The U.S. Army Just Took a Historic Step to Break China's Rare Earth Dominance

The U.S. Army has placed REalloys at the center of America’s drive to rebuild its heavy rare earth supply chain, selecting the company to build and operate the first-ever commercial critical mineral processing operation on a U.S. military installation.

REalloys (NASDAQ: ALOY) plans to build a heavy rare earth processing complex at the Tooele Army Depot in Utah capable of refining dysprosium and terbium, two of the most strategically important rare earth elements used in high-temperature permanent magnets for defense systems.

For the first time, commercial critical mineral processing is being integrated directly into America’s national security infrastructure. The Tooele platform is expected to support the U.S. Army, the Defense Logistics Agency, the Department of Energy and NASA, placing REalloys at the center of one of the country’s most strategically important industrial buildouts.

Commercial development is targeted to begin in 2027, with initial operating capability expected no later than 2028. That urgent timeframe is scheduled to coincide with the January 1, 2027, federal procurement ban on Chinese rare earth materials used in American defense systems.

REalloys expects to finance, build, and operate the facilities under an Enhanced Use Lease structure, creating a commercial processing platform on federal military property while keeping ownership, financing, and operations in private hands.

The Army award moves REalloys upstream. Earlier this year, the Defense Logistics Agency backed the company’s metallization technology through a contract to expand domestic samarium and gadolinium metal production. The Tooele project reaches further into the supply chain, adding commercial heavy rare earth processing to a platform that already includes metals and alloys.

Washington is compressing years of supply chain development into a matter of months. An integrated domestic rare earth industry is taking shape in real time.

Why The U.S. Army Chose REalloys

Much of REalloys’ heavy rare earth platform was already in place when the Army selected the company for Tooele.

Over the past two years, REalloys (NASDAQ: ALOY) has assembled feedstock agreements, processing rights, metallization technology, and downstream manufacturing capacity designed for what is expected to become the largest heavy rare earth metallization facility outside China through its partnership with the Saskatchewan Research Council.

The company committed approximately $20.6 million to upgrades at the Saskatchewan Research Council’s rare earth processing facility, securing exclusive supply rights for 80% of the facility’s expanded output, including NdPr metal and dysprosium and terbium oxides.

SRC’s initial commercial production remains targeted for early 2027, with REalloys is building a dedicated heavy rare earth metallization facility for dysprosium and terbium metals. Engineering is underway, major equipment procurement has begun, and qualification materials are expected as early as the fourth quarter of 2026

That gives REalloys something few companies in the Western rare earth sector can claim: access to separated heavy rare earth output, a path to metallization, and a U.S. manufacturing base in Euclid, Ohio.

The company has also secured long-term feedstock, including a definitive long-term offtake agreement for 15% of Phase 1 production from Critical Metals’ Tanbreez project in Greenland, a strategic alliance and offtake commitment tied to the Sheep Creek rare earth deposit in Montana, and a proposed supply framework with Ramaco Resources for coal-hosted rare earth material from the Brook Mine platform in Wyoming.

And it’s pursuing additional supply arrangements with domestic and allied sources, including coal-hosted rare earth material from Ramaco’s Brook Mine platform in Wyoming.

The result is a company already moving across multiple stages of the chain that the Army is trying to rebuild: feedstock, processing, metallization, alloys, and eventually permanent magnets.

Washington Is Building An Industry

The Tooele announcement is about far more than a single processing facility.

Over the past year, Washington has introduced procurement restrictions, awarded defense contracts, backed commercial processing, accelerated qualification programs, and now opened the gates of a U.S. military installation to commercial rare earth production.

Those decisions are reshaping an industry that scarcely existed outside China only a few years ago.

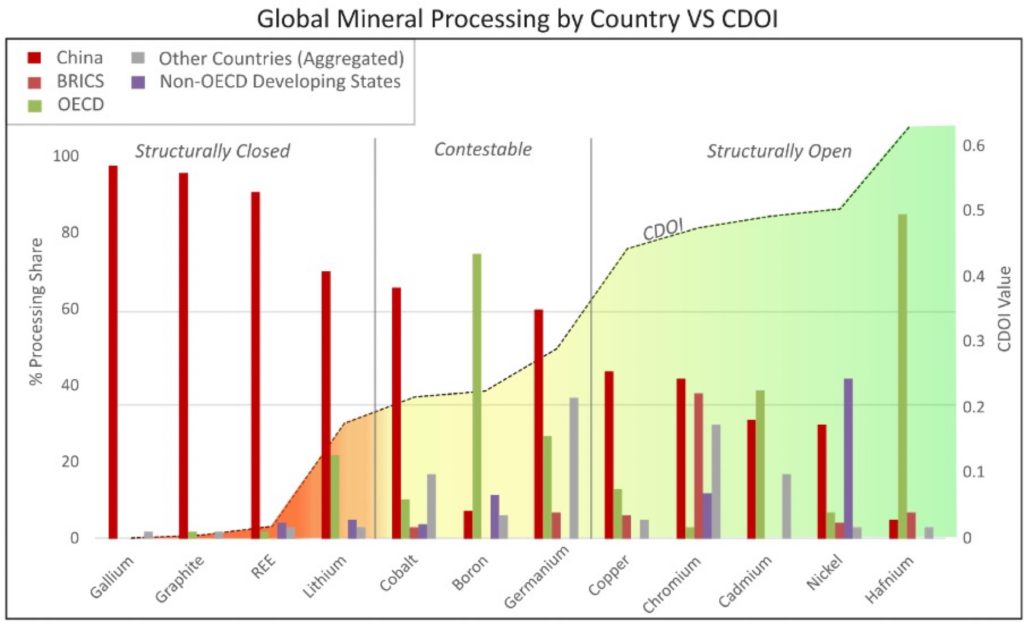

Building a domestic rare earth industry requires far more than opening new mines.

Ore must first be mined and concentrated before it can be chemically separated into individual rare earth elements. Those materials are then converted into high-purity metals, alloyed into specialized magnetic materials and ultimately manufactured into the permanent magnets that power everything from precision-guided weapons and fighter aircraft to electric motors, radar systems and naval platforms.

For decades, China built nearly every step of that industrial chain while much of the West allowed those capabilities to disappear.

The effort extends well beyond the rare earth sector itself.

Earlier this month, President Trump invoked the Defense Production Act to address production bottlenecks across the defense industrial base, citing limited manufacturing capacity, fragile supply chains and long-lead dependencies.

This week, President Trump met with the heads of Lockheed Martin, RTX, Boeing, Northrop Grumman, General Dynamics and L3Harris as the administration pressed the defense industry to accelerate production and replenish U.S. weapons stockpiles.

Three of those companies show exactly why the timeline matters.

Lockheed Martin (NYSE: LMT) builds the F-35, and that jet alone carries more than 900 pounds of rare earth materials, including roughly 50 pounds of samarium-cobalt magnets built to hold their strength at extreme heat. All of it falls under the same January 1, 2027, deadline REalloys is racing to meet at Tooele.

RTX (NYSE: RTX) carries similar exposure through its Patriot missile system and its radar and electronic warfare lines, both of which run on high-purity dysprosium and terbium. Those inputs still trace back through Chinese processing chains, the same chokepoint REalloys’ Tooele complex is meant to break.

Northrop Grumman (NYSE: NOC) has the same problem on its B-21 Raider bomber and its radar and space-surveillance work, including the Deep Space Advanced Radar Capability program. Like Lockheed Martin and RTX, it has to prove its magnet supply chain is free of Chinese material by the 2027 deadline or risk losing eligibility for covered contracts.

Those efforts coincide with the January 1, 2027, procurement restrictions, which require covered defense systems to source compliant rare earth materials and permanent magnets.

Meeting those requirements involves far more than finding new suppliers. Rare earth oxides, metals, alloys, and permanent magnets must all be qualified before they can enter defense production, a process that can take months or even years depending on the application.

That process is already underway.

REalloys (NASDAQ: ALOY) is expected to began qualification efforts for defense-grade heavy rare earth materials by the end of 2026, allowing prospective customers to validate North American-produced dysprosium, terbium and other rare earth materials ahead of the January 1, 2027, procurement deadline.

The result is one of the most coordinated industrial reconstruction efforts the United States has undertaken in decades, and REalloys is at the heart of it.

By. Michael Kern