After the Donald’s Demolition Derby in the Persian Gulf – A Last Ride on Marine One Won’t Be Far Behind

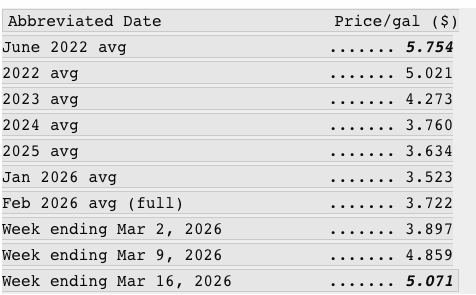

Well, here’s another flashing red warning light. The price of #2 diesel oil – the fuel that enables America’s giant trucking, rail and farm tractor fleets to generate and haul nearly $100 billion of GDP each and every day – including Sundays, holidays and snow days – is now up a staggering +44%from its January 2026 level. At $5.07 per gallon at the end of last week, in fact, it is knocking on the door of the $5.75 per gallon peak it reached during the June 2022 inflation blow-off top.

As the workhorse hydrocarbon of the American economy, #2 diesel oil is always a leading vector of stagflation: It gets embedded over and over again in supply chain costs as goods move through farm, factory, warehouse and distribution commerce, and also burdens output expansion when it begins to spurt higher like at present.

National Average Price Of Diesel Oil, 2022 to 2026

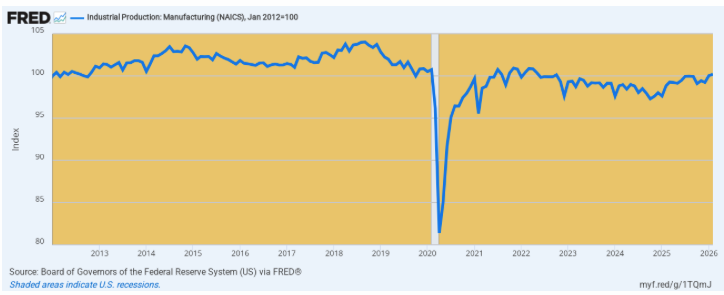

Needless to say, America’s manufacturing economy doesn’t need any new cost shock barriers. Output growth was already sputtering before the Donald had his chain pulled by Bibi Netanyahu. In fact, the index of manufacturing output for February 2026 was at the very same level it stood at in February 2012.

That’s right. We have had one quarter century of absolute stagnation in the level of physical goods output in the US economy. And now the hammer is about to come down hard on both the energy and food supply chains which fuel the aggregate economy.

Index of Manufacturing Output, 2012 to 2026

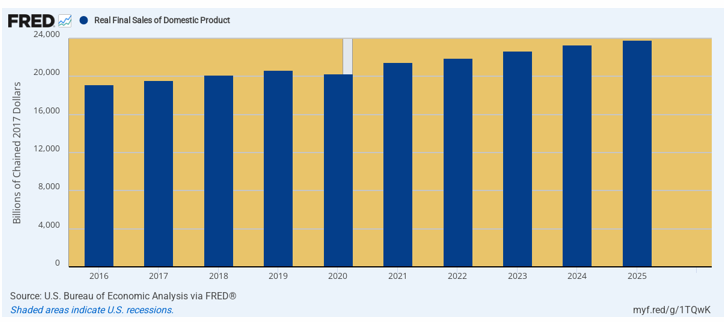

Of course, the sheer stagnation of the manufacturing economy despite the Donald’s whirligig of tariffing and attacks on alleged malefactors of trade the world over hasn’t diminished his Greatest Economy Ever boasting by one bit. So again, we must point out that the Donald has presided over the “worst growth ever” during his two turns at bat to date, not the best.

Thus, during his first term the real economic growth rate as measured by real final sales of domestic production weighed in at just 43% of the 1947 to 2000 average under 10 different presidents. Likewise, for all his attacking of Sleepy Joe’s alleged economic disaster the growth rate in 2025 was actually down by 36% from the 4-year average under Biden.

Real Economic Growth Per Annum:

- 1947-2000: 3.54%.

- 2016-2020: 1.53%.

- 2020-2024: 3.48%.

- 2024-2025: 2.23%.

Yes, the Donald never lets facts or realities get in the way of his braggadocio. Still, now that he has launched a double-barreled attack on the world via utterly misbegotten notions about both economics and national security we perforce wonder how in the world he thinks this utterly reckless escapade is not going to come crashing down on his own political head?

Real Final Sales Of Domestic Product, 2016 to 2025

That is to say, in the vernacular of the moment: There was no “imminent threat” to domestic prosperity owing to the trade policies of foreign countries, nor was there an imminent national security threat from the Iranian regime in Tehran. Putting the US economy in harms’ way owing to a globe-shaking economic cataclysm originating in the Donald’s Persian Gulf Demolition Derby is just plain insensible.

After all, we have debunked elsewhere the Bibi Netanyahu Lie about an Iranian nuke lurking around the the corner and have also shown that its military could not have gotten a plane, missile or ship even past the Strait of Gibraltar. Yet when it comes to the sheer idiocy of the scary stories about Big Bad Iran that led to the current insanity in the Persian Gulf, just consider the present topic of GDP.

We are talking about the sheer economic heft it would take any nation to mount a meaningful attack on the American as amplified below, but here’s the spoiler alert. The US economy even as impaired with inflation, debt and speculation as it is generates nearly $90 billion of GDP per day at its current run rate.

In turn, that means every four days the US economy generates more output than does the Iranian economy in an entire year!

And that’s not all. Iran’s entire defense budget of $23 billion in 2025 was equivalent to just eight days of Pentagon spending.

So holy moly. How does a pipsqueak economy and midget military constitute a threat so severe that it became necessary to ignite a Demolition Derby in the Persian Gulf?

The truth is, it’s just plain barking insanity to claim that the Iranians are so evil and irrational that even if they scrapped together enough highly enriched uranium for a few nukes that they would launch them against the territory of the United States.

Of course, they have no long-range bombers or missiles that could deliver fully weaponized nukes even if they had them, but they also don’t have another even more crucial ingredient. To wit, a raging national suicide impulse that would a prerequisite for dropping a bomb on Washington if Iran had the delivery capacity because it would mean the immediate and total incineration of their entire country – virtually every man, woman and child in every one of their major cities.

Stated more clinically, the entire case for uncorking any and all means including a devastating war in the Persian Gulf to prevent Iran from getting a nuke – which its supreme leader had a long-standing fatwa (religious command) against until Bibi Netanyahu murdered him – is that Iran purportedly presents the one case on the planet where MAD (mutual assured destruction) would fail.

That is to say, after the US incinerated upwards of 200,000 innocent civilians at Nagasaki and Hiroshima in 1945 the nuclear bomb genie has been kept in the bottle. MAD has worked, will work and there has never been any plausible case made that Iran’s theocratic regime is any exception.

So what we are dealing with amounts to a war with 21st century technology of destruction based on religious fanaticism. And we do not mean that of the Shiite clerics who misrule the Iranian people.

The real fanatics are Bibi Netanyahu and the neocon warmongers domiciled in the banks of the Potomac. They have created a “47-Year War on America” narrative which is an utter, complete and unmitigated Big Lie, as we have documented in recent posts.

But now this horrific Big Lie has become embodied in the most senseless war by far that the American Warfare State has yet launched. And its not only jeopardizing upwards of one-fourth of of globally consumed petroleum and LNG-based hydrocarbons, but the global food supply, too.

That’s because at the end of the day world agriculture production is now an embodiment of nitrogen fertilizer, which in turn is extracted from natural gas. And anyone in possession of the facts, a brain to think with and the discipline to weigh the balances inherent in attacking Iran would have known that the Persian Gulf countries sit atop the world’s cheapest and most abundant natural gas.

Qatar, Iran, and Saudi Arabia possess enormous reserves. Gas feedstock accounts for 70–90% of the cost of producing ammonia and urea. Gulf producers therefore enjoy a structural cost advantage that no one else can match. Accordingly, they have built world-scale plants right next to the gas fields and right next to the sea.The numbers are staggering:

- Global ammonia production reached approximately 189.8 million metric tons in 2024 (IFA), with seaborne trade around 18–20 million tons annually.

- The Middle East/Persian Gulf region accounted for 23% of global ammonia trade in 2025. Countries exposed to the region represent roughly 30% of all globally traded ammonia.

- Urea is even more concentrated. Global urea production hit a record 200 million metric tons in 2024. Seaborne trade volumes run 55–60 million tons per year. The Persian Gulf supplies 46–50% of globally traded urea and nearly half of all urea exports worldwide.

- The five key Gulf exporters (Iran, Qatar, Saudi Arabia, UAE, Bahrain) supplied 34% of global urea trade in 2024.

- Qatar alone accounted for 10–11% of world urea exports.

- Saudi Arabia also supplied 8–10% of the world total.

- Iran supplied 5–12% and was the second or third-largest supplier in many recent years.

- Monthly exports from the Arab Gulf routinely exceed 1.5 million tons of urea, with Iran adding another 350,000–400,000 tons per month in normal times.

In 2024, 18.5 million tons of urea — more than one-third of all globally traded urea — passed through the Strait of Hormuz. Then when you add in sulfur (the Gulf supplies about 44–50% of global exports) and phosphates, it turns out that the Strait handles roughly one-third of all global fertilizer trade.

Signal Ocean data for 2025 showed that 20% of all fertilizer flows originated from the Arabian Gulf — rising to 46% when limited to urea alone.

Needless to say, these cargoes don’t stay in the Gulf, but rather they feed the world:

- India imports more than 40% of its urea from the Persian Gulf region.

- Brazil, the United States, Europe, Southeast Asia, and Africa all rely heavily on Gulf urea and ammonia.

- One analysis showed that Qatar’s nitrogen fertilizer exports alone kept 43 million people fed in the U.S., Brazil, and India combined (2022 baseline, still relevant).

Farmers in Iowa, Punjab, and the Brazilian Cerrado plant corn, wheat, and soybeans that literally grow on Gulf natural gas transformed into fertilizer. When Gulf supply is disrupted, prices spike globally — as we have seen dramatically already.

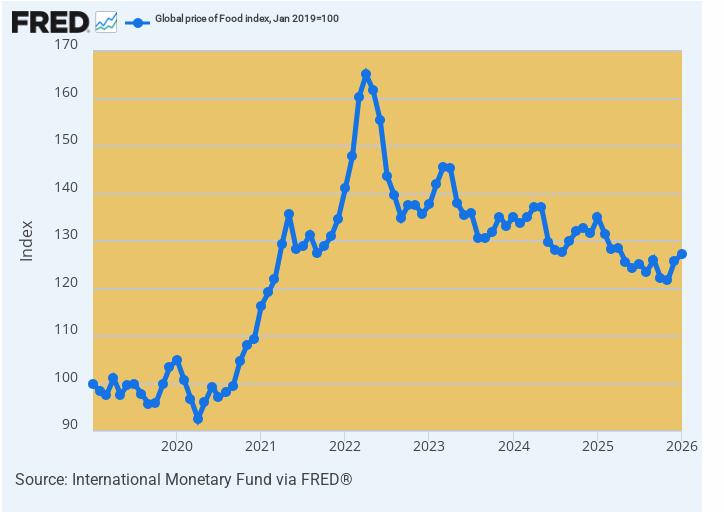

Yet we are just getting started on the food front. When war between Russia and Ukraine broke-out in February 2022, the world food index soared by 63% in a matter of months. And that was owing to both countries’ significant role as suppliers of wheat and other food and feed grains, which commodity price effects than worked their way through food supply chains for the next two years.

This time, however, we are talking about the entire food crop production system in the entire world. Prices of ammonia and urea are already up by 30-50%, and this is coming just on the eve of the planting season across the entire northern hemisphere.

It is virtually certain, therefore, that planted acreage will be reduced and yields on what is planted will fall materially because application rates will be reduced owing to soaring prices.

Global Food Price Index, 2018 to 2026

In short, roughly one-third of global fertilizer trade, 20% of oil, and 20% of LNG transit the narrow passage of the Strait of Hormuz. In normal times, 18–20 million tons of urea and millions of tons of ammonia move through it annually. When conflict closes or threatens the Strait — as has now occurred — production halts at giant plants natural gas processing and fertilizer plants in Qatar, Saudi Arabia, and Iran. Ships sit idle. Insurance costs skyrocket. And the world discovers just how dependent modern agriculture has become on one fragile maritime corridor.

In short, by November 2026 the price of food and energy will be soaring, Washington will be in paralysis owing to an inability to finance the $200 billion tab for the Bibi/Donald War announced today, and the fact the public debt would then be in excess of $40 trillion if the Donald could muster enough votes to raise the public debt ceiling to that level.

He won’t remotely have the votes because his vicious school-boy attacks have alienated most of whatever sensible heads remain in the banks of the Potomac. Even the MAGA faithful by then will be lined up in a circular firing squad long before the election.

At that point, the Donald will be confronted with “doing it the easy way or the hard way”,

He’d be well advised to read Tricky Dick Nixon’s memoirs on how best to handle the choice between resignation and a FINAL RIDE ON MARINE ONE or impeachment – a wholly deserved choice which is surely coming his way long before next year’s spring solstice.

The Donald Gets a Double-Whammy

It sure looks like the Donald is on the receiving end of a double-whammy. His victory declaration in Iran looks to rank right up there with George Dubya Bush’s “mission accomplished” pratfall on the deck of a US aircraft carrier in 2003; and that also means that his SOTU boasting about defeating “Joe Biden’s” inflation and getting the gas pump price under $2 per gallon is out the window, too.

What’s back in play front and center, therefore, is the AFFORDABILITY issue come November. The Dems have no clue about how to fix it, of course, but they sure as hell will be brutally pounding the GOP candidates and the Donald with the latter’s own bogus hot air on the matter.

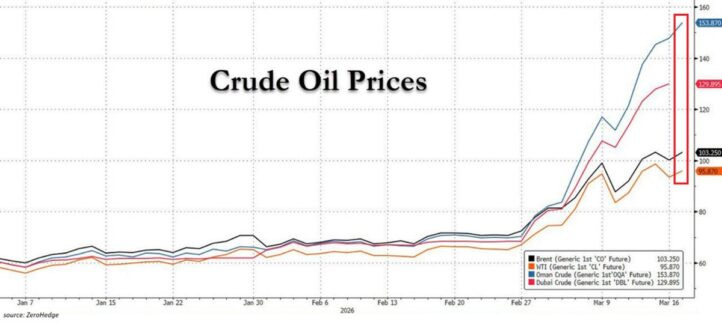

For want of doubt, consider the conflagration in the global oil markets at this very moment. At ground zero in the Persian Gulf, the major crude oil from the region have already shot the moon.

Thus, Oman crude prices are up to $154/barrel, crossing $150 for the first time ever. At the same time, Dubai crude is up to $130/barrel, while Brent is trading at $110.

This means, in turn, that the gap between Oman and world prices is off-the-charts wide, and now stands at 30% or $44 per barrel. By comparison, before the Iran War, the difference between all benchmarks was just $5 per barrel during January and February.

In very short-run, of course, Brent and WTI are priced based on US and European supply conditions, while the actual disruption is concentrated in the Middle East, meaning they do not fully capture the severity of the physical shortage. YET.

On the other hand, global crude oil markets everywhere and always eventually get arbitraged, causing the major marker grades to fully reflect worldwide supply, demand and inventory conditions. So unless the Gulf is re-opened within a matter of days, the marker grades will soon rise toward these Gulf prices as global inventories continue to be liquidated.

Short-Run Breakout of Persian Gulf Crude Oil to $150/bbl

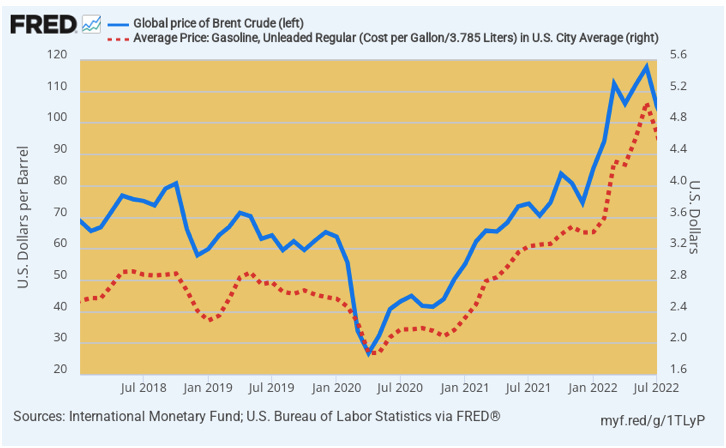

We therefore needs turn to the Brent marker crude oil price, which is the economic thermostat that measures conditions in global energy markets based on worldwide supply, demand and inventory factors. And what we can see is that Brent is already back up to nearly $110 per barrel, which is the zip code where global crude oil peaked during the June 2022 inflationary blow-off.

Brent Crude Oil Price, 2022 to 2026

Of course, the Donald bravely claims that oil prices will “drop like a rock” as soon as markets realize that the so-called Iranian Terror State is no more. But actually the opposite it true.

Contrary to White House misinformation and Hasbara lies from Bibi Netanyahu/neocon brigades on the internet, Iran still has large stashes of missiles and drones buried deep in protected underground vaults—many of them lining the Persian Gulf. These lethal weapons can and likely will turn the Strait of Hormuz into the mother of all economic dumpster fires.

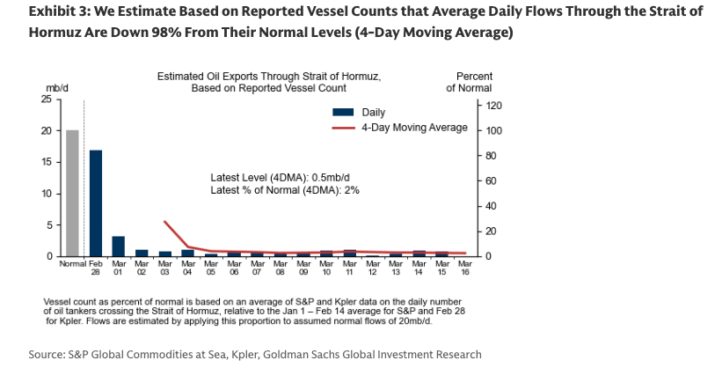

Already, crude oil tanker traffic has slowed to a crawl, meaning that effective supply in the world is running at about 85 million barrels per day (mb/d), while demand was running at 105 mb/d prior to the Bibi & Donald attack on Iran. In turn, this means that OECD commercial stocks of about 2.86 billion barrels before the war are being drawn down by 5% each and every week that the war continues.

And, no, the ballyhooed IEA release last week of 400 million barrels from strategic petroleum reserves won’t make much difference. It will off-set just 1.7 weeks of lost Persian Gulf supply.

And that’s not the half of it. As usual, the Israeli’s are busy adding insult to injury. So last night they triggered a further Persian Gulf escalation by bombing the world’s largest natural gas field, the Iranian South Pars site. The latter is offshore in the Persian Gulf, where it is shared with what Qatar’s calls the North Field.

Not surprisingly, therefore, Qatar’s foreign ministry minced no words:

“The Israeli targeting of facilities linked to Iran’s South Pars field, an extension of Qatar’s North Field, is a dangerous & irresponsible step amid the current military escalation in the region,” says Qatar’s Foreign Ministry spokesman Majed al-Ansari on X.

“Targeting energy infrastructure constitutes a threat to global energy security, as well as to the peoples of the region & its environment……”

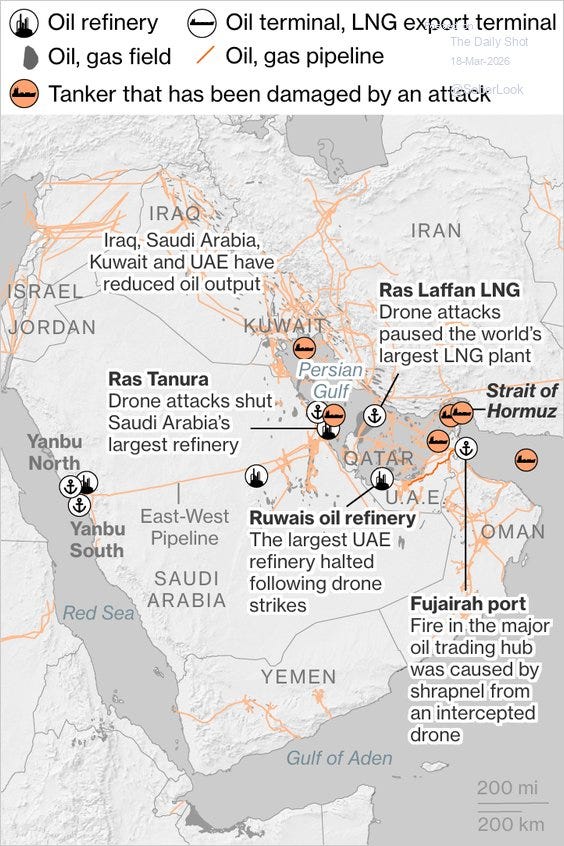

In response, the allegedly defenseless Iranians have now given fair warning for the evacuation of most major Gulf production facilities, meaning that a new barrage of disabling missile and drone attacks are likely on the way. That is to say, the global blockade of world energy supplies behind the Strait of Hormuz is about to take a further turn for the worse.

As shown by the map below, the Persian Gulf may soon go up in flames entirely. And that means not just continued blockage of crude oil and refined product flows, but also a blockage of major shares of global trade in LNG, LPGs ( primarily propane and butane used for cooking and heating), sulfur, nitrogen fertilizers and helium which is vital for semi-conductor production, among others.

The IRGC published satellite images of five specific Gulf facilities with identical Arabicevacuation warnings: military strikes within hours. Ras Laffan and Mesaieed in Qatar. Jubail and Samref in Saudi Arabia. Al-Hosn in the UAE. These are not vague threats. They are targeting packages published on open channels with coordinates the entire world can verify.

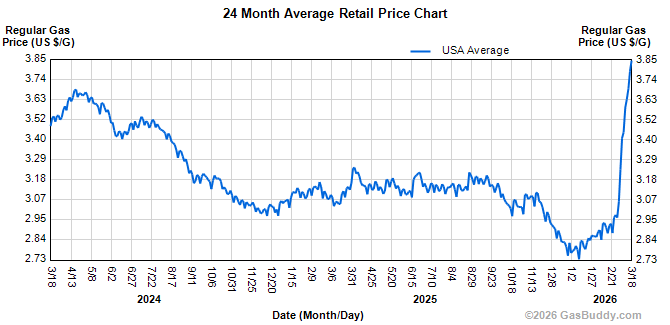

Needless to say, when the global marker crude is rising, pump prices of gasoline in the US are not far behind. Already, the national average pump price has hit just under $4 per gallon, which is up by +27% from the $3.04 per gallon level that was recorded when Joe Biden was packing his slippers, pajamas and hot water bottle to be wheel-chaired out of the White House in January 2025.

National Average Gasoline Price, Unleaded Regular, Last 24 Months

To be sure, the Donald is under the badly mistaken assumption that because the US imports very little petroleum from the Persian Gulf and because he daily genuflects to the “drill, baby, drill” mantra, that the voters in swing districts from Pennsylvania to Arizona won’t notice.

Oh, but the will!

Even junior staffer flunkies on Capitol Hill understand that crude oil is priced in a global market based on supply and demand from all corners of the planet. If the strait remains closed and oil supply stays at the aforementioned 85 million mb/d versus normal demand of 105 million mb/d (+/-), the Brent marker crude will stay well above today’s $110 per barrel; and likely in very short order—as inventories continue to be liquidated—-will ratchet upward toward or even exceed $150 per barrel.

At that point, the Donald surely won’t be “wondering” so much when the fruits of global market price arbitrage are staring him in the face— even if the US doesn’t buy even a single physical molecule of hydrocarbons from the Persian Gulf:

“I wonder what would happen if we ‘finished off’ what’s left of the Iranian Terror State, and let the Countries that use it, we don’t, be responsible for the so called ‘Straight?’ That would get some of our non-responsive ‘Allies’ in gear, and fast!!!” he posted on Truth Social.

In any event, it is not simply our contention that gas at the pump in Flyover America will go to $5/gallon in the event that the global marker crudes continue to rise. What is at work here is nothing less than the laws of markets 101.

For instance, at the Lockdown bottom in June 2020 Brent oil hit $27 per barrel and USA gasoline prices plunged to $1.85 per gallon. But when Brent exploded higher to $118 per barrel in mid-2022, the readings at the USA gas stations marched straight uphill to $5.05 per gallon.

Moreover, the major force in this instance which caused a four-fold swing in the crude oil marker price was demand-side turbulence owing to the Lockdown depression of vehicular traffic, followed by the subsequent sharp rebound as the economy was progressively re-opened and the consumers came out of their fear-driven COVID-bunkers.

By contrast, this time the swing factor will be radical supply shortfalls and sheer uncertainty about when and for how long they will rebound owing to a hot war in the Persian Gulf that is now raging out of control.

Brent Market Crude Versus US Unleaded Regular Gasoline, 2018 to 2022

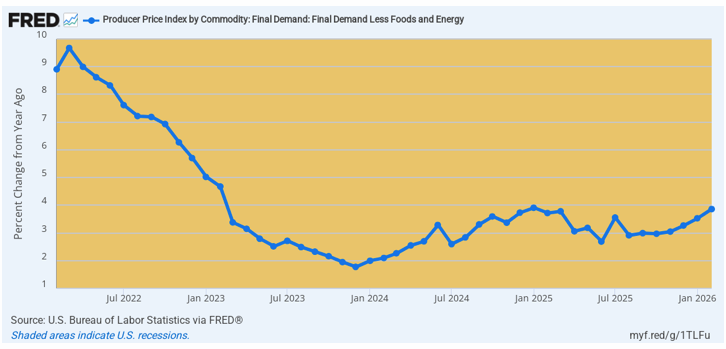

As it happens, the prospect of $5/gallon next November is not the only element of AFFORDABILITY that is lurching in a southward direction. The producer price index for February released today indicates there is a lot more inflation in the pipeline than just surging pump prices.

In particular, the PPI less food and energy has now clearly turned upward. After peaking at a Y/Y rate of 9.7% in March 2022, just ahead of the CPI peak later in the year, this index marched downhill to a low if 1.8% Y/Y in December 2023. But that’s all she wrote, with this index posting at more than double that rate at +3.9% in February.

But here’s the thing. The trend rate posted for February at damn near 4% doesn’t compute to any kind of victory over inflation in the real world where hard-pressed American wage earners struggle to keep their heads above water. At this rate, at dollar earned or saved today would be worth 55 cents after a decade’s time.

PPI For Final Demand Less For And Energy, 2022 to 2026

Thanks to the Donald’s attempted incineration of the Persian Gulf energy and industrial infrastructure, in fact, global food prices are also heading skyward. For instance, upwards of 50% of global trade in urea originates in the Persian Gulf, as does about 30% of ammonia trade, which is a critical precursor for a variety nitrogen based formulations.

Not surprisingly, coming as it does on the eve of the northern hemisphere planting season, the closure of the Strait of Hormuz has already propelled ammonia prices higher to $590 per metric ton, up by +37% from the 2023-2025 average; and in the case of urea, the current $655 price per tonne represents nearly a +28% rise from the prior three year average.

In short, both food and fuel prices will be rising consistently from present levels. In turn, that means that “affordability” has nowhere to go except to the worse.

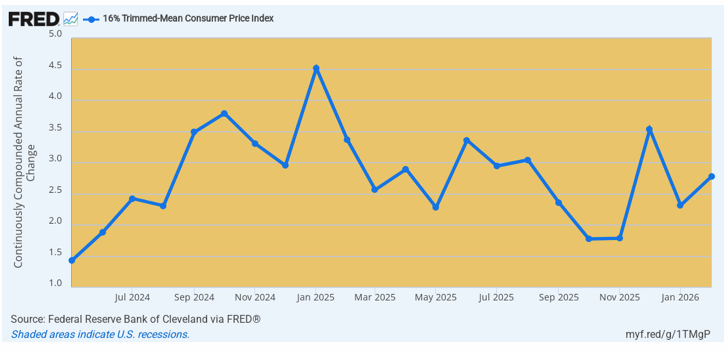

Already our trusty trimmed mean CPI has been signalling for several months that the inflation rate has bottomed and is now moving higher. But with oil above $110 per barrel and gasoline heading to $5 per gallon there is no longer any doubt.

That is to say, the Iran War is heading for an even greater disaster in the Persian Gulf and inflation is fixing to leap toward 5% and beyond. That’s a double-whammy however you slice it.

Annualized Change In 16% Trimmed Mean CPI, May 2024 to February 2026

David Stockman was a two-term Congressman from Michigan. He was also the Director of the Office of Management and Budget under President Ronald Reagan. After leaving the White House, Stockman had a 20-year career on Wall Street. He’s the author of three books, The Triumph of Politics: Why the Reagan Revolution Failed, The Great Deformation: The Corruption of Capitalism in America, TRUMPED! A Nation on the Brink of Ruin… And How to Bring It Back, and the recently released Great Money Bubble: Protect Yourself From The Coming Inflation Storm. He also is founder of David Stockman’s Contra Corner and David Stockman’s Bubble Finance Trader.

No comments:

Post a Comment