The AI boom propping up markets could trigger the next crash, central banks warn

The vast surge of investment in AI, which has powered global stock markets to record highs, risks ending in a financial bust, the Bank for International Settlements warns, as the build-up’s hidden costs begin to surface in company accounts and consumer prices alike.

In its Annual Economic Report, published on Sunday, the Bank for International Settlements (BIS), known as the central bank for central banks, warned that the enormous spending on AI is accumulating financial vulnerabilities that could amplify any future shock and spread from markets into the wider economy

Presenting the findings, BIS general manager Pablo Hernández de Cos said the message was one of "urgency", with policymakers urged to act before any reversal makes the eventual adjustment more painful.

At the core of the warning is the scale of the spending, despite massive investment having supported global growth over the past year.

The five largest "hyperscalers", the technology giants racing to build AI infrastructure, are on track to commit more than $1 trillion (€878bn) to AI-related investment across 2025 and 2026, a pace that is outstripping their earnings and free cash flow and pushing some to borrow heavily to keep up.

The BIS suggests this race is fuelled by a belief that only a handful of dominant players will ultimately prevail, encouraging firms to pour money into projects whose returns remain deeply uncertain.

Echoes of past manias

The report sets today's AI boom against a long historical lineage, from the canal mania of the 1830s and Britain's railway mania of the 1840s to the electrification of the 1920s and the dotcom bubble.

Each began with a genuine technological breakthrough that attracted more capital than commercial returns could justify, the BIS notes, with each episode ending "with an eventual reversal in investment, inducing economy-wide recessions".

Compounding the danger are stretched share prices and opaque financing.

The BIS highlights the spread of "circular financing", in which chipmakers and cloud giants take equity stakes in AI labs that then commit to buying their chips and computing power, effectively recycling money back to the original investors as revenue.

Much of the funding now flows through hedge funds and private credit vehicles that face lighter scrutiny than banks.

According to Zhang Tao, the BIS chief representative for Asia and the Pacific, that reliance on non-bank channels means an AI downturn could unwind into a sharper, faster crash than a traditional banking crisis.

The hidden costs of data centres

Beyond financial markets, critics argue the true cost of the AI build-out is being obscured in plain sight.

A central concern, examined by the Wall Street Journal, is how the technology giants account for their data centres.

By assuming the expensive equipment inside them will stay useful for longer, firms can spread its cost over more years, lowering the depreciation charged against profits in any given period and making earnings look healthier than the underlying cash burn implies.

However, the specialist chips at the heart of these facilities may become obsolete far faster than those extended schedules assume, leaving a gap between reported profits and economic reality, as well as a balance sheet more exposed than it appears should demand disappoint or a sizable need to replace hardware arise.

The physical scale is staggering

Columbia University economist Stijn Van Nieuwerburgh estimates the build-out could cost in the region of $8 trillion (€7tn) over the next six years, financed in part through the kind of off-balance-sheet arrangements the BIS flagged.

The costs are also no longer confined to corporate accounts.

Some economists now warn of a so-called "third wave" of inflation, after the pandemic and tariffs, driven this time by the AI build-out. As chip manufacturers prioritise high-margin parts for AI servers, the resulting squeeze on memory and storage has rippled out to consumer electronics.

For example, Apple raised prices on its MacBooks, iPads and other devices last week, citing an "extraordinary surge in demand for memory and storage" and saying it had "never seen a component price increase this much, this quickly".

The company's shares fell around 6%, their worst day in over a year, as Microsoft, Nintendo and Sony have also made similar moves.

Beyond hidden costs and inflationary pressures, where the strain may spread furthest is raw power.

Goldman Sachs expects data centres to account for nearly half of the growth in US electricity demand by 2030, with consumer power prices forecast to rise around 6% a year through 2026 and 2027.

The BIS itself notes that the build-out's hunger for electricity is already pressuring prices and input costs, with potential spillovers to inflation, though it stresses, as do many economists, that AI could yet prove disinflationary if its promised productivity gains eventually arrive.

The AI Power Crisis Is Creating a Massive New Market for Fuel Cells

Data center developers are scrambling for reliable power, turning away from congested grids and toward on-site fuel cells. Rystad Energy research and analysis projects a tenfold increase in fuel cell market revenues by 2030, rising from around $2.8 billion in 2025 to roughly $30 billion, as AI computing demand drives unprecedented growth in data center construction. A contracted order book of approximately 9 gigawatts (GW), including framework agreements with Oracle, AEP, Equinix, and Brookfield, points to growing confidence among major operators in fuel cells as a viable long-term power source.

US grid interconnection timelines have tripled since 2015, now stretching to three to six years for large loads. Rystad Energy’s research projects 10.4 GW of cumulative fuel cell demand from data centers between 2026 and 2030, with around 40% of projected 2030 US data center capacity modeled as likely to pursue dedicated on-site power generation rather than grid connection. Unlike conventional grid connections or large gas plants, fuel cells can be deployed quickly and run on natural gas today, transitioning to biogas, renewable natural gas or hydrogen as supply matures, while producing lower on-site emissions than combustion alternatives. North America is expected to account for 91% of installed global on-site power generation capacity, thanks to a combination of grid delays, federal tax incentives and an established domestic supply chain.

Power availability has become one of the defining constraints on data center growth, and operators are increasingly looking beyond the grid for solutions. Fuel cells have moved from a niche application to a measurable part of the firm power mix. The question now is whether the supply chain can scale at the same pace as demand.

Lein Mann Bergsmark, Vice President, Clean Tech Supply Chain Research

Fuel cell manufacturers are expanding capacity in response. Aggregate operational and planned manufacturing output is on track to reach 4 GW per year by 2030, up from 1.8 GW today. Solid oxide fuel cells (SOFC) have become the dominant technology for always-on data center power, accounting for around 53% of cumulative stationary deliveries to date. Bloom Energy holds virtually every primary-load SOFC contract in the visible order book, a concentration that presents supply chain risk if demand accelerates faster than one manufacturer’s production capacity.

That concentration extends to materials. Bloom Energy’s SOFC technology depends on scandium, a critical metal used in its electrolyte chemistry. At full utilization of its planned 2 GW manufacturing expansion, Bloom’s theoretical scandium requirement would approach the size of the entire global market, currently estimated to be around 60 tonnes per year. This potential bottleneck is compounded by the fact that China heavily controls the global scandium supply chain. Competitors using alternative electrolyte chemistries do not share this exposure, and a sustained supply constraint could influence how market share develops as the sector scales. Rystad Energy projects SOFC system costs will fall 20 to 25% by 2030, though the pace will depend on manufacturers’ ability to reduce costs across the full delivered system, not the fuel cell stack alone

The $7 Trillion AI Boom Is Turning Into The Energy Trade of the Century

You might think that Shark Tank’s “Mr. Wonderful,” Kevin O’Leary, is betting it all on AI, but he is not.

He is betting on the $5+ trillion in infrastructure required to run it, and that’s where big capital is flowing now.

And he’s betting on Bitzero (NASDAQ: AIBZ) to be one of the first to break AI’s biggest chokepoint: power.

Bitzero was looking further ahead while most of the rest of the market was narrowly focused on AI software and semiconductors.

As a result, on May 5th, Bitzero signed a binding letter for a 15-year lease deal for AI power as it makes its first official leap from low-carbon bitcoin mining to being a power provider for a $5-trillion data-center industry that is desperate for cheap electricity.

This Canadian cryptominer-turned-energy-provider for AI has already secured more than a gigawatt of low-cost power across Norway, Finland, and the United States, as the money moves into the assets that AI can’t run without.

Amazon alone projects $200 billion in 2026 capital spending, with most of it tied to data centers. Microsoft is expected to be around $190 billion. Alphabet is also projected near $190 billion, and Meta has laid out a $600 billion U.S. infrastructure plan through 2028. Current estimates now put combined 2026 capex for Amazon, Microsoft, Alphabet, and Meta as high as $725 billion, driven largely by AI data centers, chips, power, and long-lived infrastructure. McKinsey estimates another $5.2 trillion will be deployed into AI infrastructure this decade. That capital is funding land, power, facilities, substations, and equipment before AI capacity can operate.

Source: Oilprice.com; Reuters; McKinsey & Company; Amazon, Meta, Microsoft, Alphabet Q3 earnings.

Half the AI data centers being announced today may not get built because projects fail to secure power on time.

More than 70% of interconnection requests are withdrawn, and only a fraction reach operation. Global data center electricity demand is projected to approach 945 terawatt-hours by 2030, roughly equal to Japan’s total consumption, according to the latest research from Berkeley Labs, which is affiliated with the U.S. Department of Energy’s Science Office.

Megawatts will decide who builds and who doesn’t.

The AI Build List Is Under Duress

A large share of the AI data centers being announced today may never reach completion because power is not available when projects need it. That creates an advantage for companies like BitZero (NASDAQ: AIBZ) that already control gigawatt-scale electricity.

Artificial intelligence demand is expanding quickly, but the electricity required to run it is becoming harder to secure, slower to connect, and more expensive to deliver.

More than 70% of interconnection requests are withdrawn, and only a small portion reach operation. At the same time, global data center electricity demand is projected to approach 945 terawatt-hours by 2030, roughly equal to Japan’s total consumption.

While investors were previously focused on semiconductor chips as the make-or-break element of the AI boom, it’s now clear that it’s a question of power above all.

And that’s exactly why a forward-thinking cryptominer like Bitzero is well positioned to take advantage of the AI-power gap.

“As electricity prices climb across the U.S., driven in large part by soaring demand from both Bitcoin mining and the rapid expansion of AI data centers, Bitcoin miners are at a distinct advantage because we locked in power access well ahead of the curve,” Mohammed Bakhashwain, founder and CEO of Bitzero Holdings, Inc., told Oilprice.com in a recent interview.

Both cryptomining and AI require the same infrastructure: reliable power, advanced cooling, and industrial-grade data centers.

“While others are still fighting for grid access, permits, and infrastructure, Bitzero secured those assets over the past four years and knows how to operate energy-intensive facilities at scale. That creates valuable optionality. The same megawatt can mine Bitcoin or support AI and data center workloads. In a market where power is the real constraint, we believe flexibility is a competitive advantage,” Bakhashwain said.

Full Speed Ahead on the Biggest Boom in Computing History

Earlier this month, Bitzero (NASDAQ: AIBZ) completed engineering due diligence for up to 520 megawatts at its Kokemäki, Finland campus, eyeing up to 1GW at full ramp. An initial 80MW phase is targeted for the first half of 2027, with 400MW to 800MW expected to follow in later stages as the full buildout advances.

And that’s just one venue.

Bitzero’s Norway operations are already running as a fully built industrial platform. The company is operating Bitcoin mining at power costs below four cents per kilowatt-hour, which keeps the site active and monetized while additional infrastructure is layered on top.

At Namsskogan, the next 70MW tranche is scheduled for energization in the fourth quarter of 2026, tied directly to a defined 325MW expansion corridor that follows existing grid capacity.

And here, in Norway, is where Bitzero’s great leap into data center power just became official.

On May 5, Bitzero signed a binding letter of intent with OneQode Networks covering the full 110 MW capacity of its Namsskogan, Norway data center site under a 15-year lease tied to GPU-based AI workloads. The agreement carries an implied value of roughly $2.6 billion over the lease term and marks Bitzero’s formal entry into the large-scale AI data-center infrastructure market.

This is a double victory for Bitzero.

When it mines in Norway, Bitzero uses its own electricity to generate revenue from the Bitcoin it produces. Under the AI agreement, Bitzero generates revenue by leasing the site’s power capacity and infrastructure to OneQode. Simultaneously, OneQode pays the electricity bill tied to running the AI systems inside the facility.

That means Bitzero captures the recurring infrastructure revenue from the site without directly absorbing the massive ongoing power costs associated with operating large-scale AI workloads.

According to Bitzero management, at full utilization of 110 MW, the Namsskogan site could generate roughly $176 million to $178 million in annual revenue. A recent shareholder analysis modeling the agreement estimated potential annual NOI of roughly $151 million based on an 85% margin profile tied to the lease structure.

It’s the plentiful, low-cost, low-carbon energy Bitzero has harnessed in Scandinavia that OneQode is after.

Norway is served by hydro power, and Finland is served by a cocktail of low-cost hydro, nuclear, solar and wind energy.

Finally, the North Dakota footprint gives Bitzero a second operating lane tied to U.S. demand. The company controls power-backed sites there that position it inside a different pricing and regulatory environment from its Nordic assets.

Across Norway, Finland, and North Dakota, the operating model is consistent: secure power first, bring megawatts online in stages, and deploy that capacity into whichever use case offers the highest return at that point in the cycle, whether it’s mining, colocation, or AI compute.

The AI Investment Model Is Outrunning The Grid

It takes up to 7 years to build out a large-scale power source to feed a data center.

Still, investors have been operating on a massive assumption: That the power will magically be there once all the data centers are built. This is where the data center hype meets an electrification reality.

But securing power isn’t that easy. At a bare minimum, it requires grid studies, transmission access, permitting, utility negotiations and long-term pricing frameworks.

And demand is bursting.

The IEA expects global data-center electricity use to grow 4X the growth rate of total electricity demand from every other sector combined. The agency is eyeing data center power demand of roughly double to around 945 TWh by 2030.

Similarly, Goldman Sachs has forecast data-center power demand soaring 175% by 2030 compared to 2023 levels.

That’s like adding an entire country to the grid.

The business of sourcing power is not keeping pace with the business of building out data centers.

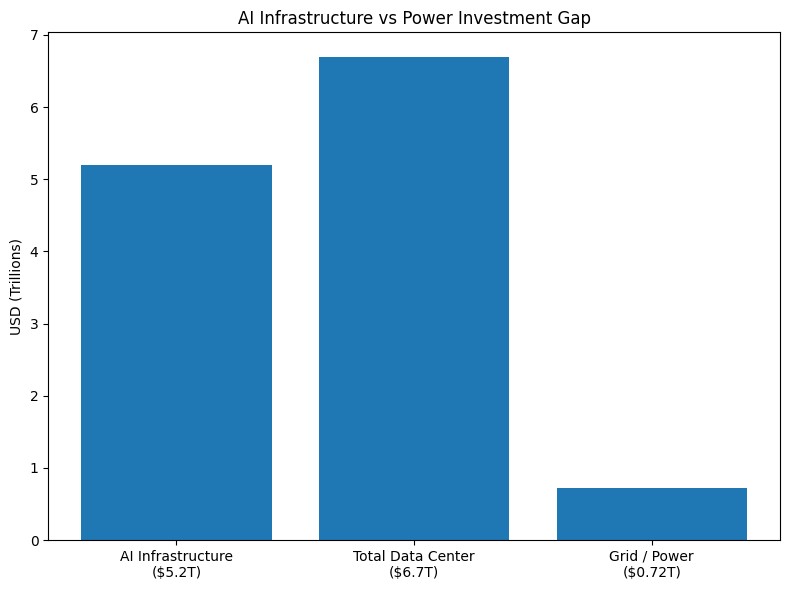

We will need $6.7 trillion in capital by 2030, including $5.2 trillion for AI infrastructure alone, in order to make the data center hype a reality. Yet, so far, grid investment expected to support that demand is only around $720 billion.

With more than a gigawatt of power already secured across Norway, Finland and North Dakota, Bitzero already controls sites, permits, grid access, and expansion capacity while AI developers line up to get a start on the 7-year process.

Why Bitzero’s Model Is Getting Attention

Bitzero (NASDAQ: AIBZ) is building large-scale campuses backed by secured, low-cost power and positioning them for AI and high-performance computing demand. It’s not choosing between crypto and AI. It is running both. Bitcoin mining keeps capacity active and generates cash flow, while the same sites are being developed to support AI and HPC workloads as that demand scales.

“We see a really big opportunity in HPC,” CEO Mohammed Bakhashwain said, pointing to an engineering team that has already worked on deployments with Microsoft and Nscale in Norway. The company controls land, power, and infrastructure in place to deliver large campuses, and is already moving to market that capacity to AI tenants.

The model is built to capture two revenue streams off the same megawatts. Mining today and higher-value AI and colocation tomorrow.

“We’re hoping to get the best of both worlds—the long-term, investment-grade cash flows from HPC and AI, while having exposure to Bitcoin,” Bakhashwain said.

That keeps sites operating while capacity is repositioned for larger, longer-term contracts.

That structure is what has drawn investor attention.

Kevin O’Leary doesn’t frame Bitzero as a mining company. He calls it an energy contract business. The asset is the site: power secured at low cost, tied to land, permits, and continuous load. Mining monetizes that power now. Leasing compute and capacity to large off-takers is where the longer-term value sits.

“The value of what Bitzero has has risen dramatically, and I think over time the market will recognize that,” O’Leary said.

The company is building capacity that can be deployed into whichever market pays more at a given time. That is how the same infrastructure can generate cash flow today and scale into larger contracts as AI demand continues to build.

The AI power boom is also reshaping investor interest across some of the largest publicly traded U.S. energy companies. EQT Corporation (NYSE: EQT), the country's largest natural gas producer, is widely viewed as a key supplier of fuel for the gas-fired generation expected to support rising electricity demand. Vistra Corp. (NYSE: VST) has become a leading AI infrastructure play through its diverse fleet of natural gas, nuclear and renewable power assets, while Constellation Energy (NASDAQ: CEG) has attracted significant attention thanks to its position as the nation's largest producer of carbon-free nuclear electricity. Together, these companies underscore a growing realization across markets: the AI race is no longer just about chips and software—it is increasingly about securing dependable, long-term power. Companies that already control energy assets and grid-connected infrastructure are likely to occupy an increasingly strategic position as electricity becomes the defining constraint on AI expansion.

Given all of this, Bitzero is not simply participating in the AI buildout. It may be sitting on part of the infrastructure that others will have to come to, just as OneQode did on May 5th.

The bigger point is where capital could start to flow as that logic sinks in.

By. Charles Kennedy