the $1 billion sale of the Copler mine in Turkey, though it was 12% lower than the previous quarter. But compared to the same period last year, the value of asset purchases was a significant 221% higher.

Brazil rare earth ambitions clash with strained mining regulator

Brazil’s aim to become a leader in rare earths mining is running head-on into budget cuts and staffing shortages at the sector’s regulatory agency.

The Latin American nation is pursuing partnerships with other countries on critical minerals and rare earths, yet its National Mining Agency, or ANM, lacks the resources to keep up with inspections and meet international commitments, said director-general Mauro Sousa.

“It’s a contradiction at the heart of the Brazilian state,” Sousa told reporters Tuesday at an industry conference organized by mining group Ibram in Brasília.

Outside of China, Brazil has the world’s largest reserves of critical minerals. Brazil’s government recently cut funding for agencies including ANM, which oversees more than 255,000 active mining claims, inspects mining structures and handles permits for new projects.

The cuts also are affecting review of structures for mine waste materials called tailings dams in a country still marked by two major disasters at operations owned by Vale SA. The regulator’s workforce is less than half the level needed, and only four employees are dedicated to critical minerals, Sousa said.

Still, ANM is facing a boom in rare earth exploration applications — ones it will likely struggle to process. Since 2023, the agency has received 3,038 requests, compared with 745 filed between 1975 and 2022.

Front: Stephane Piat, SVP – Global Supply Chain Strategy & Performance, Schneider Electric and Maryse Belanger, Torngat Metals president. Back: Sébastien Martin, French Minister Delegate for Industry French and Isabella CHAN, Senior Assistant Deputy Minister, Natural Resources Canada. Supplied image.

Schneider Electric and Torngat Metals announced Wednesday they signed a non-binding Memorandum of Understanding (MOU) to explore a strategic industrial partnership to support the development of a resilient rare earth value chain in Canada.

The partnership is anchored in the development of the Strange Lake rare earth project in Nunavik, with associated infrastructure in Labrador and a planned separation facility in Sept-Îles, Quebec.

The Strange Lake project is expected to produce both heavy and light rare earth elements essential to permanent magnets used in renewable energy, digital infrastructure, and advanced manufacturing.

The MoU is designed to support an integrated, end-to-end collaboration, connecting upstream resource development, technology integration, and future industrial demand, the companies said.

It is intended to support the development of a 360° partnership, to support the development of a next-generation mining and processing project, leveraging Schneider’s expertise in electrification, automation, digital systems and sustainable industrial design.

Strange Lake stands out among North American rare earth projects for its heavy rare earth content, particularly dysprosium and terbium—elements critical to permanent magnets used in electric vehicles, wind turbines and defence technologies.

An initial study by Quest Rare Minerals pegged indicated resources at Strange Lake’s main B-zone deposit at 278.1 million tonnes at 0.93% total rare earth oxides (TREO); 1.92% zirconium oxide and 0.18% niobium pentoxide. Inferred resources were 214.4 million tonnes of 0.85% TREO, 1.71% zirconium oxide and 0.14% niobium pentoxide.

The future collaboration represents a concrete step toward a trusted, end-to-end critical minerals value chain, the companies said.

“This partnership reflects a clear reality: the energy transition depends not only on technology, but on secure and responsible access to critical materials,” Schneider Electric Canada VP Sustainability Frederick Morency said in a news release.

“With Torngat Metals, we are aiming for a fully integrated approach, from resource to industrial use, that strengthens both project development and long-term supply resilience.”

The MOU was signed in Paris on the margins of the meeting on financing critical minerals supply chains in G7 and like-minded countries. The announcement was made in the presence of Sébastien Martin, French Minister Delegate for Industry, and Isabella Chan, Senior Assistant Deputy Minister at Natural Resources Canada and Canada’s Special Envoy for the Critical Minerals Production Alliance.

“Strange Lake is designed to become a key player in building a resilient and responsible rare earth supply chain,” Torngat Metals, interim CEO Maryse Bélanger said.

“Working with Schneider Electric will enable us to integrate world-class industrial technology designed with sustainability in mind in our future operations, while connecting our project to real downstream demand. This is an opportunity to build not just a mine, but a complete, future-ready value chain.”

MP Materials owns and operates Mountain Pass, the only rare earths mine in the US. Credit: MP Materials

MP Materials’ (NYSE: MP) chief operating officer Michael Rosenthal has added to his stake in the company amid overall weakness in the critical minerals mining sector.

In a securities filing dated June 10, Rosenthal, through his family trust, purchased an additional 10,000 shares at a price of $54.30 per share.

According to the SEC disclosure, Rosenthal now has 136,622 shares in MP Materials. For comparison, CEO James Litinsky holds about 11.8 million shares.

The stock closed at about $53 apiece on the day of the insider buy disclosure, for a market capitalization of $9.5 billion.

Since hitting an all-time high of $100.25 in October, MP Materials’ share price and market value have essentially halved.

However, compared to a year ago, the stock price has nearly doubled, owing to increased investor interest in the critical minerals sector, with MP Materials seen as a leading player for its status as the only rare earth miner in the US.

The company’s share price saw a significant jump last July after it announced a public-private partnership with the Department of Defense, which included a landmark $400 million equity investment.

US business group says some critical minerals are ‘nearly unobtainable’ from China

US access to critical minerals from China remains difficult due to export controls and licensing delays, a US business lobby said on Wednesday, with Beijing’s restrictions driving three-quarters of impacted companies to search for new supplies.

Introduced in April 2025 in retaliation for US President Donald Trump’s tariffs, Beijing’s controls tightly restrict exports of certain rare earths crucial for advanced manufacturing.

That’s despite Trump’s deal with China’s Xi Jinping in October in which the White House said China committed to “effectively eliminate” all current and proposed critical mineral export controls.

The US-China Business Council said in a report that some rare earth elements remain “nearly unobtainable.”

“Despite some progress, confidence in longer term access remains low,” USCBC said based on results of its annual member survey conducted in February and March.

According to its survey, of 38 impacted companies, 29% said they were actively shifting to non-Chinese suppliers of critical minerals while 47% said they were searching for but had not yet found viable alternatives to China.

“China is forcing this diversification away from China and creating a strong interest on the part of the corporate sector to find alternatives,” USCBC president Sean Stein told Reuters.

China’s dominance over critical minerals has brought the rival countries to at least a temporary trade war truce, but the Trump administration has made a concerted push to revive mineral supply chains from the US and partner countries.

Stein said it would be difficult for the US, despite those efforts, to eliminate supply issues over the next three years.

Samarium cobalt magnets, important for high-temperature aerospace and defense applications, and yttrium and cadmium were among minerals that were still very difficult for US companies to access, Stein said.

Kyle Sullivan, USCBC vice president, said securing finished rare earth magnets – not just the minerals themselves – was a challenge due to China’s hold over both mining and processing.

“That’s the perfect case for congressional involvement, because it can’t be solved by the Trump administration alone,” Stein said.

Uncertainty in US-China relations is suppressing companies’ investments in China, Stein added, with the report noting that “just half” (49%) of 134 companies plan to invest in China this year.

“China’s business environment for foreign companies is not improving. The country’s support for domestic companies, including through industrial policy and preferential treatment in government procurement, is eroding the gains from formal market access openings,” the USCBC report said.

Sierra Gorda mine in Chile has become one of the main engines of KGHM’s profit growth.(Image courtesy of KGHM.)

Chile’s Sierra Gorda mine and BHP’s (ASX: BHP) Spence operation have agreed to explore collaboration opportunities aimed at lowering costs, improving efficiency and strengthening the long-term competitiveness of two of the country’s largest copper mines.

The companies signed a memorandum of understanding to evaluate commercial and technical cooperation in Chile’s Sierra Gorda district, where both mines face declining ore grades, operational challenges and lower output. Areas under review include supply chains and operating processes that could generate economies of scale and improve sustainability.

“This approach allows us to identify opportunities that will contribute to long-term sustainable results for our company, but also to consolidate our relationship with the region by working collaboratively in the area,” Dee Lingenfelder, President of BHP’s Pampa Norte, which includes the Spence and Cerro Colorado operations, said.

“This agreement allows us to move forward in evaluating initiatives that can generate efficiencies in specific areas,” Marcelo Bustos, CEO of Sierra Gorda SCM said. “We are convinced that low-grade mining is viable and profitable, and to further develop it, more dialogue and collaboration are required, just as we are doing.”

The agreement reflects a broader trend across the mining industry as producers seek new ways to maintain margins and support investment while confronting lower-grade deposits and rising operational complexity. Shared infrastructure and coordinated development can reduce capital requirements while improving project economics.

Production gains

Both operations reported lower copper production in the first quarter of 2026 compared with a year earlier and are advancing projects designed to improve performance.

BHP is progressing a $600 million concentrator expansion at Spence, which remains in the design, prefeasibility and engineering stages. The project would add a new flotation circuit to address ore variability that has reduced recovery rates. BHP said it could make a final investment decision in the first half of fiscal 2027. Spence produced 254,795 tonnes of fine copper in 2025.

Sierra Gorda is advancing plans to process oxide ore currently stockpiled for future heap-leach operations. The proposed SX-EW project would produce about 30,000 tonnes of copper cathodes annually over a 10-year mine life.

The operation is also upgrading its tailings storage facility through a $400 million brownfield project and evaluating a roughly $700 million expansion of its fourth grinding line.

Sierra Gorda is owned by KGHM International (55%) and South32 (45%), while BHP owns Spence outright.

Column: Nickel’s recovery hopes tempered by growing stock overhang

A haul dump trucks used to transport mining material in the nickel mining of PT Vale Indonesia in Sorowako. Stock image.

(The opinions expressed here are those of Andy Home, a columnist for Reuters.)

Nickel’s early-year rally is a collective bet that Indonesia’s multi-year production surge is finally abating, allowing the market to rebalance after four consecutive years of oversupply.

But a growing mountain of surplus metal accumulating in London Metal Exchange (LME) and Shanghai Futures Exchange (ShFE) warehouses is a reminder that this could be a slow-fuse process.

Combined exchange inventory stands at 468,600 metric tons, the largest stock overhang since 2015 and equivalent to around six weeks of global usage.

The rate of growth has slowed as LME-registered stocks plateau out. But the rise in Shanghai inventory has been simultaneously accelerating, suggesting the refined nickel surplus is now migrating eastwards.

LME and ShFE nickel stocks

Production hits in the West

LME nickel stocks, including off-warrant inventory, rose for nine straight months between June last year and March, when they topped out just below the 400,000-metric-ton level.

They have since edged 20,000 tons lower. Although metal is still arriving at LME warehouses in sizeable clips, warrant cancellations and load-out rates have also picked up in recent weeks, signalling a stronger draw on metal from the physical market.

The Western supply chain, or what’s left of it after Indonesia’s Chinese-backed supply tsunami, is absorbing two unexpected hits to production.

The mine, which is being taken over by a consortium led by Jason Kluk, former head of nickel trading at Glencore, produced 28,000 tons of finished nickel products in 2024.

Just as Ambatovy is due to return at the end of this month, Sherritt International’s Fort Saskatchewan refinery may run out of feed.

The mines are integrated with Sherritt’s nickel plant in Alberta and the company warned last month it expected its raw materials inventory to last only to the middle of June.

Sherritt expected to produce 26,000-28,000 tons of finished nickel this year but the outlook is now highly uncertain. The sanctions have upended Sherritt’s nickel business and the company has just signed a term sheet to sell a majority stake to Gillon Capital.

China’s trade in refined nickel

Surplus moves to China

While the nickel stocks build in the West shows signs of exhaustion, Chinese inventory is rapidly climbing.

Shanghai exchange stocks have almost doubled since the start of the year and now total 87,671 tons, which is the highest level since 2017. The rise has been relentless with no discernible seasonal impact from the new year holiday period.

There may be a lot more sitting in government warehouses.

China’s imports of refined metal surprised to the upside last year and they have remained robust so far this year.

The country imported 231,000 tons of nickel in 2025, the highest tally in four years, according to the World Bureau of Metal Statistics, which collates official customs data.

Yet Chinese nickel producers also exported a record 171,000 tons of metal, mainly to LME warehouses in Asia.

The two-way flow makes little market sense unless imports included purchases by government stockpile managers.

Macquarie analysts think governments absorbed around 150,000 tons of nickel last year as they look to build reserves of what most deem to be a critical mineral. The bank expects more strategic buying this year.

China isn’t explicitly referenced but the country has long been a strategic stockpiler of nickel and soaking up more metal at a time of low prices is a tried-and-tested policy.

LME and ShFE nickel relative year-to-date performance

Slow rebalancing

China’s import surge has rolled into this year. Inbound volumes of refined nickel jumped by 56% year-on-year to 94,000 tons in the January to April period, while exports fell to just 9,400 tons.

Combined with China’s own expanded smelter capacity, running off Indonesian raw materials, it’s little surprise that domestic inventory is rising and Shanghai prices are underperforming those in London.

The price gap should create a renewed incentive for exports but so far that’s not happening.

It’s not as if the West needs more metal anyway despite the disruption in Madagascar and Canada.

While Indonesian production may well fall this year due to a combination of government mining restrictions and lack of sulfur for processing, it’s clearly going to take time before that becomes manifest in the refined metal segment of the market.

Column: LNG demand in Asia recovers from Iran shock as China buys

(The views expressed here are those of the author, Clyde Russell, a columnist for Reuters.)

Liquefied natural gas demand in Asia is quietly recovering from the shock of losing almost 20% of global supply to the Iran conflict as top buyer China shows signs of returning to the market.

The biggest-importing region is on track for arrivals of 21.83 million metric tons in June, the most for five months and also up from the 21.55 million tons in the same month last year, according to data compiled by commodity analysts Kpler.

Asia’s LNG imports had dropped to a six-year low of 18.74 million tons in April after the effective closure of the Strait of Hormuz, following US and Israeli attacks on Iran on February 28, stopped shipments from Qatar, which shipped 80.9 million tons in 2025.

China only just held onto its status as the world’s biggest LNG importer in 2025 as imports dropped to 66.48 million tons, slightly ahead of Japan.

For the first five months of 2026 it seemed certain that China would drop to second place because its utilities steered away from buying spot cargoes as prices surged in the wake of the Iran war.

The price of spot LNG for delivery to North Asia jumped to a three-year high of $25.30 per million British thermal units (mmBtu) in the week to March 20, up 143% from the $10.40 that prevailed before the Iran conflict.

Prices subsequently eased to $16.05 per mmBtu by mid-April, but have since climbed to end at $18.80 in the week to June 5.

Part of the rise in prices stems from China taking more of the super-chilled fuel, with imports forecast by Kpler to rise to reach 4.48 million tons in June, down slightly from the four-month high of 4.74 million in May.

China’s imports in May and June are also well ahead of the 3.78 million tons for March and April’s eight-year low of 3.63 million tons.

LNG imports by China, Japan, India

Japan gains

However, China’s increased appetite for LNG has been more than matched by Japan, which is also on track to see imports rise in June, with Kpler estimating arrivals of 5.33 million tons, a three-month high and also above the 4.91 million tons from June 2025.

South Korea, the third-biggest LNG importer, is forecast to have arrivals of 3.26 million tons in June, down slightly from both May’s 3.37 million and 3.48 million in June last year.

The loss of cargoes from Qatar was most felt by South Asian buyers, with India’s LNG imports dropping to a three-year low of 1.67 million tons in March.

However, they are expected to recover to 2.09 million tons in June, just behind the 2.11 million from June last year, as India sources LNG from alternative suppliers such as Angola, Nigeria and the United States.

Pakistan, which used to buy almost exclusively from Qatar, has struggled to find alternatives, with June imports expected at just 210,000 tons, with one cargo from Oman and one from Qatar, which has seen a handful of vessels manage to exit the Strait of Hormuz in recent weeks.

Pakistan’s imports in June are about one-third of the 620,000 tons from the same month in 2025, but have recovered somewhat from the 10-year low of 70,000 tons in April.

On the supply side, the initial surge of US LNG that headed to Asia in the wake of the start of the war against Iran is starting to ease, with exports of 2.73 million tons in June, down from the record high of 4.07 million in May.

However, US shipments to Asia are still running at rates well above the average of 1.15 million tons in the three months leading up to the attack on Iran.

It appears that US LNG is switching back to Europe, with Kpler estimating exports of 4.99 million tons in June, up from 4.53 million in May, which was the lowest since October 2024.

(Editing by Sonali Paul)

Malaysia to promise Japan maximum possible LNG and naphtha supplies, Nikkei reports

Malaysia’s Prime Minister will agree to provide Japan with the largest possible supplies of liquefied natural gas (LNG) and naphtha as Tokyo seeks to diversify its sources of energy and petrochemicals, the Nikkei newspaper reported on Wednesday.

Japanese Prime Minister Sanae Takaichi and Malaysian Prime Minister Anwar Ibrahim, currently visiting Tokyo, are expected to formalize this pledge in a joint statement at a summit later on Wednesday, the report added.

Japan faces a potential LNG supply crunch due to tensions linked to the Iran conflict, as air-conditioning demand in the country rises heading into summer.

Global LNG markets are already under pressure from conflict-linked supply disruptions and constrained flows through the Strait of Hormuz, a key route for about a fifth of global crude oil and LNG shipments.

Japan imports about 15% of its LNG from Malaysia, its second-largest supplier after Australia, according to the newspaper.

Malaysia and Japan will also seek to work together on economic security with China’s export restrictions on rare earth elements in mind, the article said.

Japan and Western governments have been seeking to diversify critical mineral supply chains away from China, the world’s largest rare earths producer.

In May, Japan signed an agreement with Australia to strengthen cooperation on energy and critical minerals, while public broadcaster NHK reported in April that Tokyo and Paris had agreed to bolster rare earth supply chains.

Additionally, the Japanese and Malaysian prime ministers are expected to discuss cooperation in nuclear energy, with Japan sharing its expertise in power plant technology and site selection, the report said.

The summit also includes plans for discussions on AI policy, aimed at joint applications in agriculture, mobility and education, Nikkei added.

(By Nikita Maria Jino and Kumar Tanishk; Editing by Jonathan Ananda)

Trafigura secures funding to keep Australian smelters running

The Australian government will provide a further A$105 million ($73.68 million) to support Nyrstar Australia in progressing modernization studies at its South Australian and Tasmanian smelting operations, the industry minister said on Wednesday.

The support is in addition to the previous amount of A$135 million ($87.4 million) announced in August last year, as part of Australia’s strategy to become a key supplier of critical minerals to Western allies.

The funding will support Nyrstar, a unit of the trader Trafigura, in maintaining operations at both smelters in 2026, while it completes studies to produce critical minerals. It previously said it would look at producing germanium and indium in Hobart, in the country’s south, and antimony and bismuth from Port Pirie in South Australia.

“The move highlights ongoing pressure on global smelters from high costs and weak processing fees, while underscoring the strategic importance of maintaining domestic metals processing capacity,” BMO analysts said in a note Wednesday.

The Hillgrove gold-antimony project. (Image courtesy of Larvotto Resources.)

Australia’s Larvotto Resources (ASX: LRV) has signed an offtake agreement with Glencore (LON: GLEN) for its 100%-owned Hillgrove gold-antimony project in New South Wales.

The agreement covers gold concentrate production during the first seven years of mining operations, with expected annual offtake being approximately 15,000 dry metric tonnes, Larvotto said in a press release on Tuesday.

The agreement is structured on a mine-gate basis, with Glencore responsible for all logistics from the mine to the final customer destination.

“As we move closer to first production at Hillgrove, securing a globally recognized offtake partner for our gold concentrate is another important milestone in the transition from development to operations,” managing director Ron Heeks stated in the press release.

“As expected with the strength in the gold price, there was a high level of interest for the offtake during the tender process from all major commodity houses.”

Last year, the company reported 90% tungsten recovery with a 16X increase in feed grade delivered in metallurgical testwork, which it said also indicates a simple and cost-effective processing circuit would produce a saleable tungsten concentrate.

“Metallurgical testwork continues for the potential production of a tungsten concentrate by-product from Hillgrove, with offtake discussions expected to progress as development activities advance,” Heeks said.

First production at Hillgrove remains on time and budget, with commissioning expected in August this year, the company said.

Larvotto’s stock traded flat on Tuesday. The company has a A$690.3 million ($485 million) market capitalization.

Northern Star rejects Elliott push to sell company

Australia’s largest gold miner Northern Star Resources (ASX: AU) has rejected a proposal from activist investor Elliott Investment Management to explore asset sales or a potential takeover, arguing the timing is wrong as the company works through operational challenges and a leadership transition.

Northern Star chair Michael Chaney said Wednesday the board does not support launching a sale process despite Elliott’s recent call for a strategic review after building a stake estimated at between 3% and 4%. Elliott’s proposal followed a series of guidance cuts over the past year as processing mill issues at Kalgoorlie contributed to the company’s underperformance relative to peers.

“With reference to Elliott’s suggestion that the board should run a sale process for the company, we do not consider that this is the right time to do so,” Chaney said in the letter to shareholders.

Chaney said Northern Star has previously considered takeover and merger approaches but concluded the proposals were not in shareholders’ best interests. “We had investment banks propose a spin-off of assets and we separately had our financial adviser review those options,” he said. “For now, we are comfortable holding the assets we do but this is a matter that will remain under regular review.”

The dispute comes at a sensitive time for the company. Elliott’s campaign to refresh the board and review strategy emerged days after CEO Stuart Tonkin announced plans to step down after nearly a decade in the role. Northern Star has begun searching for a successor as it seeks to restore investor confidence and improve operational performance.

Elliott’s mining track record

Elliott managed about $79.8 billion at the end of 2025 and has become one of the mining sector’s most closely watched activist investors. Last year, it disclosed a large stake in Toronto-based Barrick Mining (NYSE: B) (TSX: ABX) as the world’s third-largest gold producer struggled to capitalize on a rally in bullion prices.

The firm has also campaigned against BHP Group, pushing the miner to spin off its oil and gas business and simplify its dual-listed structure. Elliott previously targeted Kinross Gold, a campaign that resulted in a $300-million share buyback.

Northern Star faces pressure from aging pits, rising costs and recent guidance downgrades. UBS said in March the company could benefit from selling lower-margin, shorter-life mines, while Elliott argued a strategic review would allow the board to weigh a potential transaction against the risks of a multi-year turnaround.

The developments highlight growing pressure on mining companies to unlock shareholder value after periods of operational underperformance. Activist investors have increasingly targeted large resource companies, pushing for asset sales, spin-offs and strategic reviews when production setbacks or missed targets weigh on valuations.

Russian aluminum’s share of LME stocks rebounds to 93% in May

The share of available Russian-origin aluminum stocks in London Metal Exchange warehouses bounced back to 93% in May from 72% in April, exchange data showed on Wednesday, as traders opted to withdraw Indian metal.

Total available, or on-warrant, aluminum inventories on the LME fell 23% in May to 254,625 metric tons and stand at 250,525 tons, the lowest since May 2025, as production and logistical constraints in the Middle East tighten global supply.

In absolute terms, available Russian aluminum fell by 3,950 tons to 237,175 tons in May. Its share rose, however, as available Indian stocks dropped by a steeper 71,750 tons.

That left just 17,450 tons of Indian metal as the only non-Russian-origin available aluminum in LME warehouses at the end of May, after the withdrawal of 2,275 tons of Indonesian aluminum.

The share of Russian metal had been 92% in March before Indian aluminum was put back on warrant in April.

Many traders avoid Russian metal even though material produced there before April 13, 2024, can still be traded. Aluminum produced in Russia after that date was barred from the LME warehousing system to comply with Western sanctions.

Meanwhile, the share of Chinese-made copper among available LME copper stocks nudged up to 53% in May from 51% in April, even as the absolute amount fell by 36,425 tons to 141,025 tons.

Total available copper stocks decreased by 79,375 tons to 266,875 tons.

The share of Chinese-origin nickel held steady at 71% of available LME stocks at the end of last month.

(By Tom Daly; Editing by Mark Potter)

Russia fails for third time to sell off confiscated stake in gold miner

Russia, Moscow House Russian government. Stock image.

The Russian state failed for a third time to auction a 67.2% stake in gold producer Uzhuralzoloto (UGC) that it had seized from its owner last year, the state auction website showed on Wednesday.

The auction was declared void as no bidders were cleared to participate, and no deposit had been paid in respect of the sole bid received from businessman Mikhail Pimulin, the website showed.

Russia’s federal property management agency has not said whether it will hold another auction.

A Russian court ruled last July that the majority UGC stake previously owned by businessman Konstantin Strukov should be transferred to the state, part of a wider pattern of nationalizations of assets of Russian companies and Western firms that have pulled out of Russia since the start of the war in Ukraine.

Prosecutors accused Strukov and several others at the time of obtaining their property “through corruption.” However, he has not been charged and is not in custody. The government is keen to sell the stake to ease budget pressures.

The previous auction failed last month after only one bidder – gold miner Pokrovskiy Rudnik, owned by Atlas Mining – submitted a complete application and paid the deposit, while a second contender failed to pay the deposit and provide the required documents.

The sale was structured as a Dutch auction, in which the price is gradually lowered until a bid is placed. This could have seen the stake sell for as little as 50% of the starting price of 162.02 billion roubles ($2.25 billion).

Another court-confiscated asset, Moscow’s Domodedovo Airport, was sold via Dutch auction for the minimum price of $869 million in January.

($1 = 71.9500 roubles)

(By Anastasia Lyrchikova; Editing by Mark Trevelyan)

Russia to make fourth attempt to auction confiscated stake in UGC

Russia will make another attempt to sell its 67.2% stake in gold producer Uzhuralzoloto (UGC) via a Dutch auction after three failed attempts to auction the asset, state property agency Rosimushchestvo said.

Bids will be accepted from June 11 to June 18, with results expected on June 19.

The starting price has been set at 162 billion roubles ($2.25 billion) for the UGC stake and other confiscated assets previously owned by businessman Konstantin Strukov.

A Russian court last July ordered the majority UGC stake owned by Strukov to be transferred to the state, part of a broader wave of nationalizations since the start of the war in Ukraine.

($1 = 71.8455 roubles)

(By Anastasia Lyrchikova and Maxim Rodionov; Editing by Mark Trevelyan)