U.S. Scores Major Rare Earth Win With Greenland Deposit Deal

As Washington races to build a rare earth supply chain that can survive the Pentagon’s 2027 ban on Chinese-origin materials, REalloys (NASDAQ: ALOY) has locked in long-term supply from one of the largest known heavy rare earth deposits in the world.

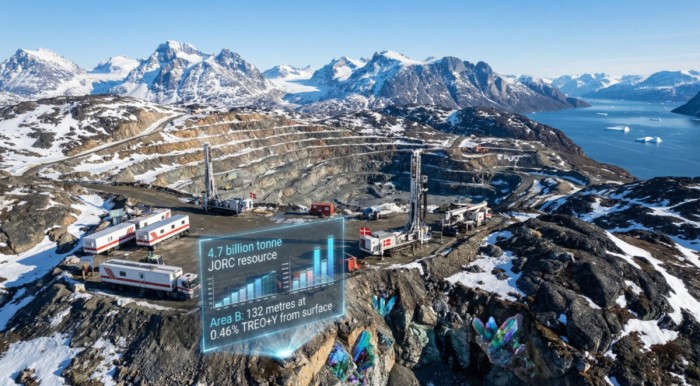

The company announced last Thursday that it has signed a definitive 15-year offtake agreement with Critical Metals Corp. (NASDAQ: CRML) covering 15% of Phase 1 production from the Tanbreez project in southern Greenland, a massive heavy rare earth deposit containing Dysprosium and Terbium, the two most strategically sensitive magnet materials used in fighter aircraft, missile systems, radar platforms, drones, and advanced defense hardware.

REalloys is building one of the only integrated heavy rare earth metallization and magnet production platforms in North America as Washington pushes to break its dependence on Chinese processing capacity before the Pentagon ban takes effect in only seven months.

The company’s Euclid, Ohio, operation focuses on the hardest part of the rare earth supply chain outside China: converting rare earth oxides into defense-grade metals, alloys, and eventually the world’s strongest and most advanced magnet: the NdFeB permanent magnet type used in missile systems, fighter aircraft, radar platforms, robotics, EV drivetrains, and advanced industrial systems.

REalloys says it is scaling that Ohio platform into the largest heavy rare earth metallization facility outside China, supported by a growing network of allied-nation feedstock agreements.

The Tanbreez agreement significantly expands that network.

Under the deal, REalloys will secure 15% of monthly Phase 1 production from the Greenland project for an initial 15-year term.

This is another major announcement for REalloys as the company rushes to stay ahead of major defense deadlines.

The Tanbreez offtake deal follows REalloys strategic partnership with Saskatchewan Research Council, tied to 80% of the output from the Saskatchewan Research Council’s commercial rare earth processing facility. It also adds to the company’s previously secured rights to up to 10% of production from the high-grade Sheep Creek rare earth deposit in Montana, and its control of the Hoidas Lake rare earth asset in Saskatchewan.

GREENLAND IS EMERGING AS A WESTERN RARE EARTH STRONGHOLD

Trump didn’t manage to buy Greenland, but REalloys got its critical minerals.

The strategic importance of the Tanbreez project goes far beyond scale.

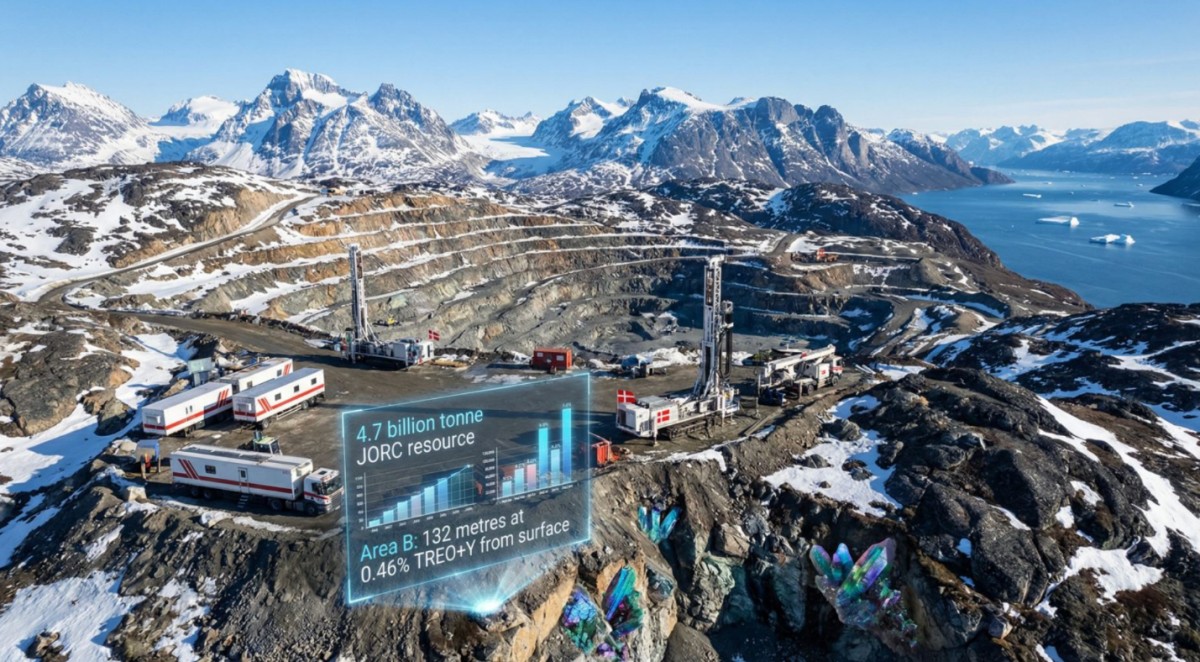

The Greenland deposit is one of the largest known heavy rare earth resources globally and one of the few major Western-aligned projects capable of supplying meaningful quantities of Dysprosium and Terbium outside China.

Tanbreez isn’t just another rare earths venue. It’s a heavy rare earth behemoth, while most global deposits focus on less valuable light rare earth production. Critical Metals estimates heavy rare earths account for roughly 27% of the project’s total profile. Most global deposits focused primarily on light rare earth production.

The Greenland project is already fully permitted and advancing under a Western-aligned ownership structure following Greenland's approval of Critical Metals’ acquisition of a controlling 92.5% interest earlier this year.

For REalloys, the deal secures another long-term heavy rare earth materials now central to Pentagon supply chain planning amid a Middle East conflict that is rapidly depleting the arsenal.

Johns Hopkins economists Steve Hanke and Jeffrey Weng told Fortune magazine that the U.S. has already burned through massive portions of its precision weapons inventory across Iran and Ukraine, while remaining dependent on Chinese-controlled rare earth materials to replace them. The economists suggest that Washington has blown through 45% of its Precision Strike Missile inventory just in Iran, and nearly 50% of its THAAD interceptors and 30% of its Tomahawk cruise missiles, among others.

Those systems rely on samarium-cobalt magnets or dysprosium- and terbium-enhanced NdFeB magnets that still flow overwhelmingly through China’s refining and metallization system. The authors estimate that replenishing just four major weapons systems could require between five and ten metric tons of finished defense-grade rare earth magnets, with more than 95% of current supply chains still tied to China.

And that’s the gap REalloys is helping to close, with a North American solution helmed by a leadership lineup that represents the who’s who of American defense.

Joe Kasper, former Chief of Staff to the U.S. Secretary of Defense, leads REalloys’ advisory board, working closely with REalloys’ Board Chair, Stephen duMont, president of GM Defense, and seated Board member, General Jack Keane, former Vice Chief of Staff of the U.S. Army.

These are the people who’ve run defense procurement from the inside, the ones who decide who gets qualified, who gets funded, and who actually ends up supplying material into weapons systems.

“This is about building a completely sovereign supply chain from input to finished product, without relying on foreign processing,” Joe Kasper, former Chief of Staff to the U.S. Secretary of Defense and now Chairman of REalloys’ advisory board, told Oilprice.com. “If the U.S. can’t access domestically-processed and manufactured materials, then it does not have a rare earths supply chain at all.”

All Systems Go

REalloys’ Phase One operations are already turning rare earths into alloys in Ohio, amid an ongoing build-out that will launch next year alongside the Pentagon ban on Chinese-origin rare earths. Its plans for Phase Two are a major scale-up.

In Phase One, REalloys intends to move into North American production of high-purity rare earth oxides that can be turned into metals and alloys, using a mix of recycled magnets and mined feedstock. This is the point at which material is produced in the United States and can move through a traceable supply chain. The capital required is about $75 million, and the buildout has $50 million in cash already allocated.

By Phase Two, it will all run through the Ohio facility, where REalloys already converts rare earth oxides into metal and alloy form. The buildout increases throughput and expands the range of material it can process, including heavy rare earths like Dysprosium and Terbium. Feedstock is expected to come from both recycled magnets and upstream feedstock supply agreements, like the one from the Tanbreez project, with the material moving through reduction and alloying in-house before leaving as finished product.

Phase Two will also vertically integrate by adding rare earths magnet production to the pipeline. By 2029, the plan is to add magnet manufacturing in Ohio, closing the full circle from processed material into finished components.

Instead of selling metal and alloys into someone else’s system, REalloys would produce NdFeB magnets itself from its own integrated solution and keep that margin.

This is where the economics takes a major leap forward, and it’s what prompted Clears Street in April to launch coverage of REalloys

Clear Street initiated coverage of REalloys with a Buy rating and a $35 price target, even though the stock was trading just under $8 at the time of the report, because the current valuation does not reflect what the system could look like once it’s running at scale.

The Rare Earths End Game

Rare earths are now facing tightening restrictions on both sides of the Pacific.

And Washington is scrambling to the point of internal divisions over how fast this entire supply chain can be built.

Bloomberg reports that internal disagreements are emerging inside the Trump administration after China’s export restrictions exposed major U.S. vulnerabilities. The argument is over whether the U.S. should rely on market forces to rebuild the rare earth industry or use aggressive state-backed financing and industrial policy similar to the model China used to dominate the sector.

The pressure is now extending well beyond junior mining and processing companies. Large U.S. industrial and defense players like GE Aerospace (NYSE:GE) and LMT (NYSE:LMT) are increasingly exposed to the rare earth supply chain bottleneck as advanced jet engines, missile systems, radar platforms, and aerospace electronics remain heavily dependent on Dysprosium-, Terbium-, and NdFeB-based magnet systems. As Pentagon restrictions tighten ahead of 2027, securing non-Chinese processing and metallization capacity is rapidly becoming a strategic issue across the broader U.S. defense-industrial base.

This is why companies capable of securing even a single strategic link in the non-Chinese rare earth supply chain could become some of the most valuable industrial and defense assets of the next decade.

By. Charles Kennedy

As Washington races to build a rare earth supply chain that can survive the Pentagon’s 2027 ban on Chinese-origin materials, REalloys (NASDAQ: ALOY) has locked in long-term supply from one of the largest known heavy rare earth deposits in the world.

The company announced last Thursday that it has signed a definitive 15-year offtake agreement with Critical Metals Corp. (NASDAQ: CRML) covering 15% of Phase 1 production from the Tanbreez project in southern Greenland, a massive heavy rare earth deposit containing Dysprosium and Terbium, the two most strategically sensitive magnet materials used in fighter aircraft, missile systems, radar platforms, drones, and advanced defense hardware.

REalloys is building one of the only integrated heavy rare earth metallization and magnet production platforms in North America as Washington pushes to break its dependence on Chinese processing capacity before the Pentagon ban takes effect in only seven months.

The company’s Euclid, Ohio, operation focuses on the hardest part of the rare earth supply chain outside China: converting rare earth oxides into defense-grade metals, alloys, and eventually the world’s strongest and most advanced magnet: the NdFeB permanent magnet type used in missile systems, fighter aircraft, radar platforms, robotics, EV drivetrains, and advanced industrial systems.

REalloys says it is scaling that Ohio platform into the largest heavy rare earth metallization facility outside China, supported by a growing network of allied-nation feedstock agreements.

The Tanbreez agreement significantly expands that network.

Under the deal, REalloys will secure 15% of monthly Phase 1 production from the Greenland project for an initial 15-year term.

This is another major announcement for REalloys as the company rushes to stay ahead of major defense deadlines.

The Tanbreez offtake deal follows REalloys strategic partnership with Saskatchewan Research Council, tied to 80% of the output from the Saskatchewan Research Council’s commercial rare earth processing facility. It also adds to the company’s previously secured rights to up to 10% of production from the high-grade Sheep Creek rare earth deposit in Montana, and its control of the Hoidas Lake rare earth asset in Saskatchewan.

GREENLAND IS EMERGING AS A WESTERN RARE EARTH STRONGHOLD

Trump didn’t manage to buy Greenland, but REalloys got its critical minerals.

The strategic importance of the Tanbreez project goes far beyond scale.

The Greenland deposit is one of the largest known heavy rare earth resources globally and one of the few major Western-aligned projects capable of supplying meaningful quantities of Dysprosium and Terbium outside China.

Tanbreez isn’t just another rare earths venue. It’s a heavy rare earth behemoth, while most global deposits focus on less valuable light rare earth production. Critical Metals estimates heavy rare earths account for roughly 27% of the project’s total profile. Most global deposits focused primarily on light rare earth production.

The Greenland project is already fully permitted and advancing under a Western-aligned ownership structure following Greenland's approval of Critical Metals’ acquisition of a controlling 92.5% interest earlier this year.

For REalloys, the deal secures another long-term heavy rare earth materials now central to Pentagon supply chain planning amid a Middle East conflict that is rapidly depleting the arsenal.

Johns Hopkins economists Steve Hanke and Jeffrey Weng told Fortune magazine that the U.S. has already burned through massive portions of its precision weapons inventory across Iran and Ukraine, while remaining dependent on Chinese-controlled rare earth materials to replace them. The economists suggest that Washington has blown through 45% of its Precision Strike Missile inventory just in Iran, and nearly 50% of its THAAD interceptors and 30% of its Tomahawk cruise missiles, among others.

Those systems rely on samarium-cobalt magnets or dysprosium- and terbium-enhanced NdFeB magnets that still flow overwhelmingly through China’s refining and metallization system. The authors estimate that replenishing just four major weapons systems could require between five and ten metric tons of finished defense-grade rare earth magnets, with more than 95% of current supply chains still tied to China.

And that’s the gap REalloys is helping to close, with a North American solution helmed by a leadership lineup that represents the who’s who of American defense.

Joe Kasper, former Chief of Staff to the U.S. Secretary of Defense, leads REalloys’ advisory board, working closely with REalloys’ Board Chair, Stephen duMont, president of GM Defense, and seated Board member, General Jack Keane, former Vice Chief of Staff of the U.S. Army.

These are the people who’ve run defense procurement from the inside, the ones who decide who gets qualified, who gets funded, and who actually ends up supplying material into weapons systems.

“This is about building a completely sovereign supply chain from input to finished product, without relying on foreign processing,” Joe Kasper, former Chief of Staff to the U.S. Secretary of Defense and now Chairman of REalloys’ advisory board, told Oilprice.com. “If the U.S. can’t access domestically-processed and manufactured materials, then it does not have a rare earths supply chain at all.”

All Systems Go

REalloys’ Phase One operations are already turning rare earths into alloys in Ohio, amid an ongoing build-out that will launch next year alongside the Pentagon ban on Chinese-origin rare earths. Its plans for Phase Two are a major scale-up.

In Phase One, REalloys intends to move into North American production of high-purity rare earth oxides that can be turned into metals and alloys, using a mix of recycled magnets and mined feedstock. This is the point at which material is produced in the United States and can move through a traceable supply chain. The capital required is about $75 million, and the buildout has $50 million in cash already allocated.

By Phase Two, it will all run through the Ohio facility, where REalloys already converts rare earth oxides into metal and alloy form. The buildout increases throughput and expands the range of material it can process, including heavy rare earths like Dysprosium and Terbium. Feedstock is expected to come from both recycled magnets and upstream feedstock supply agreements, like the one from the Tanbreez project, with the material moving through reduction and alloying in-house before leaving as finished product.

Phase Two will also vertically integrate by adding rare earths magnet production to the pipeline. By 2029, the plan is to add magnet manufacturing in Ohio, closing the full circle from processed material into finished components.

Instead of selling metal and alloys into someone else’s system, REalloys would produce NdFeB magnets itself from its own integrated solution and keep that margin.

This is where the economics takes a major leap forward, and it’s what prompted Clears Street in April to launch coverage of REalloys

Clear Street initiated coverage of REalloys with a Buy rating and a $35 price target, even though the stock was trading just under $8 at the time of the report, because the current valuation does not reflect what the system could look like once it’s running at scale.

The Rare Earths End Game

Rare earths are now facing tightening restrictions on both sides of the Pacific.

And Washington is scrambling to the point of internal divisions over how fast this entire supply chain can be built.

Bloomberg reports that internal disagreements are emerging inside the Trump administration after China’s export restrictions exposed major U.S. vulnerabilities. The argument is over whether the U.S. should rely on market forces to rebuild the rare earth industry or use aggressive state-backed financing and industrial policy similar to the model China used to dominate the sector.

The pressure is now extending well beyond junior mining and processing companies. Large U.S. industrial and defense players like GE Aerospace (NYSE:GE) and LMT (NYSE:LMT) are increasingly exposed to the rare earth supply chain bottleneck as advanced jet engines, missile systems, radar platforms, and aerospace electronics remain heavily dependent on Dysprosium-, Terbium-, and NdFeB-based magnet systems. As Pentagon restrictions tighten ahead of 2027, securing non-Chinese processing and metallization capacity is rapidly becoming a strategic issue across the broader U.S. defense-industrial base.

This is why companies capable of securing even a single strategic link in the non-Chinese rare earth supply chain could become some of the most valuable industrial and defense assets of the next decade.

By. Charles Kennedy