Aluminum’s war shock blunted by dark transits and Chinese supply

The Iran war caused one of the biggest supply shocks to ever hit the aluminum market, but the runaway price surge that many were bracing for has been blunted by the ingenuity of producers from the Middle East to China.

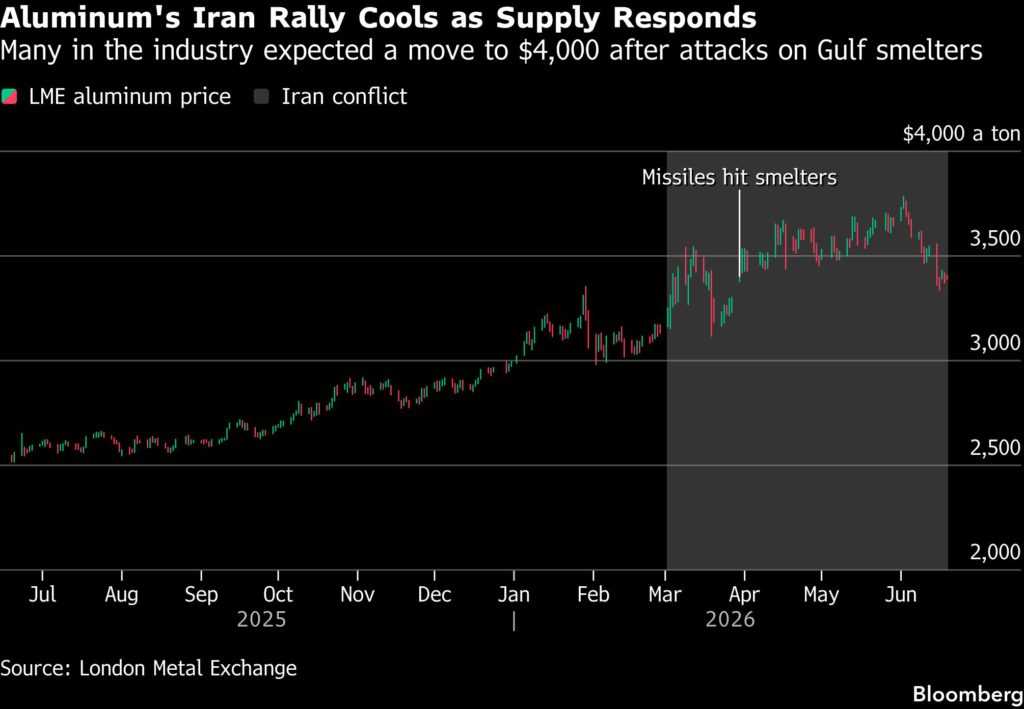

When the conflict began, market watchers warned that unless the Strait of Hormuz reopened quickly, smelters were likely to run out of raw materials within weeks, potentially forcing widespread shutdowns that would plunge the global market into crisis and send prices to record highs above $4,000 a ton.

Those fears escalated dramatically when Iran targeted smelters in the region in missile strikes, and there was broad agreement that aluminum looked set to be one of the worst-hit commodity markets outside of oil and gas.

However, in recent weeks Middle Eastern smelters have carried out a series of complex logistical operations — including daring voyages through the strait — to replenish reserves of alumina and other raw materials, helping to avert widespread closures in a region that accounts for nearly 10% of global supply. And outside the Gulf, smelters in China and Indonesia have been instrumental in keeping the global market in check as buyers wait for exports to rebound.

Now, with analysts, traders and investors staking their bets on where prices are heading next, stark disagreements are emerging on how quickly the market will recover from the squeeze.

“A full-blown physical supply freeze has been averted thanks to a combination of rerouted Middle Eastern alumina imports, rising Chinese exports, and ramping Indonesian production,” said Amelia Xiao Fu, head of commodities strategy at Bank of China International. “While the market managed to survive the last few months by drawing down inventories, these operational buffers have now been decreased.”

Middle Eastern smelters have been forced to make heavy cuts to output, but the clandestine nature of their efforts to shore up their supply chains means the precise scale of the losses is tough to quantify. Meanwhile, a regulatory cap on production in China and power constraints in Indonesia are only adding to the challenge of assessing how quickly supply and demand will rebalance.

Some of the market’s biggest bulls have trimmed their price forecasts in recent days, with JPMorgan Chase & Co. saying that a move to $4,000 a ton is taking longer than expected due to a strong supply response in Asia and an aggressive drawdown in the industry’s hidden inventories.

At the other end of the scale, Goldman Sachs Group Inc. sees prices moving towards $3,000 a ton over the coming year, even after raising forecasts it made at the start of the conflict to reflect a slower rebound in Middle Eastern supplies than anticipated. Futures in London are currently trading around $3,400.

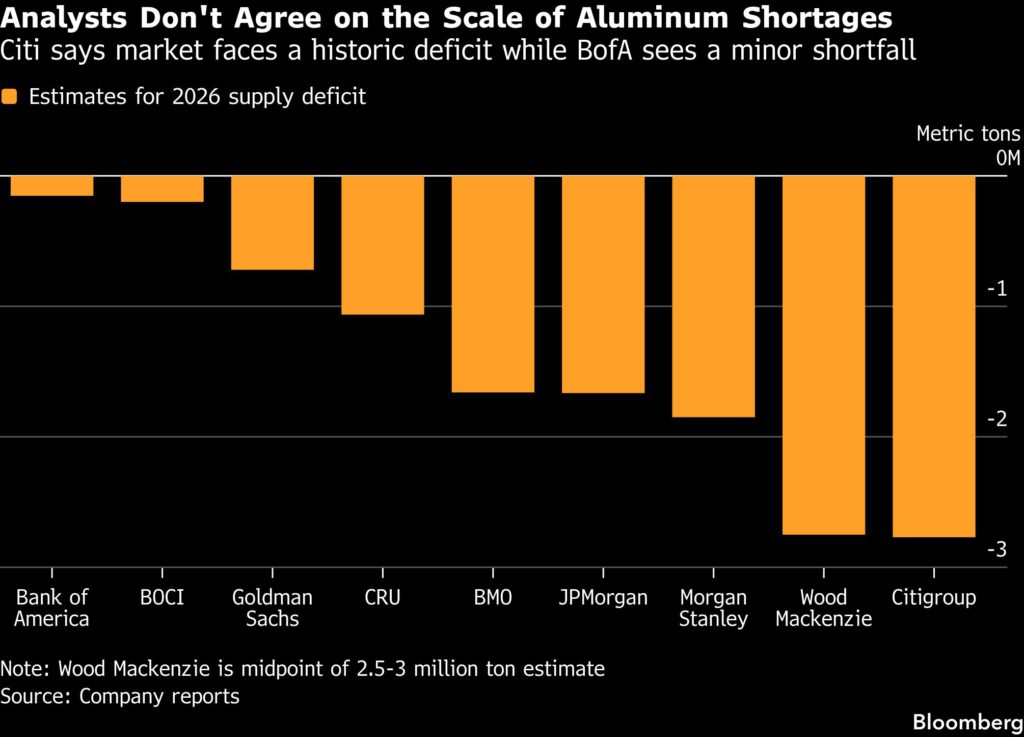

Differences in estimates for aluminum’s underlying supply balance are even starker, with Citigroup Inc. expecting the biggest supply shock in more than 50 years, while Bank of America Corp. expects supply and demand in the 76-million-ton market to be more or less balanced.

Alumina flows

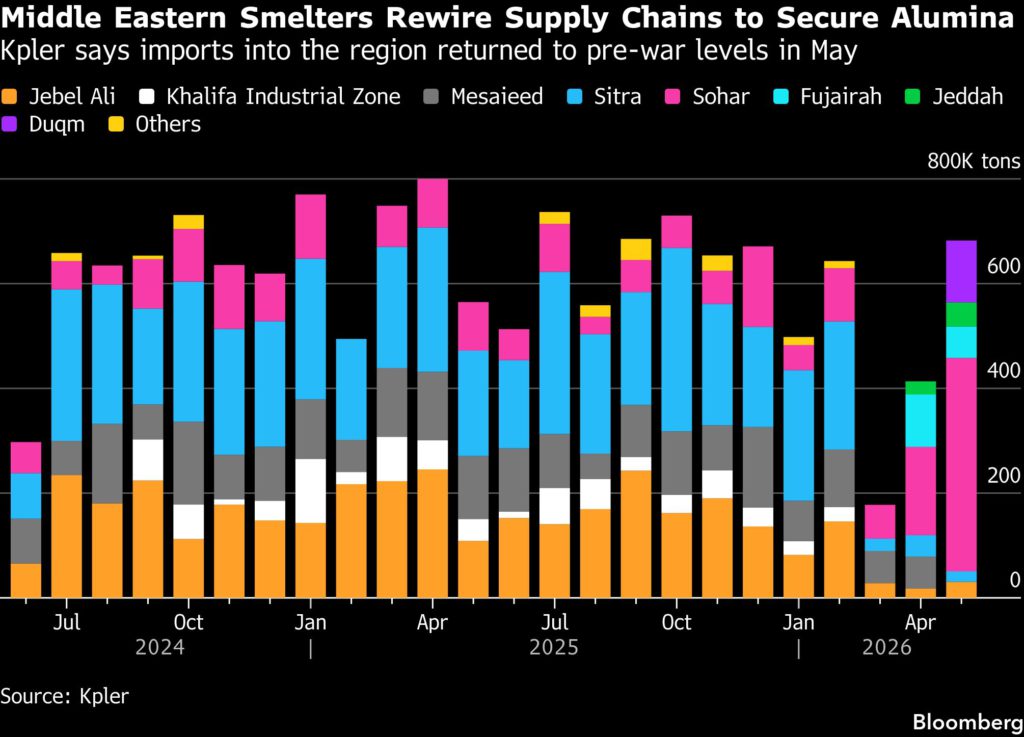

Part of the discrepancy stems from expectations that raw-material shortages have inflicted deeper supply losses on Persian Gulf smelters than they’ve publicly disclosed. But for Ben Ayre, an analyst at ship-tracking firm Kpler, a growing stream of alumina flows into the region signals that, even with Hormuz closed, smelters have made strides in replenishing their reserves.

In recent weeks, a handful of vessels have shown an appetite to move in alumina directly through the strait, switching off their tracking systems to undertake the kind of dark transits that have kept a trickle of oil flowing to global markets through the crisis, according to Kpler’s analysis.

Even greater volumes of alumina have been unloaded in ports in Oman and dispatched to smelters via trucks, in a major test of the region’s logistical capabilities. Thanks to those efforts, imports of the raw material into the Persian Gulf returned to pre-war levels in May, data from the firm show.

“It has resulted in some really novel solutions, and we’ve had to work quite hard to keep up,” Ayre said in an interview. “It’s not unique, but it is somewhat exceptional in terms of its reflection of the value of keeping these operations running.”

Shadow stocks

The challenge in assessing the scale of the supply squeeze doesn’t end in the Gulf, and JPMorgan says the market impact of global shortages has also been blunted by an aggressive drawdown in privately held inventories that are notoriously hard to monitor.

“When we speak with clients there’s a clear sense that it is tight out there, but the first port of call is those invisible stocks,” said Greg Shearer, the bank’s head of base and precious metals research. Still, he believes that it’s only a matter of time before those reserves are depleted and exchange stocks will start being drawn too, driving prices higher. “It’s taking longer than expected, but there are significant deficits that need to be covered.”

China shock

The behavior of Chinese smelters has added another analytical headache. Before the conflict, a bullish mood had swept through the aluminum industry, as smelters in China started to bump up against a regulatory cap on production that looks set to bring a long era of oversupply to an end.

Since the war started, however, official statistics have suggested that Chinese smelters are producing comfortably above that 45-million-ton cap, with April figures pointing to an annualized run-rate of 47 million tons. With exports surging, some analysts are betting that Chinese smelters could solve the global shortage single-handedly if they keep their plants running in overdrive.

In assessing whether they will, analysts need to take a view on how strictly China will enforce the cap, and how far engineers can go in feeding plants with more power than they’re designed to handle. That’s a process that one industry veteran likens to trying to balance an elephant on a finger.

Indonesia wildcard

A final wildcard is a prospective wave of new supply in Indonesia. A surge in Indonesian aluminum exports has sharpened the industry’s focus on its emerging role as a major global supplier, and there’s a growing expectation that producers there will divert scarce power to aluminum plants at the expense of less-profitable nickel operations.

“We always knew there would be capacity additions, but the view up to now was that production would lag because power wasn’t available,” said Amy Gower, head of metals and mining strategy at Morgan Stanley. “We haven’t changed our models yet, but the risk now, with power being reallocated from nickel, is that new supply could come even quicker.”

Taken together, the combination of rebounding Middle Eastern supply, elevated Chinese production and skyrocketing Indonesian output is creating a consensus in the industry that prices will head lower in the long term. But as the US and Iran negotiate a deal to end the war permanently, a debate is still raging about whether the market will face a final squeeze as inventories run dry before the new supply arrives.

“I think if it was going to happen, it would have happened by now,” said Helen Amos, head of commodities research at BMO Capital Markets. “It’s likely that aluminum is past the peak point of the deficit.”

(By Mark Burton and Julian Luk)

Column: Guinea bets bauxite dominance can reshape aluminum supply

The West African country of Guinea has grown to be the world’s largest supplier of bauxite, the raw material ultimately transformed into aluminum.

It’s now looking to use this newfound dominance to exert greater control over both price and industry structure, just as Indonesia has done in nickel and the Democratic Republic of Congo is attempting to do in cobalt.

All three resource giants are struggling to rein in mining sectors that have grown too big too fast, swamping global markets and crashing prices.

Indonesia is using mining quotas, the Congo export quotas, and Guinea looks minded to implement a mix of both as a way of stopping operators exporting more than their mining quotas allow them to produce.

For Conakry, it’s also a chance to emulate Indonesia by capturing more of its resource value by moving from bauxite mining to alumina refining.

Chinese state aluminum producer Chalco’s commitment to a new $1 billion refinery in the country is a sign the strategy is working.

Bauxite boom

Bauxite is the third most abundant element in the Earth’s crust but is mostly too dispersed or too low quality to allow for conversion into alumina.

Guinea not only boasts the world’s largest reserves of metallurgical bauxite but also produces a high-purity product prized for its natural low silica content.

Thanks to heavy Chinese investment, the country overtook Australia as the world’s largest bauxite producer in 2023 and now accounts for around 40% of global output and 70% of the seaborne export market.

Guinea’s exports jumped by 25% year on year to 183 million metric tons in 2025, which unsurprisingly caused prices to slump by almost half over the course of last year and the first part of 2026.

That is why the government is searching for the most effective way of hitting the brakes without generating the sort of market disruption caused by Congo’s cobalt export quota system.

Chinese dependency

China has become increasingly reliant on Guinea for bauxite to feed its huge aluminum production sector.

Imports of Guinean material mushroomed from just 334,000 tons in 2015 to 149 million tons in 2025, by which point they accounted for 74% of all bauxite imports.

China has its own bauxite reserves but they’ve been depleted by decades of mining and are lower quality than those in Guinea.

Moreover, the country has massively expanded its aluminum smelting capacity this century, requiring a similar build-out in alumina refining, far beyond its domestic bauxite mining capacity.

Guinea’s planned crackdown on its runaway bauxite sector has been well flagged, and Chinese buyers have had plenty of time to build precautionary stocks. March imports from Guinea hit a monthly record of 18 million tons.

But there’s little prospect of breaking the dependency, given the scale of the material flow. What will change, however, is the nature of that dependency.

Alumina ambitions

Chalco’s commitment to building the new 1.2-million-ton-per-year alumina refinery shows how seriously China takes the threat to the flow of raw materials.

It’s the first major overseas investment in alumina by China’s state giant. It’s also the third Chinese-backed alumina refinery project to be announced in recent months.

Guinea’s only existing refinery is the Friguia plant, built in the 1960s and owned first by France’s Pechiney, then by US producer Reynolds and since 2008 by Russia’s Rusal. It was out of action between 2012 and 2018 but is operating again, albeit below its 650,000-ton-per-year capacity.

The Conakry government is aiming for five or six more processing plants with a combined capacity of 7 million tons of alumina by 2030.

The seizure of mining assets from Emirates Global Aluminium last year for its failure to follow through on a commitment to refining has served as a stark warning for other operators.

New industry hub

Guinea is following closely in the footsteps of Indonesia, which banned bauxite exports in 2023 as a way of forcing miners to build out processing capacity.

While Indonesia has plenty of coal-fired power to both refine alumina and smelt the intermediate product into aluminum, Guinea doesn’t currently have sufficient energy resources to go beyond the alumina stage.

But if Guinea can successfully implement its strategy, it will turbo-charge the creation of a West African alumina hub.

Not least because other African bauxite producers are travelling the same value-added pathway to keeping more of their mineral revenues.

Nigeria has signed a $1.3 billion investment deal with Africa Finance Corporation (AFC) to build an alumina refinery, while Ghana is looking to do the same under the auspices of the Ghana Integrated Aluminium Development Corporation.

The African shift from mining to first-stage processing could have transformative effects on the aluminum supply chain.

The seaborne bauxite market will shrink. The global alumina export market will expand and China’s domestic alumina refineries will find themselves in competition with their largest raw material supplier.

(The opinions expressed here are those of Andy Home, a columnist for Reuters.)